Aircraft Paint Market Report

RA09181

Aircraft Paint Market by Application (Interior, Exterior), by Type (Enamel, Epoxy), by Aircraft Type (Narrow-body, Wide-body, Regional jets) and by End User (Military aircraft, Commercial aircraft), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Aircraft Paint Overview

Aircraft are exposed to various environmental elements, including moisture, salt, and other corrosive substances. The application of paint is essential in safeguarding the metal surfaces of the aircraft from corrosion, a critical factor in preserving the structural integrity and ensuring safety. The type and application of paint impacts the aerodynamics of an aircraft. Smooth and even surfaces are essential for optimal aerodynamic performance. Specialized aircraft paint is designed to provide a smooth surface, reduce drag, and enhance fuel efficiency. Aircraft paint is often used for marking and branding, making the aircraft easily identifiable. This is important for commercial & branding purposes and for air traffic control & other aviation safety considerations.

The high-altitude environment exposes aircraft to intense sunlight, including harmful ultraviolet (UV) rays. Aircraft paint is formulated to provide UV protection, preventing damage to both the paint itself and the underlying materials. The exterior of an aircraft experiences significant temperature variations, especially during flight. The paint is designed to withstand these temperature changes and protect the aircraft's structure.

Global Aircraft Paint Market Analysis

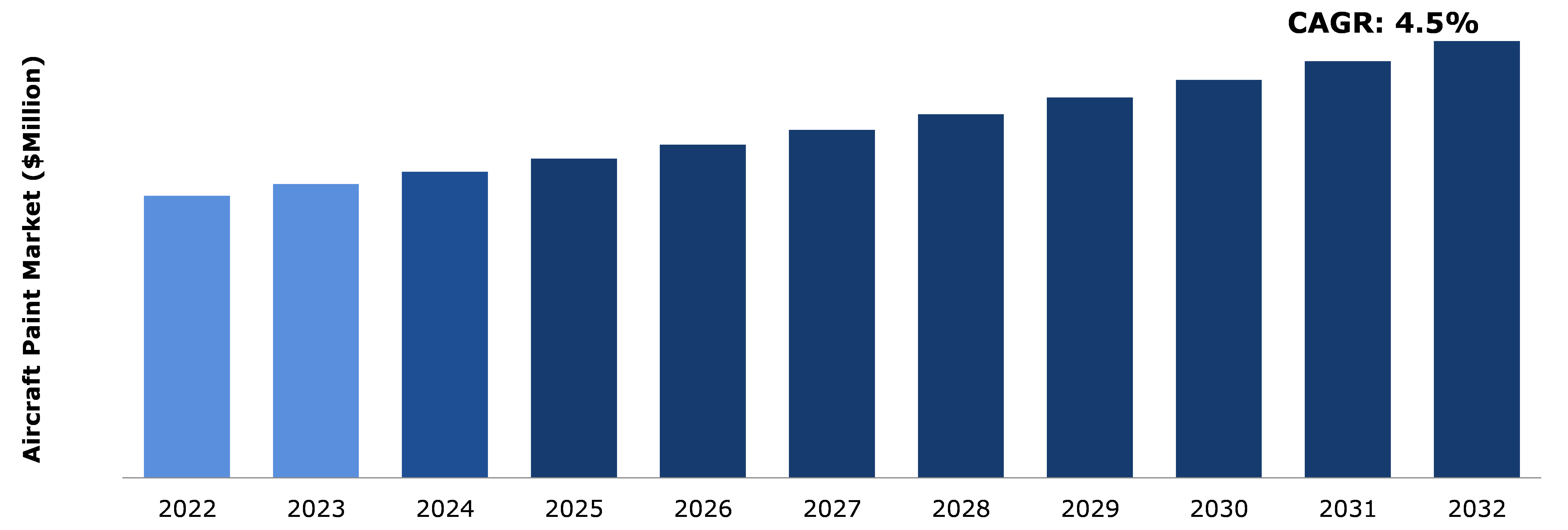

The global aircraft paint market size was $ 4153.6 million in 2022 and is predicted to grow with a CAGR of 4.5%, by generating a revenue of $ 6436.1 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Aircraft Paint Market

The COVID-19 pandemic has had a significant impact on the aircraft paint market. Airlines, facing financial challenges and drastic decrease in passenger demand, deferred or canceled orders for new aircraft. This reduction in new aircraft production directly affects the demand for aircraft paint. With airlines struggling financially, there are expected to be delays in routine maintenance, including repainting of aircraft. This impacts on the demand for paint products and services in the short term. The pandemic caused disruptions in global supply chains, affecting the production and distribution of various materials, including those used in aircraft paint. This leads to rise in costs and delays in the availability of paint products. Moreover, airlines and aircraft operators faced financial pressures, leading to a focus on cost-cutting measures. These influences decisions related to aircraft appearance and paint, with operators potentially opting for more cost-effective solutions. Airlines faced severe financial challenges, with some carriers grounding a significant portion of their fleets. This had a direct impact on the demand for repainting services, as grounded aircraft might not have undergone routine repainting as scheduled.

Rising Demand for Aircraft Fleet Expansion and Modernization to Drive the Market Growth

The growth of the global aviation industry, including both commercial and military sectors, often leads to an increase in the demand for aircraft paint. As airlines and defense forces acquire new aircraft to meet growing passenger demands or enhance military capabilities, there is a parallel need for high-quality paint to protect and enhance the appearance of these new assets. Airlines often use aircraft exteriors as a canvas for branding and marketing. The exterior appearance of an aircraft is a vital aspect of an airline's image, and high-quality paint is crucial for creating a visually appealing and recognizable livery. As airlines expand their fleets, they invest in updated or consistent branding, driving demand for aircraft paint. Moreover, aircraft painting is about aesthetics and plays a crucial role in protecting the aircraft from environmental factors. Regulatory bodies impose strict guidelines regarding the type of paint, application processes, and maintenance to ensure the safety & longevity of the aircraft. As fleets expand, compliance with these regulations becomes even more critical, leading to increased demand for paint that meets or exceeds these standards. In addition to new aircraft acquisitions, modernization of existing fleets through maintenance and refurbishment projects contributes significantly to the demand for aircraft paint. Airlines and military organizations choose to repaint aircraft during scheduled maintenance to ensure they meet safety & aesthetic standards and extend the operational life of the aircraft. Furthermore, drivers of the aircraft paint market in the context of fleet expansion and modernization are interconnected with the broader trends in the aviation industry, regulations, technological advancements, and external economic & geopolitical factors.

Regulatory Compliance and High Manufacturing Cost to Restrain the Market Growth

The aviation industry operates in a dynamic regulatory environment where standards and regulations change frequently. Manufacturers in the aircraft paint market stay abreast of these changes to ensure compliance. Increasing focus on environmental sustainability and reduction of harmful emissions lead to stricter regulations regarding the composition of aircraft paints. This necessitates the reformulation of existing products or the development of entirely new, eco-friendly coatings. Safety is paramount in aviation, and any modifications to safety standards significantly impact the approval & use of specific paint formulations. Manufacturers need to invest in R&D to ensure that their products meet evolving safety requirements. Furthermore, significant R&D investments are often necessary to create aircraft paint that fulfills the rigorous demands of the aviation industry. This includes meeting stringent requirements such as durability, resistance to harsh environmental conditions, and adherence to safety standards. The manufacturing process for high-quality aircraft paint involves advanced technologies and materials, contributing to higher production costs. This is expected to be a deterrent for both manufacturers and airlines, particularly when cost-cutting measures are prioritized. These are the major factors anticipated to hamper the aircraft paint market growth.

Growing Adoption of Fuel Efficiency, Lightweight Materials and Technological Advancements to Drive Excellent Opportunities

As the aerospace industry continues to prioritize fuel efficiency, there is a growing need for coatings that contribute to improved aerodynamics. Advanced coatings with low drag properties play a crucial role in reducing fuel consumption by enhancing the overall efficiency of the aircraft. Moreover, the development of self-healing coatings is a notable advancement. These coatings repair minor damages, such as scratches and small punctures, automatically. In the context of aircraft, this contributes to the overall maintenance & longevity of the paint job, reducing the need for frequent repainting. With the push toward lightweight aircraft materials, demand for paint formulations that are lightweight yet durable becomes crucial. Lightweight coatings contribute to the overall goal of reducing the aircraft's weight, leading to improved fuel efficiency. The aerospace industry is subject to stringent environmental regulations. Manufacturers and operators are anticipated to prefer coatings that comply with these regulations and surpass them in terms of environmentally friendly and sustainable. Coatings that help smooth the surfaces of an aircraft reduce drag, thereby improving fuel efficiency. Innovations in paint formulations that enable smoother surfaces without compromising on durability are expected to be in high demand. In addition, coatings compatible with advanced composite materials, which are increasingly used in modern aircraft construction, is expected to be essential. These coatings complement the properties of these materials, ensuring both protection and adherence. Moreover, the aircraft paint market has significant opportunities in contributing to fuel efficiency, leveraging lightweight materials, and embracing technological advancements. The development and adoption of innovative coatings plays a crucial role in shaping the future of the aerospace industry.

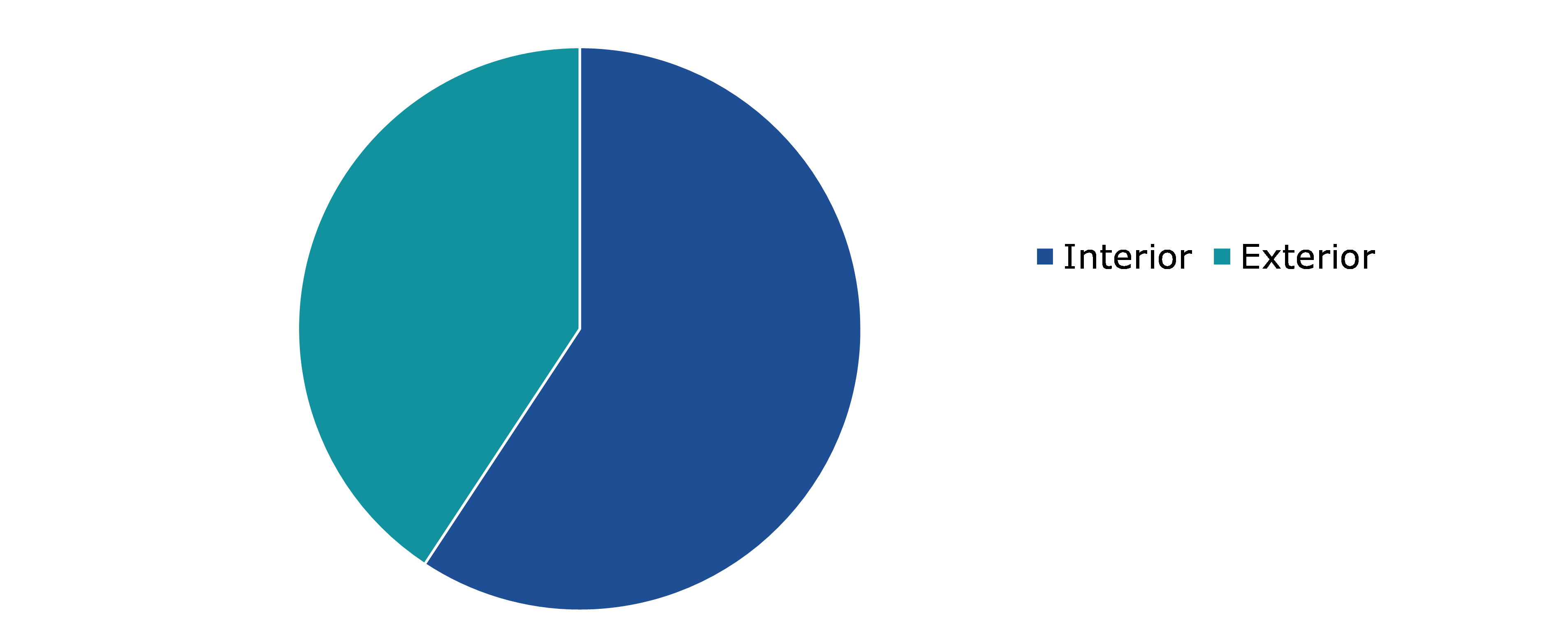

Global Aircraft Paint Market Share, by Application, 2022

Source: Research Dive Analysis

The interior sub-segment accounted for the highest market share in 2022. Airlines often seek aesthetically pleasing interior designs to enhance the overall passenger experience. This includes the selection of attractive and durable interior paints. Compliance with aviation regulations and safety standards is a significant driver. Interior paints meet specific requirements for flame resistance, low smoke & toxicity, and other safety considerations. Aircraft interiors are subjected to significant wear and tear due to frequent use. The demand for durable paints that withstand scratches, abrasions, and cleaning agents is high. This helps in reducing maintenance costs and increasing the lifespan of interior components. Moreover, aircraft manufacturers and airlines are always looking for ways to reduce weight to enhance fuel efficiency. Paints that are lightweight while maintaining durability are preferred. Advances in paint formulations, such as the development of nanotechnology-based coatings or environmentally friendly options, drive the market growth as they offer improved performance and sustainability. Airlines seek custom paint solutions to differentiate their fleets or align with brand identities. This trend drives demand for a variety of colors, finishes, and textures. As airlines retrofit and upgrade their existing fleets, there is a demand for interior components, including paints, that meet modern standards and designs. The overall growth in the aviation sector, driven by economic expansion and increase in air travel, boost demand for new aircraft and, consequently, the need for interior paints.

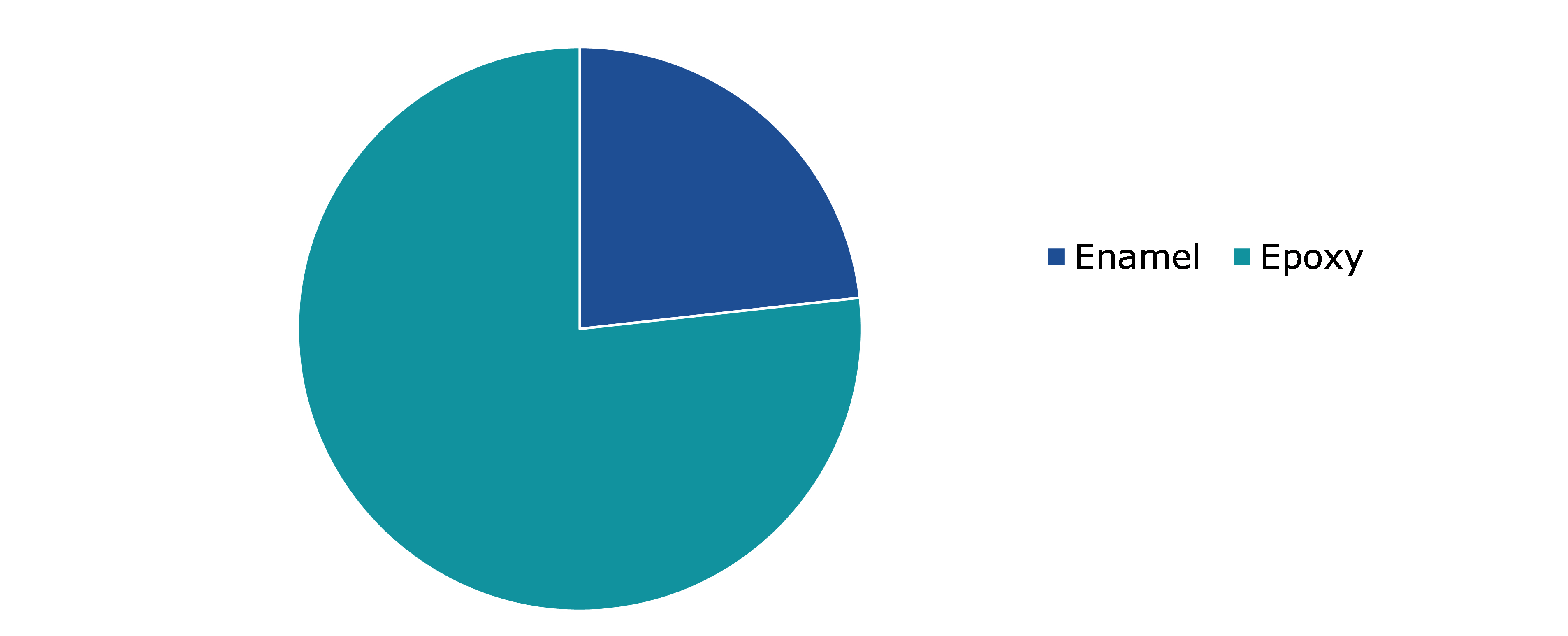

Global Aircraft Paint Market Share, by Type, 2022

Source: Research Dive Analysis

The enamel sub-segment accounted for the highest market share in 2022. Enamel coatings are known for their ability to provide effective corrosion protection. Aircraft are exposed to various environmental factors during their operation, including moisture, salt, and other corrosive elements. Enamel coatings act as a barrier, preventing these elements from reaching the underlying metal surfaces and causing corrosion. Enamel paints are favored for their durability and long-lasting performance. Aircraft undergo extreme conditions, including high-altitude flights, temperature variations, and exposure to UV radiation. Enamel coatings are formulated to withstand these harsh conditions and maintain their appearance and protective properties over an extended period. Enamel coatings often exhibit resistance to various chemicals, including aviation fuels, hydraulic fluids, and cleaning agents. This resistance is crucial for protecting the aircraft's exterior from potential damage caused by exposure to such substances. Enamel paints are chosen for their functional properties and for their aesthetic appeal. The appearance of an aircraft is a significant consideration for both commercial and military applications. Enamel coatings allow for a smooth and glossy finish, contributing to the overall visual appeal of the aircraft.

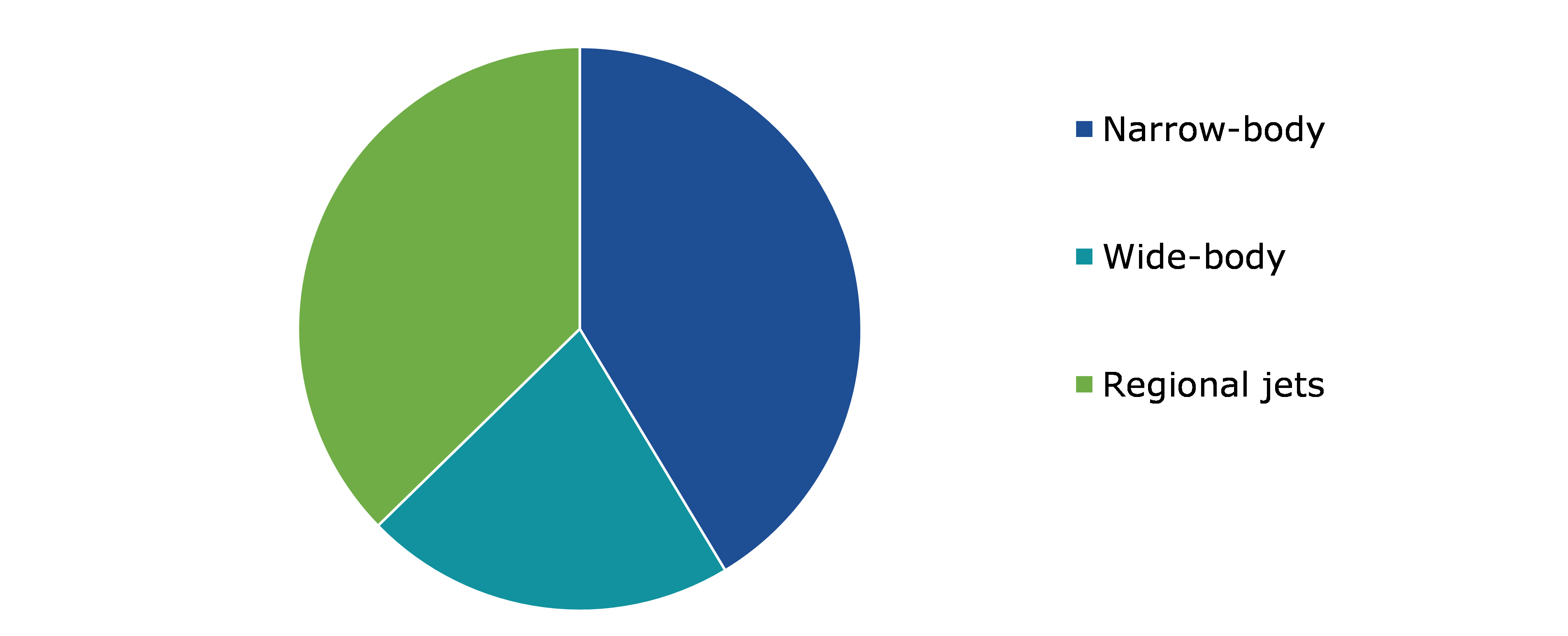

Global Aircraft Paint Market Share, by Aircraft Type, 2022

Source: Research Dive Analysis

The narrow-body sub-segment accounted for the highest market share in 2022. Airlines often expand their fleets to meet growing demand for air travel. As narrow-body aircraft are commonly used for short to medium-haul routes, an increase in the number of these aircraft in service drives the demand for aircraft paint. Airlines invest in upgrading and repainting their existing narrow-body aircraft to maintain a fresh and modern appearance. Repainting is done for aesthetic reasons and for protective purposes, helping to prevent corrosion and extend the life of the aircraft. Airlines use aircraft liveries and branding as a key component of their marketing strategy. Changes in corporate branding or the desire to differentiate themselves from competitors drive airlines to repaint their aircraft. Regulatory authorities often have guidelines and regulations regarding aircraft maintenance, including the condition of the aircraft's exterior. Moreover, airlines comply with these regulations, leading to regular maintenance, including repainting. With a growing focus on environmental sustainability, there is rise in demand for eco-friendly and low-VOC (volatile organic compounds) paint solutions. Airlines choose paints that are more environmentally friendly to align with corporate social responsibility goals.

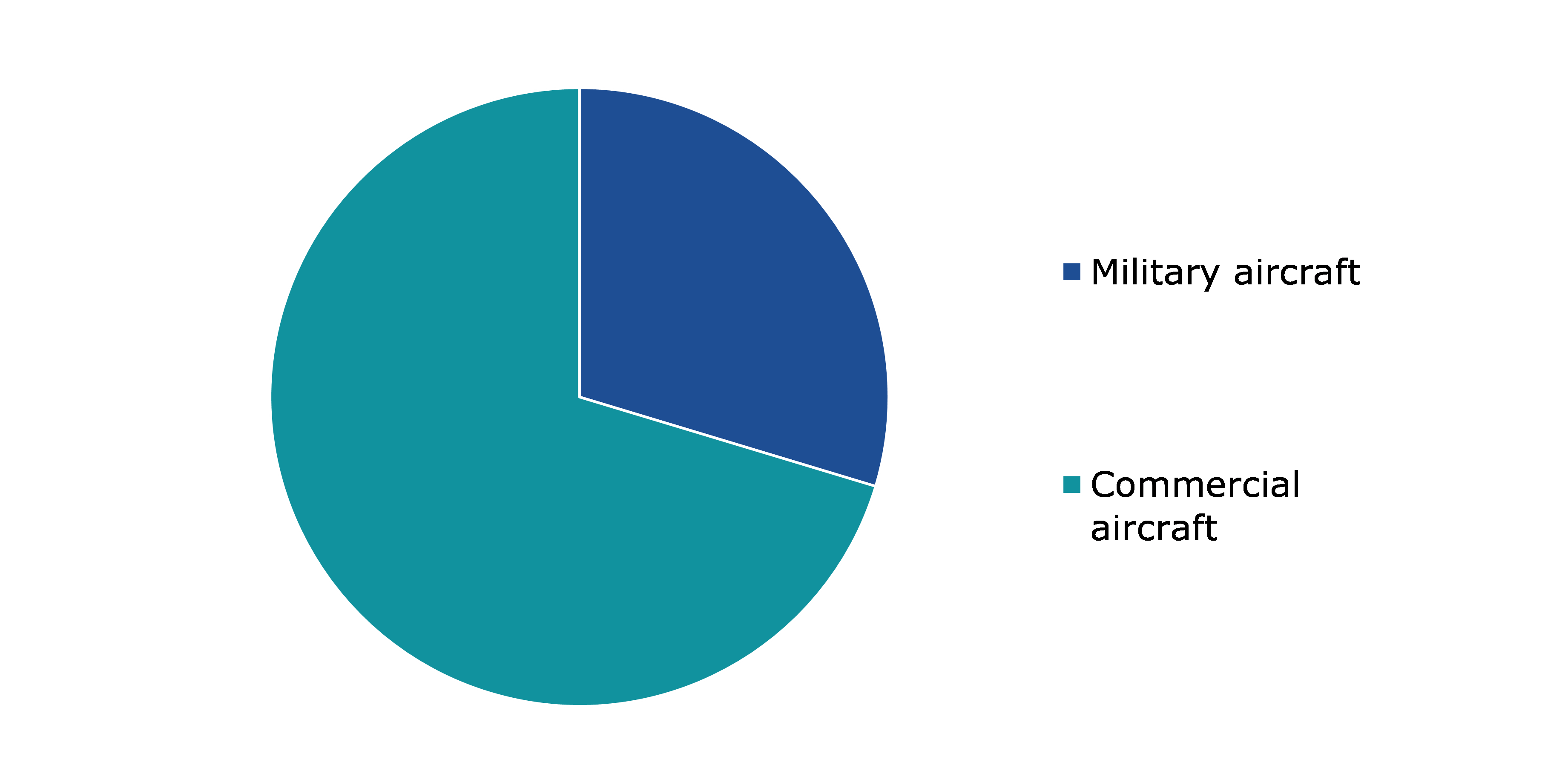

Global Aircraft Paint Market Share, by End-User, 2022

Source: Research Dive Analysis

The military aircraft sub-segment accounted for the highest market share in 2022. Many military aircraft incorporate stealth technology to minimize radar cross-section. Specialized coatings are developed to absorb or diffuse radar waves, reducing the chances of detection. The demand for advanced stealth coatings is a significant driver in this market. Military aircraft often operate in diverse and harsh environments, including maritime regions and deserts. Coatings that provide excellent corrosion resistance are crucial to protect the aircraft's structural integrity and increase its lifespan. Military aircraft need to withstand extreme weather conditions, from freezing cold to scorching heat. Coatings that resist UV radiation, temperature variations, and other weather-related factors are essential. Military aircraft encounter various chemicals, such as fuels and hydraulic fluids. Coatings need to be resistant to these substances to maintain the aircraft's performance and appearance. Depending on the mission requirements, military aircraft is expected to be painted with camouflage patterns for strategic purposes. Moreover, tactical coatings are used to enhance the aircraft's ability to operate in specific environments without getting easily detected. Military aircraft coatings comply with various regulations and standards related to environmental impact, safety, and performance. Adherence to these standards is a key driver in the development and adoption of specific coatings.

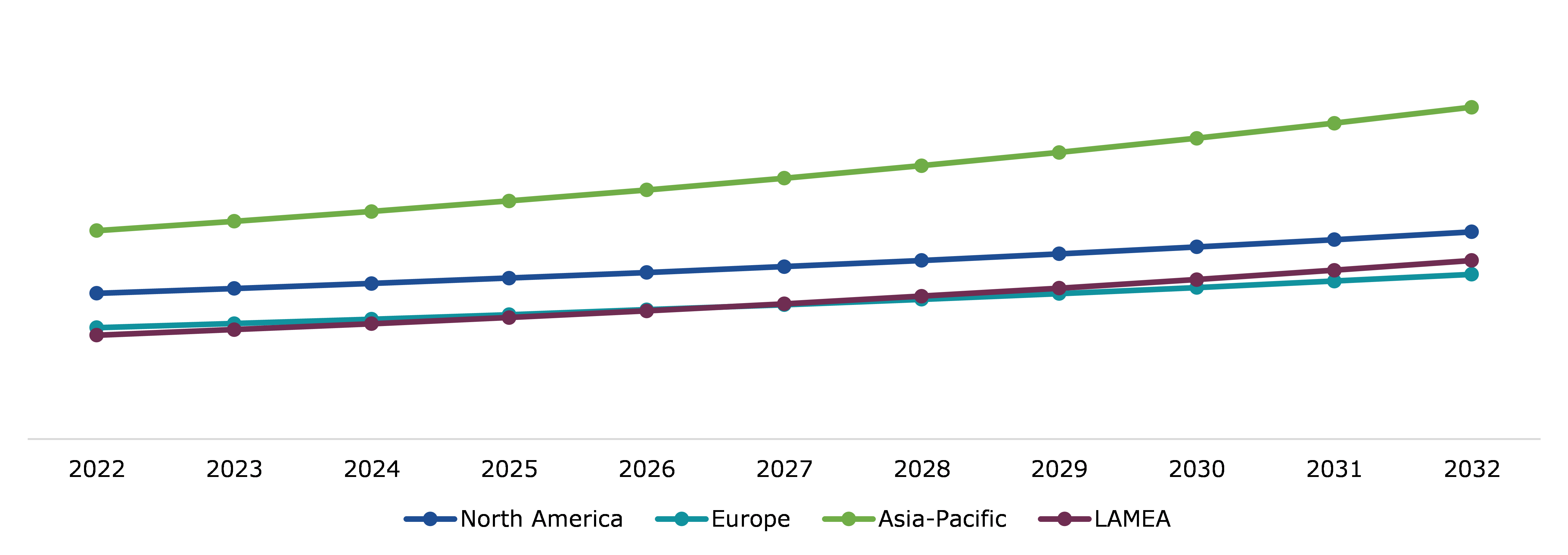

Global Aircraft Paint Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The North America aircraft paint market generated the highest revenue in 2022. The demand for aircraft paint is often linked to the growth in the number of aircraft in service. As airlines and other operators expand their fleets, there is a corresponding need for painting and repainting services. Adherence to safety and environmental regulations often requires aircraft to undergo regular painting and maintenance. This drives the demand for specific types of aircraft paint that meet regulatory standards. Innovations in paint technologies, such as the development of environmentally friendly and more durable coatings, drive market growth. Airlines and operators invest in new paint technologies to improve the efficiency and longevity of their aircraft. Moreover, they often use the external appearance of their aircraft to reinforce their brand identity. Changes in branding or the introduction of new livery drive demand for repainting services. Moreover, to obtain the most current and region-specific information on the drivers of the North America aircraft paint market, you want to refer to industry reports, market analyses, and updates from reputable sources in the aviation and aerospace sector.

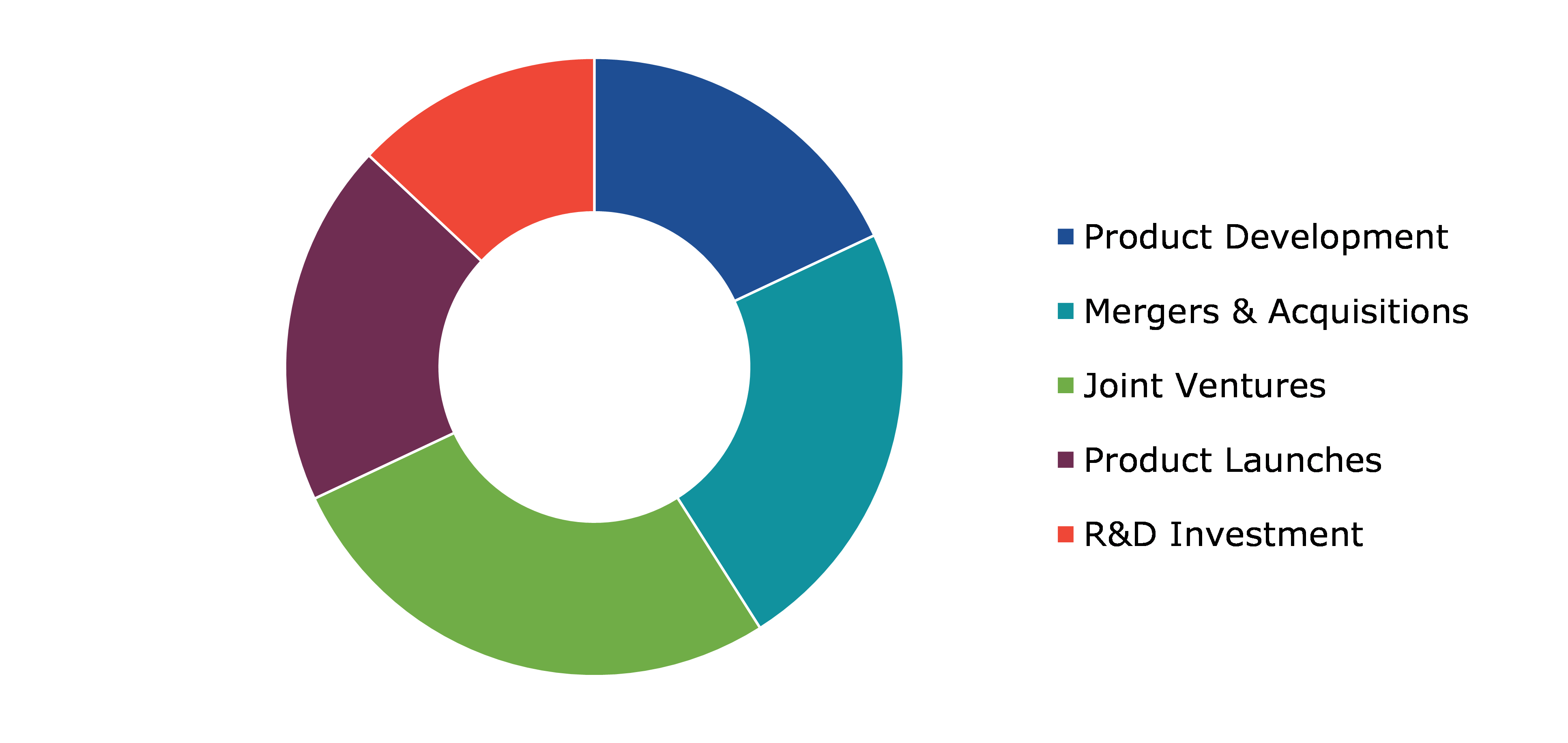

Competitive Scenario in the Global Aircraft Paint Market

Investment and agreement are common strategies followed by major market players. In July 2023, PPG announced that it partnered with Satys, a French industrial group active in aircraft sealing, painting, and surface treatment, to provide electrocoating (e-coat) of original equipment manufacturer (OEM) aircraft parts.

Source: Research Dive Analysis

Some of the companies operating in the aircraft paint market are APS Materials Inc, United coatings Group, PPG Industries Inc., AandA Thermal Spray Coatings, Praxair S.T. Technology Inc, DowDuPont Inc, Indestructible Paint Limited, OC Oerlikon Corporation AG., TURBOCAM Inc, Chromalloy Gas Turbine LLC.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Application |

|

| Segmentation by Type |

|

| Segmentation by Aircraft Type |

|

| Segmentation by End-User |

|

| Key Companies Profiled |

|

Q1. What is the size of the global aircraft paint market?

A. The size of the global aircraft paint market was over $ 4153.6 million in 2022 and is projected to reach $ 6436.1 million by 2032.

Q2. Which are the major companies in the aircraft paint market?

A. APS Materials Inc, United Coatings Group, PPG Industries Inc., are some of the key players in the global aircraft paint market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific aircraft paint market?

A. The Asia-Pacific aircraft paint market is anticipated to grow at 4.5% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more in R&D practices?

A. A and A Thermal Spray Coatings, Praxair S.T. Technology Inc, are the companies investing more in R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global aircraft paint market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive rivalry intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on Aircraft Paints Market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Aircraft Paint Market Analysis, by Application

5.1. Overview

5.2. Interior

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. Exterior

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. Research Dive Exclusive Insights

5.4.1. Market attractiveness

5.4.2. Competition heatmap

6. Aircraft Paint Market Analysis, by Type

6.1. Enamel

6.1.1. Definition, key trends, growth factors, and opportunities

6.1.2. Market size analysis, by region, 2022-2032

6.1.3. Market share analysis, by country, 2022-2032

6.2. Enamel

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Research Dive Exclusive Insights

6.3.1. Market attractiveness

6.3.2. Competition heatmap

7. Aircraft Paint Market Analysis, by Aircraft Type

7.1. Narrow-body

7.1.1. Definition, key trends, growth factors, and opportunities

7.1.2. Market size analysis, by region, 2022-2032

7.1.3. Market share analysis, by country, 2022-2032

7.2. Wide-body

7.2.1. Definition, key trends, growth factors, and opportunities

7.2.2. Market size analysis, by region, 2022-2032

7.2.3. Market share analysis, by country, 2022-2032

7.3. Regional jets

7.3.1. Definition, key trends, growth factors, and opportunities

7.3.2. Market size analysis, by region, 2022-2032

7.3.3. Market share analysis, by country, 2022-2032

7.4. Research Dive Exclusive Insights

7.4.1. Market attractiveness

7.4.2. Competition heatmap

8. Aircraft Paint Market Analysis, by End-User

8.1. Military aircraft

8.1.1. Definition, key trends, growth factors, and opportunities

8.1.2. Market size analysis, by region, 2022-2032

8.1.3. Market share analysis, by country, 2022-2032

8.2. Commercial aircraft

8.2.1. Definition, key trends, growth factors, and opportunities

8.2.2. Market size analysis, by region, 2022-2032

8.2.3. Market share analysis, by country, 2022-2032

8.3. Research Dive Exclusive Insights

8.3.1. Market attractiveness

8.3.2. Competition heatmap

9. Aircraft Paint Market, by Region

9.1. North America

9.1.1. U.S.

9.1.1.1. Market size analysis, by Application, 2022-2032

9.1.1.2. Market size analysis, by Type, 2022-2032

9.1.1.3. Market size analysis, by Aircraft Type, 2022-2032

9.1.1.4. Market size analysis, by End-User, 2022-2032

9.1.2. Canada

9.1.2.1. Market size analysis, by Application, 2022-2032

9.1.2.2. Market size analysis, by Type, 2022-2032

9.1.2.3. Market size analysis, by Aircraft Type, 2022-2032

9.1.2.4. Market size analysis, by End-User, 2022-2032

9.1.3. Mexico

9.1.3.1. Market size analysis, by Application, 2022-2032

9.1.3.2. Market size analysis, by Type, 2022-2032

9.1.3.3. Market size analysis, by Aircraft Type, 2022-2032

9.1.3.4. Market size analysis, by End-User, 2022-2032

9.1.4. Research Dive Exclusive Insights

9.1.4.1. Market attractiveness

9.1.4.2. Competition heatmap

9.2. Europe

9.2.1. Germany

9.2.1.1. Market size analysis, by Application, 2022-2032

9.2.1.2. Market size analysis, by Type, 2022-2032

9.2.1.3. Market size analysis, by Aircraft Type, 2022-2032

9.2.1.4. Market size analysis, by End-User, 2022-2032

9.2.2. UK

9.2.2.1. Market size analysis, by Application, 2022-2032

9.2.2.2. Market size analysis, by Type, 2022-2032

9.2.2.3. Market size analysis, by Aircraft Type, 2022-2032

9.2.2.4. Market size analysis, by End-User, 2022-2032

9.2.3. France

9.2.3.1. Market size analysis, by Application, 2022-2032

9.2.3.2. Market size analysis, by Type, 2022-2032

9.2.3.3. Market size analysis, by Aircraft Type, 2022-2032

9.2.3.4. Market size analysis, by End-User, 2022-2032

9.2.4. Spain

9.2.4.1. Market size analysis, by Application, 2022-2032

9.2.4.2. Market size analysis, by Type, 2022-2032

9.2.4.3. Market size analysis, by Aircraft Type, 2022-2032

9.2.4.4. Market size analysis, by End-User, 2022-2032

9.2.5. Italy

9.2.5.1. Market size analysis, by Application, 2022-2032

9.2.5.2. Market size analysis, by Type, 2022-2032

9.2.5.3. Market size analysis, by Aircraft Type, 2022-2032

9.2.5.4. Market size analysis, by End-User, 2022-2032

9.2.6. Rest of Europe

9.2.6.1. Market size analysis, by Application, 2022-2032

9.2.6.2. Market size analysis, by Type, 2022-2032

9.2.6.3. Market size analysis, by Aircraft Type, 2022-2032

9.2.6.4. Market size analysis, by End-User, 2022-2032

9.2.7. Research Dive Exclusive Insights

9.2.7.1. Market attractiveness

9.2.7.2. Competition heatmap

9.3. Asia-Pacific

9.3.1. China

9.3.1.1. Market size analysis, by Application, 2022-2032

9.3.1.2. Market size analysis, by Type, 2022-2032

9.3.1.3. Market size analysis, by Aircraft Type, 2022-2032

9.3.1.4. Market size analysis, by End-User, 2022-2032

9.3.2. Japan

9.3.2.1. Market size analysis, by Application, 2022-2032

9.3.2.2. Market size analysis, by Type, 2022-2032

9.3.2.3. Market size analysis, by Aircraft Type, 2022-2032

9.3.2.4. Market size analysis, by End-User, 2022-2032

9.3.3. India

9.3.3.1. Market size analysis, by Application, 2022-2032

9.3.3.2. Market size analysis, by Type, 2022-2032

9.3.3.3. Market size analysis, by Aircraft Type, 2022-2032

9.3.3.4. Market size analysis, by End-User, 2022-2032

9.3.4. Australia

9.3.4.1. Market size analysis, by Application, 2022-2032

9.3.4.2. Market size analysis, by Type, 2022-2032

9.3.4.3. Market size analysis, by Aircraft Type, 2022-2032

9.3.4.4. Market size analysis, by End-User, 2022-2032

9.3.5. South Korea

9.3.5.1. Market size analysis, by Application, 2022-2032

9.3.5.2. Market size analysis, by Type, 2022-2032

9.3.5.3. Market size analysis, by Aircraft Type, 2022-2032

9.3.5.4. Market size analysis, by End-User, 2022-2032

9.3.6. Rest of Asia-Pacific

9.3.6.1. Market size analysis, by Application, 2022-2032

9.3.6.2. Market size analysis, by Type, 2022-2032

9.3.6.3. Market size analysis, by Aircraft Type, 2022-2032

9.3.6.4. Market size analysis, by End-User, 2022-2032

9.3.7. Research Dive Exclusive Insights

9.3.7.1. Market attractiveness

9.3.7.2. Competition heatmap

9.4. LAMEA

9.4.1. Brazil

9.4.1.1. Market size analysis, by Application, 2022-2032

9.4.1.2. Market size analysis, by Type, 2022-2032

9.4.1.3. Market size analysis, by Aircraft Type, 2022-2032

9.4.1.4. Market size analysis, by End-User, 2022-2032

9.4.2. Saudi Arabia

9.4.2.1. Market size analysis, by Application, 2022-2032

9.4.2.2. Market size analysis, by Type, 2022-2032

9.4.2.3. Market size analysis, by Aircraft Type, 2022-2032

9.4.2.4. Market size analysis, by End-User, 2022-2032

9.4.3. UAE

9.4.3.1. Market size analysis, by Application, 2022-2032

9.4.3.2. Market size analysis, by Type, 2022-2032

9.4.3.3. Market size analysis, by Aircraft Type, 2022-2032

9.4.3.4. Market size analysis, by End-User, 2022-2032

9.4.4. South Africa

9.4.4.1. Market size analysis, by Application, 2022-2032

9.4.4.2. Market size analysis, by Type, 2022-2032

9.4.4.3. Market size analysis, by Aircraft Type, 2022-2032

9.4.4.4. Market size analysis, by End-User, 2022-2032

9.4.5. Rest of LAMEA

9.4.5.1. Market size analysis, by Application, 2022-2032

9.4.5.2. Market size analysis, by Type, 2022-2032

9.4.5.3. Market size analysis, by Aircraft Type, 2022-2032

9.4.5.4. Market size analysis, by End-User, 2022-2032

9.4.6. Research Dive Exclusive Insights

9.4.6.1. Market attractiveness

9.4.6.2. Competition heatmap

10. Competitive Landscape

10.1. Top winning strategies, 2022

10.1.1. By strategy

10.1.2. By year

10.2. Strategic overview

10.3. Market share analysis, 2022

11. Company Profiles

11.1. Praxair S.T. Technology Inc

11.1.1. Overview

11.1.2. Business segments

11.1.3. Product portfolio

11.1.4. Financial performance

11.1.5. Recent developments

11.1.6. SWOT analysis

11.2. AandA Thermal Spray Coatings

11.2.1. Overview

11.2.2. Business segments

11.2.3. Product portfolio

11.2.4. Financial performance

11.2.5. Recent developments

11.2.6. SWOT analysis

11.3. TURBOCAM Inc

11.3.1. Overview

11.3.2. Business segments

11.3.3. Product portfolio

11.3.4. Financial performance

11.3.5. Recent developments

11.3.6. SWOT analysis

11.4. APS Materials Inc

11.4.1. Overview

11.4.2. Business segments

11.4.3. Product portfolio

11.4.4. Financial performance

11.4.5. Recent developments

11.4.6. SWOT analysis

11.5. United Coatings Group

11.5.1. Overview

11.5.2. Business segments

11.5.3. Product portfolio

11.5.4. Financial performance

11.5.5. Recent developments

11.5.6. SWOT analysis

11.6. DowDuPont Inc

11.6.1. Overview

11.6.2. Business segments

11.6.3. Product portfolio

11.6.4. Financial performance

11.6.5. Recent developments

11.6.6. SWOT analysis

11.7. PPG Industries Inc.

11.7.1. Overview

11.7.2. Business segments

11.7.3. Product portfolio

11.7.4. Financial performance

11.7.5. Recent developments

11.7.6. SWOT analysis

11.8. Indestructible Paint Limited

11.8.1. Overview

11.8.2. Business segments

11.8.3. Product portfolio

11.8.4. Financial performance

11.8.5. Recent developments

11.8.6. SWOT analysis

11.9. Chromalloy Gas Turbine LLC

11.9.1. Overview

11.9.2. Business segments

11.9.3. Product portfolio

11.9.4. Financial performance

11.9.5. Recent developments

11.9.6. SWOT analysis

11.10. OC Oerlikon Corporation AG.

11.10.1. Overview

11.10.2. Business segments

11.10.3. Product portfolio

11.10.4. Financial performance

11.10.5. Recent developments

11.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com