Global Cargo Insurance Market Report

RA08749

Global Cargo Insurance Market by Insurance Type (Air Cargo, Land Cargo, and Marine Cargo), Distribution Channel (Direct Sales and Indirect Sales), End User (Traders, Cargo Owners, Ship Owners, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Opportunity Analysis and Industry Forecast, 2023-2032

Cargo Insurance Overview

Cargo insurance is a type of insurance that protects the goods in case of cargo loss or damage caused to the goods during transportation. Cargo insurance compensates for losses caused by various risks, such as fraud, loss, accidents, natural disasters, damage, and other unforeseen events that may occur during the transit of goods. Cargo insurance policies typically cover goods from point of origin to final destination, regardless of whether they are transported by sea, air, land, or a combination of modes. The cargo insurance coverage is available on a per-shipment or annual basis for regular shippers.

Major insurance companies offer cargo insurance as part of their marine insurance offerings. Cargo insurance is widely used across international trade that helps businesses in protecting their cargo and shipments against financial losses. Cargo insurance offers safety to the goods across borders as this insurance complies with custom regulations across borders thereby avoiding legal penalties for the businesses that are shipping cargo. Thus, the popularity of cargo insurance is increasing rapidly as this insurance helps in boosting the credibility of businesses by offering protection to the high-value shipments or perishable goods.

Global Cargo Insurance Market Analysis

The global cargo insurance market size was $71,414.4 million in 2022 and is predicted to grow with a CAGR of 4.1%, by generating a revenue of $105,975.1 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Cargo Insurance Market

COVID-19 caused widespread disruptions in global supply chains due to lockdown measures, travel restrictions, and reduced production capacities. Many businesses faced challenges in shipping their goods, leading to a decrease in cargo transportation and subsequently reducing the demand for cargo insurance coverage. Lockdown measures and restrictions imposed to contain the spread of the virus led to the closure of factories and manufacturing facilities in many countries. This resulted in production delays and reduced output, causing disruptions in the supply of raw materials, components, and finished goods.

In addition, the travel restrictions imposed across several countries, import-export restrictions, and closed borders declined the demand for cargo insurance as the movement of goods was restricted. Also, during the pandemic, the type of cargo and volume of cargo shipped across countries was restricted to only essential goods such as medical supplies. This in turn, reduced the volume of cargo containing consumer goods, automotive parts, chemicals & materials, and other industrial goods. Owing to the above-mentioned factors, the cargo insurance market growth was negatively impacted during the COVID-19 pandemic.

Expansion of the Transportation & Logistics Sector to Drive the Market Growth

The rapid development of the transportation sector in emerging countries is expected to benefit the cargo insurance market. The volume of goods being transported also increases as the transportation sector develops, increasing the risk of loss or damage while in transit. The cargo insurance is crucial for both shippers and carriers due to the increased risk of cargo loss and damage during transportation. In addition, developing countries may lack the same level of transportation infrastructure compared to the developed economies, which increases the risks associated with transporting cargo. For instance, unreliable transportation, lack of security, and restricted access to technology all raise the possibility of cargo loss, theft, or damage. In these situations, cargo insurance is essential to safeguard the cargo from potential thefts and damage. Governments around the world have been actively pursuing trade liberalization measures such as free trade agreements (FTAs), regional trade blocs, and tariff reductions. These efforts facilitate trade by reducing trade barriers, encouraging international business transactions, and promoting market access for goods and services. There is an increasing need for specialized cargo insurance coverage catered to particular industries or goods categories as supply chains become more complex and diverse. This includes protection for expensive cargo, perishables, flammable goods such as chemicals and oils, and specialty machinery. Through the creation of specialized coverage options and risk management strategies, the cargo insurance market growth is anticipated to boost in the upcoming years.

To know more about global cargo insurance market drivers, get in touch with our analysts here.

Intense Market Competition, Regulatory and Compliance Requirements to Restrain the Market Growth

The cargo insurance market is highly competitive, with numerous insurance providers competing for market share. Intense competition can lead to price pressure and reduced profit margins. Insurance companies need to differentiate themselves through unique coverage offerings, value-added services, and efficient claims processing to remain competitive. The cargo insurance market is subject to regulatory frameworks and compliance requirements in different jurisdictions. Insurance providers must navigate and adhere to various regulations, such as licensing requirements, financial solvency regulations, and compliance with international trade laws. Staying compliant and keeping up with regulatory changes can pose challenges for insurance companies operating in multiple markets. These factors are anticipated to restrict the cargo insurance market share during the forecast period.

Technological Advancements in the Insurance Industry to Drive Excellent Opportunities

The cargo insurance market has been positively impacted by the rising trend of digital insurance, which has increased competition, improved efficiency, increased customer satisfaction, offering more personalized insurance services for the customers. The cargo insurance companies can customize their policies to meet the unique needs of people or businesses. In order to identify risks and create a custom insurance plan that meets the needs of a logistics company, an insurance provider, for instance, can examine the shipping patterns, cargo types, and destinations of the company. The cargo insurance market is significantly impacted by technology, which presents opportunities for innovation and customer satisfaction. The popularity of insurtech which refers to the use of innovative technologies in the insurance sector to streamline and automate the claim submission process, which is anticipated to create several opportunities in the cargo insurance market in the upcoming years. For instance, the insurtech solutions for cargo insurance include advanced risk assessment tools, real-time cargo tracking systems, and automated claims processing that can improve customer service thereby driving the cargo insurance revenue. Adopting new technologies can assist insurance companies in remaining competitive and grabbing new opportunities.

To know more about global cargo insurance market opportunities, get in touch with our analysts here.

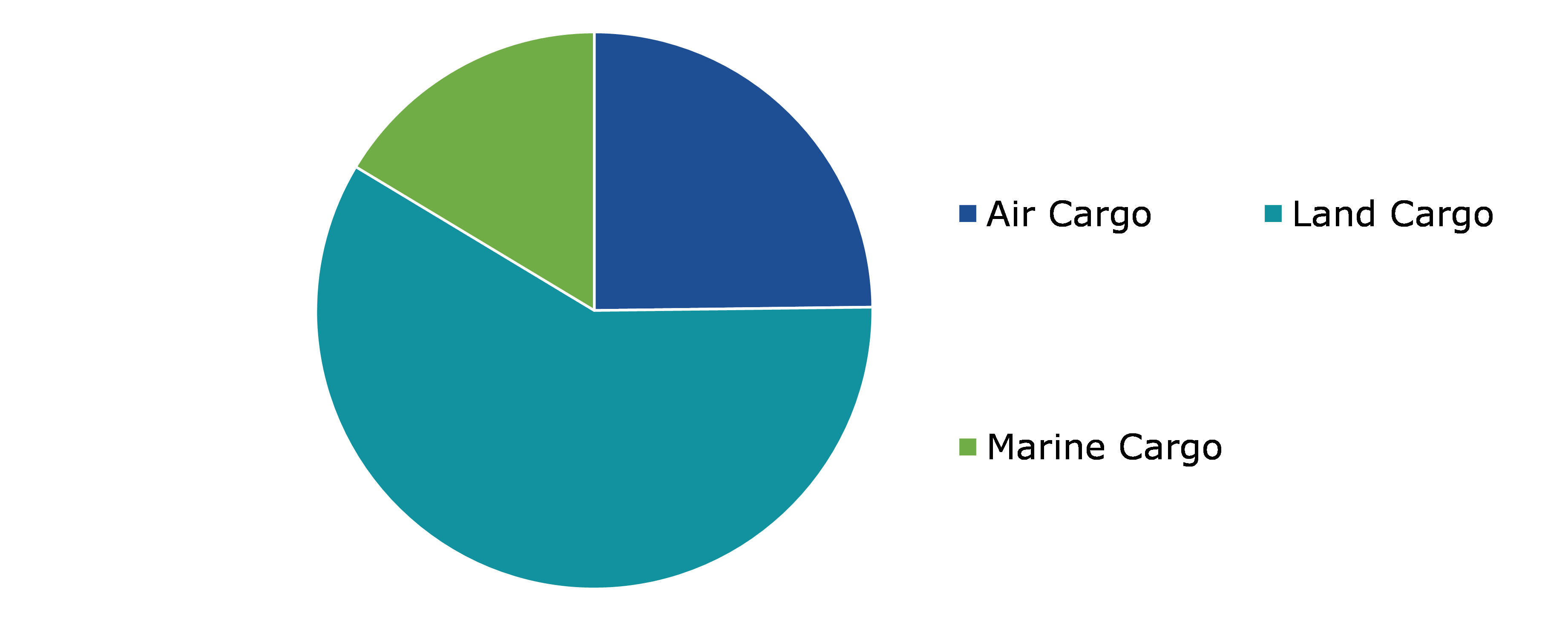

Global Cargo Insurance Market Share, by Insurance Type, 2022

Source: Research Dive Analysis

The land cargo sub-segment accounted for the highest market share in 2022. The land cargo segment of the cargo insurance market refers to the insurance coverage provided for goods and cargo that are transported over land, including by road, rail, or inland waterways. The rising popularity of land cargo insurance can be attributed to various risk factors that can result in damage, loss, or theft of goods during transit. These risks include accidents, collisions, cargo handling errors, theft, vandalism, natural disasters, fire, and other unforeseen events. Land cargo insurance provides coverage against these risks, offering financial protection to cargo owners and transporters. Cargo insurance policies for the land cargo segment typically offer coverage for physical loss or damage to goods during transportation. The coverage can be customized to specific needs, including coverage for domestic or international transit, specific commodities, perishable goods, high-value cargo, and hazardous materials. In addition, liability coverage may be included to protect against third-party claims arising from the transportation of goods. These factors are anticipated to boost the land cargo insurance market size in the upcoming years.

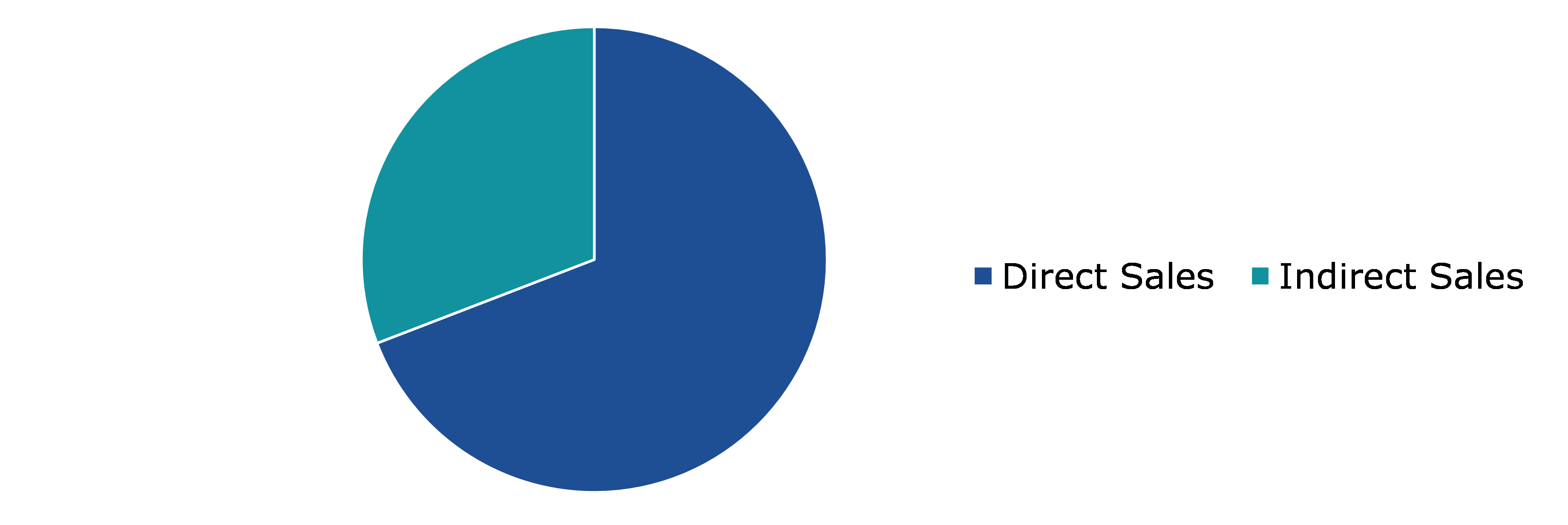

Global Cargo Insurance Market Size, by Distribution Channel, 2022

Source: Research Dive Analysis

The direct sales sub-segment accounted for the highest market share in 2022. The direct sales segment in the cargo insurance market refers to the distribution of insurance products directly to customers, bypassing traditional intermediaries such as brokers or agents. Under this segment, insurance companies sell cargo insurance policies directly to businesses or individuals involved in the transportation of goods. The direct sales sub-segment is growing rapidly as it provides an opportunity for insurance companies to enhance the customer experience. Insurers can leverage digital tools, such as online chatbots or customer service representatives, to provide real-time support and assistance to customers. Prompt responses to queries, efficient claims handling, and personalized service contribute to an overall improved customer experience. Direct sales often come with transparent pricing, as customers can see the cost breakdown and choose the coverage options that fit their budget. Insurers provide detailed information on premium rates, deductibles, and coverage limits upfront, enabling customers to make informed decisions. Direct sales in the cargo insurance market often involves simplified underwriting processes. Insurers leverage technology and automation to streamline underwriting procedures, allowing for faster policy issuance and reduced paperwork. This efficiency benefits both customers and insurers, making the purchase process quicker and more efficient. These factors are major drivers for the growth of direct sales sub-segment.

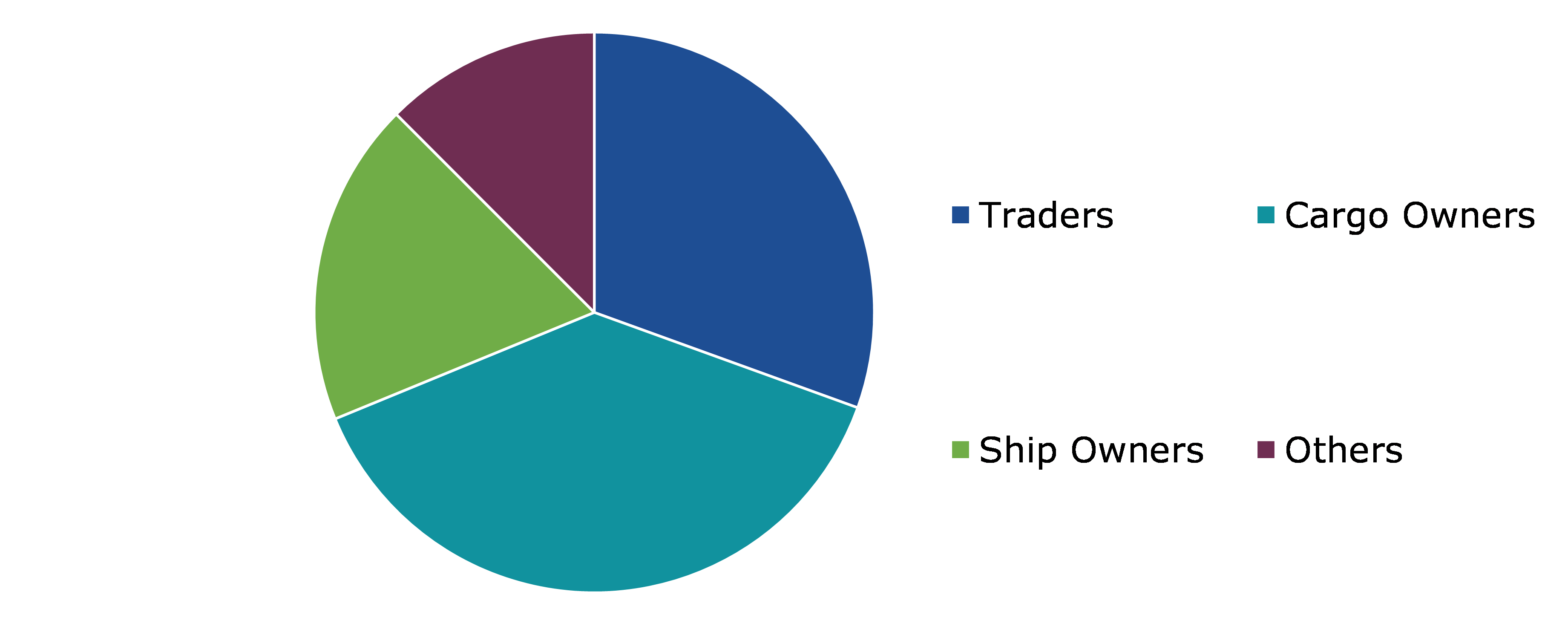

Global Cargo Insurance Market Analysis, by End User, 2022

Source: Research Dive Analysis

The cargo owners sub-segment accounted for the highest market share in 2022. The cargo owners segment in the cargo insurance market refers to businesses or individuals that owns the cargo which is being transported. Cargo owners widely opt for cargo insurance as they are responsible for insuring their cargo to protect against loss or damage during transit. Cargo owners are entities or individuals who own the goods being transported. They may include manufacturers, wholesalers, retailers, exporters, importers, or individuals shipping personal belongings. Cargo owners actively engage in risk mitigation practices to reduce the likelihood of damage or loss during transportation. This may include proper packaging and securing of goods, implementing quality control measures, using appropriate transportation methods, and adhering to industry best practices. Risk mitigation efforts help reduce the potential for claims and contribute to lower insurance premiums.

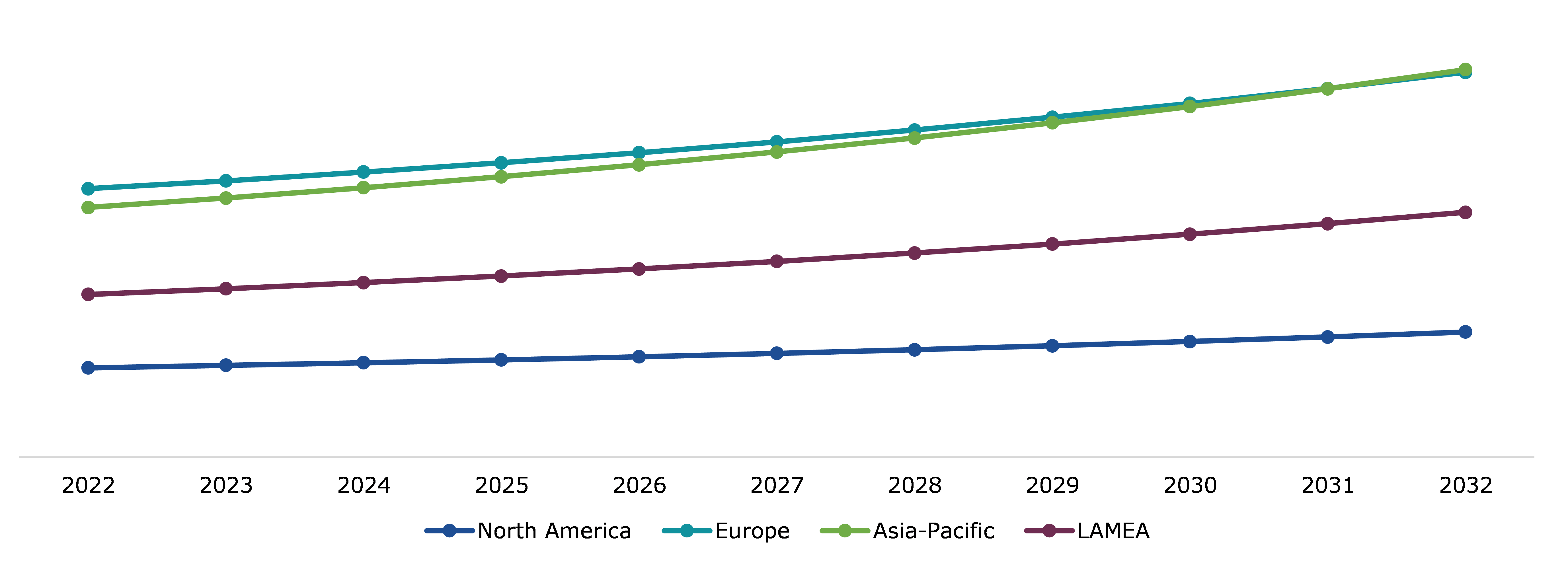

Global Cargo Insurance Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Europe cargo insurance market generated the highest revenue in 2022. The cargo insurance market has experienced tremendous growth in Europe, with consumers increasingly relying on online shopping which is leading to an increase in the volume of cargo transported from one city to another, or even from one country to another country. This shift in consumer behavior has resulted in a surge in parcel deliveries and last-mile logistics. Cargo insurance providers in the region can capitalize on this trend by offering tailored insurance solutions for e-commerce shipments and the associated risks. Europe is known for its diverse range of industries and specialized cargo transportation requirements. Cargo insurance providers can grab opportunities by offering specialized coverage for high-value cargo, perishable goods, hazardous materials, temperature-sensitive goods, and other specific industry needs. Tailoring insurance solutions to meet these specialized requirements can attract customers seeking comprehensive coverage for their unique cargo. Europe has a complex regulatory landscape, including insurance regulations, trade regulations, and customs requirements. Cargo insurance providers can capitalize on the opportunities arising from regulatory changes by staying up-to-date with the evolving regulatory environment and offering compliant insurance products. Adapting to regulatory changes can help insurers gain a competitive advantage and attract businesses seeking reliable and compliant insurance coverage.

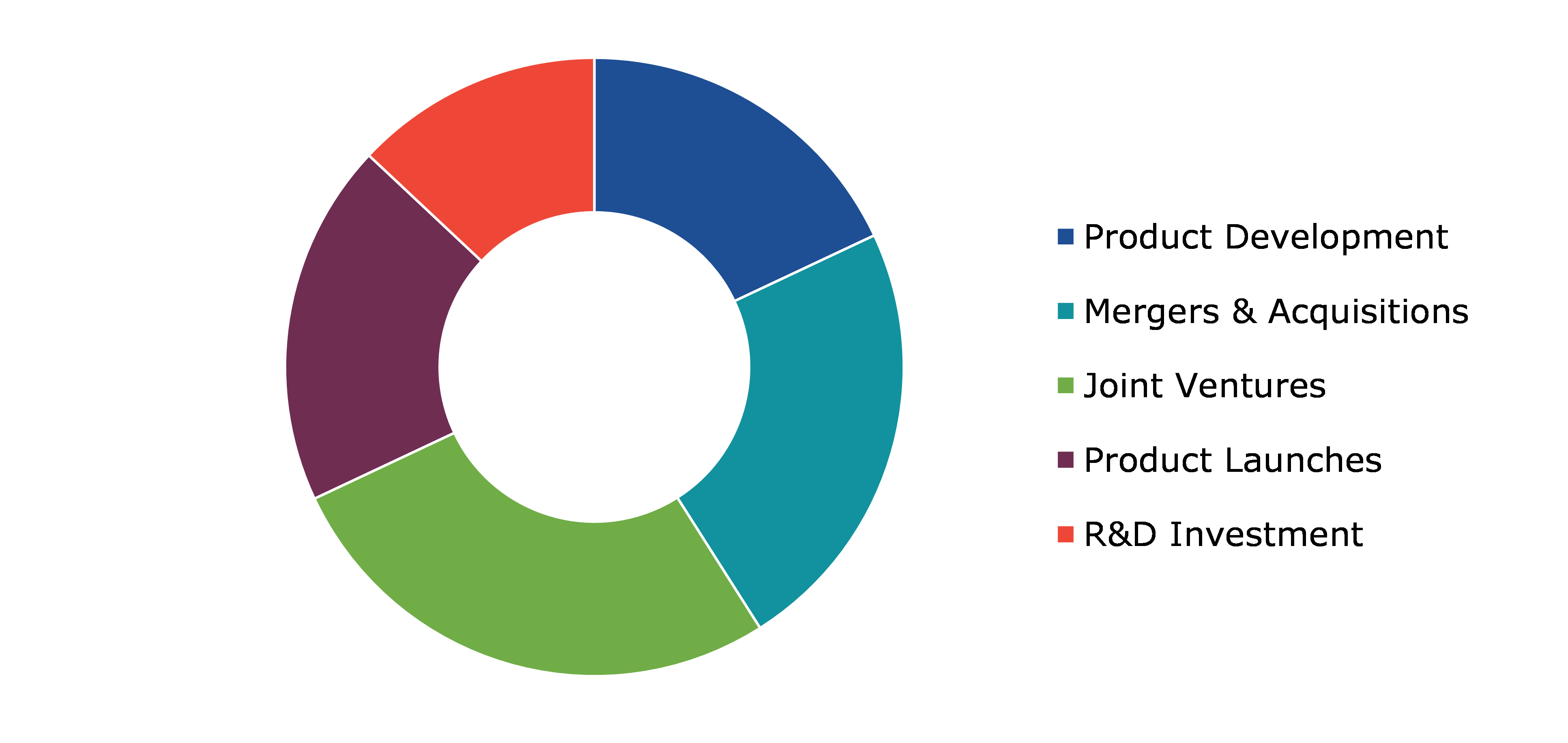

Competitive Scenario in the Global Cargo Insurance Market

Investment and agreement are common strategies followed by major market players. For instance, on September 28, 2022, the International Union of Marine Insurance (IUMI) are offering a new Masterclass in Cargo Insurance. The program was held in London in between March 20, 2023- March 24, 2023. This program has placed a strong emphasis on the fundamental ideas and procedures of cargo insurance. It was the first on-site training program offered by IUMI.

Source: Research Dive Analysis

Some of the leading cargo insurance market players are Allianz, AXA, Aon PLC, American International Group Inc, Arthur J. Gallagher & Co., Chubb, Lloyd's, Marsh LLC, Zurich Insurance Group Ltd, and Lockton Companies.

| Aspect | Particulars |

| Historical Market Estimations | 2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Insurance Type |

|

| Segmentation by Distribution Channel |

|

|

Segmentation by End User

|

|

| Key Companies Profiled |

|

Q1. What is the size of the global cargo insurance market?

A. The size of the global cargo insurance market was over $71,414.4 million in 2022 and is projected to reach $105,975.1 million by 2032.

Q2. Which are the major companies in the cargo insurance market?

A. Allianz and AXA are some of the key players in the global cargo insurance market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific cargo insurance market?

A. Asia-Pacific cargo insurance market is anticipated to grow at 4.6% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Allianz, AXA, Aon PLC, American International Group Inc, and Arthur J. Gallagher & Co., are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global cargo insurance market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on cargo insurance market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Cargo Insurance Market Analysis, by Insurance Type

5.1.Overview

5.2.Air Cargo

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2022-2032

5.2.3.Market share analysis, by country, 2022-2032

5.3.Land Cargo

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2022-2032

5.3.3.Market share analysis, by country, 2022-2032

5.4.Marine Cargo

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region, 2022-2032

5.4.3.Market share analysis, by country, 2022-2032

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness

5.5.2.Competition heatmap

6.Cargo Insurance Market Analysis, by Distribution Channel

6.1.Direct Sales

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2022-2032

6.1.3.Market share analysis, by country, 2022-2032

6.2.Indirect Sales

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2022-2032

6.2.3.Market share analysis, by country, 2022-2032

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Cargo Insurance Market Analysis, by End User

7.1.Traders

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region, 2022-2032

7.1.3.Market share analysis, by country, 2022-2032

7.2.Cargo Owners

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2022-2032

7.2.3.Market share analysis, by country, 2022-2032

7.3.Ship Owners

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region, 2022-2032

7.3.3.Market share analysis, by country, 2022-2032

7.4.Others

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region, 2022-2032

7.4.3.Market share analysis, by country, 2022-2032

7.5.Research Dive Exclusive Insights

7.5.1.Market attractiveness

7.5.2.Competition heatmap

8.Cargo Insurance Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Insurance Type, 2022-2032

8.1.1.2.Market size analysis, by Distribution Channel, 2022-2032

8.1.1.3.Market size analysis, by End User, 2022-2032

8.1.2.Canada

8.1.2.1.Market size analysis, by Insurance Type, 2022-2032

8.1.2.2.Market size analysis, by Distribution Channel, 2022-2032

8.1.2.3.Market size analysis, by End User, 2022-2032

8.1.3.Mexico

8.1.3.1.Market size analysis, by Insurance Type, 2022-2032

8.1.3.2.Market size analysis, by Distribution Channel, 2022-2032

8.1.3.3.Market size analysis, by End User, 2022-2032

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Insurance Type, 2022-2032

8.2.1.2.Market size analysis, by Distribution Channel, 2022-2032

8.2.1.3.Market size analysis, by End User, 2022-2032

8.2.2.UK

8.2.2.1.Market size analysis, by Insurance Type, 2022-2032

8.2.2.2.Market size analysis, by Distribution Channel, 2022-2032

8.2.2.3.Market size analysis, by End User, 2022-2032

8.2.3.France

8.2.3.1.Market size analysis, by Insurance Type, 2022-2032

8.2.3.2.Market size analysis, by Distribution Channel, 2022-2032

8.2.3.3.Market size analysis, by End User, 2022-2032

8.2.4.Netherlands

8.2.4.1.Market size analysis, by Insurance Type, 2022-2032

8.2.4.2.Market size analysis, by Distribution Channel, 2022-2032

8.2.4.3.Market size analysis, by End User, 2022-2032

8.2.5.Italy

8.2.5.1.Market size analysis, by Insurance Type, 2022-2032

8.2.5.2.Market size analysis, by Distribution Channel, 2022-2032

8.2.5.3.Market size analysis, by End User, 2022-2032

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Insurance Type, 2022-2032

8.2.6.2.Market size analysis, by Distribution Channel, 2022-2032

8.2.6.3.Market size analysis, by End User, 2022-2032

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia-Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Insurance Type, 2022-2032

8.3.1.2.Market size analysis, by Distribution Channel, 2022-2032

8.3.1.3.Market size analysis, by End User, 2022-2032

8.3.2.Japan

8.3.2.1.Market size analysis, by Insurance Type, 2022-2032

8.3.2.2.Market size analysis, by Distribution Channel, 2022-2032

8.3.2.3.Market size analysis, by End User, 2022-2032

8.3.3.India

8.3.3.1.Market size analysis, by Insurance Type, 2022-2032

8.3.3.2.Market size analysis, by Distribution Channel, 2022-2032

8.3.3.3.Market size analysis, by End User, 2022-2032

8.3.4.Australia

8.3.4.1.Market size analysis, by Insurance Type, 2022-2032

8.3.4.2.Market size analysis, by Distribution Channel, 2022-2032

8.3.4.3.Market size analysis, by End User, 2022-2032

8.3.5.Singapore

8.3.5.1.Market size analysis, by Insurance Type, 2022-2032

8.3.5.2.Market size analysis, by Distribution Channel, 2022-2032

8.3.5.3.Market size analysis, by End User, 2022-2032

8.3.6.Rest of Asia-Pacific

8.3.6.1.Market size analysis, by Insurance Type, 2022-2032

8.3.6.2.Market size analysis, by Distribution Channel, 2022-2032

8.3.6.3.Market size analysis, by End User, 2022-2032

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Insurance Type, 2022-2032

8.4.1.2.Market size analysis, by Distribution Channel, 2022-2032

8.4.1.3.Market size analysis, by End User, 2022-2032

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Insurance Type, 2022-2032

8.4.2.2.Market size analysis, by Distribution Channel, 2022-2032

8.4.2.3.Market size analysis, by End User, 2022-2032

8.4.3.UAE

8.4.3.1.Market size analysis, by Insurance Type, 2022-2032

8.4.3.2.Market size analysis, by Distribution Channel, 2022-2032

8.4.3.3.Market size analysis, by End User, 2022-2032

8.4.4.South Africa

8.4.4.1.Market size analysis, by Insurance Type, 2022-2032

8.4.4.2.Market size analysis, by Distribution Channel, 2022-2032

8.4.4.3.Market size analysis, by End User, 2022-2032

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Insurance Type, 2022-2032

8.4.5.2.Market size analysis, by Distribution Channel, 2022-2032

8.4.5.3.Market size analysis, by End User, 2022-2032

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2022

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2022

10.Company Profiles

10.1.Allianz

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.AXA

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.Aon PLC

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.American International Group Inc

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Arthur J. Gallagher & Co

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Chubb

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.Lloyd's

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.Marsh LLC

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.Zurich Insurance Group Ltd

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.Lockton Companies

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com