Global Polycrystalline Diamond Market Report

RA08681

Global Polycrystalline Diamond Market by Type (PCD Milling Tools, PCD Turning Tools, and Others), Application (Automotive, Machinery, Aerospace, Semiconductors, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Opportunity Analysis and Industry Forecast, 2023-2032

Polycrystalline Diamond Overview

Polycrystalline diamond (PCD) is composed of diamond grit that has fused together under high pressure, high temperature, and in the presence of a catalytic metal. Diamonds are used in the creation of cutting tools due to its extraordinary hardness, resistance to wear, and ability to transfer heat. PCD tools can be used for machining any non-ferrous material, including wood products, chipboards, high density fiberboard (HDF), laminated boards, materials used to make aluminum auto parts, and all lightweight materials used to build aircraft, including metal matrix composites (MMC), stacks, and carbon fiber reinforced plastics (CFRP).

Utilizing efficient tools for material cutting and surface finishing is essential with the economic viability of many processes and industries. In certain situations, hard tools can be more cost-effective than standard ones. Diamond is one of these incredibly tough, naturally occurring materials that is more durable than silicon carbide and corundum.

Global Polycrystalline Diamond Market Analysis

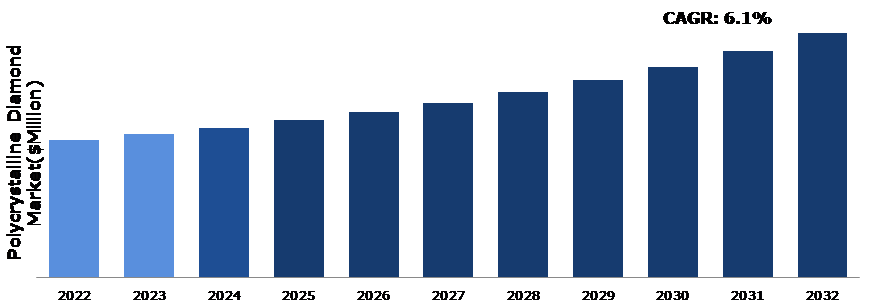

The Global Polycrystalline Diamond Market Size was $900.6 million in 2022 and is predicted to grow with a CAGR of 6.1%, by generating a revenue of $1,604.0 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Polycrystalline Diamond Market

The global polycrystalline diamond industry was negatively impacted by the COVID-19 impact on polycrystalline diamond market, which resulted in reduced exploration activities and lower demand for drilling equipment. Government considered oil & gas exploration as a critical activity and exempted it from lockdown restrictions. However, the pandemic caused either a halt or a reduction in production. Throughout the pandemic, operations were difficult due to a labor shortage, and difficulties arose owing to social isolation and other precautionary measures. Furthermore, a lack of raw materials and equipment during the pandemic also hampered the growth of drilling, repairing, maintaining, and replacing components in the automotive and aerospace industries. The COVID-19 pandemic led to reduced demand for polycrystalline diamond products in some industries, particularly in automotive and aerospace . This impacted the demand for polycrystalline diamond products used in these industries, such as cutting tools for the aerospace industry. The pandemic had a significant impact on the aerospace industry, with decreased demand for flights leading to a decrease in orders for airplanes and associated products. This has influenced the market for polycrystalline diamond products used in the production of cutting tools and other aerospace components.

Growing Applications of Polycrystalline Diamond in the Industrial Sector to Drive the Market Growth

One of the most important improvements in drilling equipment in recent years has been the development of polycrystalline diamond compact (PDC) drill bits. These bits have completely transformed the oil & gas drilling sector’s high rate of penetration (ROP) potential. Typically, steel or matrix bodies with synthetic diamond cutters are used to create these drill bits. Diamond tables that are a component of the cutter are created using a polycrystalline diamond. PDC diamond tables are tough and have a wide range of bit cutter-friendly characteristics. In addition, the growth of the global polycrystalline diamond compact is anticipated to be driven by rising shale gas performance and production. The industrial use of polycrystalline diamond (PCD) is predicted to increase, which is further expected to support the market growth. Polycrystalline diamond is appropriate for a variety of industrial applications due to its superior hardness, wear resistance, and thermal conductivity. PCD is often used in cutting tools and machining for industrial processes like turning, milling, and drilling. It can be machined at high speeds and has longer tool lives because of its hardness and wear resistance, which boosts production and reduces costs. Polycrystalline diamond finds applications in the metalworking industry to cut and shape hardened metals, alloys, and composite materials. In difficult metalworking procedures, PCD tools can produce excellent precision and surface polish.

To know more about global polycrystalline diamond market drivers, get in touch with our analysts here.

High Cost of Polycrystalline Diamond to Restrain the Market Growth

Polycrystalline diamond is a relatively expensive material compared to other cutting and drilling tools, which is expected to limit its adoption in some industries. High initial investment costs is also projected to be a barrier for small and medium-sized businesses or developing countries with limited financial resources. These factors can impact the availability of raw materials and the ability of companies to do business in certain countries, which is anticipated to limit the polycrystalline diamond market growth opportunities in the upcoming years.

Use of Polycrystalline Diamond in the Manufacturing and Construction Sector to Drive Excellent Opportunities

Matrix body drill bits provide several advantages, including longer life, higher fluid capacity, and several runs. This tool has high structural strength as well as resistance to erosion, wear, and tear. Rising demand for matrix body PDC drill bits is expected to increase the need of advanced and efficient drilling technologies in the future. Polycrystalline diamond is widely utilized in the manufacturing, building, mining, and other sectors due to its greater hardness and endurance. As these sectors continue to seek high-performance cutting and drilling equipment, the demand for polycrystalline diamond is likely to increase. Polycrystalline diamond is utilized in various sectors to cut and shape materials such as carbon fiber composites and high-strength metals. In the construction sector, polycrystalline diamond (PCD) is frequently used for various of application, including cutting and polishing hard materials like concrete and asphalt. PCD tools are especially useful for tasks that require high precision and durability, and they offer greater abrasive wear resistance than other diamond tools. In addition, PCD polishing tools are used to polish marble and other fine stone surfaces, while PCD tool inserts are utilized in machines to engrave ceramics and high-speed metal. All these factors are projected to drive the polycrystalline diamond market growth during the forecast period.

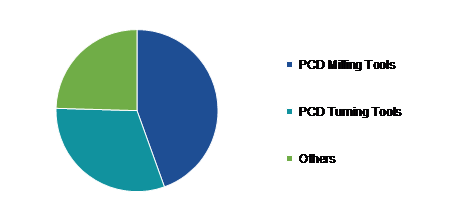

Global Polycrystalline Diamond Market Size, by Type, 2022

Source: Research Dive Analysis

The PCD milling tools sub-segment accounted for the highest market share in 2022. PCD milling tools have numerous advantages compared to traditional carbide milling tools. This results in reduced processing time, superior surface finish, better process control, and reduced downtime. In addition, as the main component of PCD tools is diamond, the cutting and grinding forces are greater than other tools, allowing for higher cutting and grinding rates. Another advantage of PCD milling tools is that they can produce stronger tolerances than conventional tools, leading to greater accuracy. PCD milling tools are ideal for high volume production, as the tools require less frequent sharpening and maintenance, ultimately reducing costs. These factors are anticipated to boost the growth of the PCD milling tools sub-segment during the forecast time.

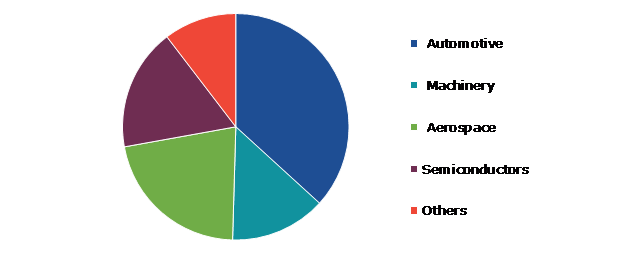

Global Polycrystalline Diamond Market Share, by Application, 2022

Source: Research Dive Analysis

The automotive sub-segment accounted for the highest market share in 2022. Polycrystalline diamond tools are widely utilized in the automobile sector due to their greater efficiency and accuracy. They are ideal for high-speed machining and can reach surface speeds of up to 9,000 feet per minute. In addition, polycrystalline diamond tools produce less heat during the cutting process, making them suitable for use on materials like aluminum that are susceptible to warping or distortion due to high temperatures. They are therefore perfect for cutting gearbox and engine parts, including pistons and cylinder heads. Tools made of polycrystalline diamond are also resistant to severe wear and tear, making them a more durable option for automakers and possibly reducing production costs. Overall, the use of polycrystalline diamond tools can significantly increase productivity and precision in the automotive sector. These factors are anticipated to boost the growth of the automotive sub-segment in the upcoming years.

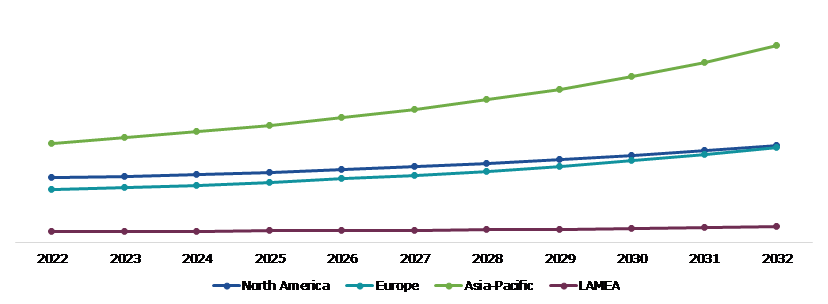

Global Polycrystalline Diamond Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Asia-Pacific polycrystalline diamond market generated the highest revenue in 2022 and is anticipated to show the fastest growth during the forecast period. This growth is due to the significant demand for diamond tools in the construction, automotive, aerospace, oil & gas, and other industries. The market for polycrystalline diamonds is anticipated to be driven by the increasing oil & gas exploration and production in Asia-Pacific. The high hardness of polycrystalline diamond (PCD) tools, which makes them extremely wear-resistant and robust, is one of their benefits driving the regional market growth. PCD tool producers in Asia-Pacific use cutting-edge technologies and sophisticated manufacturing processes to create PCD tools that are incredibly effective, long-lasting, and efficient. PCD tool makers in Asia-Pacific are dedicated to continuously enhancing their products to satisfy the changing needs of the market. All these factors are projected to drive the polycrystalline diamond market share in Asia-Pacific during the forecast period.

Competitive Scenario in the Global Polycrystalline Diamond Market

Investment and agreement are common strategies followed by major market players. For instance, in February 2021, NOC Inc., a global provider of equipment and components that are used in oil & gas drilling and production operations, oilfield services, and supply chain integration services to the upstream oil & gas industry, introduced ION+ polycrystalline diamond compact cutter technology. ION+ cutters feature a wide range of application-specific cutter grades, incorporating refined diamond feeds, higher man.

Source: Research Dive Analysis

Some of the leading polycrystalline diamond market analysis players are Sandvik Group, Mapal Kennametal, Preziss Tool, Wirutex, Ceratizat, Sumitomo Electric, Kyocera, Mitsubishi Materials, and Union Tool.

| Aspect | Particulars |

| Historical Market Estimations | 2021-2022 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global polycrystalline diamond market?

A. The size of the global polycrystalline diamond market size was over $900.6 million in 2022 and is projected to reach $1,604.0 million by 2032.

Q2. Which are the major companies in the polycrystalline diamond market?

A. Nudge Rewards Inc. and GuideSpark Sandvik Group, Mapal, Kennametal, and Preziss Tool are some of the key players in the global polycrystalline diamond market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific polycrystalline diamond market?

A. The Asia-Pacific polycrystalline diamond market share is anticipated to grow at 7.3% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Sandvik Group, Mapal, Kennametal, and Preziss Tool are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Polycrystalline Diamond market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Polycrystalline Diamond market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Polycrystalline Diamond Market Analysis, by Type

5.1.Overview

5.2.PCD Milling Tools

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2022-2032

5.2.3.Market share analysis, by country, 2022-2032

5.3.PCD Turning Tools

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2022-2032

5.3.3.Market share analysis, by country, 2022-2032

5.4.Others

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region, 2022-2032

5.4.3.Market share analysis, by country, 2022-2032

5.4.4.Research Dive Exclusive Insight

5.5.Research Dive Exclusive Insights

5.5.1.Market attractiveness

5.5.2.Competition heatmap

6.Polycrystalline Diamond Market Analysis, by Application

6.1.Automotive

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2022-2032

6.1.3.Market share analysis, by country, 2022-2032

6.2.Machinery

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2022-2032

6.2.3.Market share analysis, by country, 2022-2032

6.3.Aerospace

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region, 2022-2032

6.3.3.Market share analysis, by country, 2022-2032

6.4.Semiconductors

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region, 2022-2032

6.4.3.Market share analysis, by country, 2022-2032

6.5.Others

6.5.1.Definition, key trends, growth factors, and opportunities

6.5.2.Market size analysis, by region, 2022-2032

6.5.3.Market share analysis, by country, 2022-2032

6.6.Research Dive Exclusive Insights

6.6.1.Market attractiveness

6.6.2.Competition heatmap

7.Polycrystalline Diamond Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Type, 2022-2032

7.1.1.2.Market size analysis, by Application, 2022-2032

7.1.2.Canada

7.1.2.1.Market size analysis, by Type, 2022-2032

7.1.2.2.Market size analysis, by Application, 2022-2032

7.1.3.Mexico

7.1.3.1.Market size analysis, by Type, 2022-2032

7.1.3.2.Market size analysis, by Application, 2022-2032

7.1.4.Research Dive Exclusive Insights

7.1.4.1.Market attractiveness

7.1.4.2.Competition heatmap

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Type, 2022-2032

7.2.1.2.Market size analysis, by Application, 2022-2032

7.2.2.UK

7.2.2.1.Market size analysis, by Type, 2022-2032

7.2.2.2.Market size analysis, by Application, 2022-2032

7.2.3.France

7.2.3.1.Market size analysis, by Type, 2022-2032

7.2.3.2.Market size analysis, by Application, 2022-2032

7.2.4.Spain

7.2.4.1.Market size analysis, by Type, 2022-2032

7.2.4.2.Market size analysis, by Application, 2022-2032

7.2.5.Italy

7.2.5.1.Market size analysis, by Type, 2022-2032

7.2.5.2.Market size analysis, by Application, 2022-2032

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Type, 2022-2032

7.2.6.2.Market size analysis, by Application, 2022-2032

7.2.7.Research Dive Exclusive Insights

7.2.7.1.Market attractiveness

7.2.7.2.Competition heatmap

7.3.Asia-Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Type, 2022-2032

7.3.1.2.Market size analysis, by Application, 2022-2032

7.3.2.Japan

7.3.2.1.Market size analysis, by Type, 2022-2032

7.3.2.2.Market size analysis, by Application, 2022-2032

7.3.3.India

7.3.3.1.Market size analysis, by Type, 2022-2032

7.3.3.2.Market size analysis, by Application, 2022-2032

7.3.4.Australia

7.3.4.1.Market size analysis, by Type, 2022-2032

7.3.4.2.Market size analysis, by Application, 2022-2032

7.3.5.South Korea

7.3.5.1.Market size analysis, by Type, 2022-2032

7.3.5.2.Market size analysis, by Application, 2022-2032

7.3.6.Rest of Asia-Pacific

7.3.6.1.Market size analysis, by Type, 2022-2032

7.3.6.2.Market size analysis, by Application, 2022-2032

7.3.7.Research Dive Exclusive Insights

7.3.7.1.Market attractiveness

7.3.7.2.Competition heatmap

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Type, 2022-2032

7.4.1.2.Market size analysis, by Application, 2022-2032

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Type, 2022-2032

7.4.2.2.Market size analysis, by Application, 2022-2032

7.4.3.UAE

7.4.3.1.Market size analysis, by Type, 2022-2032

7.4.3.2.Market size analysis, by Application, 2022-2032

7.4.4.South Africa

7.4.4.1.Market size analysis, by Type, 2022-2032

7.4.4.2.Market size analysis, by Application, 2022-2032

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Type, 2022-2032

7.4.5.2.Market size analysis, by Application, 2022-2032

7.4.6.Research Dive Exclusive Insights

7.4.6.1.Market attractiveness

7.4.6.2.Competition heatmap

8.Competitive Landscape

8.1.Top winning strategies, 2022

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2022

9.Company Profiles

9.1.Sandvik Group

9.1.1.Overview

9.1.2.Business segments

9.1.3.Type portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.Mapal

9.2.1.Overview

9.2.2.Business segments

9.2.3.Type portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.Kennametal

9.3.1.Overview

9.3.2.Business segments

9.3.3.Type portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4.Preziss Tool

9.4.1.Overview

9.4.2.Business segments

9.4.3.Type portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.Wirutex.

9.5.1.Overview

9.5.2.Business segments

9.5.3.Type portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.Ceratizat

9.6.1.Overview

9.6.2.Business segments

9.6.3.Type portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.Sumitomo Electric

9.7.1.Overview

9.7.2.Business segments

9.7.3.Type portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.Kyocera

9.8.1.Overview

9.8.2.Business segments

9.8.3.Type portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

9.9.Mitsubishi Materials

9.9.1.Overview

9.9.2.Business segments

9.9.3.Type portfolio

9.9.4.Financial performance

9.9.5.Recent developments

9.9.6.SWOT analysis

9.10.Union Tool

9.10.1.Overview

9.10.2.Business segments

9.10.3.Type portfolio

9.10.4.Financial performance

9.10.5.Recent developments

9.10.6.SWOT analysis

In today's fast changing world, where technological developments drive innovation across multiple industries, the need for high-performance materials has never been greater. One such substance that has received a great deal of attention is Polycrystalline diamond (PCD).

The polycrystalline diamond market has grown significantly in recent years because of its unique characteristics and many applications. Polycrystalline diamond (PCD) is made up of diamond grit that has melted together under high temperature, high pressure, and the presence of a catalytic metal. Diamonds are employed in the production of cutting tools due to their exceptional hardness, ability to transfer heat, and wear resistance. PCD tools may be used to manufacture any nonferrous material, such as wood, high density fiberboard (HDF), chipboards, laminated boards, materials used to create aluminum auto parts, and all lightweight materials.

Recent Trends in the Polycrystalline Diamond Market

The polycrystalline diamond market is continuously evolving, with new technologies and applications emerging. PCD manufacturers have been focusing on providing customized solutions to fulfil unique customer requirements. Tailored PCD solutions with unique binder materials, grain sizes, and diamond content are being developed to optimize performance in various applications. Additionally, there is a rising need for eco-friendly products as sustainability is being emphasized more and more. PCD, as a synthetic diamond substance, provides a more sustainable alternative to natural diamonds, reducing the environmental impact of diamond mining.

Newest Insights in the Polycrystalline Diamond Market

As per a report by Research Dive, the global polycrystalline diamond market is expected to grow at a CAGR of 6.1% and generate revenue of $1,604.0 million by 2032. The primary factors driving the growth of the market are the growing shale gas performance and production, the expanding use of polycrystalline diamond in the manufacturing and construction industries, and the rising demand for matrix body PDC drill bits, which increase the demand for cutting-edge and effective drilling technology. However, the high initial investment costs of polycrystalline diamond are expected to hinder the market growth.

The polycrystalline diamond market in Asia-Pacific is expected to remain dominant in the coming years. The region's high revenue in 2022 was driven by rising oil and gas exploration and production as well as the growing demand for diamond tools in the oil and gas, construction, automotive, and other industries. This has led to a rising demand for high-quality cutting and drilling tools developed from polycrystalline diamond (PCD).

How are Market Players Responding to the Rising Demand for Polycrystalline Diamond?

Market players are responding to the rising demand for polycrystalline diamond by investing in research and development to create more advanced and efficient polycrystalline diamond (PCD) products. They are also boosting their production capacity to satisfy the increasing market demand.

In addition, market players are increasingly focusing on strategic partnerships and collaborations with other players in the industry to leverage their strengths and expand their reach. Some of the foremost players in the polycrystalline diamond market are Mapal Kennametal, Sandvik Group, Preziss Tool, Ceratizat, Wirutex, Sumitomo Electric, Mitsubishi Materials, Union Tool, Kyocera, and others. These players are focused on implementing strategies such as mergers and acquisitions, novel developments, collaborations, and partnerships to reach a leading position in the global market.

For instance:

-

In Octobor 2020, Hyperion Materials & Technologies, a global leader in engineering and producing innovative materials with a U.S. base, announced Compax2.0TM SE (Superior Edge) is the company's newest grade of high-performance polycrystalline diamond (PCD), suited for machining nonferrous materials such as titanium alloys, aluminium, and graphite.

-

In February 2021, Kennametal, an American manufacturer and distributor of industrial supplies, launched a new series of PCD (Polycrystalline Diamond) round tools for cutting aluminium that offer up to ten times the productivity of carbide tooling. The new series of drills, reamers and end mills provides remarkable tool life and wear resistance even in highly abrasive aluminium alloys and is easily accessible with very short lead times.

-

In June 2022, Horn, a business that produces high-quality tools, launched new step drills with PCD-tipped cutting edges for drilling, boring, and countersinking nonferrous metals.

COVID-19 Impact on the Global Polycrystalline Diamond Market

The COVID-19 pandemic had an adverse impact on the global polycrystalline diamond market. During the pandemic, the government considered oil and gas drilling to be essential and exempted it from lockdown restrictions. However, the outbreak either stopped or decreased manufacturing. Moreover, throughout the outbreak, operations were difficult due to a labour scarcity, and challenges emerged because of social isolation and other cautious measures. Furthermore, during the pandemic, a lack of raw materials and equipment restricted the growth of repairing, drilling, maintaining, and replacing components in the aerospace and automotive industries. Thus, the pandemic affected demand for polycrystalline diamond products in various industries, most notably automotive and aerospace. This influenced the demand for products made of polycrystalline diamond that were employed in various sectors, like cutting tools for the aerospace sector. These factors significantly hindered the polycrystalline diamond market growth amidst the pandemic.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com