Global Self Service Supermarket Sensor Market Report

RA08682

Global Self Service Supermarket Sensor Market by Component (Systems and Services), Type (Cash Based Systems and Cashless Based Systems), and Region (North America, Europe, Asia-Pacific, and LAMEA): Opportunity Analysis and Industry Forecast, 2023-2032

Self Service Supermarket Sensor Overview

Self-checkout systems are automated systems used in the retail, grocery, and hospitality industries to assist customers with self-ordering and checkout without the intervention of workers. Earlier self-checkout systems required a lot of storage space and were made up of individual and off-the-shelf components. Modern self-checkout systems, on the other hand, are modified and manufactured to fulfill market demand and to improve functionality, cost, form factors, and dependability.

Self service supermarket sensor refer to the use of various sensors and technologies to enhance the shopping experience of customers in supermarkets. These sensors can be used to track inventory levels, monitor foot traffic, analyze shopper behavior, and provide personalized recommendations to customers. Radio frequency identification (RFID) tags are commonly used in the self service supermarket sensor to track inventory levels and ensure that products are restocked in a timely manner. These tags can be attached to products and scanned by sensors to provide real-time information on product availability and shelf location.

Global Self Service Supermarket Sensor Market Analysis

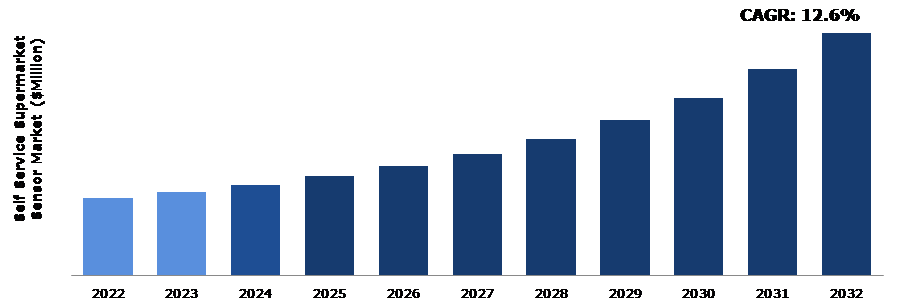

The Global Self Service Supermarket Sensor Market Size was $3,400.0 million in 2022 and is predicted to grow with a CAGR of 12.6%, by generating a revenue of $10,678.7 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Self Service Supermarket Sensor Market

The COVID-19 pandemic created challenges for the self service supermarket sensor market. Though the pandemic also created opportunities for sensor systems to enable contactless technologies and help with inventory management. As a result of the pandemic, retailers may have reduced budgets for new technologies and capital investments, which can make it more difficult to justify the investment in sensor systems. Economic downturns can create uncertainty in the market, making it more difficult for retailers to plan and make investment decisions. The worldwide market landscape has changed dramatically after the COVID-19 pandemic. The virus's breakout and the accompanying measures put in place have had a significant impact on a variety of businesses and markets. Companies in various industries are adapting to the new normal in the post-COVID-19 period, which is characterized by shifting customer behaviors, increasing attention on cleanliness and safety, and quicker adoption of digital technology.

Consumer preferences and purchase habits have shifted as a result of the pandemic. With restrictions and lockdowns in place, e-commerce and Internet shopping have seen an increase in demand as people looked for convenient and frictionless methods of accessing goods and services. This encouraged firms to improve their online presence and digital skills in order to satisfy the demands.

Rising Demand for Improved Customer Experience to Drive the Market Growth

Increase in need for improved customer experience is one of the primary drivers of the self service supermarket sensor market growth. By using sensors and other technologies, retailers can provide customers with a more personalized and efficient shopping experience. Sensors can be used to track a customer's shopping behavior and make personalized product recommendations based on their preferences. For example, if a customer frequently purchases organic products, the sensor system can suggest similar products or offer personalized coupons. Self-checkout systems using sensors can speed up the checkout process, eliminating the need for customers to wait in long billing queues. By scanning products and automatically deducting them from the customer's account, sensors can provide a faster and more efficient checkout experience. Sensors can be used to monitor foot traffic and analyze shopper behavior, allowing retailers to optimize store layouts and product placements. For example, sensors can determine which areas of the store are most frequently visited and adjust product displays accordingly.

To know more about global self service supermarket sensor market drivers, get in touch with our analysts here.

Lack of Awareness about the Self Service Supermarket to Restrain the Market Growth

Lack of awareness regarding self service supermarket sensors in undeveloped regions is expected to limit market growth. It is anticipated that the rising incidences of shoplifting, fraud, and skimming will hinder market expansion. Another factor that could have an effect on the market expansion is the elderly population's reluctance to use self-checkout services. Seniors with mobility problems and ailments like dementia, hearing loss, vision loss, and memory loss need more in-person care. In addition, the lack of technical expertise in developing nations frequently results in the avoidance of self-checkout systems at retail establishments. All these are the major factors anticipated to hamper the self service supermarket sensor market growth during the forecast period.

Increasing Use of AI and IoT in Self Service Supermarket Systems to Drive Excellent Opportunities

Various organizations aim to provide a shopping experience that meets the consumer's digital wants and expectations. Self-checkout systems utilizing AI technology, for example, aims to improve revenues while also streamlining all shopping activities. Customers may scan items, pay, and obtain receipts fast and without waiting due to this revolutionary technology. These self-service checkout technologies, aided by artificial intelligence, allow to recognize objects easily. In other words, they recognize items almost instantaneously and from any perspective. This cutting-edge technology allows for more convenient and personalized experiences, as well as more automation and less physical contact.. With personalized information and services available at the click of a button on all social media, entertainment, and e-commerce platforms, customers want the same level of customization to occur in the offline world, notably in physical businesses. The autonomy afforded by self-checkout systems with artificial intelligence leads customers through the purchasing process and assists them in saving money and time. In addition to this, AI technologies enable this experience to run smoothly since they regulate everything the customer puts in the basket - specifically, using cameras and sensors. Image recognition software is also available to help organizations easily identify consumers and their purchasing habits. Therefore, the consumer may be recommended products or given advice on a product that is in stock.

To know more about global self service supermarket sensor market opportunities, get in touch with our analysts here.

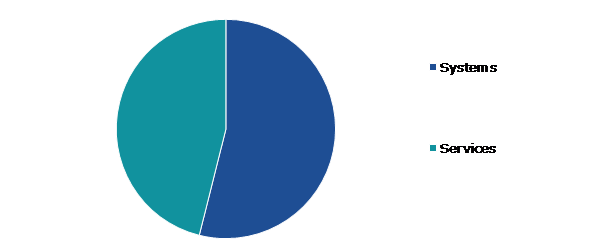

Global Self Service Supermarket Sensor Market Size, by Component, 2022

Source: Research Dive Analysis

The systems sub-segment accounted for the highest market share in 2022. The considerable share is due to the increase in usage of cutting-edge technology in self-checkout systems, such as artificial intelligence, voice interface, and computer vision. Retailers prefer new hardware systems to outdated checkout techniques. The most recent hybrid self-checkout systems contain advanced security measures, big coin dispenser capacity, user-friendly customer interfaces, multi-item scanning, and cashless transactions. Furthermore, rising consumer desire for both cash and cashless transactions is encouraging retailers to install brand-new and high-tech systems.

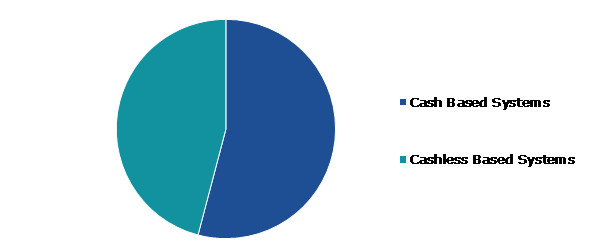

Global Self Service Supermarket Sensor Market Share, by Type, 2022

Source: Research Dive Analysis

The cash based systems sub-segment accounted for the highest market share in 2022. The market is being driven by the rising number of paper-based transaction options available to small, medium, and large merchants. Customers who just have a few items in their bags prefer to pay at retail self-service kiosks. Furthermore, many clients prefer to pay with cash which is projected to drive the segment growth. Another element factor influencing boosting market growth is the government's promotion of cash-based transactions at retail outlets.

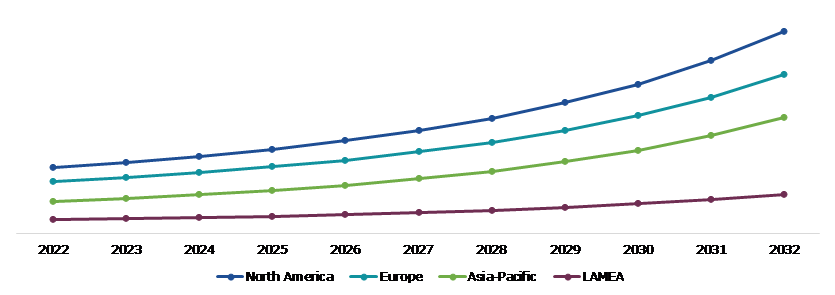

Global Self Service Supermarket Sensor Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The North America self service supermarket sensor market generated the highest revenue in 2022. North America is known for its highly advanced technology and infrastructure. The growth of the regional market is expected to be aided by the expansion of the retail and hospitality industries, as well as the rising trend of automation and digitalization. Retail stores in the region are expanding through hyperlocal services and gradually embracing omnichannel tactics to provide customers with a smooth shopping experience. Other factors that contribute to regional market expansion include increasing urbanization, contact less shopping experience, and the adoption of new technology.

Competitive Scenario in the Global Self Service Supermarket Sensor Market

Investment and agreement are common strategies followed by major market players. For instance, in May 2023, Teamwork Commerce, a global retail management software company, announced the release of their RFID-Powered Self-Checkout solution, which is intended to make the checkout process easier for in-store customers. Customers may rapidly scan all purchases and cut checkout times, making in-store experiences more convenient.

Source: Research Dive Analysis

Some of the leading self service supermarket sensor market players are Diebold Nixdorf, Incorporated ECR Software Corporation, FUJITSU, Gilbarco Inc., ITAB Group, NCR Corporation, Pan-Oston, PCMS Group Ltd., Strong Point, and Toshiba Global Commerce Solutions.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Component |

|

| Segmentation by Type |

|

| Key Companies Profiled |

|

Q1. What is the size of the global self service supermarket sensor market?

A. The size of the global self service supermarket sensor market was over $3,400.0 million in 2022 and is projected to reach $10,678.7 million by 2032.

Q2. Which are the major companies in the self service supermarket sensor market?

A. Diebold Nixdorf, Incorporated ECR Software Corporation, and FUJITSU are some of the key players in the global self service supermarket sensor market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific self service supermarket sensor market?

A. Asia-Pacific self service supermarket sensor market is anticipated to grow at 14.2% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Strong Point and Toshiba Global Commerce Solutions are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global self service supermarket sensor market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on self service supermarket sensor market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Self Service Supermarket Sensor Market Analysis, by Component

5.1.Overview

5.2.Systems

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2022-2032

5.2.3.Market share analysis, by country,2022-2032

5.3.Services

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2022-2032

5.3.3.Market share analysis, by country,2022-2032

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Self Service Supermarket Sensor Market Analysis, by Type

6.1.Overview

6.2.Cash Based Systems

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2022-2032

6.2.3.Market share analysis, by country,2022-2032

6.3.Cashless Based Systems

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2022-2032

6.3.3.Market share analysis, by country,2022-2032

6.4.Research Dive Exclusive Insights

6.4.1.Market attractiveness

6.4.2.Competition heatmap

7.Electronic Protection Device Coatings Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Component,2022-2032

7.1.1.2.Market size analysis, by Type,2022-2032

7.1.2.Canada

7.1.2.1.Market size analysis, by Component,2022-2032

7.1.2.2.Market size analysis, by Type,2022-2032

7.1.3.Mexico

7.1.3.1.Market size analysis, by Component,2022-2032

7.1.3.2.Market size analysis, by Type,2022-2032

7.1.4.Research Dive Exclusive Insights

7.1.5.Market attractiveness

7.1.6.Competition heatmap

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Component,2022-2032

7.2.1.2.Market size analysis, by Type,2022-2032

7.2.2.UK

7.2.2.1.Market size analysis, by Component,2022-2032

7.2.2.2.Market size analysis, by Type,2022-2032

7.2.3.France

7.2.3.1.Market size analysis, by Component,2022-2032

7.2.3.2.Market size analysis, by Type,2022-2032

7.2.4.Spain

7.2.4.1.Market size analysis, by Component,2022-2032

7.2.4.2.Market size analysis, by Type,2022-2032

7.2.5.Italy

7.2.5.1.Market size analysis, by Component,2022-2032

7.2.5.2.Market size analysis, by Type,2022-2032

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Component,2022-2032

7.2.6.2.Market size analysis, by Type,2022-2032

7.2.7.Research Dive Exclusive Insights

7.2.8.Market attractiveness

7.2.9.Competition heatmap

7.3.Asia-Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Component,2022-2032

7.3.1.2.Market size analysis, by Type,2022-2032

7.3.2.Japan

7.3.2.1.Market size analysis, by Component,2022-2032

7.3.2.2.Market size analysis, by Type,2022-2032

7.3.3.India

7.3.3.1.Market size analysis, by Component,2022-2032

7.3.3.2.Market size analysis, by Type,2022-2032

7.3.4.Australia

7.3.4.1.Market size analysis, by Component,2022-2032

7.3.4.2.Market size analysis, by Type,2022-2032

7.3.5.South Korea

7.3.5.1.Market size analysis, by Component,2022-2032

7.3.5.2.Market size analysis, by Type,2022-2032

7.3.6.Rest of Asia-Pacific

7.3.6.1.Market size analysis, by Component,2022-2032

7.3.6.2.Market size analysis, by Type,2022-2032

7.3.7.Research Dive Exclusive Insights

7.3.8.Market attractiveness

7.3.9.Competition heatmap

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Component,2022-2032

7.4.1.2.Market size analysis, by Type,2022-2032

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Component,2022-2032

7.4.2.2.Market size analysis, by Type,2022-2032

7.4.3.UAE

7.4.3.1.Market size analysis, by Component,2022-2032

7.4.3.2.Market size analysis, by Type,2022-2032

7.4.4.South Africa

7.4.4.1.Market size analysis, by Component,2022-2032

7.4.4.2.Market size analysis, by Type,2022-2032

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Component,2022-2032

7.4.5.2.Market size analysis, by Type,2022-2032

7.4.6.Research Dive Exclusive Insights

7.4.7.Market attractiveness

7.4.8.Competition heatmap

8.Competitive Landscape

8.1.Top winning strategies, 2022

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2022

9.Company Profiles

9.1.Diebold Nixdorf, Incorporated

9.1.1.Overview

9.1.2.Business segments

9.1.3.Product portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.ECR Software Corporation

9.2.1.Overview

9.2.2.Business segments

9.2.3.Product portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.FUJITSU

9.3.1.Overview

9.3.2.Business segments

9.3.3.Product portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4.Gilbarco Inc.

9.4.1.Overview

9.4.2.Business segments

9.4.3.Product portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.ITAB Group.

9.5.1.Overview

9.5.2.Business segments

9.5.3.Product portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.NCR Corporation

9.6.1.Overview

9.6.2.Business segments

9.6.3.Product portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.Pan-Oston.

9.7.1.Overview

9.7.2.Business segments

9.7.3.Product portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.PCMS Group Ltd.

9.8.1.Overview

9.8.2.Business segments

9.8.3.Product portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

9.9.Strong Point

9.9.1.Overview

9.9.2.Business segments

9.9.3.Product portfolio

9.9.4.Financial performance

9.9.5.Recent developments

9.9.6.SWOT analysis

9.10.Toshiba Global Commerce Solutions

9.10.1.Overview

9.10.2.Business segments

9.10.3.Product portfolio

9.10.4.Financial performance

9.10.5.Recent developments

9.10.6.SWOT analysis

In the ever-evolving world of retail, technology continues to revolutionize the shopping experience. Self-service supermarket sensors are among the latest innovations that have gained prominence in the industry. By leveraging advanced technologies, these sensors are transforming the way customers shop and empowering store management with real-time data and insights. One of the key benefits of self-service supermarket sensors is their ability to streamline inventory management. By employing technologies, such as radio-frequency identification (RFID) and computer vision, these sensors enable accurate and automated tracking of products throughout the store. This reduces the need for manual stock checks, ensuring that shelves are adequately stocked, and reducing instances of out-of-stock items. Store managers can access real-time data on product availability, allowing them to optimize inventory levels, plan restocking efficiently, and improve overall operational efficiency.

Moreover, these sensors can provide detailed information about products, such as pricing, ingredients, and allergen warnings, through interactive displays or mobile applications. This can allow customers to easily locate the items within the store using digital store maps, which can guide them to the exact aisle or shelf. Additionally, the sensors offer personalized recommendations and promotions based on individual preferences and purchase history, making the shopping experience more convenient and tailored to the customer’s needs.

Forecast Analysis of the Self Service Supermarket Sensor Market

According to the report published by Research Dive, the global self service supermarket sensor market is projected to garner a revenue of $10,678.7 million and rise at a striking CAGR of 12.6% over the estimated timeframe from 2023 to 2032.

The increasing use of sensors and other technologies in the retail industry to provide a more personalized and efficient shopping experience to customers is expected to fortify the growth of the market over the estimated timeframe. Moreover, the increasing implementation of AI and IoT in self- service supermarket systems to provide more convenient and customized experiences to customers globally is predicted to create wide growth opportunities for the self service supermarket sensor market over the analysis period. However, the lack of awareness about the self-service supermarket may hinder the growth of the market throughout the analysis period.

The major players of the self service supermarket sensor market include Toshiba Global Commerce Solutions, Diebold Nixdorf, Incorporated, Strong Point, ITAB Group, ECR Software Corporation, PCMS Group Ltd., FUJITSU, NCR Corporation, Gilbarco Inc., and many more.

Self Service Supermarket Sensor Market Developments

The key companies operating in the industry are adopting various growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, which is subsequently helping the global self service supermarket sensor market to grow exponentially. For instance:

- In August 2022, Vontier Corporation, a global industrial technology company announced its acquisition of Invenco, a global provider of self-service payment solutions. With this acquisition, the companies aimed to develop modern, innovative, and highly-secured solutions for retailers that would satisfy their dynamic needs and offer them different energy futures, automated consumer services, and digital payments.

- In January 2023, Fujitsu Frontech North America Inc., a leading provider of innovative retail technology and front-end solutions introduced the next-generation retail service innovation, namely Fujitsu S3 (Self-Service Simplified). This innovation would help retailers to transform operations and improve productivity with engaging experiences by delivering self-service solutions that are easy to deploy.

- In September 2023, Diebold Nixdorf, a leading provider of world-leading banking solutions and retail technology systems announced its collaboration with WMF Professional Coffee Machines, a renowned German-based supplier of coffee machines for commercial use. This collaboration would benefit WMF to attract new customers with Diebold Nixdorf’s point-of-sale (POS) and self-service systems.

Most Profitable Region

The North America region of the self service supermarket sensor market held the highest market share in 2022. The rising trend of automation and digitalization in the retail industry across the region to provide customers with a smooth shopping experience is expected to drive the growth of the market over the estimated period. Furthermore, the growing expansion of the retail and hospitality industries in the region is predicted to boost the regional growth of the market throughout the forecast period.

Covid-19 Impact on the Self Service Supermarket Sensor Market

Initially, though the outbreak of the Covid-19 pandemic has brought numerous challenges to the self service supermarket sensor market, it has brought several opportunities for the market as well. Due to the economic slowdown and market uncertainty, many retailers have reduced their budgets for new technologies and capital investments. This made it tough for retailers to take investment decisions for sensor systems. However, the increasing preference of customers to shop online and quicker adoption of digital technology across industries have provided various growth opportunities for the market throughout the crisis.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com