Digital Educational Publishing Market Report

RA08354

Digital Educational Publishing Market by End User (K-12, Higher Education, and Corporate or Skill Based), Product Type (Digital Textbooks, Digital Assessment Books, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022–2031

Digital Educational Publishing Market Analysis

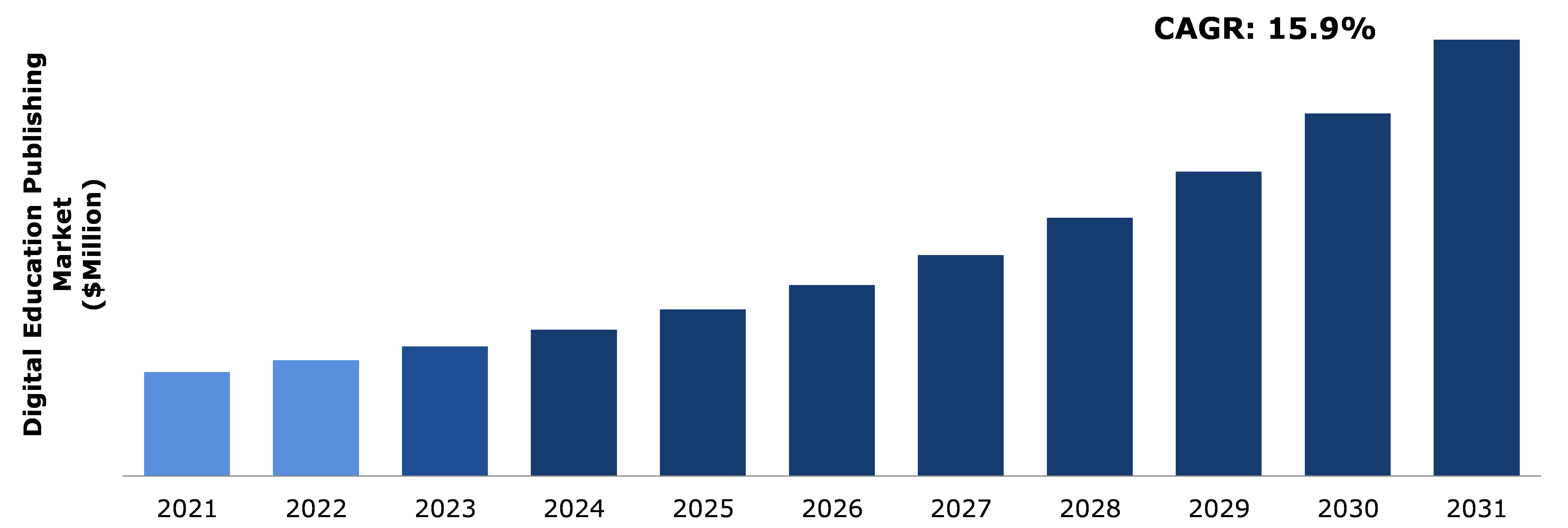

The Global Digital Educational Publishing Market Size was $9,878.9 million in 2021 and is predicted to grow with a CAGR of 15.9%, by generating a revenue of $41,498.9 million by 2031.

Global Digital Educational Publishing Market Synopsis

The increased global usage of smartphone devices is one of the key factors fueling the growth of the digital educational publishing market. Consumer reading interests are gradually switching from conventional print media toward device-compatible forms such as smartphones. It enables many of the world's major educational content providers to deliver a varied selection of digital material that can be accessed via internet-enabled smartphone devices such as mobile phones and tablets. Many nations are adopting various steps to promote the use of digital technology in education. Furthermore, multiple institutes' attempts to provide remote learning facilities are projected to boost the expansion of the digital education publishing market during the forecast period.

The arrival of massively open online courses, the availability of free-source platforms such as Mozilla Firefox, Google Chrome, Apache HTTP server, and others may provide a threat to the rise of the digital educational publishing market. Additionally, digital and mobile material must apply more severe security and content quality criteria. These issues may hinder the expansion of the digital educational publishing market.

Governments across the globe are undertaking a number of projects to boost the usage of digital technology in the education sector. The approach was mostly focused with the employment of digital technology devices in educational institutions as well as the development of digital literacy and capabilities in students. Similarly, emerging nations such as China and India are supporting the use of technology-enabled education through a range of programs.

In May 2020, Blinkist, a Berlin-based micro learning software company, teamed up with Monte Carlo, Inc., an American data reality platform, to get more trustworthy data via data observability. Monte Carlo, a data platform, enables automatic monitoring and intelligent alerts that allowed Blinkist data engineers to focus on innovation and product and recover up to 120 hours each week.

Digital Educational Publishing Overview

Digital educational publishing is the use of digital media to advertise educational content. The content is accessible on multiple pages and is suitable for many devices, such as computers, cellphones, desktops, and tablets. The books given by digital education are referred to as e-books, which allow students access to particular license fees. E-books are alternatives to printed books, as they involve a lesser printing expense.

COVID-19 Impact on Global Digital Educational Publishing Market

The coronavirus pandemic has unleashed a sequence of unprecedented occurrences affecting every industry. With the continued spread of the new coronavirus pandemic, companies across the globe are gradually flattening their recessionary curve by leveraging technology. Many businesses will go through response, recuperation, and refresh phases. Building business resilience and enabling agility will enable firms to go forward in their journey out of the COVID-19 issue. The digital educational publishing industry would experience a positive influence during the forecast period owing to the widespread proliferation of the COVID-19 pandemic. Due to the influence of COVID-19, the shut-down of educational institutions has resulted in the substitution of schools and colleges with online learning. As a result, the global digital learning and publishing markets are expanding rapidly. For instance, in August 2018, Cengage Learning Holdings II Inc. unveiled a new subscription plan called Cengage Unlimited. It gave full access to more than 675 courses and 20,000 digital volumes in 70 disciplines at a cost of USD 119.99 per semester. The Cengage Unlimited subscription model attracted many educational institutions, such as the University of Missouri, Liberty University, and Ultimate Medical Academy, between August and November 2018.

Rapid Penetration of Smartphones to be an Important Factor for the Growth the Market

The primary reason driving the growth of the digital educational publishing market is the rise in adoption of smartphone devices internationally. The preferences of consumers for reading are gradually changing from conventional print forms to device-compatible formats as smartphones. It enables several top educational content providers to deliver a wide selection of digital content that can be accessed through internet-enabled smartphone devices such as mobile phones and tablets. Many nations are taking various initiatives to allow increased use of digital technology in the education sector. Furthermore, initiatives by different institutes to give remote learning facilities are projected to promote the growth of the digital education publishing market during the forecast period.

Open-source Platforms may Affect the Growth of the Market

Availability of open-source platforms like Mozilla Firefox, Google Chrome, Apache HTTP Server, and others, with the emergence of massively open online courses, can be a challenge for the expansion of digital educational publishing sector. Furthermore, digital and mobile content must adhere to stricter security and quality standards. These challenges can impede the growth of the digital educational publishing market. Several poor countries do not have stable internet access and electrical supplies. To finish the course, online students need to have a good internet connection to surf the content online or download the content.

Government Initiatives are Creating Major Investment Opportunities

Governments throughout the world are implementing different steps to promote the penetration of digital technology in the education sector. For instance, in 2018, the European Commission published the Digital Education Action Plan for the promotion of digital competence in the education sector in the EU member nations. The strategy largely focused on the deployment of digital technology devices in educational institutions and the development of digital literacy and skills in students. Similarly, emerging nations such as China and India are supporting the use of technology-enabled education through various programs. Many such government assistance programs are helping the growth of the global digital educational publishing business. Such activities by government agencies are offering substantial investment possibilities.

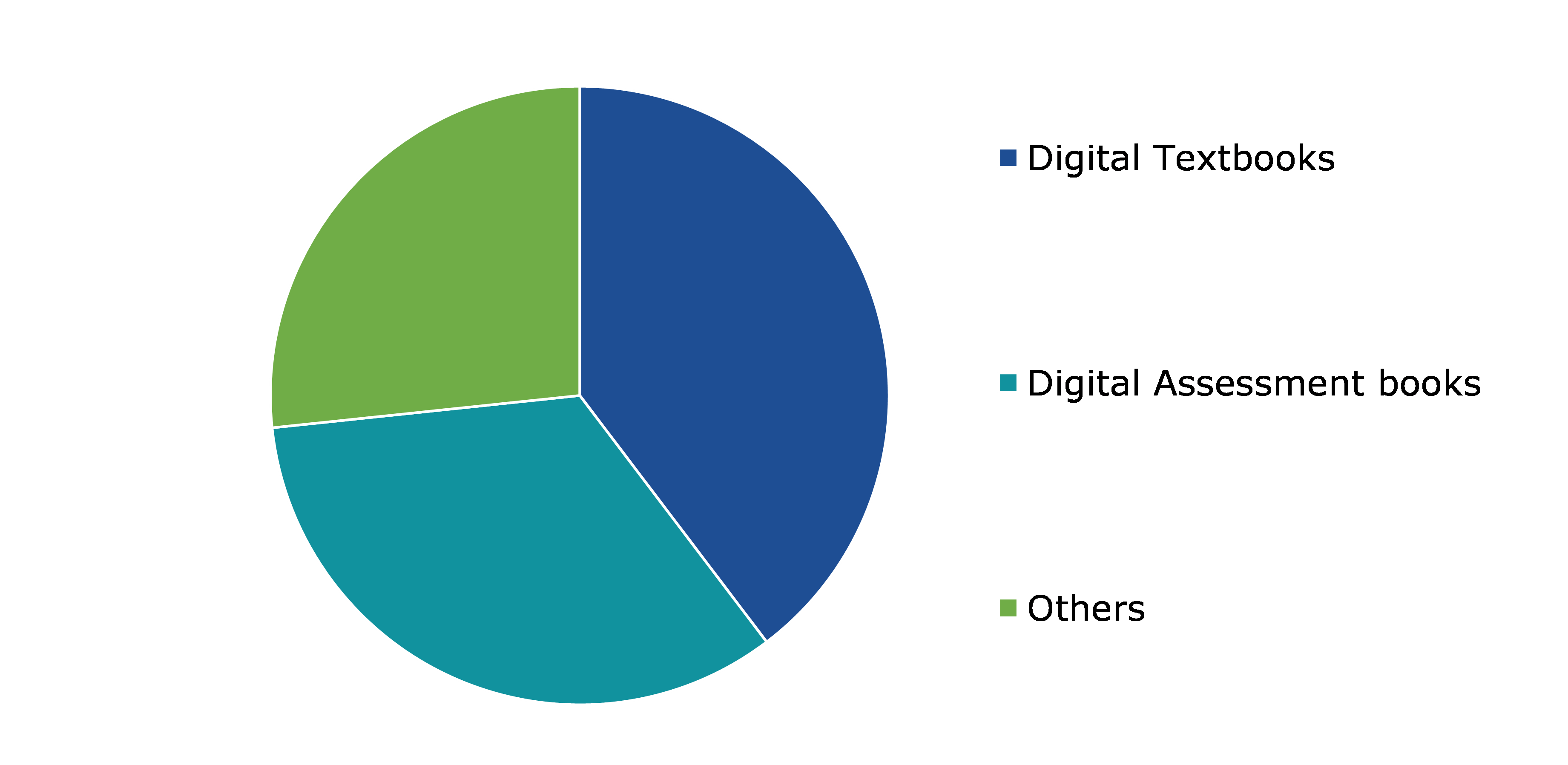

Global Digital Educational Publishing Market, by Product Type

On the basis of product type, digital educational publishing market is segmented into digital textbooks, digital assessment books, and others. Among these, digital textbooks sub-segment is anticipated to hold the largest share of the global market revenue. Furthermore, digital assessment books sub-segment is expected to be the fastest growing sub-segment.

Global Digital Educational Publishing Market Size, by Product Type, 2021

Source: Research Dive Analysis

Digital textbooks sub-segment is expected to hold a significant share in the forecast period. The digital textbooks sub-segment was the highest contributor to the market. Digital textbooks may offer lower prices, make it easier to assess student progress, and are easier and less expensive to update as needed. Open-source e-textbooks may offer the chance to develop free, editable textbooks for fundamental topics, or allow individual teachers the opportunity to create e-texts for their own courses. This may enable improved access to excellent literature in developing countries.

Digital assessment books sub-segment is anticipated to be the fastest growing during the forecast period. With the ongoing digital trend, students and institutions prefer online modes of assessment. Through digital assessment, students may take the test from anywhere and at any time, based on the restrictions specified by the institution or the teacher. Furthermore, online test systems can incorporate multimedia, such as movies or recordings, in the examination itself. These reasons are fueling the expansion of the digital assessment sub-segment.

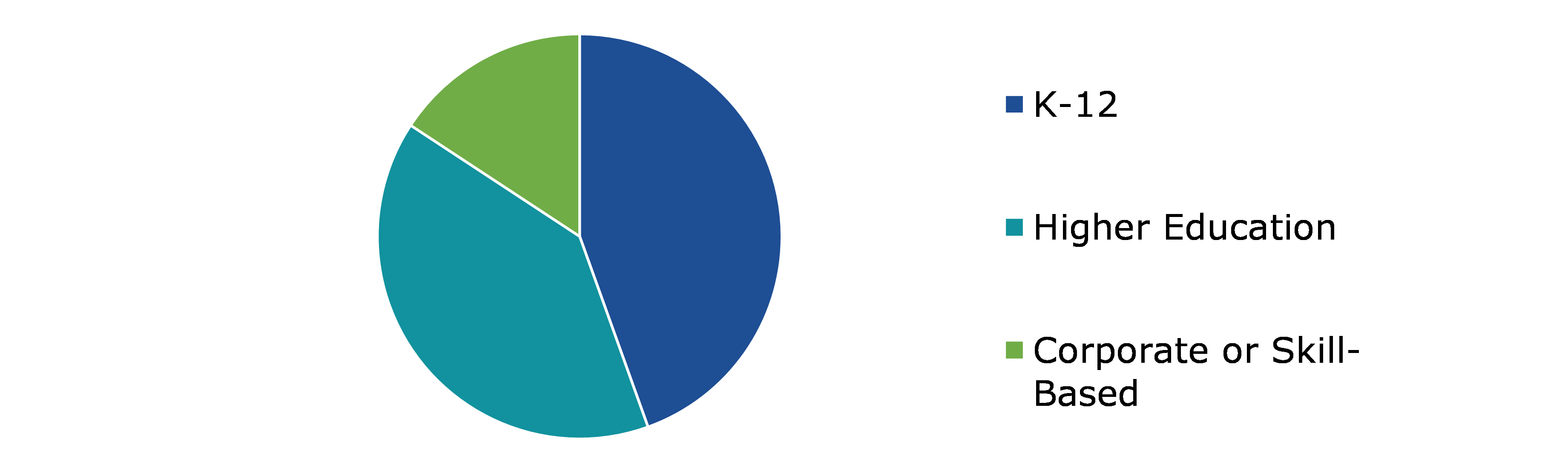

Global Digital Educational Publishing Market, by End-user Industry

On the basis of end user, digital educational publishing market is segmented into K-12, higher education, and corporate or skill-based. Among these, K-12 sub-segment is anticipated to hold the largest share of the global market revenue. Furthermore, higher education sub-segment is expected to be the fastest growing sub-segment.

Global Digital Educational Publishing Market Share, by End-user Industry, 2021

Source: Research Dive Analysis

The K-12 sub-segment was the highest contributor to the market. The K-12 education market is driven by schools shifting from the traditional blackboard approach to integrating smart technology into learning environments. In addition to stressing 21st-century capabilities, K-12 schools began to emphasize the significance of life skills and social-emotional learning. These significant trends in the K-12 subsegment are likely to contribute to the revenue increase.

The higher education sub-segment is anticipated to be the fastest growing sub-segment. Several higher education institutes are incorporating intercultural and international components into education due to the increased need to recruit the best students and staff, improve the quality of education, and earn cash. Furthermore, the increase in tertiary enrollments internationally has led to a rise in the necessity for internationalization. The globalization of teaching and research is one of the key development strategies followed by numerous higher education schools. Factors such as the rise in the use of modern technology, and the constant development of new products and solutions for higher education will have a significant influence on the expansion of the higher education.

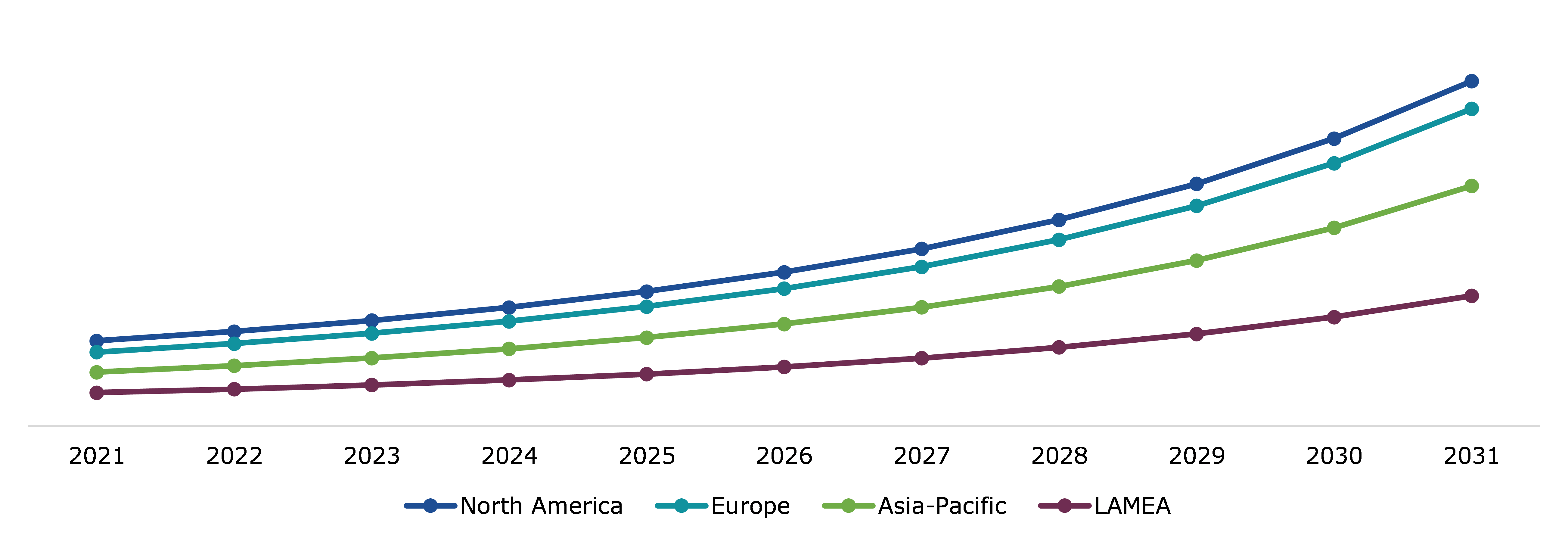

Global Digital Educational Publishing Market, Regional Insights

The digital educational publishing market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Digital Educational Publishing Market Size & Forecast, by Region, 2021 (USD Million)

Source: Research Dive Analysis

The Market for Digital Educational Publishing in North America to be the Most Dominant

North America was the highest revenue contributor. The market in North America is set to dominate the global digital educational publishing market in terms of value, and this trend is projected to sustain itself throughout the assessment period. North America’s digital educational publishing market is the most appealing, increasing at a strong CAGR during the projection period. Increase in online communications combined with a rise in work-from-home structures throughout North America have led to an increased need for digital publishing and are anticipated to boost the region market in the forecast years.

The Market for Digital Educational Publishing in Asia-Pacific to be the Fastest Growing

Asia-Pacific is the fastest-growing region. Rise in smartphone adoption in emerging economies such as China and India is boosting the Asia-Pacific market. Additionally, the lower smartphone pricing owing to greater competition among manufacturers and service providers is further predicted to boost the client base and consequently benefit the digital educational publishing business.

Competitive Scenario in the Global Digital Educational Publishing Market

Product launches and mergers & acquisitions are common strategies followed by major markets. For instance, in September 2020, Coursera partnered with Salesforce and SV Academy to launch a new entry-level SDR Professional Certificate. By integrating content from Salesforce’s online learning platform, Trailhead, the program would prepare learners for a career in sales development.

Source: Research Dive Analysis

Some of the significant digital educational publishing market players are Scholastic Corp., McGraw-Hill Education Inc., Georg von Holtzbrinck, Hachette Livre, Pearson, Cambridge University Press, Cengage Learning, John Wiley & Sons, Oxford University Press, and Thomson Reuters.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product Type |

|

| Segmentation by End User |

|

| Key Companies Profiled |

|

Q1. What is the size of the global digital educational publishing market?

A. The global digital educational publishing market was valued at $9,878.9 million in 2021 and is projected to reach $41,498.9 million by 2031, at a CAGR of 15.9%.

Q2. Which are the major companies in the digital educational publishing market?

A. Scholastic Corp., McGraw-Hill Education Inc., and Georg von Holtzbrinck are some of the key players in the global digital educational publishing market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific digital educational publishing market?

A. The Asia-Pacific mobile value-added services market was valued at $2,159.5 million in 2021 and is estimated to reach $9,652.6 million by 2031, with a CAGR of 16.6%.

Q5. What are the strategies opted for by the leading players in this market?

A. Technological development and strategic partnerships are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more in R&D practices?

A. Pearson, Cambridge University Press, and Cengage Learning are investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Digital Educational Publishing market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Digital Educational Publishing market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Digital Educational Publishing Market Analysis, by End User

5.1.Overview

5.2.K-12

5.2.1.Definition, key trends, growth factors, and opportunities, 2021-2030

5.2.2.Market size analysis, by region, 2021-2030

5.2.3.Market share analysis, by country, 2021-2030

5.3.Higher Education

5.3.1.Definition, key trends, growth factors, and opportunities, 2021-2030

5.3.2.Market size analysis, by region, 2021-2030

5.3.3.Market share analysis, by country, 2021-2030

5.4.Corporate or Skill Based

5.4.1.Definition, key trends, growth factors, and opportunities, 2021-2030

5.4.2.Market size analysis, by region, 2021-2030

5.4.3.Market share analysis, by country, 2021-2030

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness, 2021-2030

5.5.2.Competition heatmap, 2021-2030

6.Digital Educational Publishing Market Analysis, by Product Type

6.1.Digital Textbooks

6.1.1.Definition, key trends, growth factors, and opportunities, 2021-2030

6.1.2.Market size analysis, by region, 2021-2030

6.1.3.Market share analysis, by country, 2021-2030

6.2.Digital Assessment Books

6.2.1.Definition, key trends, growth factors, and opportunities, 2021-2030

6.2.2.Market size analysis, by region, 2021-2030

6.2.3.Market share analysis, by country, 2021-2030

6.3.Others

6.3.1.Definition, key trends, growth factors, and opportunities, 2021-2030

6.3.2.Market size analysis, by region, 2021-2030

6.3.3.Market share analysis, by country, 2021-2030

6.4.Research Dive Exclusive Insights

6.4.1.Market attractiveness, 2021-2030

6.4.2.Competition heatmap, 2021-2030

7.Digital Educational Publishing Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Product, 2021-2030

7.1.1.2.Market size analysis, by End-user, 2021-2030

7.1.2.Canada

7.1.2.1.Market size analysis, by Product, 2021-2030

7.1.2.2.Market size analysis, by End-user, 2021-2030

7.1.3.Mexico

7.1.3.1.Market size analysis, by Product, 2021-2030

7.1.3.2.Market size analysis, by End-user, 2021-2030

7.1.4.Research Dive Exclusive Insights

7.1.4.1.Market attractiveness, 2021-2030

7.1.4.2.Competition heatmap, 2021-2030

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Product, 2021-2030

7.2.1.2.Market size analysis, by End-user, 2021-2030

7.2.2.UK

7.2.2.1.Market size analysis, by Product, 2021-2030

7.2.2.2.Market size analysis, by End-user, 2021-2030

7.2.3.France

7.2.3.1.Market size analysis, by Product, 2021-2030

7.2.3.2.Market size analysis, by End-user, 2021-2030

7.2.4.Spain

7.2.4.1.Market size analysis, by Product, 2021-2030

7.2.4.2.Market size analysis, by End-user, 2021-2030

7.2.5.Italy

7.2.5.1.Market size analysis, by Product, 2021-2030

7.2.5.2.Market size analysis, by End-user, 2021-2030

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Product, 2021-2030

7.2.6.2.Market size analysis, by End-user, 2021-2030

7.2.7.Research Dive Exclusive Insights

7.2.7.1.Market attractiveness, 2021-2030

7.2.7.2.Competition heatmap, 2021-2030

7.3.Asia Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Product, 2021-2030

7.3.1.2.Market size analysis, by End-user, 2021-2030

7.3.2.Japan

7.3.2.1.Market size analysis, by Product, 2021-2030

7.3.2.2.Market size analysis, by End-user, 2021-2030

7.3.3.India

7.3.3.1.Market size analysis, by Product, 2021-2030

7.3.3.2.Market size analysis, by End-user, 2021-2030

7.3.4.Australia

7.3.4.1.Market size analysis, by Product, 2021-2030

7.3.4.2.Market size analysis, by End-user, 2021-2030

7.3.5.South Korea

7.3.5.1.Market size analysis, by Product, 2021-2030

7.3.5.2.Market size analysis, by End-user, 2021-2030

7.3.6.Rest of Asia Pacific

7.3.6.1.Market size analysis, by Product, 2021-2030

7.3.6.2.Market size analysis, by End-user, 2021-2030

7.3.7.Research Dive Exclusive Insights

7.3.7.1.Market attractiveness, 2021-2030

7.3.7.2.Competition heatmap, 2021-2030

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Product, 2021-2030

7.4.1.2.Market size analysis, by End-user, 2021-2030

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Product, 2021-2030

7.4.2.2.Market size analysis, by End-user, 2021-2030

7.4.3.UAE

7.4.3.1.Market size analysis, by Product, 2021-2030

7.4.3.2.Market size analysis, by End-user, 2021-2030

7.4.4.South Africa

7.4.4.1.Market size analysis, by Product, 2021-2030

7.4.4.2.Market size analysis, by End-user, 2021-2030

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Product, 2021-2030

7.4.5.2.Market size analysis, by End-user, 2021-2030

7.4.6.Research Dive Exclusive Insights

7.4.6.1.Market attractiveness, 2021-2030

7.4.6.2.Competition heatmap, 2021-2030

8.Competitive Landscape

8.1.Top winning strategies, 2021

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2021

9.Company Profiles

9.1. Scholastic Corp.

9.1.1.Overview

9.1.2.Business segments

9.1.3.Product portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.McGraw-Hill Education Inc

9.2.1.Overview

9.2.2.Business segments

9.2.3.Product portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.Georg von Holtzbrinck

9.3.1.Overview

9.3.2.Business segments

9.3.3.Product portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4. Hachette Livre

9.4.1.Overview

9.4.2.Business segments

9.4.3.Product portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.Pearson

9.5.1.Overview

9.5.2.Business segments

9.5.3.Product portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.Cambridge University Press

9.6.1.Overview

9.6.2.Business segments

9.6.3.Product portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.Cengage Learning

9.7.1.Overview

9.7.2.Business segments

9.7.3.Product portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.John Wiley & Sons

9.8.1.Overview

9.8.2.Business segments

9.8.3.Product portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

9.9.Oxford University Press

9.9.1.Overview

9.9.2.Business segments

9.9.3.Product portfolio

9.9.4.Financial performance

9.9.5.Recent developments

9.9.6.SWOT analysis

9.10.Thomson Reuters

9.10.1.Overview

9.10.2.Business segments

9.10.3.Product portfolio

9.10.4.Financial performance

9.10.5.Recent developments

9.10.6.SWOT analysis

10.Appendix

10.1.Parent & peer market analysis

10.2.Premium insights from industry experts

10.3.Related reports

In today’s world, education is absolutely essential for both personal and professional development. It provides people with the skills, knowledge, and critical thinking capabilities that are necessary for success in numerous aspects of life. Additionally, there is a rising need for digital learning, which is now more common and significant. This is where digital educational publishing solutions come in.

The digital educational publishing market refers to a sector that creates and distributes educational content in digital format. The information is available on several sites and is appropriate for a variety of gadgets, such as tablets, desktops, cellphones, and computers. E-books, which offer learners access to certain license costs, are provided through digital education. E-books are an alternative to printed books because they require less money for production.

Recent Trends in the Digital Educational Publishing Market

The digital educational publishing market is continuously evolving with new technologies and trends. Adaptive learning technology has gained popularity in the digital educational publishing sector. Adaptive learning systems combine artificial intelligence and data analytics to personalize the learning experience for each student. These systems assess students' performance and offer suggestions and content that are customized to their individual requirements and rate of learning. Additionally, publishers utilized learning analytics and data analytics to acquire insights into learner performance and engagement. By examining data acquired from digital platforms, educators and publishers may identify areas for development, customize learning experiences, and track student progress.

Newest Insights in the Digital Educational Publishing Market

As per a report by Research Dive, the global digital educational publishing market is expected to grow at a CAGR of 15.9% and generate revenue of $41,498.9 million by 2031. The primary factors driving the growth of the market are the growing use of smartphones globally and efforts by many institutions to offer remote learning options. However, the accessibility of open-source platforms and the fact that numerous developing countries lack stable electricity and internet connections are expected to hinder market growth.

The digital educational publishing market in North America is expected to remain dominant in the coming years. The region's high revenue in 2021 was driven by increasing online communication coupled with an expansion in work-from-home structures in this region, which has resulted in an increasing need for digital publishing. This has led to a rising demand for online educational tools and content.

How are Market Players Responding to the Rising Demand for Digital Educational Publishing?

Market players are responding to the rising demand for digital educational publishing by investing in research and development to create more unique and interactive digital teaching materials. They are also growing their digital distribution platforms and collaborating with educational institutions to provide comprehensive digital solutions.

In addition, market players are increasingly focusing on strategic partnerships and collaborations with other players in the industry to leverage their strengths and expand their reach. Some of the foremost players in the digital educational publishing market are McGraw-Hill Education Inc., Scholastic Corp., Hachette Livre, Georg von Holtzbrinck, Pearson, Cengage Learning, Cambridge University Press, John Wiley & Sons, Thomson Reuters, Oxford University Press, and others. These players are focused on implementing strategies such as mergers and acquisitions, novel developments, collaborations, and partnerships to reach a leading position in the global market.

For instance:

- In May 2020, Top Hat, the most popular active learning platform in higher education, announced that the company purchased more than 400 volumes of textbooks for higher education from Nelson, the largest educational publisher in Canada. Top Hat transformed these print-only textbooks into digital courseware on its platform and infused them with interactive aspects, allowing instructors to bring active learning to life for their students.

- In September 2020, Coursera, a U.S.-based company offering massive open online courses, announced two new entry-level professional certifications in collaboration with SV Academy, Salesforce, and IBM. The certifications do not require any specialized education or professional experience, making them available to students from all backgrounds.

- In July 2021, Byju's, an innovative educational technology platform founded in India, purchased Epic, a digital reading platform for kids aged 12 and under located in the US, to enhance Byju's strategy for increasing its presence in the US and overcoming the learning gap among students there.

COVID-19 Impact on the Global Digital Educational Publishing Market

The COVID-19 pandemic had a positive impact on the global digital educational publishing market. As the new coronavirus pandemic continues to grow, businesses all over the world are steadily flattening their recessionary curve by utilizing digital technology. Many firms went through recovery, response, and refresh phases. Building organizational resilience and promoting adaptability helped businesses to overcome the Covid-19 problem. Moreover, due to COVID-19's influence, schools and colleges replaced online learning as a result of the closure of educational institutions. In turn, this led to a rapid expansion of the global markets for digital publishing and learning. These factors are projected to fuel the digital educational publishing market growth amidst the pandemic.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com