Packaged Food Products Market Report

RA08397

Packaged Food Products Market by Product (Cheese Sauces & Dips, Jams & Jellies, and Apple Compote), Packaging Type (Cans, Jars, Cups, and Flexibles), Sales Channel (Retails and Food Services), and Regional Analysis (North America, Europe, Asia-Pacific and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022–2030

Global Packaged Food Products Market Analysis

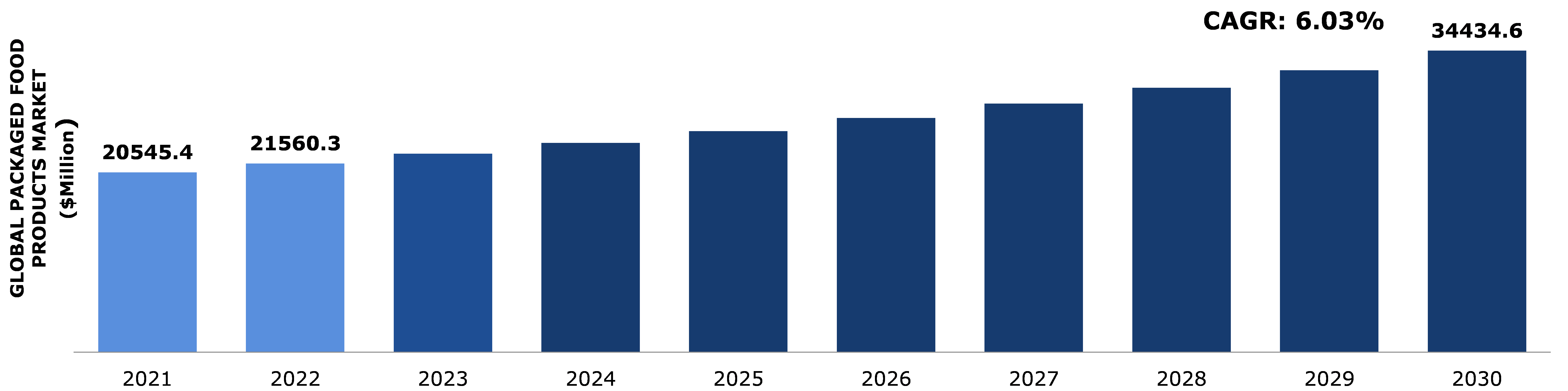

The global packaged food products market size is predicted to garner a revenue of $34,434.6 million in the 2022–2030 timeframe, growing from $20,545.4 million in 2021, at a healthy CAGR of 6.03%.

Market Synopsis

The expansion of the packaged food products market can be attributed to advancements in processing techniques for extending food product shelf life. Furthermore, variations in food consumption patterns brought about by the world's growing working population push market growth. Improvements in retail infrastructure have increased the availability of packaged goods, and this increased ease of acquiring food items, combined with options for free home delivery and various promotional offers, has resulted in the growth of the global packaged food products market. Furthermore, particular customer demands including such organic food, health food ingredients, vegan cuisine, dairy-free goods, and some are expected to open new possibilities for the packaged food products market.

However, consumer perceptions of the negative effects of packaged goods stifle growth and act as a major restraint on the global market.

According to the regional outlook, the Asia-Pacific packaged food products market is expected to create massive growth opportunities for market investors by growing at a CAGR of 6.93% during the review period.

Packaged Food Products Overview

Packaged foods are foods that have been prepared in advance and packed in a way that extends their shelf life. Most packaged food products are industrially produced and distributed for consumption. The idea of packaged food came as a result of factors such as ease of processing, intake, ability to handle, and opposition to external tampering. Packaged foods are easy to handle, prepare, and eat. Because they are highly convenient for city dwellers, they have been getting popular in both developed and emerging nations. Packaged food is a product that is frequently purchased by consumers. As a result, consumer demand for such products remains stable.

Packaged food products include the ready–to-eat and convenient food items like snacks, beverages, chips, frozen vegetables, and more. The demand for packaged food products is increasing at a fast pace due to growing adoption of ready-to-eat and healthy food products among working professionals.

COVID-19 Impact on Packaged Food Products Market

In COVID-19 pandemic, many industries faced major decline and losses due to poor raw supply, decrease in demand & supply, and more. However, packaged food products market saw an unexpected boost during the pandemic situation. This growth is attributed to the increase in the consumption of snacks & beverages, chips, chocolates, and frozen food products during lockdown along with work from home facility for the employees. Due to complete lockdown, people changed their shopping behavior and started buying packaged food products in bulk to stock up their kitchen supplies. This in turn encouraged the companies and the manufacturing units to speed up their production line and maintain the packaged food supply & demand chain.

The COVID-19 pandemic has affected the health of the people adversely throughout the world. People are suffering from many health ailments post coronavirus infections and hence, consumers are preferring ready-to-eat & less time consuming healthy food product alternatives which will enhance their health and immunity. Hence, consumers are shifting their preference towards healthy food snacks. This factor has driven the companies to manufacture healthy food products which are low in calories & fats and high in minerals & vitamin content.

Increased Demand for Ready-to-eat Healthy Food Products to Drive the Packaged Food Products Market in the Forecast Time Period

The predicted time period will see an exponential increase in the number of working people and their hectic time schedules which will drive the packaged food products market. Working people, due to a lack of time, prefer food products that can be prepared with few ingredients and in a short amount of time. This factor has increased demand for ready-to-eat food products such as frozen food, bakery items, snacks, chocolates, and other items. Furthermore, increased urbanization has resulted in a high urbanization rate, which has positively impacted the growth of the packaged food products market due to increased packaged food demand. Aside from that, consumer preference for healthy food and beverage alternatives will accelerate market growth.

Consumers are now demanding food products which are made up of natural components and contain less preservatives. To ensure this, the packaged food manufacturing companies are now focusing on the production of healthy organic based food products. For instance, Just in time, JOI, UK based company, introduced in April, 2021, its first zero waste plant milk product which is made with only one ingredient which is sustainable source, organic, and gluten free oats packed in a compostable pouch.

Furthermore, packaged food products market is also being driven by the rising trend of health and sustainability among well-informed consumers. Globally, consumers are becoming more aware of food source and sustainability, and as a result, they are becoming more selective about the source of protein they consume, increasing demand for plant-based packaged food products. Therefore, all such aspects and developments are projected to gain traction for packaged food products.

To know more about global packaged food products market trends, get in touch with our analysts here.

Risk of Contamination of Food Products due to Packaging Materials to Restrain the Market Growth

High risk of contamination of food because of packaging material is the main restraining factor for the packaged food products market. Plastic is a widely used packaging material in the food industry as it is light weight and can be carried easily anywhere while travelling, but it is made of chemicals that can easily react with preservatives & antioxidants and thus contaminates the food. For instance, according to an article published in the South Wale Arugs, on May 2, 2021, the supermarkets in the U.K. issued warnings to consumers over the health risk on consuming items they have purchased in stores including Tesco, Morrisons, Asda, Sainsbury's, and Aldi. Packaged food products at the stores like chocolates, dates, and other were contaminated with salmonella bacteria responsible for causing food allergies.

Technological Advancements to Increase the Opportunities in the Packaged Food Products Market

Inclination of the millennials towards healthy packaged food alternatives has opened many opportunities for companies of the packaged food products market. Consumers prefer healthy food products with rich nutritional value, low cholesterol, less preservatives, and low fat. Thus, due to the high demand for the healthy food, many beverage industries have started manufacturing organic and non-alcoholic juices to target health oriented customers. This factor will contribute to the growth of the market in the forecast time. For instance, according to a news published in Nutritional Outlook, on April 28, 2021, New Jersey based Diana Food introduced an organic cultured celery powder to its Food Protection Platform for natural meat curing.

Furthermore, majority of the leading brands are shifting to flexible packaging to provide multiple environmental benefits. Flexible packaging takes advantage of the best qualities of paper, aluminum, or plastic materials without sacrificing overall food quality. It is versatile and increases food shelf life, which is why flexible films are replacing traditional packaging materials in the market. Aside from that, the packaged food products market is heavily focused on sustainability and intelligent packaging. The staggering rise in consumer awareness, combined with frequent discussions about individual responsibilities to the environment has pushed brands away from traditional packaging. Whereas working to improve shelf appeal is still important, manufacturers are also focusing on cutting-edge new tech. Some are even incorporating intelligent packaging and nanotechnology to provide maximum convenience to customers. Some of them are employing "smart materials," which react to the external environment and alert users to the condition of the product within. Thus, such factors create an opportunity to gain major pull in the coming years for packaged food products market.

To know more about global packaged food products market opportunities, get in touch with our analysts here.

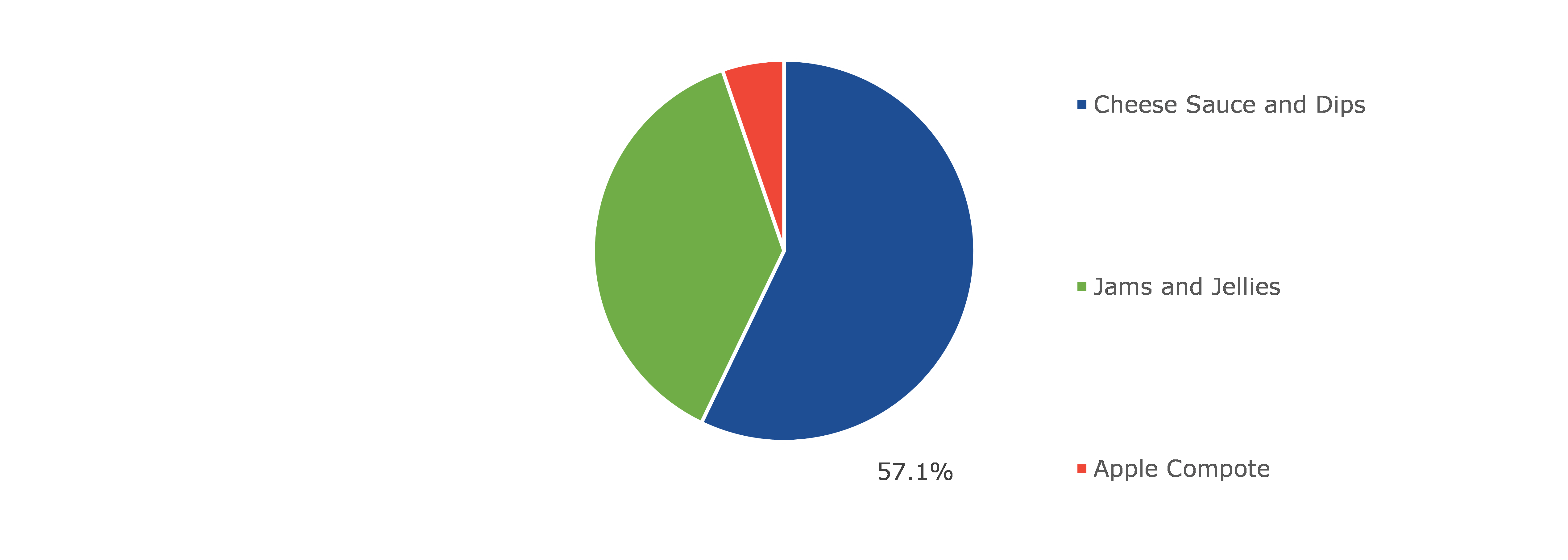

Global Packaged Food Products Market, by Product

Based on product, the packaged food products market has been segmented into cheese sauce & dips, jams & jellies, and apple compote. Cheese sauce & dips sub-segment is projected to generate the maximum revenue and show the fastest growth.

Global Packaged Food Products Market Share, By Product, 2021

Source: Research Dive Analysis

In 2030, the global cheese sauce & dips packaged food products sub-segment will be worth more than $22,056.8 million. This increase owes to factors such as more consumption of cheese sauce & dips in European countries. Also, rising demand for fast foods like pizzas, burgers, tacos, and more will accelerate the market growth as these fast foods use cheese sauce as a dressing. Massive expansion of pizza & burger fast food outlets, combined with an expanding confection & bakery market has increased global demand for cheese sauce & dips. These trends have attracted a number of well-established global suppliers, making this same cheese sauce industry extremely competitive. All such factors are expected to promote the adoption of cheese sauce & dips packaged food products growth during the forecast period.

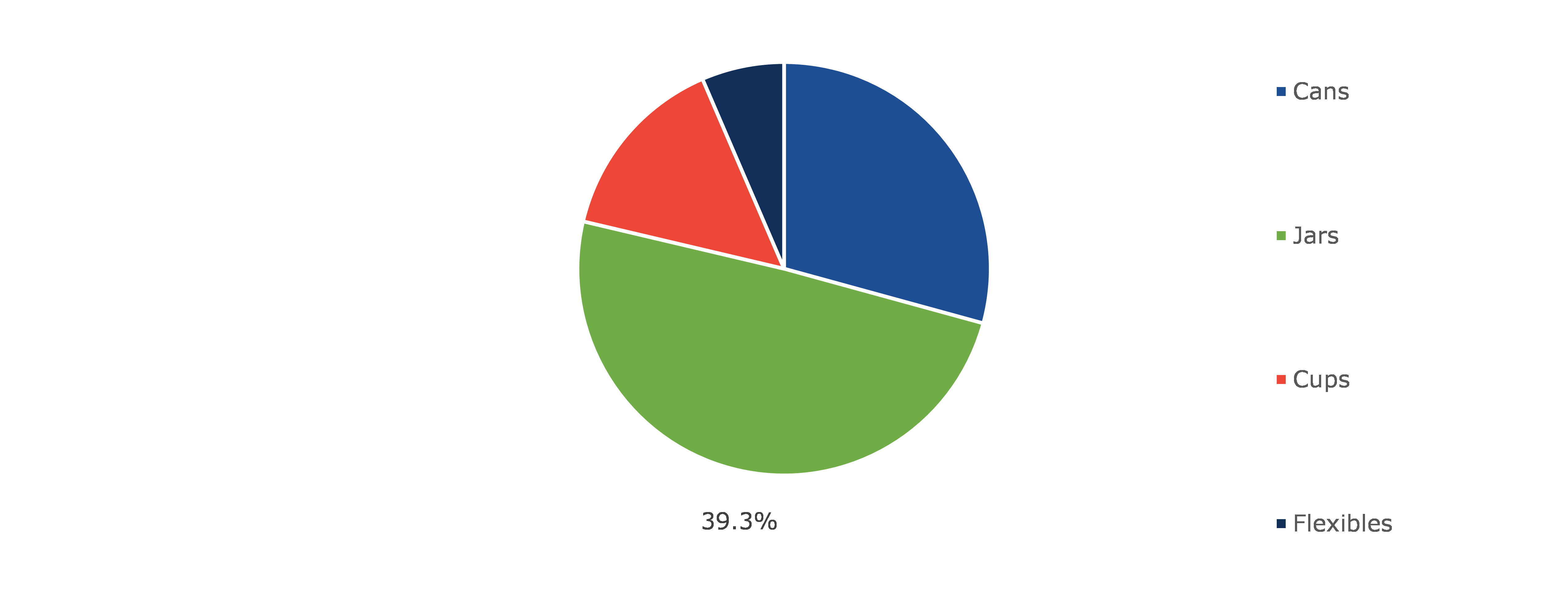

Global Packaged Food Products Market, by Packaging Type

Based on packaging type, the packaged food products market is segmented into cans, jars, cups, and flexibles. Jars sub-segment is projected to generate the maximum revenue whereas cups sub-segment is predicted to show the fastest growth in the forecast period.

Global Packaged Food Products Market Share, By Packaging Type, 2021

Source: Research Dive Analysis

In 2030, the global jars sub-segment will be worth more than $16,882.1 million. This growth is due to many benefits of glass jars such as their non-corrosive nature and high physical appeal. Also, jars made up of glass increase the shelf life of the food by providing extra protection to food from outside environment, maintain flavors, texture, & aroma of the food, provide visual delight to the consumers, and prevent food contamination. Wide end use applications and market penetration of appealing packaging jars are some of the major factors driving packaged food products market. All such factors are expected to promote the adoption of packaged food products growth during the forecast period.

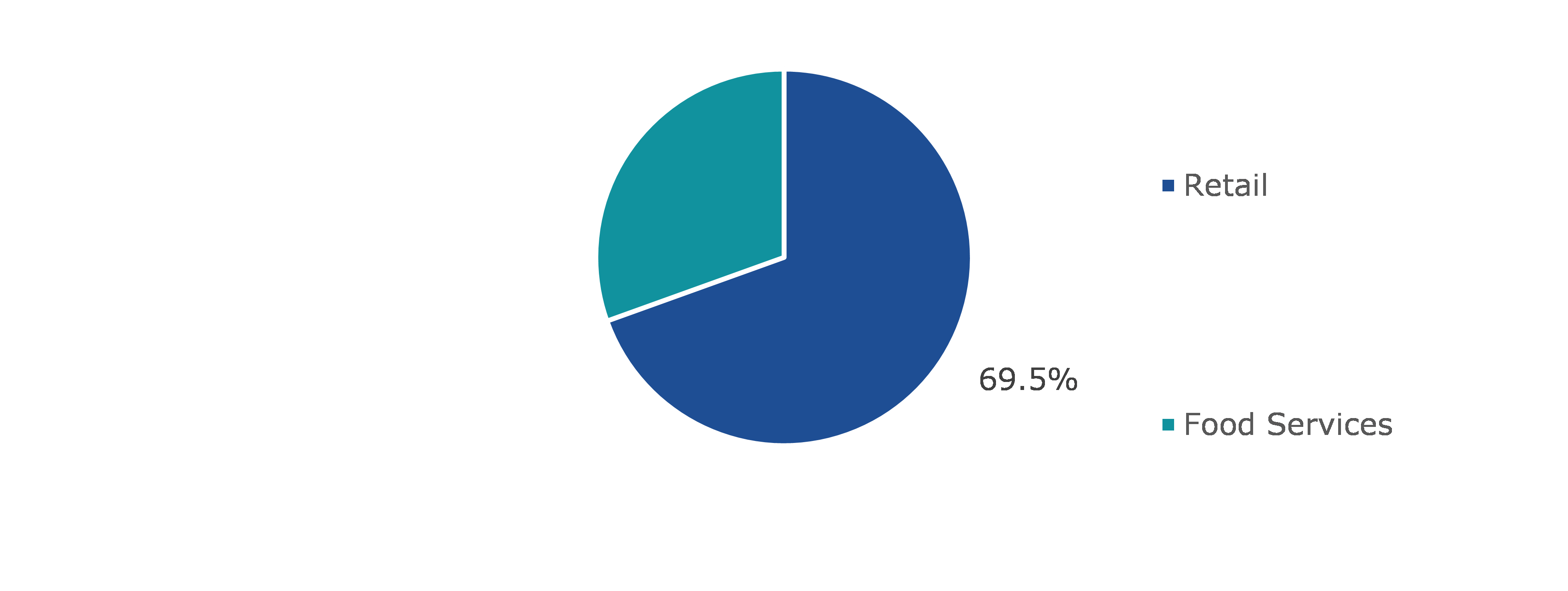

Global Packaged Food Products Market, by Sales Channel

Based on sales channel, the packaged food products market is segmented into retail and food services. Retail sub-segment is projected to generate the maximum revenue whereas food services sub-segment is predicted to show the fastest growth in the forecast period.

Global Packaged Food Products Market Share, By Sales Channel, 2021

Source: Research Dive Analysis

In 2030, the global retail sub-segment will be worth more than $23,156.6 million. This sub-segment growth is attributed to increasing trend of purchasing packaged food products from the retail and convenience stores among the consumers. Moreover, the retail shops offer opportunity to the customers to hand pick the products of their choices without going to other places for food products. The concept of food products & convenience has grown rapidly in India and China. People are becoming more aware of the benefits of organized retailing. One of the reasons a consumer visits the retail is for the physical experience. Shopping malls will see an increase in customers as more people get vaccinated. All such factors are expected to promote the growth of sub-segment during the forecast period.

Global Packaged Food Products Market, Regional Insights:

The packaged food products market was inspected across North America, Europe, Asia-Pacific, and LAMEA.

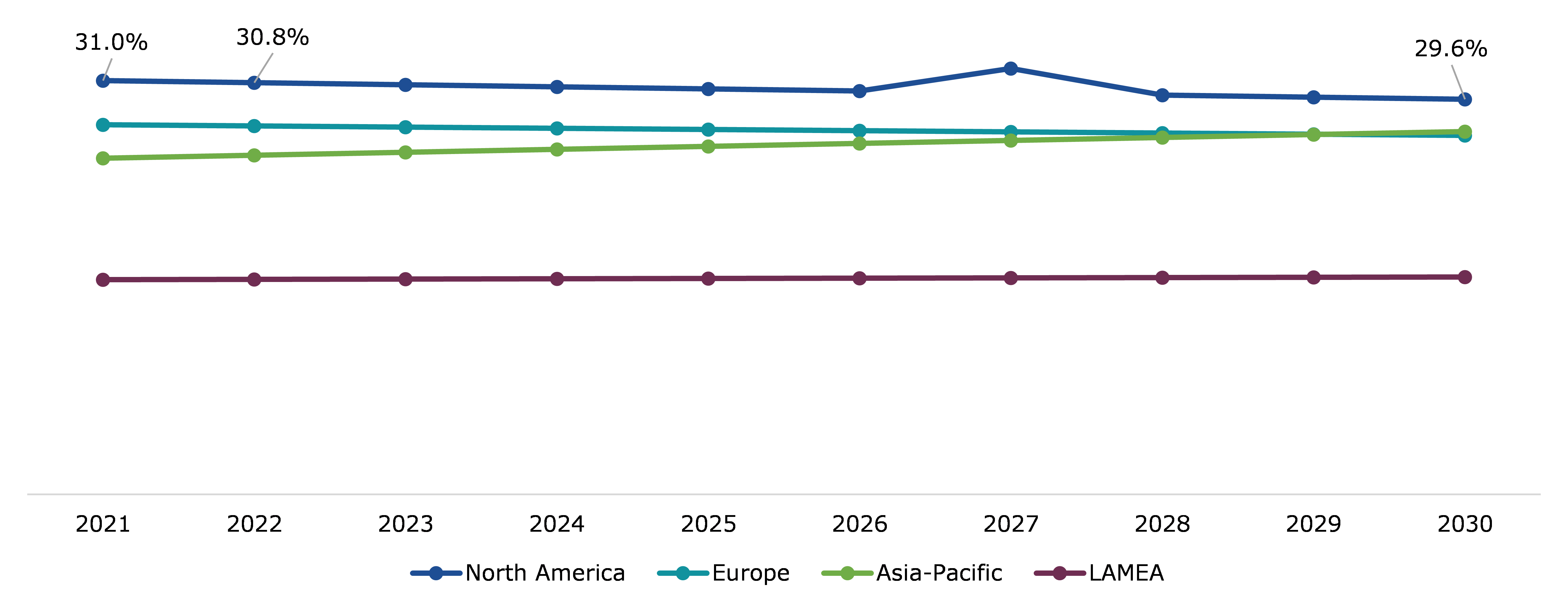

Global Packaged Food Products Market Size & Forecast, By Region, 2021-2030 (USD Million)

Source: Research Dive Analysis

The Market for Packaged Food Products in North America to Hold the Maximum Revenue

North America packaged food products market is anticipated to generate maximum revenue during the forecast time period and reach $10,192.6 million by 2030, with a CAGR of 5.48%. This growth is due to the hectic work life of consumers in the region and their growing preference for ready-to-eat food and convenience. In addition, increasing innovations in food packaging, organic based food products, bold flavors, and healthy ingredients are further expected to contribute to the growth of the packaged food products market in next few years. Rising global health concerns, as well as changing lifestyles and dietary patterns have increased demand for a variety of snacking options. The rising replacement of snacks for meals and the growing preference for vegan & allergen-free snack foods are going to fuel the packaged food products industry. Global companies have heavily invested in the growing demands for snacks by packaging their products in the more convenient extending shelf life and promoting snack intake on the go. For instance, Kwik Lok Corp., in the U.S., provides its Eco-Lok closing packaging solution, which allows customers to reclose the same package and utilize the treats later. Creative food products, various packaging solutions, and busy lifestyles are expected to aid industry growth. All such factors are expected to drive the North America packaged food products market and witness noticeable growth.

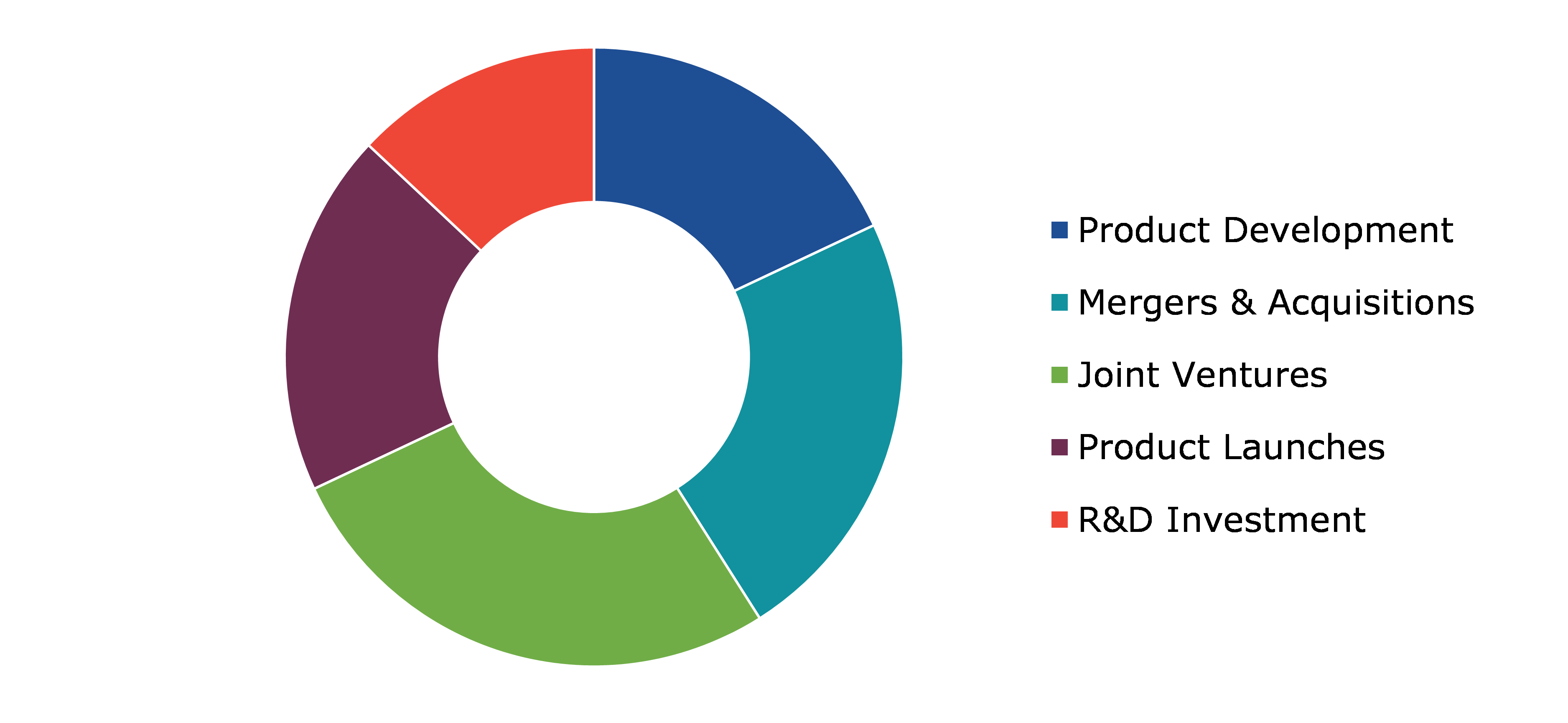

Competitive Scenario in the Global Packaged Food Products Market

Product launches and mergers & acquisitions are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading packaged food products market players are B and G Foods, INC., Andros Foods, Histon Sweets Spreads Limited, The J.M. Smucker Co., Gehl Foods, LLC. Conagra Brands, Tree Top, and Kraft Heinz.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2030 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product |

|

| Segmentation by Packaging Type |

|

| Segmentation by Sales Channel |

|

| Key Companies Profiled |

|

Q1. What is the size of the packaged food products market?

A. The packaged food products market is predicted to generate $ 49,685.2 million in the 2020-2027 timeframe, growing from $ 30,830.0 million in 2019 at a healthy CAGR of 6.3%.

Q2. Which are the major companies in the packaged food products market?

A. B and G Foods, INC. and Andros Foods are some of the prominent companies in the packaged food products market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia packaged food products market?

A. The share of Asia market is anticipated to grow at a CAGR of 9.5%.

Q5. What are the strategies opted by the leading players in this market?

A. New product development and strategic partnerships are the key strategies opted by the operating companies in this market.

Q6. Which industries are expected to drive the growth of the packaged food products market in the next 5 years?

A. Retail industry is expected to drive the growth of the packaged food products market in the next 5 years.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global packaged food products market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on packaged food products market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Packaged Food Products Market, by Product

5.1.Overview

5.1.1.Market size and forecast, by Enterprise Size

5.2.Cheese Sauce and Dips

5.2.1.Key market trends, growth factors, and opportunities

5.2.2.Market size and forecast, by region, 2022-2030

5.2.3.Market share analysis, by country 2022 & 2030

5.3.Jams and Jellies

5.3.1.Key market trends, growth factors, and opportunities

5.3.2.Market size and forecast, by region, 2022-2030

5.3.3.Market share analysis, by country 2022 & 2030

5.4.Apple Compote

5.4.1.Key market trends, growth factors, and opportunities

5.4.2.Market size and forecast, by region, 2022-2030

5.4.3.Market share analysis, by country 2022 & 2030

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness

5.5.2.Competition heatmap

6.Packaged Food Products Market, by Packaging Type

6.1.Overview

6.1.1.Market size and forecast, by Sales Channel

6.2.Cans

6.2.1.Key market trends, growth factors, and opportunities

6.2.2.Market size and forecast, by region, 2022-2030

6.2.3.Market share analysis, by country 2022 & 2030

6.3.Jars

6.3.1.Key market trends, growth factors, and opportunities

6.3.2.Market size and forecast, by region, 2022-2030

6.3.3.Market share analysis, by country 2022 & 2030

6.4.Cups

6.4.1.Key market trends, growth factors, and opportunities

6.4.2.Market size and forecast, by region, 2022-2030

6.4.3.Market share analysis, by country 2022 & 2030

6.5.Flexibles

6.5.1.Key market trends, growth factors, and opportunities

6.5.2.Market size and forecast, by region, 2022-2030

6.5.3.Market share analysis, by country 2022 & 2030

6.6.Research Dive Exclusive Insights

6.6.1.Market attractiveness

6.6.2.Competition heatmap

7.Packaged Food Products Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Product

7.1.1.2.Market size analysis, by Packaging Type

7.1.1.3.Market size analysis, by Sale Channel

7.1.2.Canada

7.1.2.1.Market size analysis, by Product

7.1.2.2.Market size analysis, by Packaging Type

7.1.2.3.Market size analysis, by Sale Channel

7.1.3.Mexico

7.1.3.1.Market size analysis, by Product

7.1.3.2.Market size analysis, by Packaging Type

7.1.3.3.Market size analysis, by Sale Channel

7.1.4.Research Dive Exclusive Insights

7.1.4.1.Market attractiveness

7.1.4.2.Competition heatmap

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Product

7.2.1.2.Market size analysis, by Packaging Type

7.2.1.3.Market size analysis, by Sale Channel

7.2.2.UK

7.2.2.1.Market size analysis, by Product

7.2.2.2.Market size analysis, by Packaging Type

7.2.2.3.Market size analysis, by Sale Channel

7.2.3.France

7.2.3.1.Market size analysis, by Product

7.2.3.2.Market size analysis, by Packaging Type

7.2.3.3.Market size analysis, by Sale Channel

7.2.4.Spain

7.2.4.1.Market size analysis, by Product

7.2.4.2.Market size analysis, by Packaging Type

7.2.4.3.Market size analysis, by Sale Channel

7.2.5.Italy

7.2.5.1.Market size analysis, by Product

7.2.5.2.Market size analysis, by Packaging Type

7.2.5.3.Market size analysis, by Sale Channel

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Product

7.2.6.2.Market size analysis, by Packaging Type

7.2.6.3.Market size analysis, by Sale Channel

7.2.7.Research Dive Exclusive Insights

7.2.7.1.Market attractiveness

7.2.7.2.Competition heatmap

7.3.Asia Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Product

7.3.1.2.Market size analysis, by Packaging Type

7.3.1.3.Market size analysis, by Sale Channel

7.3.2.Japan

7.3.2.1.Market size analysis, by Product

7.3.2.2.Market size analysis, by Packaging Type

7.3.2.3.Market size analysis, by Sale Channel

7.3.3.India

7.3.3.1.Market size analysis, by Product

7.3.3.2.Market size analysis, by Packaging Type

7.3.3.3.Market size analysis, by Sale Channel

7.3.4.Australia

7.3.4.1.Market size analysis, by Product

7.3.4.2.Market size analysis, by Packaging Type

7.3.4.3.Market size analysis, by Sale Channel

7.3.5.South Korea

7.3.5.1.Market size analysis, by Product

7.3.5.2.Market size analysis, by Packaging Type

7.3.5.3.Market size analysis, by Sale Channel

7.3.6.Rest of Asia Pacific

7.3.6.1.Market size analysis, by Product

7.3.6.2.Market size analysis, by Packaging Type

7.3.6.3.Market size analysis, by Sale Channel

7.3.7.Research Dive Exclusive Insights

7.3.7.1.Market attractiveness

7.3.7.2.Competition heatmap

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Product

7.4.1.2.Market size analysis, by Packaging Type

7.4.1.3.Market size analysis, by Sale Channel

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Product

7.4.2.2.Market size analysis, by Packaging Type

7.4.2.3.Market size analysis, by Sale Channel

7.4.3.UAE

7.4.3.1.Market size analysis, by Product

7.4.3.2.Market size analysis, by Packaging Type

7.4.3.3.Market size analysis, by Sale Channel

7.4.4.South Africa

7.4.4.1.Market size analysis, by Product

7.4.4.2.Market size analysis, by Packaging Type

7.4.4.3.Market size analysis, by Sale Channel

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Type

7.4.5.2.Market size analysis, by Enterprise Size

7.4.6.Research Dive Exclusive Insights

7.4.6.1.Market attractiveness

7.4.6.2.Competition heatmap

8.Competitive Landscape

8.1.Top winning strategies, 2021

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2021

9.Company Profiles

9.1.B and G Foods, INC.

9.1.1.Overview

9.1.2.Business segments

9.1.3.Type portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.Andros Foods

9.2.1.Overview

9.2.2.Business segments

9.2.3.Type portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.Histon Sweets Spreads Limited

9.3.1.Overview

9.3.2.Business segments

9.3.3.Type portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4.The J.M. Smucker Co.

9.4.1.Overview

9.4.2.Business segments

9.4.3.Type portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.Gehl Foods, LLC.

9.5.1.Overview

9.5.2.Business segments

9.5.3.Type portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.Conagra Brands

9.6.1.Overview

9.6.2.Business segments

9.6.3.Type portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.Tree Top

9.7.1.Overview

9.7.2.Business segments

9.7.3.Type portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.Kraft Heinz

9.8.1.Overview

9.8.2.Business segments

9.8.3.Type portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

10.Appendix

10.1.Parent & peer market analysis

10.2.Premium insights from industry experts

10.3.Related reports

Urban consumers, usually having a hectic lifestyle, are in search of food products that can be made in limited time, with minimum efforts. They prefer meal options that are easier, quick, and non-fussy; this propelled the demand for packaged foods, which can also be stated as convenience foods, that are ready-to-cook, ready-to-serve, ready-to-eat, and frozen foods. Packaged food products may include products ranging from beverages, frozen vegetables, snacks, chips, ready-to-eat products, and others.

Why is the Demand for Packaged Food Products Increasing?

The demand for packaged food items is growing rapidly these days owing to growing time-constraints among working professionals and rising availability of convenience food products in the market. Moreover, packaged food products provide better physical protection, barrier protection, containment or accumulation, advertising, detailed information about the ingredients, safety, suitability, and more. The demand is shifting towards packaged foods or ready-to-eat foods because of the bulging time-constraints owing to work shifts of a majority of consumers, especially women. This is eventually boosting the packaged food products market growth.

In addition, growing technological developments in packing and ultrasonic sealing assure that packaged foods do not contaminate and leak outside the packaging. Moreover, packaging trends, for instance: worldwide environmental concerns about packaging materials and use of environment-friendly and sustainable packaging materials are helping brands grab consumers’ attention, which is propelling the market growth further.

Latest Trends in the Packaged Food Products Market

As per a report by Research Dive, the global packaged food products market is expected to grow from $20,545.4 million in 2021 to $34,434.6 million by 2030. The packaged food products market in North America is the most dominant and anticipated to grow speedily with a CAGR of 5.48% from 2022 to 2030. This is mainly owing to the rising improvements in food packing and growing launch of packed organic food products in this region. The region is deliberated as the most rewarding market for the packaged food products, due to increase in busy work schedules of people and their rising preference for ready-to-eat and convenience foods.

Market players are profoundly investing in research and development to satisfy the mounting demand for packaged food products. Some of the prominent players of the packaged food products market are Andros Foods, Kraft Heinz, Histon Sweets Spreads Limited, The J.M. Smucker Co., Gehl Foods, LLC. Conagra Brands, B and G Foods, INC., Tree Top, and others. These players are focused on forming strategies, for example, mergers and acquisitions, partnerships, novel developments, and collaborations to achieve a prominent position in the global market.

For instance,

- In December 2020, Nestle, the world's leading food & beverage company, launched a series of FreshlyFit ready-to-eat meals for consumers that prefer healthy eating and wish to adopt active lifestyles.

- In January 2021, The Taste Company, a food start-up, entered into the ‘ready-to-eat’ food industry. The company aims to focus on manufacturing ready-to-eat breakfast as well as Indian meals menu.

- In December 2021, Food Flavours, a Kochi-based start-up, introduced box-packed wellness diet products including variants of whole-wheat ready-to-cook chapatis with finger millet, moringa leaves, spinach, flaxseeds, and foxtail millet.

COVID-19 Impact on the Packaged Food Products Market

The unexpected rise of the COVID-19 pandemic in 2020 has skyrocketed the growth of the global packaged food products market. This is mainly because many restaurants and cafes were forced to shut down during the lockdown. However, people preferred ordering food from outside, and packaged food products were the only savior during the tough times in the course of the pandemic period. Also, the work-from-home working model has resulted in a speedy change in consumer culture and consumption habits. This has turned out as a rewarding opportunity for the convenience food product makers. All these factors portray that the global packaged food products market is likely to have a promising future in the upcoming years.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com