Retail Logistics Market Report

RA09167

Retail Logistics Market by Type (Conventional Retail Logistics and E-commerce Retail Logistics), Solution (Commerce Enablement, Supply Chain Solutions, Reverse Logistics & Liquidation, Transportation Management, and Others), Mode of Transport (Railways, Airways, Roadways, and Waterways), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Retail Logistics Overview

Retail logistics is the process of managing the flow of goods from the source of supply to customers through efficient movement of logistics. Retail logistics system is highly dynamic and customer-focused in nature. There are a wide variety of products in the market and they require a planned approach right from the start line until the point of delivery. Retail logistics ensures that everything is in place to offer better delivery and service at lower costs by way of efficient logistics and added value. The process of logistics can be viewed in terms of two inter-related efforts, inventory flow and information flow. In order to make products available, retailers must manage their logistics in terms of product movement and demand management.

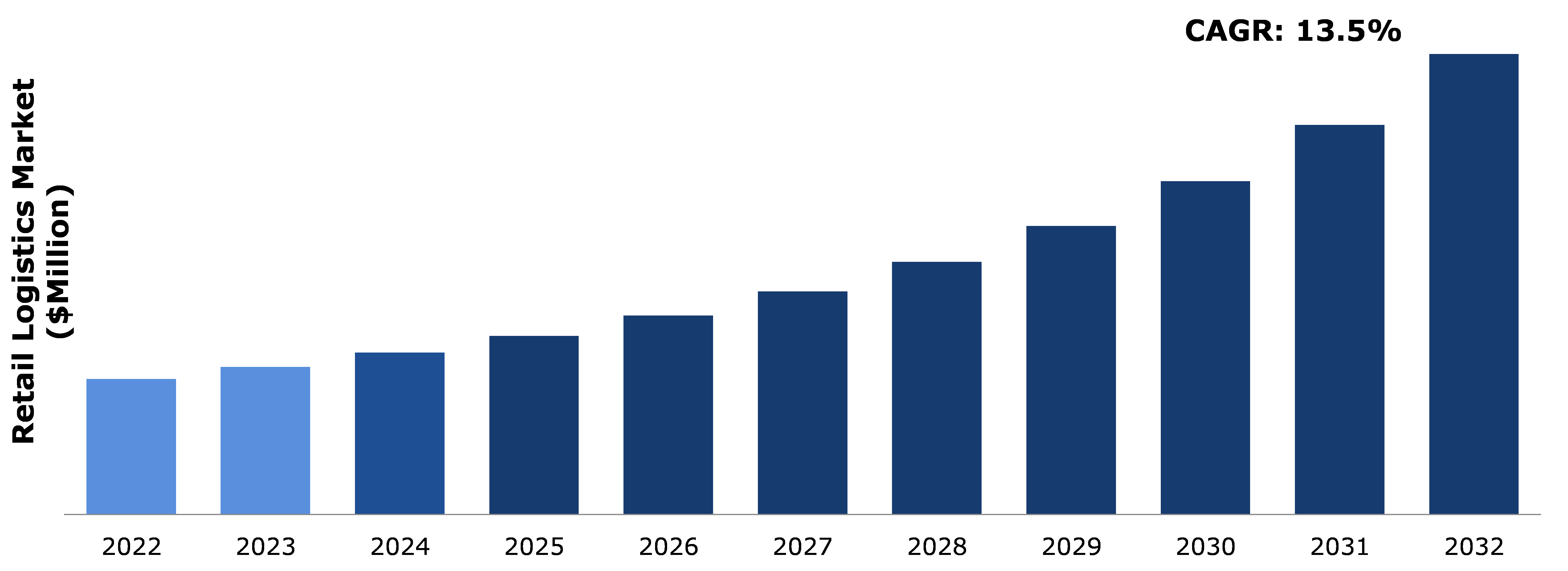

Global Retail Logistics Market Analysis

The global retail logistics market size was $238,500.00 million in 2022 and is predicted to grow with a CAGR of 13.5%, by generating a revenue of $809,690.10 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Retail Logistics Market

The COVID-19 pandemic has had a significant impact on the retail logistics market. Lockdowns, travel restrictions, and factory closures disrupted global supply chains. Manufacturers, suppliers, and distributors struggled to maintain regular operations, leading to delays and shortages of various products. With physical stores closed or operating at limited capacity there was a massive surge in online shopping. Retailers had to adapt quickly to handle the increased volume of online orders and ensure efficient last-mile delivery. Logistics and warehouse workers faced challenges due to safety concerns and labor shortages.

The pandemic accelerated the shift to e-commerce and leading to sustained higher demand for online shopping. Retailers continue to invest in optimizing their online platforms and delivery capabilities. Companies are reevaluating their supply chain strategies to increase resilience against future disruptions. This includes diversifying suppliers, adopting technology for real-time tracking and building contingency plans.

Increase in E-commerce Growth to Drive the Market Growth

The continuous growth of the e-commerce industry has created a massive surge in online orders. This surge has increased the volume of goods that need to be shipped from warehouses to customers doorsteps. The retail logistics sector had to adapt to handle this increase in demand efficiently. Moreover, last- mile delivery is indeed the final step in the logistics and supply chain process, where products are transported from a distribution center or hub to the customer's doorstep or designated delivery location. With customers demanding faster delivery times and the rise of same-day and next-day delivery options, there has been an increase in emphasis on optimizing last-mile delivery processes. This has driven innovations in route optimization, advanced tracking technologies, and alternative delivery methods (drones, robots, and others). This demand for speed has led retailers to optimize their supply chains, adopt technologies like automation and robotics in warehouses and explore last-mile delivery solutions such as drones and autonomous vehicles. The need to streamline processes and reduce lead times is a major driver of innovation in retail logistics. Furthermore, the concentration of people in urban areas has driven the need for efficient logistics solutions due to higher demand for e-commerce services.

Infrastructure Limitations and Rising Transportation Costs to Restrain the Market Growth

Insufficient or outdated infrastructure can indeed pose significant challenges and constraints to the retail logistics market. Outdated transportation networks, congested roads and inadequate ports can result in delays and inefficiencies in the movement of goods. These delays can lead to longer lead times which can negatively affect supply chain planning and customer satisfaction. Poor infrastructure can increase operational costs for retailers. Longer transit times and delays can lead to higher fuel consumption and maintenance costs for transportation vehicles. Inefficient port facilities can result in demurrage charges and additional handling costs. Furthermore, inadequate roads and transportation systems can lead to increased wear and tear of vehicles and goods. This can result in damage to products during transit, leading to financial losses for retailers. Inefficient transportation systems can contribute to higher greenhouse gas emissions due to longer travel times and congestion. This can be a concern for environmentally conscious retailers and customers.

Omni-Channel Fulfillment, Augmented Reality (AR) and Virtual Reality (VR) Technologies to Drive Excellent Opportunities

Augmented Reality (AR) and Virtual Reality (VR) technologies can create immersive and interactive shopping experiences that go beyond traditional brick-and-mortar and e-commerce platforms. Customers can visualize products in their real-world environment or experience virtual showrooms and try products before making a purchase. Moreover, with omni-channel fulfillment, retailers need to manage their inventory more effectively across various sales channels. This involves real-time inventory visibility, demand forecasting, and allocation strategies to prevent stockouts and overstock situations. The last mile of delivery remains a critical aspect of omni-channel fulfillment. Retailers are investing in innovative solutions like autonomous delivery vehicles, drones, and crowd-sourced delivery models to expedite the final stage of the customer journey. Retailers can leverage AR and VR to offer personalized shopping experiences. By analyzing customer preferences and behavior, these technologies can suggest products tailored to individual tastes and needs. Furthermore, the continued growth of online shopping is driving the need for effective logistics solutions to fulfill these orders. Retailers are looking to optimize their supply chain networks to accommodate the rise in online sales. As AR and VR technologies continue to develop, there might be opportunities for retailers to collaborate with tech companies and developers to create innovative solutions that cater to changing customer expectations. The continuous technological advancements offer a wide range of opportunities for key players operating in the retail logistics market.

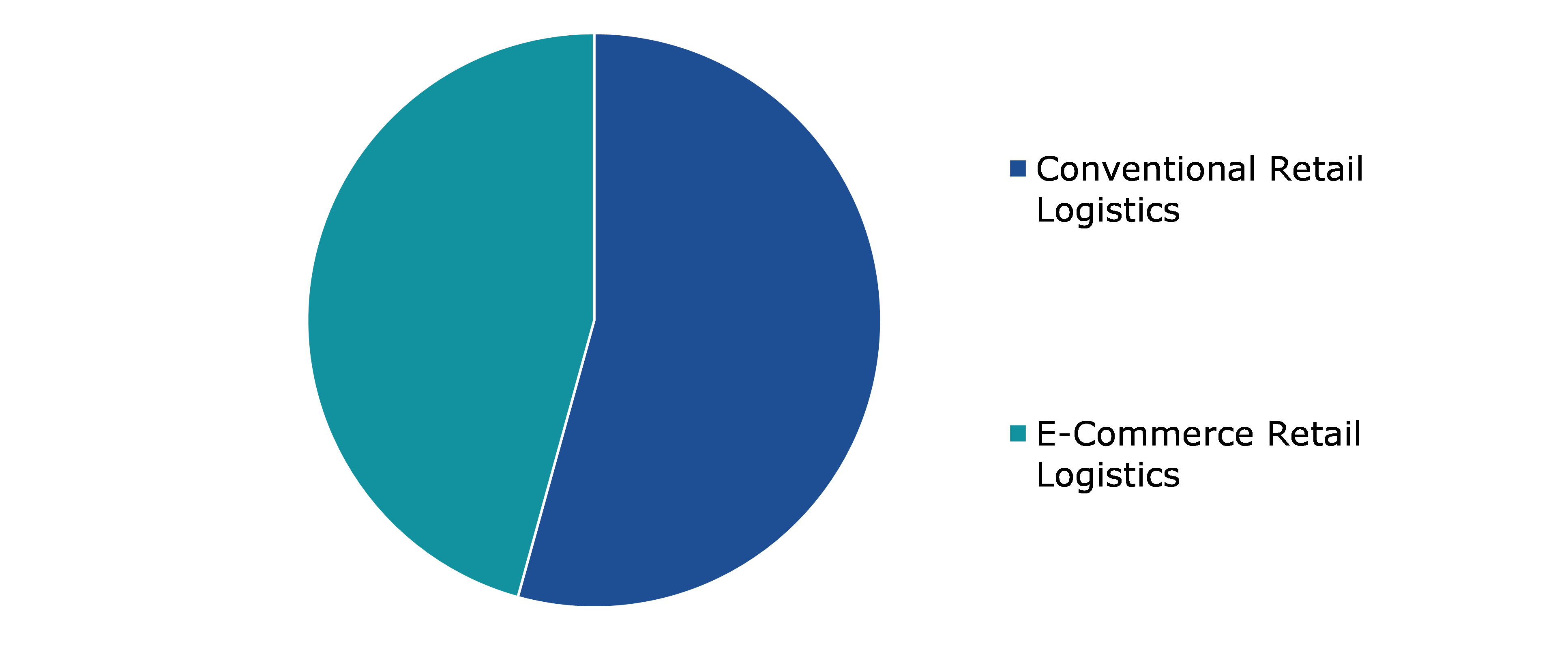

Global Retail Logistics Market Share, by Type, 2022

Source: Research Dive Analysis

The conventional retail logistics sub-segment accounted for the highest market share in 2022. Consumer preferences, purchasing behavior, and demand for products heavily influence the need for efficient retail logistics. As consumer preferences change, retailers must adapt their logistics strategies to ensure products are available in the right quantities and locations. Economic factors such as GDP growth, inflation, and disposable income levels impact retail sales and consequently the demand for retail logistics services. During economic booms, there is generally increased retail activity and demand for logistics services. Moreover, the globalization of markets has led to an increase in international trade, which requires complex logistics networks to move products across borders efficiently. Conventional retail logistics players must adapt to international supply chains and customs regulations. Furthermore, the rise of e-commerce has transformed the retail landscape, placing greater emphasis on efficient warehousing, order fulfillment, and last-mile delivery. Conventional retail logistics companies have to integrate e-commerce capabilities into their operations. Technology plays a crucial role in optimizing retail logistics. Automation, robotics, AI-powered demand forecasting, route optimization software, and warehouse management systems are examples of technologies that improve efficiency and reduce costs.

Global Retail Logistics Market Share, by Solution, 2022

Source: Research Dive Analysis

The supply chain solutions sub-segment accounted for the highest market share in 2022. The rapid growth of e-commerce has significantly impacted retail logistics. Online shopping requires efficient and reliable supply chain solutions to handle the increased volume of orders, last-mile delivery, returns management, and other tasks. Retailers aim to optimize inventory levels to reduce carrying costs while ensuring products are available for customers when they want them Supply chain solutions that can manage international shipping, customs clearance, and coordination across multiple countries and regions are crucial for global retail operations. The integration of technologies like Internet of Things (IoT), Radio-Frequency Identification (RFID), Artificial Intelligence (AI), and analytics enhances visibility, efficiency, and decision-making within the supply chain. These technologies help track shipments, monitor inventory, predict demand, and optimize routes. Environmental concerns have led to a greater emphasis on sustainability in retail logistics. Supply chain solutions that focus on reducing carbon footprint through optimized routing, alternative fuels, and waste reduction resonate well with environmentally conscious consumers and businesses.

Global Retail Logistics Market Share, by Mode of Transport, 2022

![]()

Source: Research Dive Analysis

The roadways sub-segment accounted for the highest market share in 2022. The rapid expansion of e-commerce has significantly increased the demand for efficient and timely transportation of goods. Online shopping requires reliable and fast logistics networks, with roadways being a crucial component for the last-mile delivery to consumers. As more people move to urban areas, there is a higher concentration of consumers that need goods delivered to their doorsteps. Roadways offer accessibility in urban environments, making them an essential mode of transportation for retail goods. With the rise of companies offering same-day or next-day delivery, retailers are under pressure to provide faster delivery options. Roadway transportation networks often enable quicker delivery compared to other modes like sea or rail transport. Roadways provide a high degree of flexibility, allowing retailers to reach even remote or less accessible areas. This connectivity is crucial for ensuring a wide reach of retail products, contributing to market growth. Investments in roadway infrastructure, such as improved road quality, expressways, and bypasses, lead to enhanced transportation efficiency. These improvements can lead to faster transit times and reduced operational costs for retail logistics.

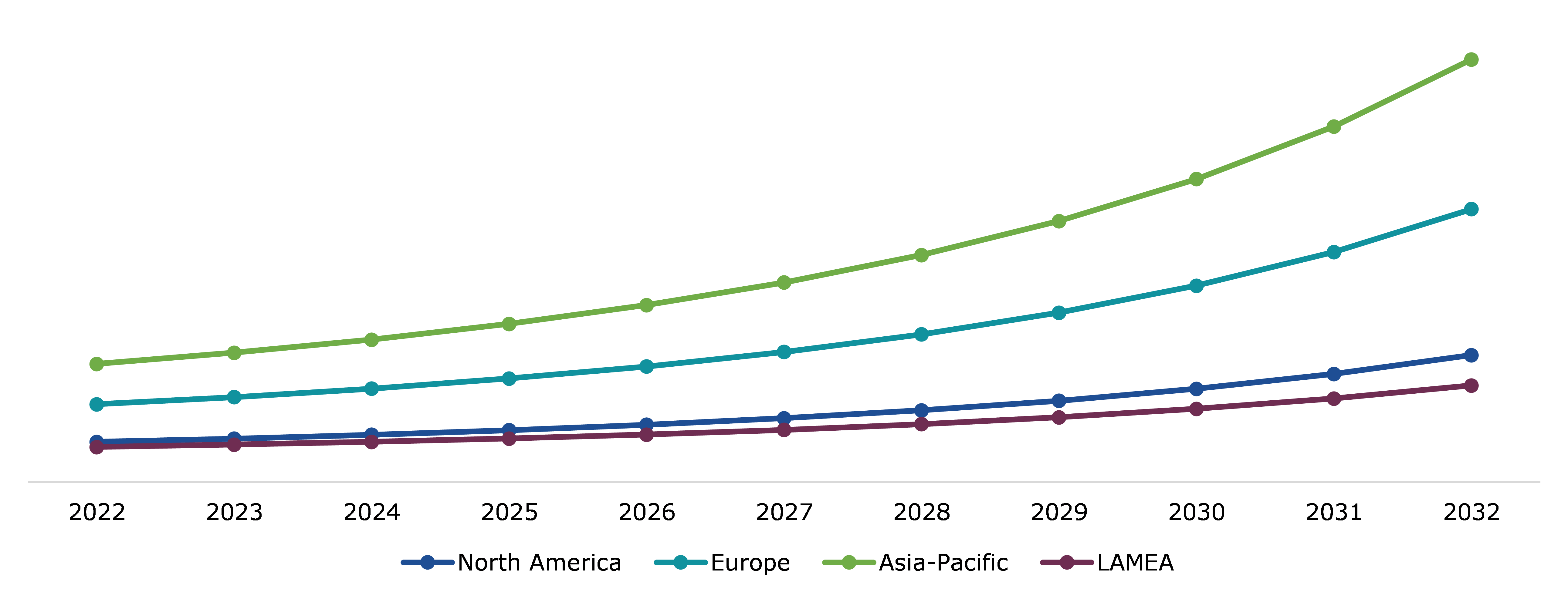

Global Retail Logistics Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Asia-Pacific retail logistics market generated the highest revenue in 2022. Asia-Pacific is experiencing significant urbanization, leading to the concentration of populations in cities. This trend increases the demand for effective logistics networks to supply goods to densely populated areas. Moreover, investments in transportation and logistics infrastructure, such as roads, ports, and warehouses, are crucial for efficient movement of goods within and between countries. Improvements in infrastructure positively impact the retail logistics market. Furthermore, consumers in the region increasingly expect faster, more flexible, and transparent delivery options. Retailers are under pressure to provide convenient delivery time slots, real-time tracking, and easy returns to stay competitive. With growing awareness of environmental issues, retailers are increasingly focusing on sustainable and eco-friendly logistics solutions. This includes optimizing delivery routes to reduce emissions and exploring alternative energy sources for transportation. Government policies and initiatives aimed at boosting trade, investment, and economic growth can have a significant impact on the regional retail logistics market. These policies can influence infrastructure development, trade agreements, and ease of doing business.

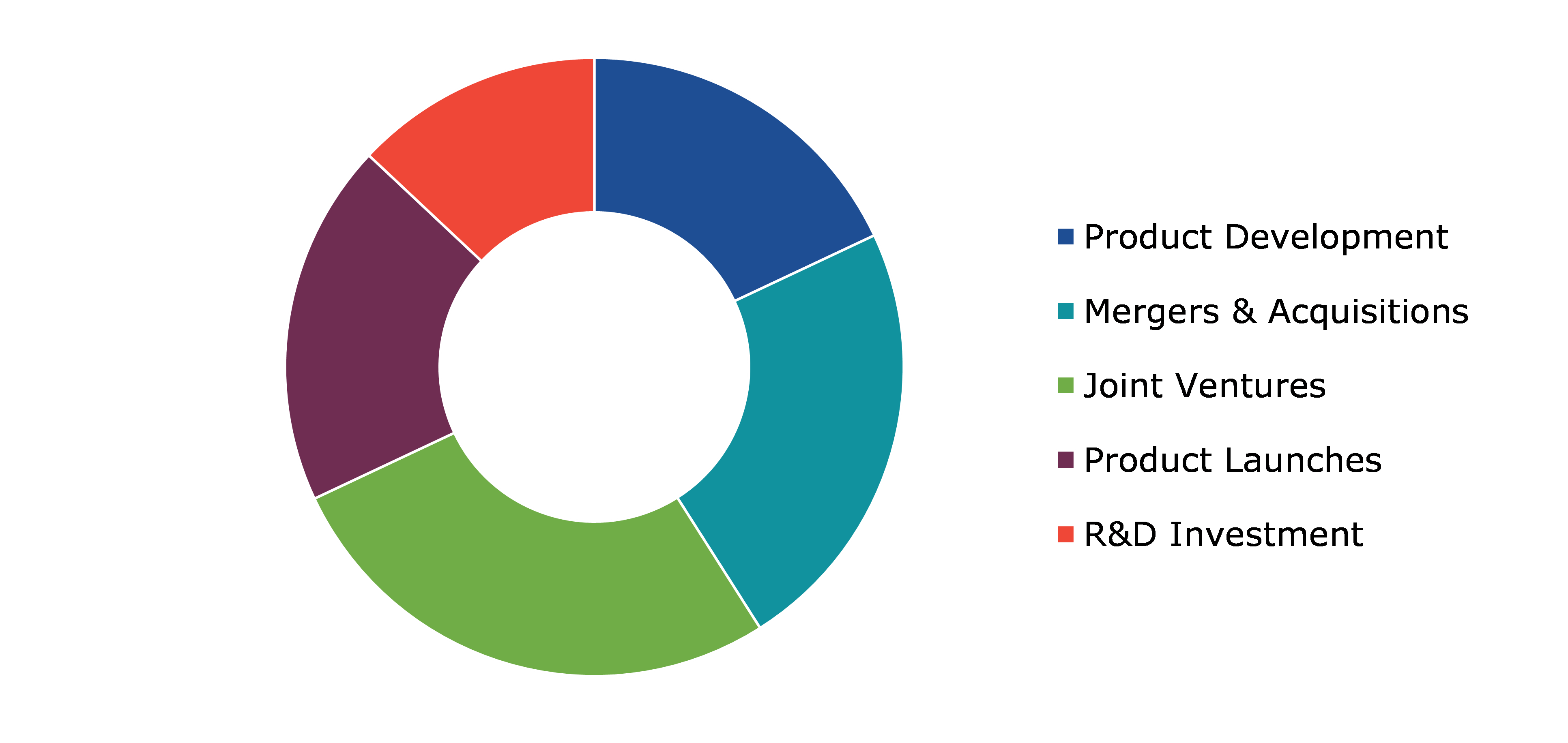

Competitive Scenario in the Global Retail Logistics Market

Investment and agreement are common strategies followed by major market players. In October 2022, Aramex PJSC recently declared that it had successfully acquired Access USA Shipping, LLC (MyUS), a technology-focused worldwide platform facilitating cross-border e-commerce. Aramex obtained all required regulatory authorizations and finalized the acquisition, paying a total cash amount of approximately $265 million.

Source: Research Dive Analysis

Some of the leading retail logistics market players XPO Logistics, Inc., DSV, Kuehne + Nagel International, C.H. Robinson Worldwide, Inc., Nippon Express, FedEx, Schneider, United Parcel Service, APL Logistics Ltd, DHL International GmbH, and A.P. Moller - Maersk.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by Solution |

|

|

Segmentation by Mode of Transport

|

|

| Key Companies Profiled |

|

Q1. What is the size of the global retail logistics market?

A. The size of the global retail logistics market was over $ 238,500.00 million in 2022 and is projected to reach $ 809,690.10 million by 2032.

Q2. Which are the major companies in the retail logistics market?

A. XPO Logistics, Inc., DSV, Kuehne + Nagel International, and C.H. Robinson Worldwide, Inc., are some of the key players in the global retail logistics market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. North America possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the North America retail logistics market?

A. North America retail logistics market is anticipated to grow at 12.7% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Nippon Express, FedEx, and Schneider are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global Retail Logistics market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on the Retail Logistics market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Retail Logistics Market Analysis, by Type

5.1. Overview

5.2. Conventional Retail Logistics

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2023-2032

5.2.3. Market share analysis, by country, 2023-2032

5.3. E-commerce Retail Logistics

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2023-2032

5.3.3. Market share analysis, by country, 2023-2032

5.4. Research Dive Exclusive Insights

5.4.1. Market attractiveness

5.4.2. Competition heatmap

6. Retail Logistics Market Analysis, by Solution

6.1. Commerce Enablement

6.1.1. Definition, key trends, growth factors, and opportunities

6.1.2. Market size analysis, by region, 2023-2032

6.1.3. Market share analysis, by country, 2023-2032

6.2. Supply Chain Solutions

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2023-2032

6.2.3. Market share analysis, by country, 2023-2032

6.3. Reverse Logistics & Liquidation

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2023-2032

6.3.3. Market share analysis, by country, 2023-2032

6.4. Transportation Management

6.4.1. Definition, key trends, growth factors, and opportunities

6.4.2. Market size analysis, by region, 2023-2032

6.4.3. Market share analysis, by country, 2023-2032

6.5. Others

6.5.1. Definition, key trends, growth factors, and opportunities

6.5.2. Market size analysis, by region, 2023-2032

6.5.3. Market share analysis, by country, 2023-2032

6.6. Research Dive Exclusive Insights

6.6.1. Market attractiveness

6.6.2. Competition heatmap

7. Retail Logistics Market Analysis, by Mode of Transport

7.1. Railways

7.1.1. Definition, key trends, growth factors, and opportunities

7.1.2. Market size analysis, by region, 2023-2032

7.1.3. Market share analysis, by country, 2023-2032

7.2. Airways

7.2.1. Definition, key trends, growth factors, and opportunities

7.2.2. Market size analysis, by region, 2023-2032

7.2.3. Market share analysis, by country, 2023-2032

7.3. Roadways

7.3.1. Definition, key trends, growth factors, and opportunities

7.3.2. Market size analysis, by region, 2023-2032

7.3.3. Market share analysis, by country, 2023-2032

7.4. Waterways

7.4.1. Definition, key trends, growth factors, and opportunities

7.4.2. Market size analysis, by region, 2023-2032

7.4.3. Market share analysis, by country, 2023-2032

7.5. Research Dive Exclusive Insights

7.5.1. Market attractiveness

7.5.2. Competition heatmap

8. Retail Logistics Market, by Region

8.1. North America

8.1.1. U.S.

8.1.1.1. Market size analysis, by Type, 2023-2032

8.1.1.2. Market size analysis, by Solution, 2023-2032

8.1.1.3. Market size analysis, by Mode of Transport, 2023-2032

8.1.2. Canada

8.1.2.1. Market size analysis, by Type, 2023-2032

8.1.2.2. Market size analysis, by Solution, 2023-2032

8.1.2.3. Market size analysis, by Mode of Transport, 2023-2032

8.1.3. Mexico

8.1.3.1. Market size analysis, by Type, 2023-2032

8.1.3.2. Market size analysis, by Solution, 2023-2032

8.1.3.3. Market size analysis, by Mode of Transport, 2023-2032

8.1.4. Research Dive Exclusive Insights

8.1.4.1. Market attractiveness

8.1.4.2. Competition heatmap

8.2. Europe

8.2.1. Germany

8.2.1.1. Market size analysis, by Type, 2023-2032

8.2.1.2. Market size analysis, by Solution, 2023-2032

8.2.1.3. Market size analysis, by Mode of Transport, 2023-2032

8.2.2. UK

8.2.2.1. Market size analysis, by Type, 2023-2032

8.2.2.2. Market size analysis, by Solution, 2023-2032

8.2.2.3. Market size analysis, by Mode of Transport, 2023-2032

8.2.3. France

8.2.3.1. Market size analysis, by Type, 2023-2032

8.2.3.2. Market size analysis, by Solution, 2023-2032

8.2.3.3. Market size analysis, by Mode of Transport, 2023-2032

8.2.4. Spain

8.2.4.1. Market size analysis, by Type, 2023-2032

8.2.4.2. Market size analysis, by Solution, 2023-2032

8.2.4.3. Market size analysis, by Mode of Transport, 2023-2032

8.2.5. Italy

8.2.5.1. Market size analysis, by Type, 2023-2032

8.2.5.2. Market size analysis, by Solution, 2023-2032

8.2.5.3. Market size analysis, by Mode of Transport, 2023-2032

8.2.6. Rest of Europe

8.2.6.1. Market size analysis, by Type, 2023-2032

8.2.6.2. Market size analysis, by Solution, 2023-2032

8.2.6.3. Market size analysis, by Mode of Transport, 2023-2032

8.2.7. Research Dive Exclusive Insights

8.2.7.1. Market attractiveness

8.2.7.2. Competition heatmap

8.3. Asia-Pacific

8.3.1. China

8.3.1.1. Market size analysis, by Type, 2023-2032

8.3.1.2. Market size analysis, by Solution, 2023-2032

8.3.1.3. Market size analysis, by Mode of Transport, 2023-2032

8.3.2. Japan

8.3.2.1. Market size analysis, by Type, 2023-2032

8.3.2.2. Market size analysis, by Solution, 2023-2032

8.3.2.3. Market size analysis, by Mode of Transport, 2023-2032

8.3.3. India

8.3.3.1. Market size analysis, by Type, 2023-2032

8.3.3.2. Market size analysis, by Solution, 2023-2032

8.3.3.3. Market size analysis, by Mode of Transport, 2023-2032

8.3.4. Australia

8.3.4.1. Market size analysis, by Type, 2023-2032

8.3.4.2. Market size analysis, by Solution, 2023-2032

8.3.4.3. Market size analysis, by Mode of Transport, 2023-2032

8.3.5. South Korea

8.3.5.1. Market size analysis, by Type, 2023-2032

8.3.5.2. Market size analysis, by Solution, 2023-2032

8.3.5.3. Market size analysis, by Mode of Transport, 2023-2032

8.3.6. Rest of Asia-Pacific

8.3.6.1. Market size analysis, by Type, 2023-2032

8.3.6.2. Market size analysis, by Solution, 2023-2032

8.3.6.3. Market size analysis, by Mode of Transport, 2023-2032

8.3.7. Research Dive Exclusive Insights

8.3.7.1. Market attractiveness

8.3.7.2. Competition heatmap

8.4. LAMEA

8.4.1. Brazil

8.4.1.1. Market size analysis, by Type, 2023-2032

8.4.1.2. Market size analysis, by Solution, 2023-2032

8.4.1.3. Market size analysis, by Mode of Transport, 2023-2032

8.4.2. Saudi Arabia

8.4.2.1. Market size analysis, by Type, 2023-2032

8.4.2.2. Market size analysis, by Solution, 2023-2032

8.4.2.3. Market size analysis, by Mode of Transport, 2023-2032

8.4.3. UAE

8.4.3.1. Market size analysis, by Type, 2023-2032

8.4.3.2. Market size analysis, by Solution, 2023-2032

8.4.3.3. Market size analysis, by Mode of Transport, 2023-2032

8.4.4. South Africa

8.4.4.1. Market size analysis, by Type, 2023-2032

8.4.4.2. Market size analysis, by Solution, 2023-2032

8.4.4.3. Market size analysis, by Mode of Transport, 2023-2032

8.4.5. Rest of LAMEA

8.4.5.1. Market size analysis, by Type, 2023-2032

8.4.5.2. Market size analysis, by Solution, 2023-2032

8.4.5.3. Market size analysis, by Mode of Transport, 2023-2032

8.4.6. Research Dive Exclusive Insights

8.4.6.1. Market attractiveness

8.4.6.2. Competition heatmap

9. Competitive Landscape

9.1. Top winning strategies, 2022

9.1.1. By strategy

9.1.2. By year

9.2. Strategic overview

9.3. Market share analysis, 2021

10. Company Profiles

10.1. XPO Logistics, Inc.

10.1.1. Overview

10.1.2. Business segments

10.1.3. Product portfolio

10.1.4. Financial performance

10.1.5. Recent developments

10.1.6. SWOT analysis

10.2. DSV

10.2.1. Overview

10.2.2. Business segments

10.2.3. Product portfolio

10.2.4. Financial performance

10.2.5. Recent developments

10.2.6. SWOT analysis

10.3. Kuehne + Nagel International

10.3.1. Overview

10.3.2. Business segments

10.3.3. Product portfolio

10.3.4. Financial performance

10.3.5. Recent developments

10.3.6. SWOT analysis

10.4. C.H. Robinson Worldwide, Inc.

10.4.1. Overview

10.4.2. Business segments

10.4.3. Product portfolio

10.4.4. Financial performance

10.4.5. Recent developments

10.4.6. SWOT analysis

10.5. Nippon Express

10.5.1. Overview

10.5.2. Business segments

10.5.3. Product portfolio

10.5.4. Financial performance

10.5.5. Recent developments

10.5.6. SWOT analysis

10.6. FedEx

10.6.1. Overview

10.6.2. Business segments

10.6.3. Product portfolio

10.6.4. Financial performance

10.6.5. Recent developments

10.6.6. SWOT analysis

10.7. Schneider

10.7.1. Overview

10.7.2. Business segments

10.7.3. Product portfolio

10.7.4. Financial performance

10.7.5. Recent developments

10.7.6. SWOT analysis

10.8. United Parcel Service

10.8.1. Overview

10.8.2. Business segments

10.8.3. Product portfolio

10.8.4. Financial performance

10.8.5. Recent developments

10.8.6. SWOT analysis

10.9. APL Logistics Ltd

10.9.1. Overview

10.9.2. Business segments

10.9.3. Product portfolio

10.9.4. Financial performance

10.9.5. Recent developments

10.9.6. SWOT analysis

10.10. DHL International GmbH

10.10.1. Overview

10.10.2. Business segments

10.10.3. Product portfolio

10.10.4. Financial performance

10.10.5. Recent developments

10.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com