EVA Solar Films Market Report

RA09233

EVA Solar Films Market by Type (Normal EVA Films, Anti-PID EVA Films, and Others), Application (Thin-film Solar Cells, Crystalline Solar cells, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

EVA Solar Films Overview

Ethylene Vinyl Acetate (EVA) solar films play a crucial role in the photovoltaic industry, serving as a key component in the encapsulation of solar cells. These films are a type of polymer sheet made from the copolymerization of ethylene and vinyl acetate. EVA solar films are transparent, flexible, and possess excellent adhesion properties, making them ideal for lamination purposes in solar panel manufacturing. In addition, the introduction of EVA solar films reformed the solar energy sector by enhancing the durability & performance of solar modules.

Moreover, the transparent nature of EVA solar films ensures optimal light transmission, a critical factor in maximizing energy conversion efficiency. When employed as encapsulants, these films act as protective shields for solar cells, safeguarding them against environmental elements such as moisture and UV radiation. This dual functionality not only extends the lifespan of solar panels but also maintains the modules' optical clarity, allowing for the efficient capture of sunlight for energy conversion. The blend of ethylene and vinyl acetate grants EVA solar films a unique combination of attributes. Their flexibility facilitates easy integration into the solar panel manufacturing process, conforming to varying shapes and sizes. Simultaneously, the films' excellent adhesion properties contribute to the overall structural integrity of the solar modules.

Global EVA Solar Films Market Analysis

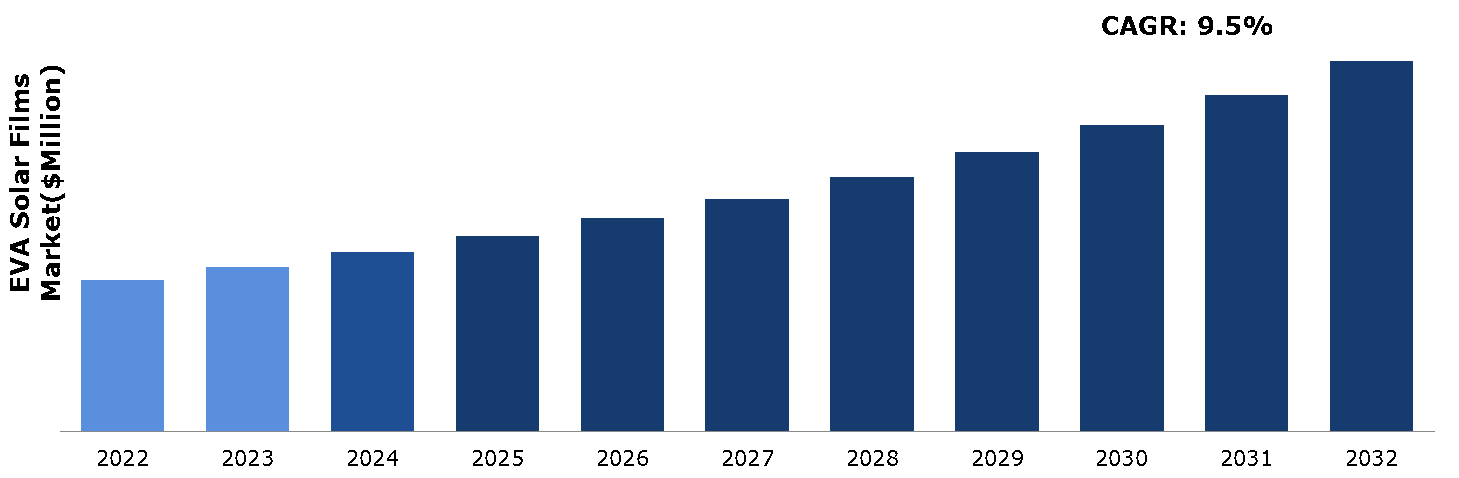

The global EVA solar films market size was $3,168.2 million in 2022 and is predicted to grow with a CAGR of 9.5%, by generating a revenue of $7,771.0 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global EVA Solar Films Market

The global EVA solar films market has undergone significant transformations in the wake of the COVID-19 pandemic. The pandemic's impact on the solar industry, coupled with global disruptions in supply chains and economic downturns, has left an indelible mark on the EVA solar films market. As countries grappled with lockdowns and restrictions, the solar energy sector faced challenges in project execution, manufacturing delays, and logistical hurdles, directly influencing the demand for EVA solar films. Despite the initial setbacks, the EVA solar films market displayed resilience and adaptability. The urgent need for sustainable energy solutions and an increasing focus on renewable sources remained pivotal drivers for the market recovery. Governments worldwide continued to emphasize clean energy initiatives, providing stimulus packages and incentives to bolster solar projects. This strategic support played a crucial role in mitigating the adverse effects of the pandemic on the EVA solar films market.

The EVA solar films adaptability and efficiency have positioned them as integral components in photovoltaic modules. The films enhance the durability, performance, and longevity of solar panels, contributing to the overall efficiency of solar energy systems. This critical role in the solar energy value chain has ensured a steady rebound for the EVA solar films market on a global scale post pandemic.

Increasing Installation of Solar Panels to Drive the Market Growth

The escalating adoption of solar panels is poised to drive a significant surge in demand for solar films. As the global focus intensifies on sustainable & renewable energy sources, solar power has emerged as a key player in meeting these demands. Moreover, the installation of solar panels has witnessed a notable surge, fueled by both environmental consciousness and governmental initiatives promoting clean energy. Furthermore, EVA solar films, a critical component in photovoltaic modules, play a pivotal role in enhancing the efficiency & longevity of solar panels. It acts as encapsulants, serving to protect the sensitive photovoltaic cells within solar panels from environmental factors such as moisture, dust, and mechanical stress. Their unique properties, including light transmittance and strong adhesion, contribute to the robust performance of solar modules. These films effectively bond the various layers of a solar panel, ensuring durability & reliability under diverse weather conditions. Further, rise in demand for EVA solar films is amplified by the growing solar energy market, which is witnessing increased investments & advancements in technology. The films provide a protective barrier and contribute to the overall performance of solar panels by facilitating light transmission, a crucial factor in optimizing energy conversion. As governments worldwide continue to promote solar energy as a sustainable solution, the installation of solar panels across residential, commercial, and industrial sectors is expected to soar, thereby propelling the growth of the EVA solar films market.

High Price of EVA Solar Films to Restrain the Market Growth

However, the soaring costs associated with EVA solar films pose a significant barrier to the growth trajectory of the EVA solar films market. In addition, EVA solar films, a crucial component in the photovoltaic module manufacturing process, have witnessed a surge in prices that may potentially hinder the expansion of the solar film market. As a key element in solar module encapsulation, EVA films play a vital role in ensuring the durability & performance of solar panels. Moreover, the escalating prices of these films pose challenges for manufacturers and stakeholders in the solar energy sector. In markets such as solar energy, where cost-effectiveness is pivotal for widespread adoption, the high price of EVA solar films potentially hinders the attainment of ambitious renewable energy targets. Stakeholders, including solar panel manufacturers and project developers, face challenges in maintaining competitive pricing and achieving desirable returns on investment. Addressing the issue of the high price of EVA solar films requires a multifaceted approach. Innovations in manufacturing processes, cost-effective sourcing of raw materials, and advancements in technology could contribute to mitigating the cost challenges faced by the EVA solar films market.

Escalating Adoption in Architectural Applications and The Automotive Industry to Drive Excellent Opportunities

On the other hand, the EVA solar films market is expected to experience a surge in popularity, particularly in architectural applications and the automotive industry. In addition, this growing traction is poised to significantly propel the expansion of the EVA solar films market. In architectural applications, EVA solar films serve as a pivotal component in solar photovoltaic (PV) modules, contributing to the harnessing of solar energy for sustainable power generation. Moreover, the architectural sector embraces EVA solar films for their versatility in seamlessly integrating with building structures. These films can be incorporated into various surfaces, including glass facades and windows, enabling the integration of solar energy harvesting without compromising aesthetic and architectural design. This dual functionality of energy generation and design flexibility positions EVA solar films as a preferred choice in the realm of sustainable architecture. Furthermore, while the automotive sector is increasingly recognizing the potential of EVA solar films for applications such as solar roofs in electric and hybrid vehicles. These films not only contribute to the reduction of carbon emissions but also enhance the energy efficiency of vehicles by harnessing solar power to supplement traditional charging systems. The lightweight & flexible nature of EVA solar films align well with the automotive industry's ongoing efforts to enhance fuel efficiency and reduce the environmental impact of vehicles.

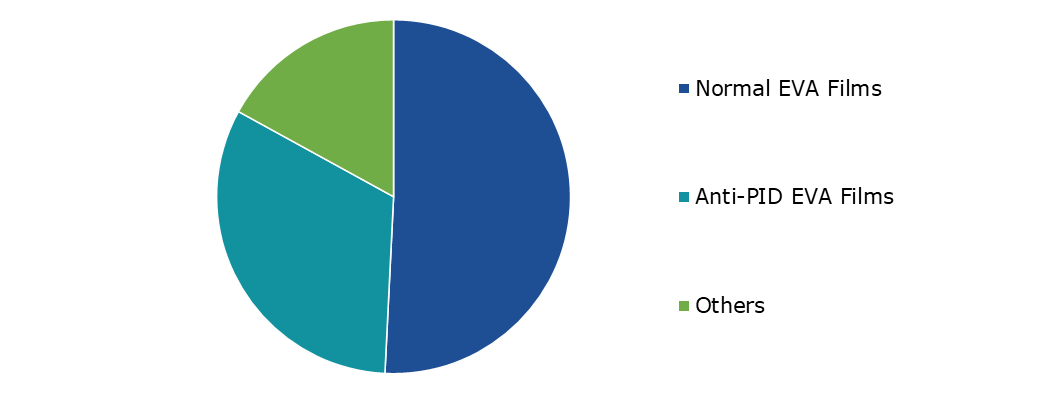

Global EVA Solar Films Market Share, by Type, 2022

Source: Research Dive Analysis

The normal EVA films sub-segment accounted for the highest market share in 2022. Durability is a major benefit of normal EVA films, with the material exhibiting resistance to environmental factors and wear, ensuring the longevity of solar panels in various conditions. This durability is particularly crucial given the exposure of solar panels to diverse weather conditions and external elements. Moreover, the cost-effectiveness of normal EVA films positions them as a pragmatic choice. Widely available and economically viable, EVA films strike an appropriate balance between performance & affordability, benefiting manufacturers seeking to optimize production costs without compromising on the quality & durability of their solar panels. The advantageous properties of normal EVA films extend beyond their individual merits, as they contribute to the efficiency of the manufacturing process. The films facilitate easy lamination processes during the production of solar modules, streamlining the workflow for manufacturers. This ease of integration enhances overall production efficiency, facilitating a smoother and more cost-effective manufacturing experience.

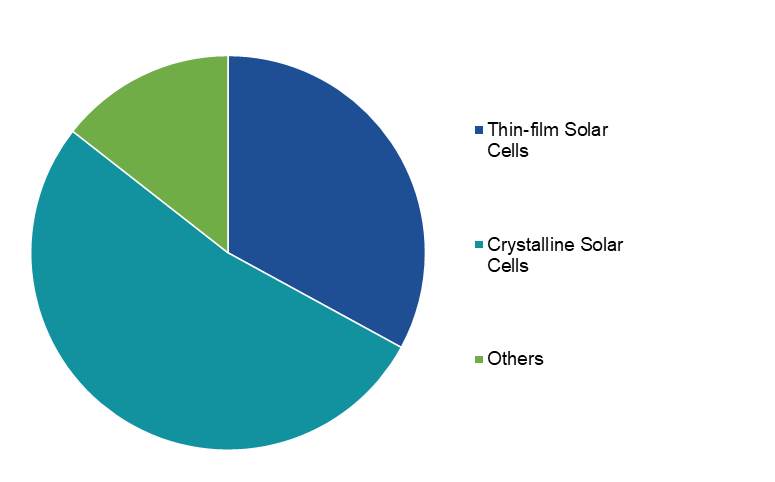

Global EVA Solar Films Market Share, by Application, 2022

Source: Research Dive Analysis

The crystalline solar cells sub-segment accounted for the highest market share in 2022. Crystalline solar cells have emerged as the dominant force in the EVA solar films market. This can be attributed to their inherent advantages and widespread adoption across the solar energy sector. Crystalline solar cells, known for their efficiency & durability, have become the preferred choice for harnessing solar energy. These cells utilize crystalline silicon, offering a high level of conversion efficiency, which is crucial in maximizing the electricity output from sunlight. This efficiency factor has propelled crystalline solar cells to the forefront of the EVA solar films market. The product finds application in residential rooftop installations to large-scale solar farms. Their versatility allows for seamless integration into different settings, meeting the diverse needs of the solar energy landscape. This adaptability positions crystalline solar cells as a go-to solution for both established and emerging solar projects, consolidating their dominating share in the EVA solar films market.

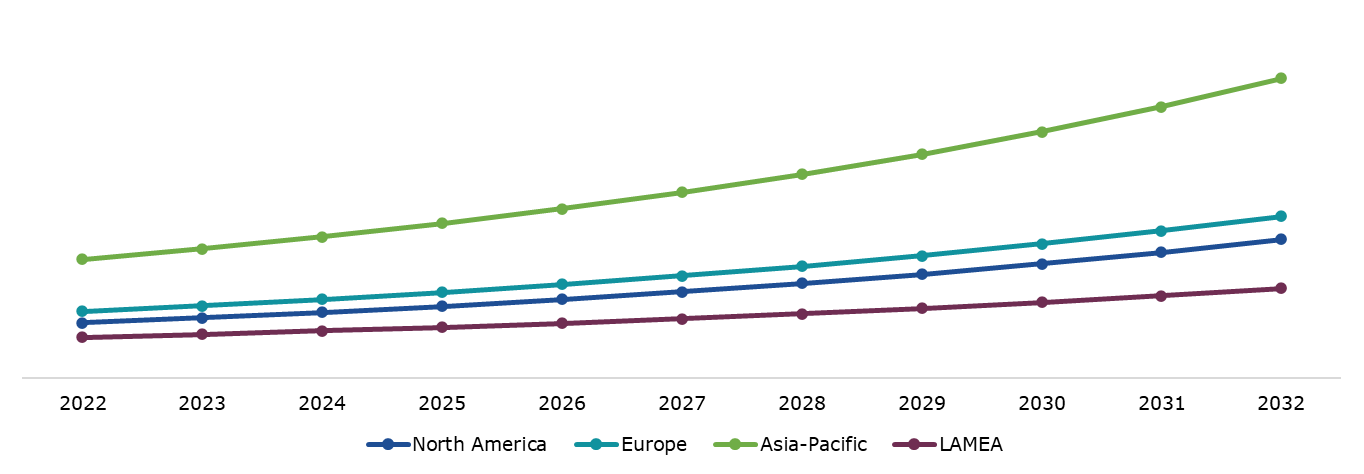

Global EVA Solar Films Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Asia Pacific EVA solar films market generated the highest revenue in 2022. The Asia Pacific region held a dominating position in the EVA solar films market, wielding a dominating share in this dynamic sector. With an ever-growing demand for sustainable energy solutions, the solar industry in the Asia Pacific has witnessed substantial growth, propelling the utilization of EVA solar films in photovoltaic applications. Countries across the Asia Pacific, driven by a collective commitment to renewable energy and environmental sustainability, have significantly invested in solar power infrastructure. This strategic focus has led to an increased deployment of solar modules, where EVA solar films play a pivotal role in enhancing the longevity & performance of photovoltaic panels. The dominance of the Asia Pacific region in the EVA solar films market can be attributed to its proactive approach to adopting solar energy technologies to meet escalating energy needs while mitigating environmental impact.

Competitive Scenario in the Global EVA Solar Films Market

Product launch, investment, and acquisition are common strategies followed by major market players. For instance, in September 2022, Hanwha Solutions, a player in the chemical and energy sector under South Korea's Hanwha Group, has strategically allocated a substantial infusion of $549 million to fortify its solar cell material business, aiming to establish a robust foundation for the production of high-power solar core products. This strategic move is a direct response to the intense competition posed by Chinese companies in the solar energy arena.

The focal point of this investment lies in augmenting the production capacity of EVA, a critical component in solar modules functioning as an encapsulating agent. With this, Hanwha Group's cumulative production capacity of EVA is set to soar to an impressive 9,20,000 tons, outstripping Exxon Mobil's capacity of 7,90,000 tons. EVA is recognized for its qualities such as good radiation transmission and resistance to sunlight degradation, which play a pivotal role in enhancing the durability & efficiency of solar modules. In a strategic collaboration, Hanwha Solutions has partnered with GS Energy, a total energy solution provider in South Korea, to establish an EVA joint venture named H&G Chemical. This venture, backed by a total investment of 590 billion won, aims to achieve an annual production capacity of 300,000 tons starting from September 2025.

Source: Research Dive Analysis

Some of the leading EVA solar films market players are Hangzhou First Applied, Str Holdings, Inc., Hanwha Solutions, Mitsui Chemicals, KENGO, Bridgestone Corporation, 3M, Astenik Solar, Guangzhou Lushan New Materials Co., Ltd., and Celanese Corporation.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global EVA solar films market?

A. The size of the global EVA solar films market was $3,168.2 million in 2022 and is projected to reach $7,771.0 million by 2032.

Q2. Which are the major companies in the EVA solar films market?

A. Hangzhou First Applied, Str Holdings, Inc., Hanwha Solutions, Mitsui Chemicals, KENGO, Bridgestone Corporation, 3M, Astenik Solar, Guangzhou Lushan New Materials Co., Ltd., and Celanese Corporation are some of the key players in the global EVA solar films market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia Pacific region possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia Pacific EVA solar films market?

A. The Asia Pacific EVA solar films market is anticipated to grow at 9.8% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Continuous improvement and brand product differentiation are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more in R&D activities?

A. Hangzhou First Applied, Str Holdings, Inc., Hanwha Solutions, and Mitsui Chemicals are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global EVA Solar Films market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry Intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on the EVA Solar Films Market.

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. EVA Solar Films Market Analysis, by Type

5.1. Overview

5.2. Normal EVA Films

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. Anti-PID EVA Films

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. Others

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2022-2032

5.4.3. Market share analysis, by country, 2022-2032

5.5. Research Dive Exclusive Insights

5.5.1. Market attractiveness

5.5.2. Competition heatmap

6. EVA Solar Films Market Analysis, by Application

6.1. Overview

6.2. Thin-film Solar Cells

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Crystalline Solar cells

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2022-2032

6.3.3. Market share analysis, by country, 2022-2032

6.4. Others

6.4.1. Definition, key trends, growth factors, and opportunities

6.4.2. Market size analysis, by region, 2022-2032

6.4.3. Market share analysis, by country, 2022-2032

6.5. Research Dive Exclusive Insights

6.5.1. Market attractiveness

6.5.2. Competition heatmap

7. 6. EVA Solar Films Market, by Region

7.1. North America

7.1.1. U.S.

7.1.1.1. Market size analysis, by Type, 2022-2032

7.1.1.2. Market size analysis, by Application, 2022-2032

7.1.2. Canada

7.1.2.1. Market size analysis, by Type, 2022-2032

7.1.2.2. Market size analysis, by Application, 2022-2032

7.1.3. Mexico

7.1.3.1. Market size analysis, by Type, 2022-2032

7.1.3.2. Market size analysis, by Application, 2022-2032

7.1.4. Research Dive Exclusive Insights

7.1.4.1. Market attractiveness

7.1.4.2. Competition heatmap

7.2. Europe

7.2.1. Germany

7.2.1.1. Market size analysis, by Type, 2022-2032

7.2.1.2. Market size analysis, by Application, 2022-2032

7.2.2. UK

7.2.2.1. Market size analysis, by Type, 2022-2032

7.2.2.2. Market size analysis, by Application, 2022-2032

7.2.3. France

7.2.3.1. Market size analysis, by Type, 2022-2032

7.2.3.2. Market size analysis, by Application, 2022-2032

7.2.4. Spain

7.2.4.1. Market size analysis, by Type, 2022-2032

7.2.4.2. Market size analysis, by Application, 2022-2032

7.2.5. Italy

7.2.5.1. Market size analysis, by Type, 2022-2032

7.2.5.2. Market size analysis, by Application, 2022-2032

7.2.6. Rest of Europe

7.2.6.1. Market size analysis, by Type, 2022-2032

7.2.6.2. Market size analysis, by Application, 2022-2032

7.2.7. Research Dive Exclusive Insights

7.2.7.1. Market attractiveness

7.2.7.2. Competition heatmap

7.3. Asia-Pacific

7.3.1. China

7.3.1.1. Market size analysis, by Type, 2022-2032

7.3.1.2. Market size analysis, by Application, 2022-2032

7.3.2. Japan

7.3.2.1. Market size analysis, by Type, 2022-2032

7.3.2.2. Market size analysis, by Application, 2022-2032

7.3.3. India

7.3.3.1. Market size analysis, by Type, 2022-2032

7.3.3.2. Market size analysis, by Application, 2022-2032

7.3.4. Australia

7.3.4.1. Market size analysis, by Type, 2022-2032

7.3.4.2. Market size analysis, by Application, 2022-2032

7.3.5. South Korea

7.3.5.1. Market size analysis, by Type, 2022-2032

7.3.5.2. Market size analysis, by Application, 2022-2032

7.3.6. Rest of Asia-Pacific

7.3.6.1. Market size analysis, by Type, 2022-2032

7.3.6.2. Market size analysis, by Application, 2022-2032

7.3.7. Research Dive Exclusive Insights

7.3.7.1. Market attractiveness

7.3.7.2. Competition heatmap

7.4. LAMEA

7.4.1. Brazil

7.4.1.1. Market size analysis, by Type, 2022-2032

7.4.1.2. Market size analysis, by Application, 2022-2032

7.4.2. UAE

7.4.2.1. Market size analysis, by Type, 2022-2032

7.4.2.2. Market size analysis, by Application, 2022-2032

7.4.3. Saudi Arabia

7.4.3.1. Market size analysis, by Type, 2022-2032

7.4.3.2. Market size analysis, by Application, 2022-2032

7.4.4. South Africa

7.4.4.1. Market size analysis, by Type, 2022-2032

7.4.4.2. Market size analysis, by Application, 2022-2032

7.4.5. Rest of LAMEA

7.4.5.1. Market size analysis, by Type, 2022-2032

7.4.5.2. Market size analysis, by Application, 2022-2032

7.4.6. Research Dive Exclusive Insights

7.4.6.1. Market attractiveness

7.4.6.2. Competition heatmap

8. Competitive Landscape

8.1. Top winning strategies, 2022

8.1.1. By strategy

8.1.2. By year

8.2. Strategic overview

8.3. Market share analysis, 2022

9. Company Profiles

9.1. Hangzhou First Applied

9.1.1. Overview

9.1.2. Business segments

9.1.3. Product portfolio

9.1.4. Financial performance

9.1.5. Recent developments

9.1.6. SWOT analysis

9.2. Str Holdings, Inc.

9.2.1. Overview

9.2.2. Business segments

9.2.3. Product portfolio

9.2.4. Financial performance

9.2.5. Recent developments

9.2.6. SWOT analysis

9.3. Hanwha Solutions

9.3.1. Overview

9.3.2. Business segments

9.3.3. Product portfolio

9.3.4. Financial performance

9.3.5. Recent developments

9.3.6. SWOT analysis

9.4. Mitsui Chemicals

9.4.1. Overview

9.4.2. Business segments

9.4.3. Product portfolio

9.4.4. Financial performance

9.4.5. Recent developments

9.4.6. SWOT analysis

9.5. KENGO

9.5.1. Overview

9.5.2. Business segments

9.5.3. Product portfolio

9.5.4. Financial performance

9.5.5. Recent developments

9.5.6. SWOT analysis

9.6. Bridgestone Corporation

9.6.1. Overview

9.6.2. Business segments

9.6.3. Product portfolio

9.6.4. Financial performance

9.6.5. Recent developments

9.6.6. SWOT analysis

9.7. 3M

9.7.1. Overview

9.7.2. Business segments

9.7.3. Product portfolio

9.7.4. Financial performance

9.7.5. Recent developments

9.7.6. SWOT analysis

9.8. Astenik Solar

9.8.1. Overview

9.8.2. Business segments

9.8.3. Product portfolio

9.8.4. Financial performance

9.8.5. Recent developments

9.8.6. SWOT analysis

9.9. Guangzhou Lushan New Materials Co., Ltd.

9.9.1. Overview

9.9.2. Business segments

9.9.3. Product portfolio

9.9.4. Financial performance

9.9.5. Recent developments

9.9.6. SWOT analysis

9.10. Celanese Corporation

9.10.1. Overview

9.10.2. Business segments

9.10.3. Product portfolio

9.10.4. Financial performance

9.10.5. Recent developments

9.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com