Cybersecurity In Banking Market Report

RA09189

Cybersecurity in Banking Market by Deployment (Public Cloud, Private Cloud, Data Center, and Managed Services), Bank Size (Small, Medium, and Large), Technology (Data Protection, Governance, Risk & Compliance, Email Security & Awareness, Cloud Security, Network Security, Identity & Access Management, Security Consulting, Web Security, IoT/OT, Endpoint Security, Application Security, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Cybersecurity in Banking Overview

Cybersecurity in banking refers to a systematic arrangement of technologies, protocols, and methods to provide protection against cyberattacks, damage, malware, viruses, hacking, data theft, and unauthorized access to devices, programs, networks, and data. As the word shifts to digital economy, cybersecurity in banking is becoming a serious concern. Utilizing methods and procedures created to safeguard the data is essential for a successful digital revolution. Banks use a combination of analytical models and deterministic solutions as part of a robust cyber framework. Cyber solutions are used in banking for the following three priorities: safeguard web and mobile applications, identify risk exposure, and review existing cyber defenses.

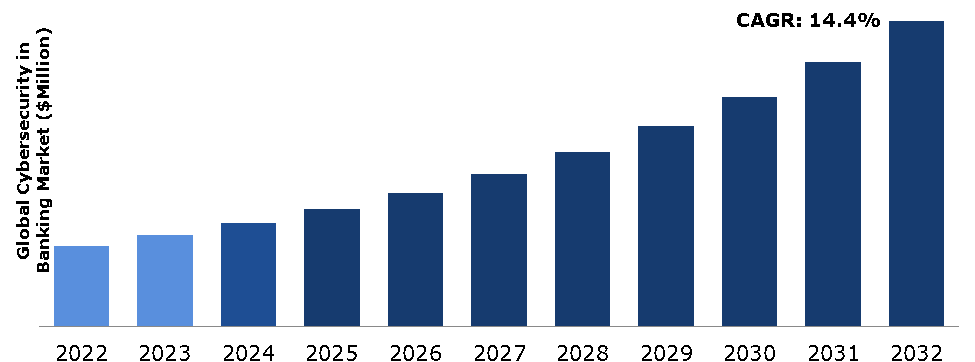

Global Cybersecurity in Banking Market Analysis

The global cybersecurity in banking market size was $74,300.0 million in 2022 and is predicted to grow with a CAGR of 14.4%, by generating a revenue of $281,987.5 million by 2032.

Source: Research Dive Analysis

Covid-19 Impact on Global Cybersecurity in Banking Market Analysis

Financial institutions (FIs), such as banks and insurance providers, reported significant increase in threat levels from COVID-related cybercrime during the pandemic. Rapid increase in new pandemic-related threats along with a rise in challenges caused by enforced work from home guidelines led to insecure gaps in financial institutional networks. This was majorly due to the financial losses and cost cutting on budget related to cybersecurity in financial institutions. Moreover, IT security teams witnessed pressure from decreased budgets and team redundancies. A spike in online shopping due to the lockdown and travel restrictions has also led to increase in cybercrimes. Increase in shopping from the fraudulent sites during the pandemic led to concerns over sharing data, leaving consumers worried about their digital identity and personal information online. Therefore, during the pandemic several people faced financial losses due to less awareness about online activities and transactions.

Growing Digital Transformation in Banking to Drive the Market Growth

Banks and financial institutions around the world have been adopting technology driven services, especially since the COVID-19 pandemic. The banking sector has always been victim of cyberattacks or cyberthreats, and with COVID-19, this sector has become more vulnerable. According to VMware Carbon Black, a cybersecurity company based in Waltham, Massachusetts, cyberattacks against banks and financial institutions around the world increased to 238% between February 2020 and April 2020. Malware, ransomware, trojans, spoofing, and phishing attacks are few cyber threats faced by the banking sector. Protecting digital banking systems from malware can be done by blocking these attacks using reliable antiviruses and runtime application self-protection (RASP) solutions. Moreover, implementing two-factor authentication and behavioral authentication can provide protection to the users even if the hacker manages to steal the user credentials. Furthermore, there were approximately 54,000 installation packages for mobile banking trojans in the first quarter of 2022 across the globe. There has been a rise of more than 53% as compared to 2021 fourth quarter. After declining for the first three quarters of 2021, the number of trojan packages targeting mobile banking increased in the fourth quarter. Thus, increasing digitization is projected to boost the growth of the cybersecurity in banking market in upcoming years.

Lack of Skilled Professionals to Restrain the Market Growth

With the rapid developments in technology, it has become necessary for everyone to keep up with their IT knowledge. However, several sectors are still struggling with this idea, especially the banking industry. The lack of skilled professionals in the banking sector can cause several challenges. With the increase in cyber-attacks, it has become more important for all the companies to have trained employees in order to secure information. Lack of skilled professionals enable attackers to get into the systems and steal data easily. This is attributed due to the cybersecurity talent gap where the number of appropriately trained professionals is significantly less than the demand and uninformed employees are not appropriately trained about cybersecurity. According to the Global Cybersecurity Outlook 2023 by World Economic Forum, the shortfall between supply and demand for cybersecurity experts was estimated at 2.27 million in 2021. However, banks can address these issues by overcoming the talent gap by partnering with other organizations and security partners offering managed services to help provide protection. Also, conducting various security awareness training programs can help companies to avoid major cyberattacks.

Advancements in Technology to Drive Excellent Opportunities

Banks and financial institutions can leverage new technologies like artificial intelligence, machine learning, and blockchain to enhance their cybersecurity and can greatly benefit from these technologies. Emerging technologies in the financial services industry such as AI chatbots and automation help to reduce human effort, make better customer relationships, and increase profitability. Introduction of AI in banking can facilitate advanced predictive analytics and automated decision-making by analyzing and processing large amounts of data. AI is also used to detect and address cyberthreats and cyber risk such as malicious files and suspicious IP addresses. Application of AI in banking has enabled fully automated fraud detection, stock price forecasting, and loan applications processing. Furthermore, blockchain and Distributed Ledger Technology (DLT) has led to the rise of cryptoassets, which conventional financial services businesses, such as Visa, Mastercard, and PayPal have started to embrace. The banking industry is witnessing the emergence of digital wallets, digital assets, decentralized finance (DeFi), and non-fungible tokens (NFTs), whereas few countries are working on launching of ‘central bank digital currency (CBDC)’.

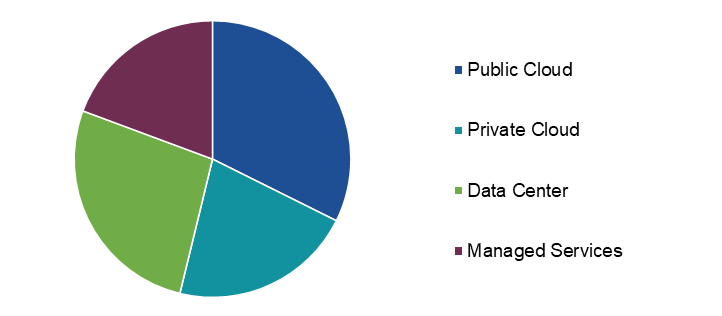

Global Cybersecurity in Banking Market Share, by Deployment, 2022

Source: Research Dive Analysis

The public cloud segment accounted for the highest market share in 2022, as the public cloud is a more secure environment than most on-premise systems, and it offers multiple layers of protection against data breaches and other attacks. Banks can reduce the cost by migrating their applications and data to the cloud. The pay-as-you-go pricing model of public clouds makes it more affordable for financial institutions to use these services. Furthermore, the use of public clouds also allows banks and other financial services firms to deploy applications quickly without having to worry about hardware maintenance or software upgrades. Therefore, the demand for public cloud deployment is expected rise in the future.

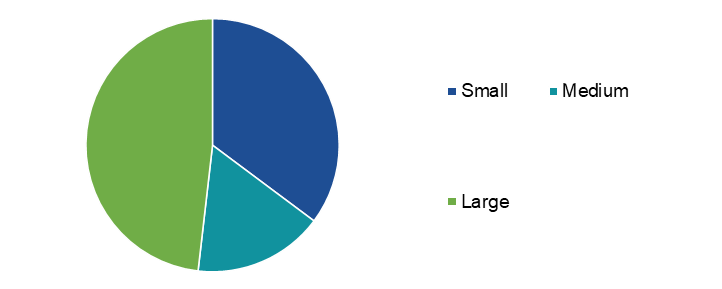

Global Cybersecurity in Banking Market Share, by Bank Size, 2022

Source: Research Dive Analysis

The large sub-segment accounted for the highest market share in 2022, as these institutions are spending heavily on the cybersecurity of their products and services. For instance, large institutions, such as Bank of America in 2021 stated that it spends over $1 billion per year on cybersecurity. Also, these institutions are working on aligning the best strategy for cybersecurity such as embracing Zero Trust Security Framework for enhancing the security of their products and services. Further, the average security breach cost is very high. For instance, according to IBM and Ponemon Institute’s Cost of a Data Breach Report 2022 report, the average cost of data breach was $4.35 million in 2022. Hence it is very critical for large financial institutions to have a secured network. Therefore, rising need for securing the products and services against cyberattacks is expected to boost the growth for cybersecurity in large organizations.

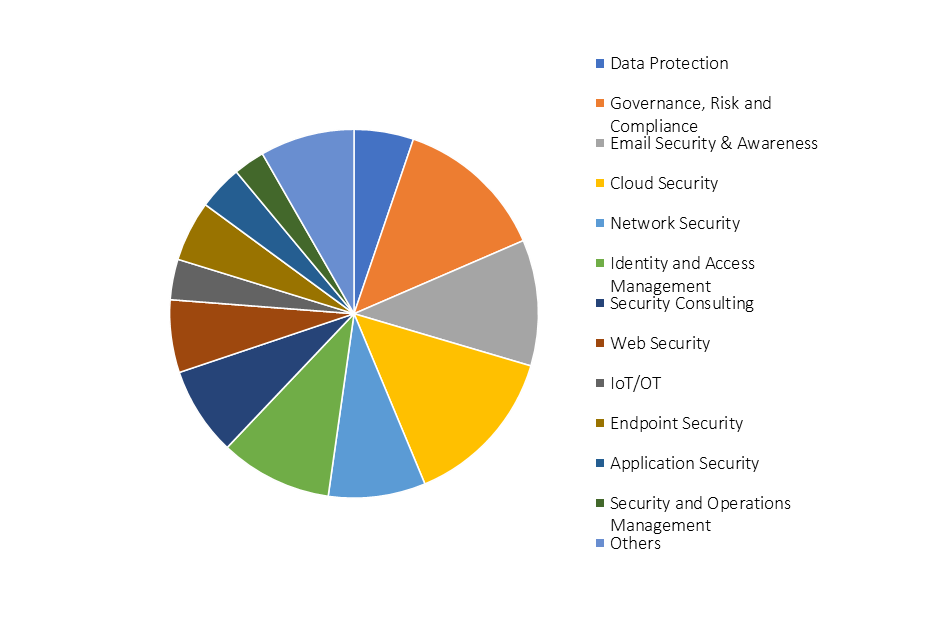

Global Cybersecurity in Banking Market Share, by Technology, 2022

Source: Research Dive Analysis

The cloud security sub-segment accounted for the highest market share in 2022. Migration towards cloud can help financial and banking sector improve their customer deliverables, break down internal silos, reduce costs, drive innovation – and even enhance security. New and exciting financial domains like fintech and insurtech have become possible owing to cloudification and an out-of-the-box approach to tech infrastructure, platforms, and services. According to a survey by Google Cloud and Harris Poll, 83% of financial services companies are using the public cloud in some form. In addition, a Cloud Security Alliance report found very similar adoption rates, with 91% of banking and finance respondents using cloud services or planning to in the next 6-9 months. Thus, adoption of cloud services for improving the security of products and services is increasing in the banking sector.

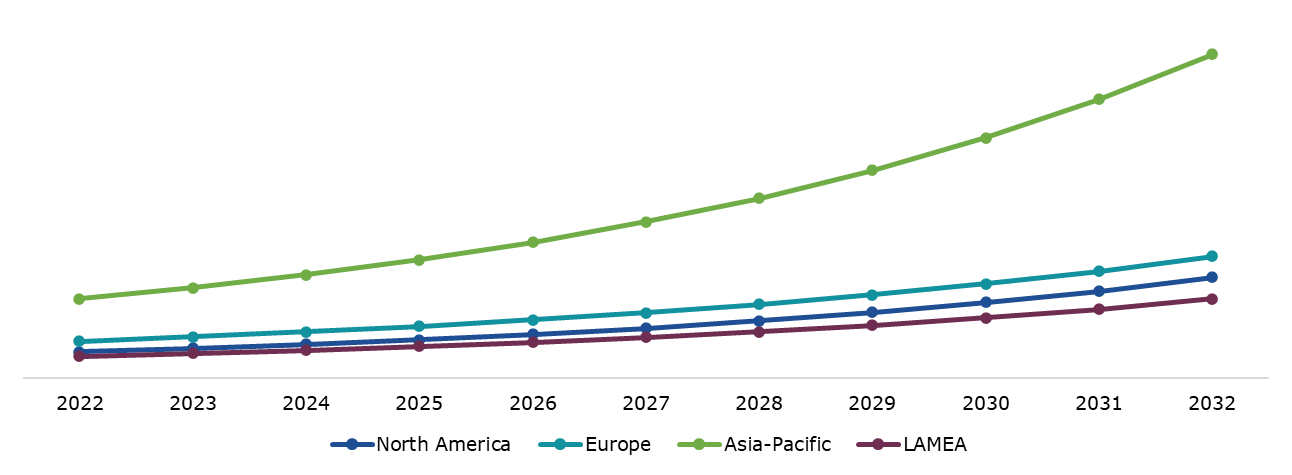

Global Cybersecurity in Banking Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Asia-Pacific cybersecurity in banking market generated the highest revenue in 2022. Asia-Pacific is known for its vibrant banking industry. It is also a home for various top notch banks such as Bank of China, Agricultural Bank of China, ICBC banks, DBS bank, United Overseas Banks, and others. Asian banks experienced strong growth and profitability in the years leading up to 2020, due to broad economic expansion and surging demand for financial services, in areas such as commercial banking, retail lending and wealth management. The COVID-19 pandemic has tested the sectors’ resilience, widening the gap between the region's digital leaders and laggards. For Asian banks, digitalization is considered as one of the highest priorities post-COVID-19 pandemic. Therefore, cybersecurity is of utmost importance for the banking industry in this region. Digitalization is expected to create growth opportunities in markets such as India, Indonesia, and China further driving the scope for cybersecurity in the region.

Competitive Scenario in the Global Cybersecurity in Banking Market

Partnerships and agreement are common strategies followed by major market players. In October 2022, Deutsche Bank announced that it would extend its partnership with Kyndryl, a U.S.-based IT infrastructure service provider, in a quest to deliver its digital transformation goals. With this new agreement, Kyndryl will continue to manage Deutsche Bank’s continental European core banking and mission-critical IT infrastructure needs. In addition, it will support the bank’s cloud migration and on-demand scalability to enhance the bank’s global service availability.

Source: Research Dive Analysis

Some of the leading players for cybersecurity in banking market players are JP Morgan Chase & Co. Bank of America, Wells Fargo, BNP Paribas, CITI Group Inc, Bank of China, Barclays, HSBC, Standard Chartered, Agricultural Bank of China, and Mitsubishi UFJ Financial Group.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Deployment |

|

| Segmentation by Bank Size |

|

|

Segmentation by Technology

|

|

| Key Companies Profiled |

|

Q1. What is the size of the global cybersecurity in banking market?

A. The global cybersecurity in banking market size $74,300.0 million in 2022 and is predicted to grow with a CAGR of 14.4%, by generating a revenue of $281,987.5 million by 2032.

Q2. Which are the major companies in the global cybersecurity in banking market?

A. Deutsche Bank and Bank of America are some of the key players in the global cybersecurity in banking market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific cybersecurity in banking market?

A. The Asia-Pacific cybersecurity in banking market is anticipated to grow at 15.3% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Partnerships and agreement are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. JP Morgan Chase, Deutsche Bank, and Bank of America are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global cybersecurity in banking market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive rivalry intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on cybersecurity in banking market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Cybersecurity in Banking Market Analysis, by Deployment

5.1. Overview

5.2. Public Cloud

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. Private Cloud

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. Data Center

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2022-2032

5.4.3. Market share analysis, by country, 2022-2032

5.5. Managed Services

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2. Market size analysis, by region, 2022-2032

5.5.3. Market share analysis, by country, 2022-2032

5.6. Research Dive Exclusive Insights

5.6.1. Market attractiveness

5.6.2. Competition heatmap

6. Cybersecurity in Banking Market Analysis, by Bank Size

6.1. Small

6.1.1. Definition, key trends, growth factors, and opportunities

6.1.2. Market size analysis, by region, 2022-2032

6.1.3. Market share analysis, by country, 2022-2032

6.2. Medium

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Large

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2022-2032

6.3.3. Market share analysis, by country, 2022-2032

6.4. Research Dive Exclusive Insights

6.4.1. Market attractiveness

6.4.2. Competition heatmap

7. Cybersecurity in Banking Market Analysis, by Technology

7.1. Data Protection

7.1.1. Definition, key trends, growth factors, and opportunities

7.1.2. Market size analysis, by region, 2022-2032

7.1.3. Market share analysis, by country, 2022-2032

7.2. Manufacturing

7.2.1. Definition, key trends, growth factors, and opportunities

7.2.2. Market size analysis, by region, 2022-2032

7.2.3. Market share analysis, by country, 2022-2032

7.3. Governance, Risk & Compliance

7.3.1. Definition, key trends, growth factors, and opportunities

7.3.2. Market size analysis, by region, 2022-2032

7.3.3. Market share analysis, by country, 2022-2032

7.4. Email Security & Awareness

7.4.1. Definition, key trends, growth factors, and opportunities

7.4.2. Market size analysis, by region, 2022-2032

7.4.3. Market share analysis, by country, 2022-2032

7.5. Cloud Security

7.5.1. Definition, key trends, growth factors, and opportunities

7.5.2. Market size analysis, by region, 2022-2032

7.5.3. Market share analysis, by country, 2022-2032

7.6. Network Security

7.6.1. Definition, key trends, growth factors, and opportunities

7.6.2. Market size analysis, by region, 2022-2032

7.6.3. Market share analysis, by country, 2022-2032

7.7. Identity & Access Management

7.7.1. Definition, key trends, growth factors, and opportunities

7.7.2. Market size analysis, by region, 2022-2032

7.7.3. Market share analysis, by country, 2022-2032

7.8. Security Consulting

7.8.1. Definition, key trends, growth factors, and opportunities

7.8.2. Market size analysis, by region, 2022-2032

7.8.3. Market share analysis, by country, 2022-2032

7.9. Web Consulting

7.9.1. Definition, key trends, growth factors, and opportunities

7.9.2. Market size analysis, by region, 2022-2032

7.9.3. Market share analysis, by country, 2022-2032

7.10. IoT/OT

7.10.1. Definition, key trends, growth factors, and opportunities

7.10.2. Market size analysis, by region, 2022-2032

7.10.3. Market share analysis, by country, 2022-2032

7.11. End-point Security

7.11.1. Definition, key trends, growth factors, and opportunities

7.11.2. Market size analysis, by region, 2022-2032

7.11.3. Market share analysis, by country, 2022-2032

7.12. Application Security

7.12.1. Definition, key trends, growth factors, and opportunities

7.12.2. Market size analysis, by region, 2022-2032

7.12.3. Market share analysis, by country, 2022-2032

7.13. Security and Operations Management

7.13.1. Definition, key trends, growth factors, and opportunities

7.13.2. Market size analysis, by region, 2022-2032

7.13.3. Market share analysis, by country, 2022-2032

7.14. Others

7.14.1. Definition, key trends, growth factors, and opportunities

7.14.2. Market size analysis, by region, 2022-2032

7.14.3. Market share analysis, by country, 2022-2032

7.15. Research Dive Exclusive Insights

7.15.1. Market attractiveness

7.15.2. Competition heatmap

8. Cybersecurity in Banking Market, by Region

8.1. North America

8.1.1. U.S.

8.1.1.1. Market size analysis, by Deployment, 2022-2032

8.1.1.2. Market size analysis, by Bank Size, 2022-2032

8.1.1.3. Market size analysis, by Technology, 2022-2032

8.1.2. Canada

8.1.2.1. Market size analysis, by Deployment, 2022-2032

8.1.2.2. Market size analysis, by Bank Size, 2022-2032

8.1.2.3. Market size analysis, by Technology, 2022-2032

8.1.3. Mexico

8.1.3.1. Market size analysis, by Deployment, 2022-2032

8.1.3.2. Market size analysis, by Bank Size, 2022-2032

8.1.3.3. Market size analysis, by Technology, 2022-2032

8.1.4. Research Dive Exclusive Insights

8.1.4.1. Market attractiveness

8.1.4.2. Competition heatmap

8.2. Europe

8.2.1. Germany

8.2.1.1. Market size analysis, by Deployment, 2022-2032

8.2.1.2. Market size analysis, by Bank Size, 2022-2032

8.2.1.3. Market size analysis, by Technology, 2022-2032

8.2.2. UK

8.2.2.1. Market size analysis, by Deployment, 2022-2032

8.2.2.2. Market size analysis, by Bank Size, 2022-2032

8.2.2.3. Market size analysis, by Technology, 2022-2032

8.2.3. France

8.2.3.1. Market size analysis, by Deployment, 2022-2032

8.2.3.2. Market size analysis, by Bank Size, 2022-2032

8.2.3.3. Market size analysis, by Technology, 2022-2032

8.2.4. Netherlands

8.2.4.1. Market size analysis, by Deployment, 2022-2032

8.2.4.2. Market size analysis, by Bank Size, 2022-2032

8.2.4.3. Market size analysis, by Technology, 2022-2032

8.2.5. Spain

8.2.5.1. Market size analysis, by Deployment, 2022-2032

8.2.5.2. Market size analysis, by Bank Size, 2022-2032

8.2.5.3. Market size analysis, by Technology, 2022-2032

8.2.6. Rest of Europe

8.2.6.1. Market size analysis, by Deployment, 2022-2032

8.2.6.2. Market size analysis, by Bank Size, 2022-2032

8.2.6.3. Market size analysis, by Technology, 2022-2032

8.2.7. Research Dive Exclusive Insights

8.2.7.1. Market attractiveness

8.2.7.2. Competition heatmap

8.3. Asia-Pacific

8.3.1. China

8.3.1.1. Market size analysis, by Deployment, 2022-2032

8.3.1.2. Market size analysis, by Bank Size, 2022-2032

8.3.1.3. Market size analysis, by Technology, 2022-2032

8.3.2. Japan

8.3.2.1. Market size analysis, by Deployment, 2022-2032

8.3.2.2. Market size analysis, by Bank Size, 2022-2032

8.3.2.3. Market size analysis, by Technology, 2022-2032

8.3.3. India

8.3.3.1. Market size analysis, by Deployment, 2022-2032

8.3.3.2. Market size analysis, by Bank Size, 2022-2032

8.3.3.3. Market size analysis, by Technology, 2022-2032

8.3.4. South Korea

8.3.4.1. Market size analysis, by Deployment, 2022-2032

8.3.4.2. Market size analysis, by Bank Size, 2022-2032

8.3.4.3. Market size analysis, by Technology, 2022-2032

8.3.5. Australia

8.3.5.1. Market size analysis, by Deployment, 2022-2032

8.3.5.2. Market size analysis, by Bank Size, 2022-2032

8.3.5.3. Market size analysis, by Technology, 2022-2032

8.3.6. Rest of Asia-Pacific

8.3.6.1. Market size analysis, by Deployment, 2022-2032

8.3.6.2. Market size analysis, by Bank Size, 2022-2032

8.3.6.3. Market size analysis, by Technology, 2022-2032

8.3.7. Research Dive Exclusive Insights

8.3.7.1. Market attractiveness

8.3.7.2. Competition heatmap

8.4. LAMEA

8.4.1. Brazil

8.4.1.1. Market size analysis, by Deployment, 2022-2032

8.4.1.2. Market size analysis, by Bank Size, 2022-2032

8.4.1.3. Market size analysis, by Technology, 2022-2032

8.4.2. UAE

8.4.2.1. Market size analysis, by Deployment, 2022-2032

8.4.2.2. Market size analysis, by Bank Size, 2022-2032

8.4.2.3. Market size analysis, by Technology, 2022-2032

8.4.3. Saudi Arabia

8.4.3.1. Market size analysis, by Deployment, 2022-2032

8.4.3.2. Market size analysis, by Bank Size, 2022-2032

8.4.3.3. Market size analysis, by Technology, 2022-2032

8.4.4. South Africa

8.4.4.1. Market size analysis, by Deployment, 2022-2032

8.4.4.2. Market size analysis, by Bank Size, 2022-2032

8.4.4.3. Market size analysis, by Technology, 2022-2032

8.4.5. Rest of LAMEA

8.4.5.1. Market size analysis, by Deployment, 2022-2032

8.4.5.2. Market size analysis, by Bank Size, 2022-2032

8.4.5.3. Market size analysis, by Technology, 2022-2032

8.4.6. Research Dive Exclusive Insights

8.4.6.1. Market attractiveness

8.4.6.2. Competition heatmap

9. Competitive Landscape

9.1. Top winning strategies, 2021

9.1.1. By strategy

9.1.2. By year

9.2. Strategic overview

9.3. Market share analysis, 2021

10. Company Profiles

10.1. JP Morgan Chase & Co.

10.1.1. Overview

10.1.2. Business segments

10.1.3. Product portfolio

10.1.4. Financial performance

10.1.5. Recent developments

10.1.6. SWOT analysis

10.2. Bank of America

10.2.1. Overview

10.2.2. Business segments

10.2.3. Product portfolio

10.2.4. Financial performance

10.2.5. Recent developments

10.2.6. SWOT analysis

10.3. Wells Fargo

10.3.1. Overview

10.3.2. Business segments

10.3.3. Product portfolio

10.3.4. Financial performance

10.3.5. Recent developments

10.3.6. SWOT analysis

10.4. BNP Paribas

10.4.1. Overview

10.4.2. Business segments

10.4.3. Product portfolio

10.4.4. Financial performance

10.4.5. Recent developments

10.4.6. SWOT analysis

10.5. CITI Group Inc.

10.5.1. Overview

10.5.2. Business segments

10.5.3. Product portfolio

10.5.4. Financial performance

10.5.5. Recent developments

10.5.6. SWOT analysis

10.6. Bank of China

10.6.1. Overview

10.6.2. Business segments

10.6.3. Product portfolio

10.6.4. Financial performance

10.6.5. Recent developments

10.6.6. SWOT analysis

10.7. Barclays

10.7.1. Overview

10.7.2. Business segments

10.7.3. Product portfolio

10.7.4. Financial performance

10.7.5. Recent developments

10.7.6. SWOT analysis

10.8. HSBC

10.8.1. Overview

10.8.2. Business segments

10.8.3. Product portfolio

10.8.4. Financial performance

10.8.5. Recent developments

10.8.6. SWOT analysis

10.9. Standard Chartered

10.9.1. Overview

10.9.2. Business segments

10.9.3. Product portfolio

10.9.4. Financial performance

10.9.5. Recent developments

10.9.6. SWOT analysis

10.10. Agricultural Bank of China

10.10.1. Overview

10.10.2. Business segments

10.10.3. Product portfolio

10.10.4. Financial performance

10.10.5. Recent developments

10.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com