Start Stop Technology Market Report

RA09222

Start Stop Technology Market by Type (Belt-driven Alternator Starter (BAS), Integrated Starter Generator (ISG), Direct Starter, and Integrated Starter Generator) Application (Passenger Car and Commercial Car), and Region (North America, Europe, Asia-Pacific, and LAMEA): Opportunity Analysis and Industry Forecast, 2023-2032

Start Stop Technology Overview

‘Start-Stop Technology,’ also known as ‘stop-start’ or ‘idle-stop,’ is a system used in internal combustion engine vehicles that turns off the engine when the vehicle comes to a stop and restarts when the driver intends to go again. This technique is intended to reduce fuel consumption and emissions, particularly when the vehicle is stationary, such as at traffic lights or in congested areas.

The system works by automatically turning off the engine when the vehicle is stationary and the brake is applied. Once the driver releases the brake pedal or engages the clutch (in manual transmission vehicles), the engine restarts instantly, allowing the vehicle to resume normal operation. Start-stop technology is particularly effective in urban driving conditions, where vehicles frequently come to a stop and spend a significant amount of time idling.

Global Start Stop Technology Market Analysis

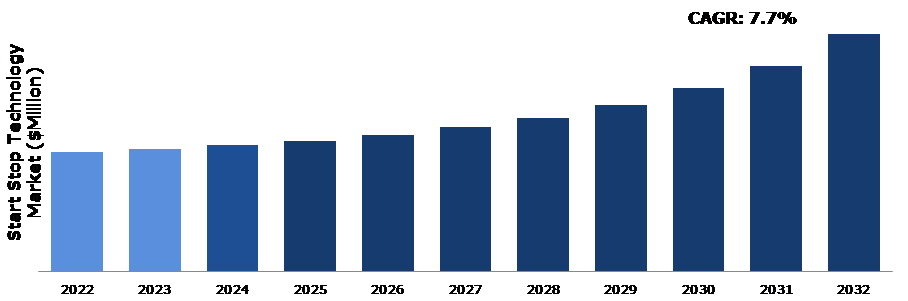

The global start stop technology market size was $1,774.0 million in 2022 and is predicted to grow with a CAGR of 7.7%, by generating a revenue of $3,530.5 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on the Global Start Stop Technology Market

The COVID-19 pandemic had a significant impact on various industries, including the automotive sector. The extent of the impact on the global start-stop technology market depended on several factors, including regional outbreaks, lockdown measures, and disruptions in the supply chain. Many automotive manufacturing plants around the world experienced temporary closures or reduced production capacities due to lockdowns and restrictions imposed to curb the spread of the virus. This affected the production and integration of start-stop technology into vehicles. The automotive industry relies on complex global supply chains. Disruptions in the supply chain, including shortages of components or delays in shipments, affected the availability of start-stop technology components during the pandemic.

Increasing Demand for Fuel Efficient Vehicles is Expected to Drive the Market Growth

The increasing demand for fuel-efficient vehicles is indeed a significant driver for the growth of the start stop technology market. As consumers and regulatory bodies around the world become more concerned about environmental sustainability and fuel efficiency, automotive manufacturers are under pressure to develop and adopt technologies that can enhance the fuel efficiency of their vehicles. Start-stop technology plays a crucial role in achieving fuel efficiency by reducing unnecessary idling time when a vehicle is stationary, such as at traffic lights or in congested traffic. By automatically shutting off the engine during these situations and restarting it when needed, the system helps to save fuel and reduce emissions. Growing awareness regarding environmental issues and the need to reduce carbon emissions drive consumers and governments to support technologies that promote fuel efficiency and reduce the overall environmental impact of transportation. The development of advanced battery technologies, such as absorbent glass mat (AGM) and lithium-ion batteries, has enhanced the efficiency and durability of start-stop systems. These batteries can handle the frequent cycling associated with engine stop-start events. Some governments provide incentives or impose regulations favoring fuel-efficient and low-emission vehicles. Incentives such as tax credits or rebates encourage automakers to adopt start-stop technology, while regulations mandate its inclusion in certain vehicle categories. Increasing awareness and positive experiences with start-stop systems contribute to consumer acceptance. As drivers become familiar with the benefits and operation of the technology, its adoption is likely to increase.

Excessive Start-stop Cycles, Inoperability Under Certain Conditions, and Optional Use is Likely to Restrain the Growth of the Market

Hybrid/electric cars do not experience any delay in power from the engine stop. However, conventional fuel vehicles mostly experience slight delays, which can hinder driving capability in stop and go traffic conditions and lead to excessive start-stop cycles. In addition, larger capacity batteries are required to deal with the extra wear & tear caused by the system, which further increases the load on the vehicle. Furthermore, the sudden forward jerk of a car in an automatic restart instead of the steadily moving forward can lead to risks in heavy traffic conditions. In several vehicles, the system activates only under optimal conditions. In addition, the increase in pressure on the vehicle's battery and starter motor during frequent start-stop events can impact their durability over time. If these components are not designed to handle the additional stress, it may lead to more frequent replacements, affecting the cost-effectiveness of the technology.

Increasing Demand for High-Efficiency Engines to Drive Excellent Opportunities

High efficiency engines are frequently combined with start-stop systems as they further increase fuel economy and lower the number of pollutants. Consumers are increasingly buying cars with high-efficiency engines as a means of lowering their fuel expenditures and environmental effect. In addition, increasing urbanization and resultant traffic congestion in many regions create situations where vehicles frequently come to a stop. Start-stop technology is particularly effective in urban environments, where it minimizes fuel consumption during idling, aligning with the driving patterns of many city drivers. In addition, one of the major factors driving the automotive start stop system market is consumers' growing preference for fuel-efficient automobiles as a result of rising fuel prices. Fuel price increases have made it harder for consumers to afford traditional fuels for their vehicles. Continuous fuel prices have spurred global demand for fuel-efficient automobiles, forcing manufacturers to launch vehicles with a start-stop system that are low in weight in order to achieve improved fuel efficiency. All these factors are anticipated to create several growth opportunities in the start stop technology market during the forecast period.

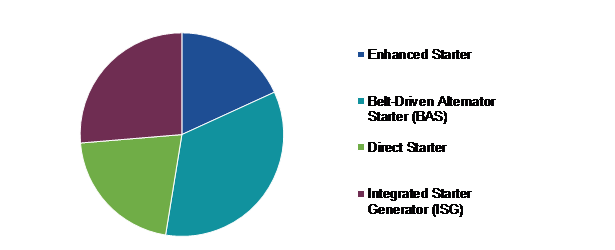

Global Start Stop Technology Market Share, by Type, 2022

Source: Research Dive Analysis

The belt-driven alternator starter sub-segment accounted for the highest market share in 2022. Belted Alternator Starter (BAS) is a category of automotive parallel hybrid technology that uses an electric motor to contribute power to the internal combustion engine's crankshaft via a serpentine belt. A belt-driven alternator's principal duty is to create electrical power. It transforms mechanical energy from the engine, which is transferred via the belt and pulley system, into electrical energy. This electrical power is essential for charging the vehicle's battery and powering numerous components including lights, radios, and other electronic systems.

Global Start Stop Technology Market Share, by Application, 2022

Source: Research Dive Analysis

The passenger car sub-segment accounted for the highest market share in 2022. Start-stop technology is very useful in urban settings with frequent stop-and-go traffic. When the vehicle is stationary, such as at a traffic signal or in heavy traffic, the engine automatically switches off and restarts fast when the driver is ready to move again. This saves fuel and lowers pollution, particularly in instances when idling would otherwise occur. The potential for fuel savings is the key motivator driving the adoption of start-stop technology. The car does not consume fuel when the engine is not running during idling times. This can contribute to increased fuel efficiency, making it a desirable feature for both manufacturers and users, particularly in areas where gasoline prices are quite high. All these are the major factors projected to boost the segment growth in the future.

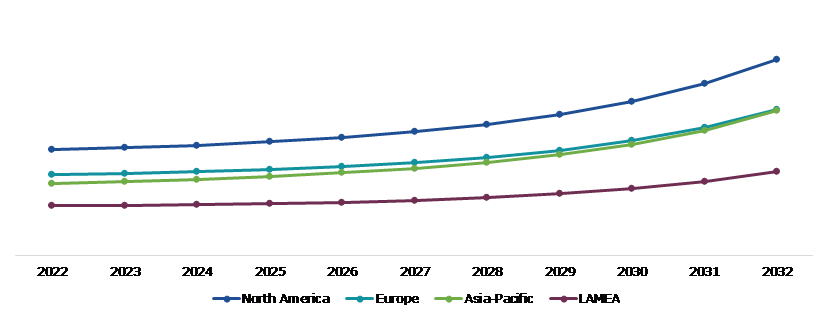

Global Start Stop Technology Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The North America start stop technology market generated the highest revenue in 2022. The stringent fuel efficiency standards imposed by regulatory agencies in North America drive automakers to implement technologies that improve miles per gallon (MPG). Start-stop systems help meet these standards by reducing unnecessary fuel consumption during idling. Growing environmental consciousness among consumers and a focus on reducing greenhouse gas emissions have led to increased interest in fuel-efficient vehicles. Start-stop technology aligns with these environmental concerns as it helps lower overall fuel consumption and tailpipe emissions. Consumers in North America are increasingly seeking ways to save on fuel costs. Start-stop technology provides a practical solution by automatically shutting down the engine during brief stops, such as at traffic lights or in traffic jams, contributing to fuel savings over time. Start-stop systems rely on advanced battery technology to smoothly restart the engine. The development of more efficient and durable batteries has facilitated the widespread adoption of this technology. The prevalence of urban traffic conditions in North American cities, where frequent stops and slow-moving traffic are common, makes start-stop technology particularly relevant. Drivers benefit from reduced fuel consumption during frequent idling situations.

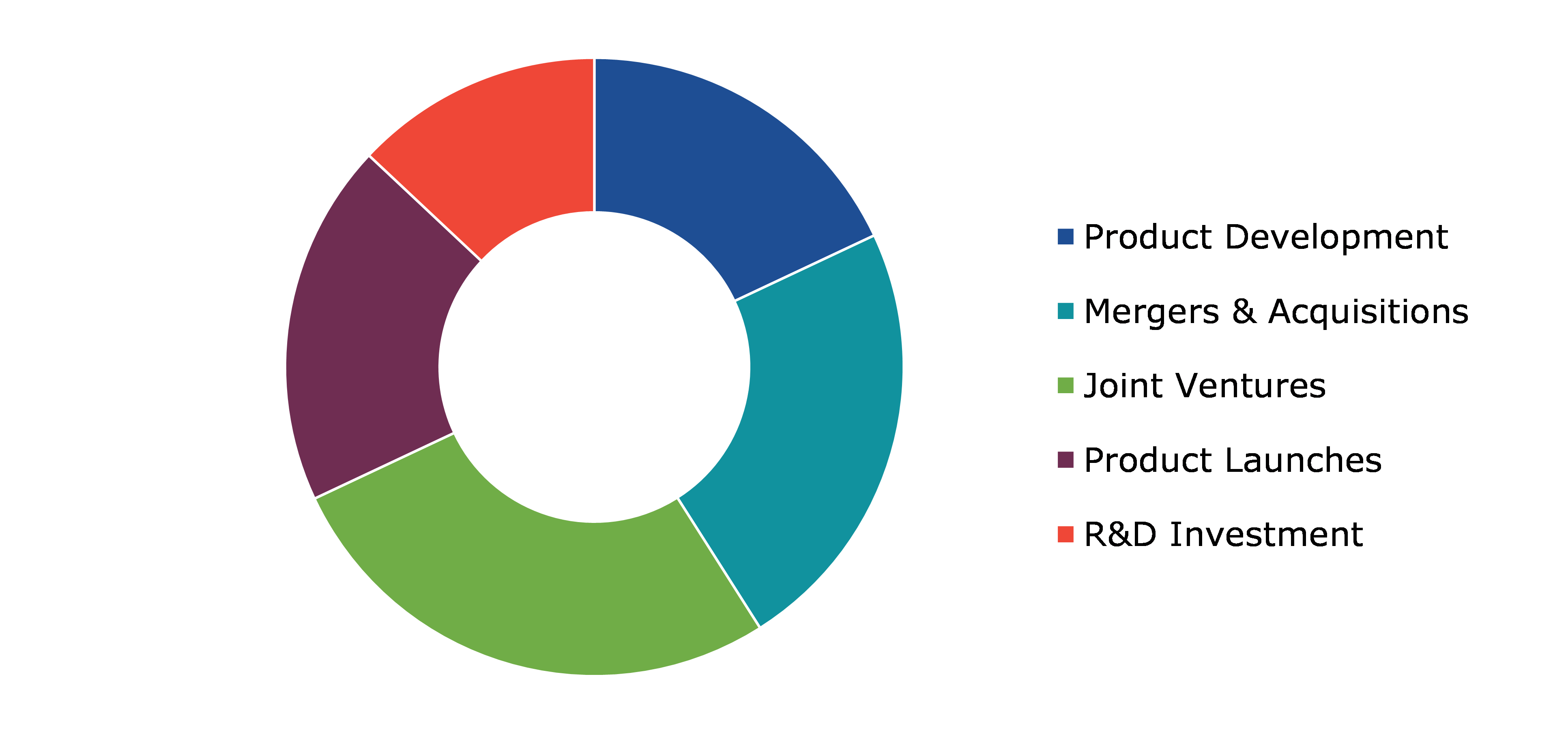

Competitive Scenario in the Global Start Stop Technology Market

Investment and agreement are common strategies followed by major market players. For instance, on December 7, 2022, Suzuki Motorcycle India revealed an upgraded variant for its Burgman Street maxi-scooter. The newly launched model is equipped with a cutting-edge Suzuki Eco Performance Alpha (SEP-a) engine, featuring an automatic stop-start function and a quiet starter mechanism. The Engine Auto Start-Stop (EASS) system is designed to reduce fuel consumption by automatically shutting down the engine during idle moments and restarting it when the rider accelerates. This feature proves beneficial in situations like stop-and-go traffic and when waiting at traffic lights.

Source: Research Dive Analysis

Some of the companies operating in the start stop technology market are Valeo, Robert Bosch GmbH, Continental AG, DENSO CORPORATION, Mitsubishi Electric Corporation, BorgWarner Inc., AISIN SEIKI Co., Ltd., Delphi Automotive LLP, Johnson Controls, and Hitachi Automotive Systems, Ltd.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global start stop technology market?

A. The size of the global start stop technology market was over $1,774.0 million in 2022 and is projected to reach $3,527.7 million by 2032.

Q2. Which are the major companies in the start stop technology?

A. Robert Bosch GmbH, Continental AG, and DENSO CORPORATION are some of the key players in the global start stop technology market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific start stop technology market?

A. The Asia-Pacific start stop technology market is anticipated to grow at 5.0% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. DENSO CORPORATION and Mitsubishi Electric Corporation are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global start stop technology market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact force

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry Intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Legal

4.6.6. Environmental

4.7. Impact of COVID-19 on start stop technology market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Start Stop Technology Market Analysis, By Type

5.1. Overview

5.2. Belt-driven Alternator Starter (BAS)

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. Integrated Starter Generator (ISG)

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. Direct Starter

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2022-2032

5.4.3. Market share analysis, by country, 2022-2032

5.5. Integrated Starter Generator

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2. Market size analysis, by region, 2022-2032

5.5.3. Market share analysis, by country, 2022-2032

5.6. Research Dive Exclusive Insights

5.6.1. Market attractiveness

5.6.2. Competition heatmap

6. Start Stop Technology Market Analysis, by Application

6.1. Overview

6.2. Passenger Car

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Commercial Car

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2022-2032

6.3.3. Market share analysis, by country, 2022-2032

6.4. Research Dive Exclusive Insights

6.4.1. Market attractiveness

6.4.2. Competition heatmap

7. Start Stop Technology Market, by Region

7.1. North America

7.1.1. U.S.

7.1.1.1. Market size analysis, by Product, 2022-2032

7.1.1.2. Market size analysis, by Application, 2022-2032

7.1.2. Canada

7.1.2.1. Market size analysis, by Product, 2022-2032

7.1.2.2. Market size analysis, by Application, 2022-2032

7.1.3. Mexico

7.1.3.1. Market size analysis, by Product, 2022-2032

7.1.3.2. Market size analysis, by Application, 2022-2032

7.1.4. Research Dive Exclusive Insights

7.1.4.1. Market attractiveness

7.1.4.2. Competition heatmap

7.2. Europe

7.2.1. Germany

7.2.1.1. Market size analysis, by Product, 2022-2032

7.2.1.2. Market size analysis, by Application, 2022-2032

7.2.2. UK

7.2.2.1. Market size analysis, by Product, 2022-2032

7.2.2.2. Market size analysis, by Application, 2022-2032

7.2.3. France

7.2.3.1. Market size analysis, by Product, 2022-2032

7.2.3.2. Market size analysis, by Application, 2022-2032

7.2.4. Spain

7.2.4.1. Market size analysis, by Product, 2022-2032

7.2.4.2. Market size analysis, by Application, 2022-2032

7.2.5. Italy

7.2.5.1. Market size analysis, by Product, 2022-2032

7.2.5.2. Market size analysis, by Application, 2022-2032

7.2.6. Rest of Europe

7.2.6.1. Market size analysis, by Product, 2022-2032

7.2.6.2. Market size analysis, by Application, 2022-2032

7.2.7. Research Dive Exclusive Insights

7.2.7.1. Market attractiveness

7.2.7.2. Competition heatmap

7.3. Asia-Pacific

7.3.1. China

7.3.1.1. Market size analysis, by Product, 2022-2032

7.3.1.2. Market size analysis, by Application, 2022-2032

7.3.2. Japan

7.3.2.1. Market size analysis, by Product, 2022-2032

7.3.2.2. Market size analysis, by Application, 2022-2032

7.3.3. India

7.3.3.1. Market size analysis, by Product, 2022-2032

7.3.3.2. Market size analysis, by Application, 2022-2032

7.3.4. Australia

7.3.4.1. Market size analysis, by Product, 2022-2032

7.3.4.2. Market size analysis, by Application, 2022-2032

7.3.5. Indonesia

7.3.5.1. Market size analysis, by Product, 2022-2032

7.3.5.2. Market size analysis, by Application, 2022-2032

7.3.6. Rest of Asia-Pacific

7.3.6.1. Market size analysis, by Product, 2022-2032

7.3.6.2. Market size analysis, by Application, 2022-2032

7.3.7. Research Dive Exclusive Insights

7.3.7.1. Market attractiveness

7.3.7.2. Competition heatmap

7.4. LAMEA

7.4.1. Brazil

7.4.1.1. Market size analysis, by Product, 2022-2032

7.4.1.2. Market size analysis, by Application, 2022-2032

7.4.2. UAE

7.4.2.1. Market size analysis, by Product, 2022-2032

7.4.2.2. Market size analysis, by Application, 2022-2032

7.4.3. South Africa

7.4.3.1. Market size analysis, by Product, 2022-2032

7.4.3.2. Market size analysis, by Application, 2022-2032

7.4.4. Argentina

7.4.4.1. Market size analysis, by Product, 2022-2032

7.4.4.2. Market size analysis, by Application, 2022-2032

7.4.5. Rest of LAMEA

7.4.5.1. Market size analysis, by Product, 2022-2032

7.4.5.2. Market size analysis, by Application, 2022-2032

7.4.6. Research Dive Exclusive Insights

7.4.6.1. Market attractiveness

7.4.6.2. Competition heatmap

8. Competitive Landscape

8.1. Top winning strategies, 2022

8.1.1. By strategy

8.1.2. By year

8.2. Strategic overview

8.3. Market share analysis, 2022

9. Company Profiles

9.1. Valeo

9.1.1. Overview

9.1.2. Business segments

9.1.3. Product portfolio

9.1.4. Financial performance

9.1.5. Recent developments

9.1.6. SWOT analysis

9.2. Robert Bosch GmbH

9.2.1. Overview

9.2.2. Business segments

9.2.3. Product portfolio

9.2.4. Financial performance

9.2.5. Recent developments

9.2.6. SWOT analysis

9.3. Continental AG

9.3.1. Overview

9.3.2. Business segments

9.3.3. Product portfolio

9.3.4. Financial performance

9.3.5. Recent developments

9.3.6. SWOT analysis

9.4. DENSO CORPORATION

9.4.1. Overview

9.4.2. Business segments

9.4.3. Product portfolio

9.4.4. Financial performance

9.4.5. Recent developments

9.4.6. SWOT analysis

9.5. Mitsubishi Electric Corporation

9.5.1. Overview

9.5.2. Business segments

9.5.3. Product portfolio

9.5.4. Financial performance

9.5.5. Recent developments

9.5.6. SWOT analysis

9.6. BorgWarner Inc

9.6.1. Overview

9.6.2. Business segments

9.6.3. Product portfolio

9.6.4. Financial performance

9.6.5. Recent developments

9.6.6. SWOT analysis

9.7. AISIN SEIKI Co., Ltd

9.7.1. Overview

9.7.2. Business segments

9.7.3. Product portfolio

9.7.4. Financial performance

9.7.5. Recent developments

9.7.6. SWOT analysis

9.8. Delphi Automotive LLP

9.8.1. Overview

9.8.2. Business segments

9.8.3. Product portfolio

9.8.4. Financial performance

9.8.5. Recent developments

9.8.6. SWOT analysis

9.9. Johnson Controls

9.9.1. Overview

9.9.2. Business segments

9.9.3. Product portfolio

9.9.4. Financial performance

9.9.5. Recent developments

9.9.6. SWOT analysis

9.10. Hitachi Automotive Systems, Ltd.

9.10.1. Overview

9.10.2. Business segments

9.10.3. Product portfolio

9.10.4. Financial performance

9.10.5. Recent developments

9.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com