Agriculture Insurance Market Report

RA09177

Agriculture Insurance Market by Product Type (Multi-Peril Crop Insurance (MPCI), Crop-Hail Insurance, Livestock Insurance, and Others), Distribution Channel (Banks, Insurance Companies, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Agriculture Insurance Overview

Agriculture stands as the most crucial industry worldwide, with its impact on economic and social areas growing even more significant due to the rising global population. Agricultural insurance plays a key role in mitigating economic losses resulting from crop and animal damage or loss due to adverse natural and other factors. This insurance safeguards specific crops and livestock against defined natural occurrences like droughts, floods, pests, and winds. However, the scope of agricultural insurance goes beyond this, encompassing diverse domains such as aquaculture, forestry, high-value animals like pedigree breeds, greenhouse crops, and others. This inclusive approach benefits both individuals and enterprises engaged in agricultural production, sustaining their resilience against unforeseen challenges.

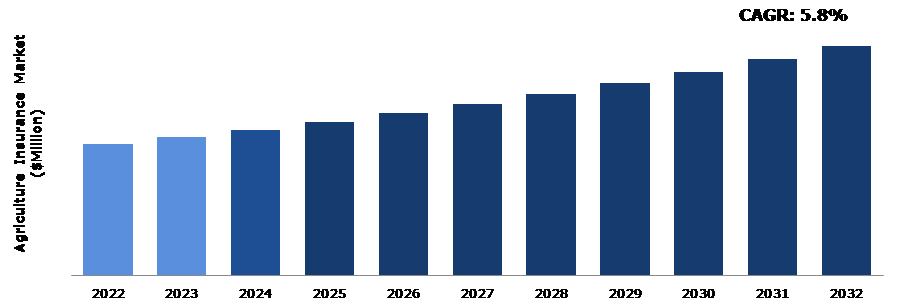

Global Agriculture Insurance Market Analysis

The global agriculture insurance market size was $38,502.60 million in 2022 and is predicted to grow with a CAGR of 5.8%, by generating a revenue of $67,437.20 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Agriculture Insurance Market

The COVID-19 pandemic emerged as a global health crisis, with profound impacts on the world economy. The pandemic also had a significant impact on the food and agriculture sector. While the food supply chain was undisrupted, the implementation of measures to control the spread of the virus across various countries disrupted the flow of agri-food products, both domestically and internationally. This sector additionally witnessed shifts in demand for certain products. During the pandemic, the agriculture insurance industry faced unusual challenges. This global scenario urged insurance companies to embrace new technologies and solutions, driving an increased focus on procedural and protocol adjustments such as digitization, data analytics, blockchain technology, and others.

In the survey conducted by Agroinsurance International between July 2020 and February 2021, it was revealed that the crop and livestock insurance sales season in 2020 remained almost similar compared to previous years for many companies. Surprisingly, farmers in the majority of countries did not alter their methods for obtaining crop insurance in response to the COVID-19 pandemic. They continued to use insurance as a risk management tool, with farmers signing up for agricultural insurance schemes or renewing their coverage.

Unpredictable Weather Conditions to Drive the Growth of the Market

Farming involves uncertainties, primarily stemming from the dependence of most farmers on weather conditions for successful crop production. These risks can have profound negative impacts on farmers' income, stability of food supply, and overall advancement and competitiveness of the agricultural sector, particularly for major commercial farms and marginal farmers. Over the past 5 to 6 years, the world has witnessed a rise in frequency of floods, droughts, and pandemics, which have caused a tremendous amount of damage to the agricultural sector. These events have underscored the importance of the agriculture insurance.

The frequency of these occurrences has led farmers across the globe to express keen interest in obtaining insurance coverage for their crops and related activities, increasing their sense of security. Consequently, the demand for agricultural insurance is experiencing unprecedented growth. This surge can be attributed to agricultural insurance's comprehensive coverage of various risk factors, particularly those related to weather hazards like floods, droughts, and hail. Agricultural insurance providers get benefited by offering coverage for an extensive range of risk factors regarding the weather conditions. This approach helps them to attract a larger customer base, aligned with the increased demand arising from the increased awareness regarding the risks posed by unpredictable weather patterns.

Inability to Reach Marginal Farmers to Restrain the Growth of the Market

The agriculture insurance market faces a substantial constraint driven by the significant gap in insurance coverage for smallholder farmers. These farmers encounter a multitude of unpredictable challenges and issues that can severely impact their income and overall quality of life. These challenges encompass unforeseen agricultural events such as market fluctuations, price volatility, pest infestations, and disease outbreaks. Globally, the limitation is evident in the fact that less than 20% of smallholder farmers have access to any type of crop insurance. In Sub-Saharan Africa, the coverage gap becomes much more significant, falling to fewer than 3%. In Asia, nearly 78% of marginal farmers lack agricultural insurance. Latin America, too, has this dilemma, with more than 67% of farmers in the region still uninsured.

On the demand side, a notable adoption barrier is the limited awareness regarding insurance services and a challenge intensified by the less availability of financial services in rural areas. Insurance premium costs and the inconvenience of traveling to urban centers for services and claims submission have posed obstacles to smallholder farmers seeking insurance. Furthermore, the existing insurance offerings often fail to align with farmers' specific needs. There is also a deficit of trust in providers and a low expectation of receiving payouts among marginal farmers. These circumstances depict that agriculture insurance providers are hindered from tapping into the potential market of marginal farmer insurance buyers, impeding the growth of the industry.

Developing Index-Based Insurance Plans to Create Excellent Opportunities in the Market

Index-based agriculture insurance, also known as parametric agriculture insurance, is a type of insurance that compensates farmers based on specific predetermined indices or parameters, rather than individual losses. Instead of relying on traditional loss assessment methods, which can be time-consuming and costly, index-based insurance uses easily measurable and objective variables, such as weather data or satellite imagery, to generate payouts. This approach minimizes weather-based risks on agricultural production, making index-based insurance solutions for agriculture an attractive alternative. Index-based weather insurance products can effectively substitute conventional agricultural insurance products. Index-based agricultural insurance payouts are typically faster since they rely on readily available data, reducing the time farmers need to wait for compensation. This factor attracts more farmers to buy the insurance, while also avoiding administrative costs for the agriculture insurer, as there is no need for costly on-site loss assessments. This approach makes the agriculture insurance more affordable and appealing to a broader customer base.

The payout mechanism in index-based insurance is simple and based on predetermined parameters, making it easier for farmers to understand the terms of their coverage. This simplicity also reduces the efforts required by the insurance company. The use of indexes in the most efficient weather insurance plans ensures their long-lasting effectiveness, providing an excellent opportunity for agricultural insurance providers to scale their businesses.

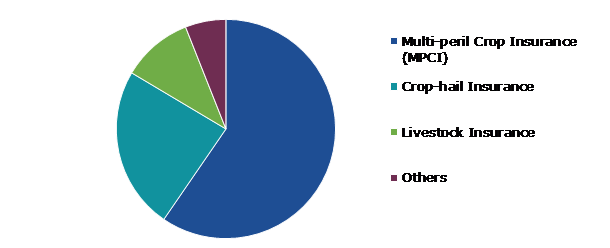

Global Agriculture Insurance Market Share, by Product Type, 2022

Source: Research Dive Analysis

The multi-peril crop insurance (MPCI) sub-segment accounted for the highest market share in 2022. Multi-peril crop insurance policies protect agricultural producers against a variety of naturally occurring hazards. MPCI insurance plans cover production losses or a combination of yield and price coverage. In addition to the dangers covered by ordinary loss of yield coverage, these combination plans cover value loss owing to a change in market price throughout the crop insurance period. The multi-peril insurance policy covers a wide variety of crops. Producers can tailor their insurance by selecting price alternatives, coverage levels, and a variety of other program features to create an insurance package that is unique to their business. The multi-peril crop insurance stands as a robust shield, offering farmers comprehensive protection against an unpredictable and dynamic agricultural landscape. By combining extensive coverage, market responsiveness, and customizable features, these policies provide farmers with the peace of mind to get over challenges while focusing on the growth and prosperity of their agricultural endeavors.

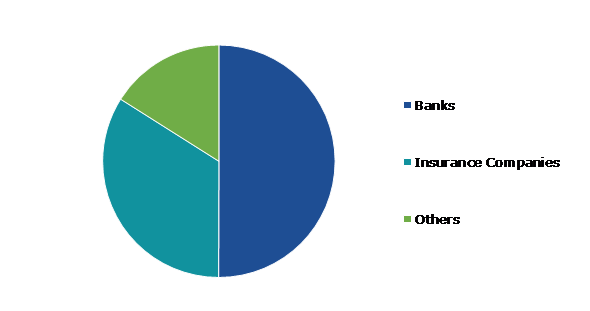

Global Agriculture Insurance Market Share, by Distribution Channel, 2022

Source: Research Dive Analysis

The banks sub-segment accounted for the highest market share in 2022. Banks play a primary role in the distribution of agricultural insurance, as they are a major source of financial resources for farmers globally. As key financial institutions, banks have established themselves as a primary channel for offering insurance products to farmers worldwide. Due to their extensive reach, banks effectively bridge the gap between insurance providers and the agricultural community. By leveraging their established networks and expertise in financial services, banks have emerged as the preferred choice for farmers seeking reliable coverage and seamless access to insurance solutions. This dominance of the banks sub-segment in the market represents the integral partnership between the financial sector and agricultural resilience.

Global Agriculture Insurance Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The North America agriculture insurance market generated the highest revenue in 2022. The agriculture insurance market in North America is a strong and dynamic business that represents the region's dedication to agricultural sustainability and risk management. With its diversified crop and farming practices, North America's agriculture industry faces a variety of problems, ranging from extreme weather occurrences to market volatility. Therefore, the agriculture insurance industry has developed, providing a wide range of coverage alternatives customized to the special needs of North American farmers. Governments and insurance providers in the region have worked together to create innovative solutions that use advanced technologies such as satellite imaging and data analytics to precisely assess risks and promote rapid claims processing. In addition, the rise in awareness about agriculture insurance in the region has prompted businesses to make investments in agriculture insurance products. Therefore, companies are constantly innovating and increasing their product alternatives to cater to the developing needs of the regional market.

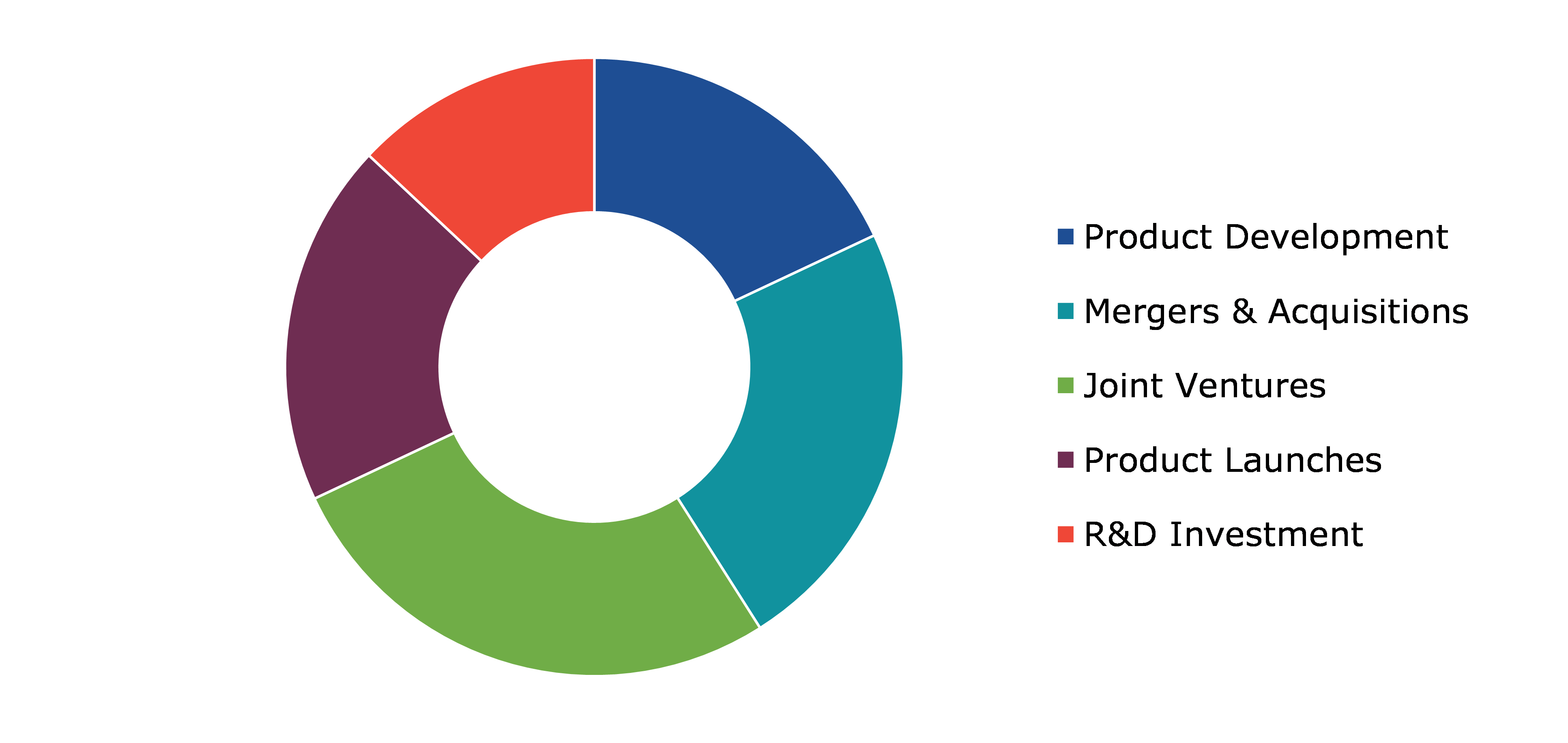

Competitive Scenario in the Global Agriculture Insurance Market

Investment and agreement are common strategies followed by major market players. For instance, in May 2023, according to company authorities, the Agriculture Insurance Company of India (AIC) secured an IRDAI license and will introduce products for the sericulture, aquaculture, and livestock sectors. Under the PMFBY system, sponsored by the Centre and State Governments, AIC already controls 50% of the crop insurance market.

Source: Research Dive Analysis

Some of the leading agriculture insurance market players are Great American Insurance Company Agriculture Insurance Company of India Limited (AIC), Allianz SE Reinsurance, Munich Re Group, Chubb, Sompo International Holdings Ltd, Zurich, AXA, People's Insurance Company (Group) of China Limited, and QBE Insurance Ltd.

| Aspect | Particulars |

| Historical Market Estimations | 2021-2022 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Product Type |

|

| Segmentation by Distribution Channel |

|

| Key Companies Profiled |

|

Q1. What is the size of the global agriculture insurance market?

A. The size of the global agriculture insurance market was over $38,502.60 million in 2022 and is projected to reach $67,437.20 million by 2032.

Q2. Which are the major companies in the agriculture insurance market?

A. Agriculture Insurance Company of India Limited (AIC), Allianz SE Reinsurance, and Munich Re Group are some of the key players in the global agriculture insurance market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific agriculture insurance market?

A. The Asia-Pacific agriculture insurance market is anticipated to grow at 6.5% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Sompo International Holdings Ltd, Zurich, and AXA are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global agriculture insurance market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on the agriculture insurance market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Agriculture Insurance Market Analysis, by Product Type

5.1. Overview

5.2. Multi-peril Crop Insurance (MPCI)

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2023-2032

5.2.3. Market share analysis, by country, 2023-2032

5.3. Crop-hail Insurance

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2023-2032

5.3.3. Market share analysis, by country, 2023-2032

5.4. Livestock Insurance

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2023-2032

5.4.3. Market share analysis, by country, 2023-2032

5.5. Others

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2. Market size analysis, by region, 2023-2032

5.5.3. Market share analysis, by country, 2023-2032

5.6. Research Dive Exclusive Insights

5.6.1. Market attractiveness

5.6.2. Competition heatmap

6. Agriculture Insurance market Analysis, by Distribution Channel

6.1. Banks

6.1.1. Definition, key trends, growth factors, and opportunities

6.1.2. Market size analysis, by region, 2023-2032

6.1.3. Market share analysis, by country, 2023-2032

6.2. Insurance Companies

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2023-2032

6.2.3. Market share analysis, by country, 2023-2032

6.3. Others

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2023-2032

6.3.3. Market share analysis, by country, 2023-2032

6.4. Research Dive Exclusive Insights

6.4.1. Market attractiveness

6.4.2. Competition heatmap

7. Agriculture Insurance market, by Region

7.1. North America

7.1.1. U.S.

7.1.1.1. Market size analysis, by Product Type, 2023-2032

7.1.1.2. Market size analysis, by Distribution Channel, 2023-2032

7.1.2. Canada

7.1.2.1. Market size analysis, by Product Type, 2023-2032

7.1.2.2. Market size analysis, by Distribution Channel, 2023-2032

7.1.3. Mexico

7.1.3.1. Market size analysis, by Product Type, 2023-2032

7.1.3.2. Market size analysis, by Distribution Channel, 2023-2032

7.1.4. Research Dive Exclusive Insights

7.1.4.1. Market attractiveness

7.1.4.2. Competition heatmap

7.2. Europe

7.2.1. Germany

7.2.1.1. Market size analysis, by Product Type, 2023-2032

7.2.1.2. Market size analysis, by Distribution Channel, 2023-2032

7.2.2. Greece

7.2.2.1. Market size analysis, by Product Type, 2023-2032

7.2.2.2. Market size analysis, by Distribution Channel, 2023-2032

7.2.3. France

7.2.3.1. Market size analysis, by Product Type, 2023-2032

7.2.3.2. Market size analysis, by Distribution Channel, 2023-2032

7.2.4. Spain

7.2.4.1. Market size analysis, by Product Type, 2023-2032

7.2.4.2. Market size analysis, by Distribution Channel, 2023-2032

7.2.5. Italy

7.2.5.1. Market size analysis, by Product Type, 2023-2032

7.2.5.2. Market size analysis, by Distribution Channel, 2023-2032

7.2.6. Rest of Europe

7.2.6.1. Market size analysis, by Product Type, 2023-2032

7.2.6.2. Market size analysis, by Distribution Channel, 2023-2032

7.2.7. Research Dive Exclusive Insights

7.2.7.1. Market attractiveness

7.2.7.2. Competition heatmap

7.3. Asia-Pacific

7.3.1. China

7.3.1.1. Market size analysis, by Product Type, 2023-2032

7.3.1.2. Market size analysis, by Distribution Channel, 2023-2032

7.3.2. Japan

7.3.2.1. Market size analysis, by Product Type, 2023-2032

7.3.2.2. Market size analysis, by Distribution Channel, 2023-2032

7.3.3. India

7.3.3.1. Market size analysis, by Product Type, 2023-2032

7.3.3.2. Market size analysis, by Distribution Channel, 2023-2032

7.3.4. Australia

7.3.4.1. Market size analysis, by Product Type, 2023-2032

7.3.4.2. Market size analysis, by Distribution Channel, 2023-2032

7.3.5. South Korea

7.3.5.1. Market size analysis, by Product Type, 2023-2032

7.3.5.2. Market size analysis, by Distribution Channel, 2023-2032

7.3.6. Rest of Asia-Pacific

7.3.6.1. Market size analysis, by Product Type, 2023-2032

7.3.6.2. Market size analysis, by Distribution Channel, 2023-2032

7.3.7. Research Dive Exclusive Insights

7.3.7.1. Market attractiveness

7.3.7.2. Competition heatmap

7.4. LAMEA

7.4.1. Brazil

7.4.1.1. Market size analysis, by Product Type, 2023-2032

7.4.1.2. Market size analysis, by Distribution Channel, 2023-2032

7.4.2. Peru

7.4.2.1. Market size analysis, by Product Type, 2023-2032

7.4.2.2. Market size analysis, by Distribution Channel, 2023-2032

7.4.3. Kenya

7.4.3.1. Market size analysis, by Product Type, 2023-2032

7.4.3.2. Market size analysis, by Distribution Channel, 2023-2032

7.4.4. South Africa

7.4.4.1. Market size analysis, by Product Type, 2023-2032

7.4.4.2. Market size analysis, by Distribution Channel, 2023-2032

7.4.5. Rest of LAMEA

7.4.5.1. Market size analysis, by Product Type, 2023-2032

7.4.5.2. Market size analysis, by Distribution Channel, 2023-2032

7.4.6. Research Dive Exclusive Insights

7.4.6.1. Market attractiveness

7.4.6.2. Competition heatmap

8. Competitive Landscape

8.1. Top winning strategies, 2022

8.1.1. By strategy

8.1.2. By year

8.2. Strategic overview

8.3. Market share analysis, 2021

9. Company Profiles

9.1. Great American Insurance Company

9.1.1. Overview

9.1.2. Business segments

9.1.3. Product portfolio

9.1.4. Financial performance

9.1.5. Recent developments

9.1.6. SWOT analysis

9.2. Agriculture Insurance Company of India Limited (AIC)

9.2.1. Overview

9.2.2. Business segments

9.2.3. Product portfolio

9.2.4. Financial performance

9.2.5. Recent developments

9.2.6. SWOT analysis

9.3. Allianz SE Reinsurance

9.3.1. Overview

9.3.2. Business segments

9.3.3. Product portfolio

9.3.4. Financial performance

9.3.5. Recent developments

9.3.6. SWOT analysis

9.4. Munich Re Group

9.4.1. Overview

9.4.2. Business segments

9.4.3. Product portfolio

9.4.4. Financial performance

9.4.5. Recent developments

9.4.6. SWOT analysis

9.5. Chubb

9.5.1. Overview

9.5.2. Business segments

9.5.3. Product portfolio

9.5.4. Financial performance

9.5.5. Recent developments

9.5.6. SWOT analysis

9.6. Sompo International Holdings Ltd

9.6.1. Overview

9.6.2. Business segments

9.6.3. Product portfolio

9.6.4. Financial performance

9.6.5. Recent developments

9.6.6. SWOT analysis

9.7. Zurich

9.7.1. Overview

9.7.2. Business segments

9.7.3. Product portfolio

9.7.4. Financial performance

9.7.5. Recent developments

9.7.6. SWOT analysis

9.8. AXA

9.8.1. Overview

9.8.2. Business segments

9.8.3. Product portfolio

9.8.4. Financial performance

9.8.5. Recent developments

9.8.6. SWOT analysis

9.9. People's Insurance Company (Group) of China Limited

9.9.1. Overview

9.9.2. Business segments

9.9.3. Product portfolio

9.9.4. Financial performance

9.9.5. Recent developments

9.9.6. SWOT analysis

9.10. QBE Insurance Ltd.

9.10.1. Overview

9.10.2. Business segments

9.10.3. Product portfolio

9.10.4. Financial performance

9.10.5. Recent developments

9.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com