AI Accelerator Chip Market Report

RA08599

AI Accelerator Chip Market by Chip Type [Graphics Processing Unit (GPU), Application-Specific Integrated Circuit (ASIC), Field Programmable Gate Arrays (FPGA), Central Processing Unit (CPU) and Others], Processing Type (Edge and Cloud), Application [Natural Language Processing (NLP), Computer Vision, Robotics, and Network Security], Industry Vertical (Financial Services, Automotive and Transportation, Healthcare, Retail, Telecom, and Others) and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2031

Global AI Accelerator Chip Market Analysis

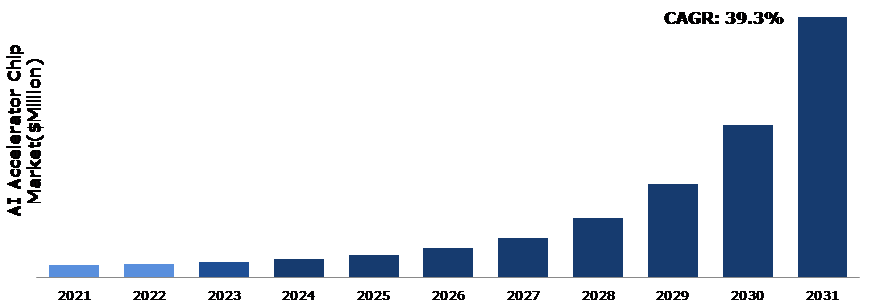

The Global AI Accelerator Chip Market Size was $14,948.6 million in 2021 and is predicted to grow with a CAGR of 39.3%, by generating a revenue of $332,142.7 million by 2031.

Global AI Accelerator Chip Market Synopsis

An AI accelerator is a high-performance parallel computation machine designed to execute AI workloads such as neural networks efficiently. Deep learning's rising usage is a key driver of the artificial intelligence accelerator industry. Deep learning reduces some of the data pre-processing required by machine learning. These systems can ingest and comprehend unstructured data like text and images, and they automate feature extraction, reducing the need for human experts. Deep learning is now considered a strong tool for enterprises that require meaningful insights and automated responses to vast volumes of unstructured data. Much of the advanced automation observed in business AI systems is due to the advancement and use of machine learning and deep learning. Such factors are expected to drive the global AI Accelerator Chip market share growth.

However, some of the disadvantages of AI accelerator chip include lack of technical knowledge. Users must have the technical knowledge to use these technologies. The requirement for cognitive thinking, deep learning, and Ml are technical abilities that must be developed. It is inoperable for people who lack technological expertise. Even minor errors in this program can produce significant changes in the results. The AI accelerator chip market size is hampered by a lack of competent workers. The need for AI chipsets is decreasing due to professional standards. These issues in the AI chipset industry may have an impact on the product's demand and supply.

The use of AI accelerator chip is anticipated to gain significant market share. Human resourcing AI will become anticipated to gain significant market share. The rise of AI technology is having a positive impact on AI accelerator chip market growth. Many developers nowadays find it difficult to create an interactive machine. Human involvement with AI accelerators brings up new opportunities for analysis. The advancement of human-ware AI creates new prospects for growth in the AI accelerators chips market trends.

In addition, the rise of the cyber safety business will provide new market growth prospects. The frequency of cyber-attacks is increasing. As a result of the increasing usage of mobile phones and technological gadgets, attackers have an easy target. These exposed dangers might put more at risk. AI accelerator chip industries are expected to increase in the coming years.

AI Accelerator Chip Market Overview

AI accelerator chips are specialist silicon chips that include AI accelerator technology used for machine learning. In several industrial verticals, AI assists in reducing or even eliminating the risk to human life. As the volume of data has expanded, so has the demand for more efficient methods for addressing mathematical and computational issues.

COVID-19 Impact on Global AI Accelerator Chip Market

The pandemic of COVID-19 harms the artificial intelligence accelerator chips market. The supply of cable and manufacturing in the market is declining. The semiconductors marketplace is facing many losses. The employees in the AI accelerator chips market are facing restrictions. Due to the COVID-19 spread, employees have limitations and few employees can work at the same time. In various countries, the supply of chipset is fully stopped. The pandemic has proved negative for the market and will continue to have a negative impact in the future years. This is due to the disruption of supply chain operations, the industrial sector, and the limited deployment of AI in developing sectors. As a result of the lockdown restrictions, various manufacturing firms have stopped production, causing disruptions in the global supply chain. According to the index of industrial production (IIP) statistics, manufacturing sector output fell 11.1% in July of 2020, as the COVID-19 lockout slowed the manufacturing process. This pandemic has slowed the development of AI-powered hardware and applications. Various sectors, such as automotive, manufacturing, and others, have been impacted the worst by this crisis, but numerous other industry verticals, such as healthcare manufacturing, medical devices, and others, have benefited from it, hence, to address such problems, prominent market participants are offering advance AI-based solutions to meet expanding customer demand.

THE USE OF AI ACCELERATOR CHIP IN HEALTHCARE INDUSTRY TO BOOST MARKET GROWTH

AI accelerator chip with artificial neural networks (ANN) improves medical data mining quality and the physician decision-making process. That is the technological application. In such a situation, the chip can make the customized healthcare product timelier, increase computing speed, and ultimately lead to a faster understanding of the personal and societal determinants of health and disease. By incorporating the photonic effect, the artificial intelligence accelerator improves data transmission reliability and ensures beneficial human-machine interactions. Artificial Neural Network (ANN) is a branch of AI and a machine learning technique inspired by the human brain that uses AI accelerator chips. These factors are anticipated to drive the AI accelerator chips market growth.

To know more about the global AI accelerator chip market drivers, get in touch with our analysts here.

Lack of Skilled AI Accelerator Chip Workforce to Restrain the Market Growth

The integration of AI solutions in the existing systems is a difficult task that requires extensive data processing to replicate the behavior of a human brain. Even a minor error can fail the system or can adversely affect the desired result. Furthermore, the absence of professional standards and certifications in AI/ML technologies is curbing the growth of AI accelerator chip. The AI accelerator chip service providers are facing challenges to service their solutions at their customer sites. This is because of a lack of technology awareness and limitations of AI accelerator chip experts.

To know more about the global AI accelerator chip market restraints, get in touch with our analysts here.

Use of AI Accelerator Chip Semiconductors to Offer Excellent Opportunities

AI hardware accelerators are providing the best opportunities for semiconductor companies. To adapt to an industry driven by the need for AI hardware, semiconductor makers will need to deliver industry-specific end-to-end solutions, innovation, and the creation of new software ecosystems. End-to-end services will provide chip manufacturers to collaborate with partners to build industry-specific AI hardware. The fast growth of AI is an opportunity for both the public and commercial sectors, and as a result, the relevance of AI to the semiconductor industry is growing at a fast pace.

To know more about global AI accelerator chip market opportunities, get in touch with our analysts here.

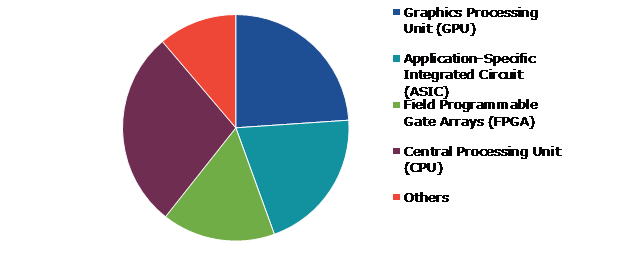

Global AI Accelerator Chip Market, by Chip Type

Based on chip type, the market has been divided into Graphics Processing Unit (GPU), Application-Specific Integrated Circuit (ASIC), Field Programmable Gate Arrays (FPGA), Central Processing Unit (CPU), and others. Among these, the Central Processing Unit (CPU) sub-segment accounted for the highest market share in 2021 whereas the Graphics Processing Unit (GPU) sub-segment is estimated to show the fastest growth during the forecast period.

Global AI Accelerator Chip Market Size, by Chip Type, 2021

Source: Research Dive Analysis

The Central Processing Unit (CPU) sub-type is anticipated to have a dominant market share in 2021. A CPU accelerator is a software application that speeds up program performance by altering how memory and processing power are allocated for execution of a program. A CPU is an integrated circuit, sometimes known as a chip, at the hardware level. This is commonly done to speed up a computer or improve performance when running software such as graphics or video editors, as well as computer games. While it is possible to overclock a CPU rather than employ a CPU accelerator chip, this is often more complex and can result in hardware damage.

The Graphics Processing Unit (GPU) sub-type is anticipated to show the fastest growth in 2021. GPUs (Graphics Processing Units) were originally intended for image processing but have achieved success in AI. A GPU has thousands of cores and can process thousands of threads at the same time. Because of their parallel computing architecture, GPUs are particularly powerful for large-scale data crunching.

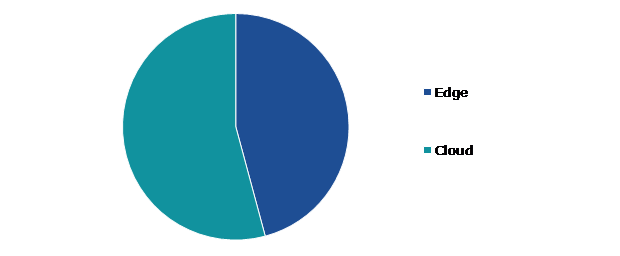

Global AI Accelerator Chip Market, by Processing Type

Based on processing type, the market has been divided into edge and cloud. Among these, the cloud sub-segment accounted for highest revenue share in 2021.

Global AI Accelerator Chip Market Forecast, by Processing Type, 2021

Source: Research Dive Analysis

The Cloud sub-segment is anticipated to have a dominant market share in 2021. A cloud acceleration chip is a form of service that enables content creators, publishers, and other organizations to provide material to end users or customers promptly. It offers the technology and services that allow material or data to arrive quickly at a requesting node. Cloud optimization is the act of reducing cloud resource waste by carefully choosing, providing, and sizing the resources used on certain cloud functionalities. Cloud optimization in a production context refers to discovering the most effective method to allocate cloud resources across distinct use cases.

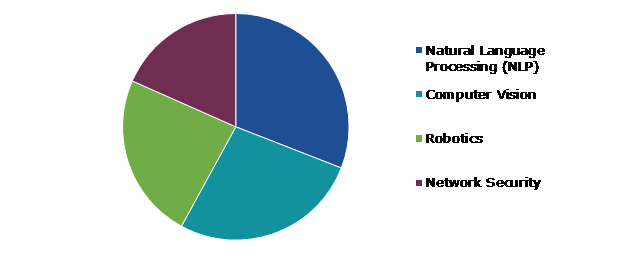

Global AI Accelerator Chip Market, by Application

Based on application, the market has been divided into natural language processing (NLP), computer vision, robotics, and network security. Among these, the natural language processing (NLP) sub-segment accounted for highest revenue share in 2021.

Global AI Accelerator Chip Market Growth, by Application, 2021

Source: Research Dive Analysis

The Natural Language Processing (NLP) sub-segment is anticipated to have a dominant market share in 2021. Natural language processing (NLP) is a set of artificial intelligence techniques that allow computers to recognize and understand human language. It contributes to making computers more accessible to individuals. Natural language processing bridges the gap between human communication and machine comprehension by utilizing computer science and computational linguistics. It accomplishes this by speedily evaluating massive volumes of textual data and comprehending the meaning of the instruction. Natural language processing allows computers to understand complex human concepts like purpose, mood, and emotion. It is akin to cognitive computing in that it tries to make computer-human interactions more natural.

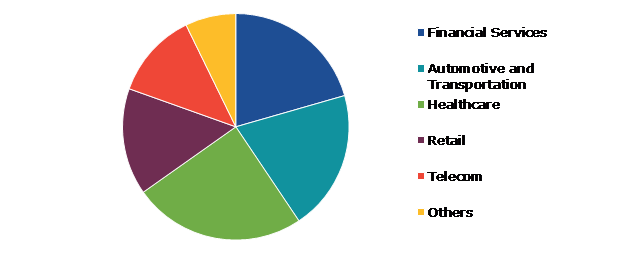

Global AI Accelerator Chip Market, by Industry Vertical

Based on industry vertical, the market has been divided into financial services, automotive and transportation, healthcare, retail, telecom, and others. Among these, the healthcare sub-segment accounted for highest revenue share in 2021.

Global AI Accelerator Chip Market Share, by Industry Vertical, 2021

Source: Research Dive Analysis

The Healthcare sub-segment is anticipated to have a dominant market share in 2021. GE Healthcare collaborated with Nex Cubed to create the Edison Accelerator program in Canada. The program's purpose is to accelerate, validate, and scale innovative solutions that solve critical issues in the health industry. Six digital health start-ups from five countries were recently chosen as the program's initial cohort. All of the start-ups are focused on artificial intelligence (AI), primarily on using AI to complement medical imaging. They expect that by altering the way healthcare is delivered, they will be able to spend more direct time on patient care and, as a result, prevent burnout.

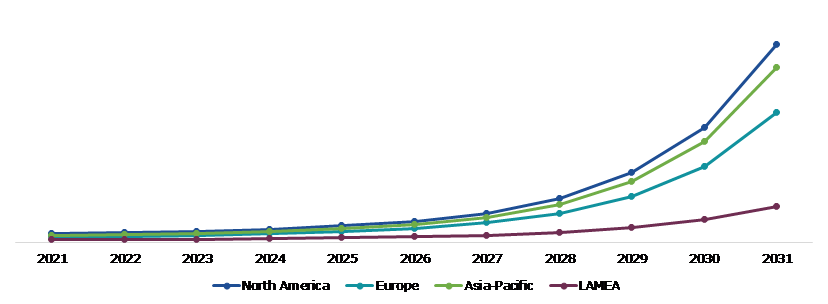

Global AI Accelerator Chip Market, Regional Insights

The AI accelerator chip market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global AI Accelerator Chip Market Size & Forecast, by Region, 2021-2031 (USD Million)

Source: Research Dive Analysis

The Market for AI Accelerator Chip in North America to be the Most Dominant

The North America AI accelerator chips market is anticipated to generate highest market share in 2021. North America is anticipated to dominate the global artificial intelligence (AI) accelerator market during the forecast period due to the region's high number of artificial intelligence (AI) accelerator producers. Furthermore, several well-established North American firms are working on the development of new technologies in artificial intelligence (AI) accelerators, which are projected to drive the region's market throughout the forecast period. As the North American region moves toward economic recovery and financial prosperity, artificial intelligence (AI) has the power to advance, improve, and find solutions for the lives of North Americans. The growth of the North American AI chipsets market is being driven by increased investments in the construction of regional data center infrastructure. The Intuit Prosperity Accelerator: AI is intended for high-potential seed-stage entrepreneurs situated in North America that have AI-driven solutions with market-ready products aimed at addressing financial concerns. Pre-seed and later-stage company applications will also be considered depending on their fit with the program's themes and focus areas. International startups are invited to apply, but they must demonstrate their worth to the North American market.

Competitive Scenario in the Global AI Accelerator Chip Market

Investment and agreement are common strategies followed by major market players. In February 2022, IBM Corporation announced the launch of the IBM Sustainability Accelerator, a global pro bono social impact program that applies IBM technologies, such as artificial intelligence, and an ecosystem of experts to enhance and scale non-profit and government organization operations, focused on populations vulnerable to environmental threats, including climate change, extreme weather, and pollution.

Source: Research Dive Analysis

Some of the leading AI Accelerator Chip Market players are NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., International Business Machines Corporation, Micron Technology, Inc., Microsoft Corporation, Alphabet Inc. (Google Inc.), NXP Semiconductors N.V., Advanced Micro Devices, Inc. (AMD), and Graphcore Limited.

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Chip Type |

|

| Segmentation by Processing Type |

|

| Segmentation by Application |

|

| Segmentation by Industry Vertical |

|

| Key Companies Profiled |

|

Q1. What is the size of the global AI accelerator chip market?

A. The size of the global AI accelerator chip market was over $14,948.6 million in 2021 and is projected to reach $332,142.7 million by 2031.

Q2. Which are the major companies in the AI accelerator chip market?

A. NVIDIA Corporation, Intel Corporation, and Qualcomm Technologies, Inc. are some of the key players in the global AI accelerator chip market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The North America region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the North America AI accelerator chip market?

A. North America AI accelerator chip market is anticipated to grow at 4.9% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Micron Technology, Inc, Alphabet Inc. (Google Inc.), and Advanced Micro Devices, Inc. (AMD) are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global AI accelerator chip market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on AI accelerator chip market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.AI Accelerator Chip Market Analysis, by Chip Type

5.1.Overview

5.2.Graphics Processing Unit (GPU)

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region

5.2.3.Market share analysis, by country

5.3.Application-Specific Integrated Circuit (ASIC)

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region

5.3.3.Market share analysis, by country

5.4.Field Programmable Gate Arrays (FPGA)

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region

5.4.3.Market share analysis, by country

5.5.Central Processing Unit (CPU)

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region

5.5.3.Market share analysis, by country

5.6.Other

5.6.1.Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region

5.6.3.Market share analysis, by country

5.7.Research Dive Exclusive Insights

5.7.1.Market attractiveness

5.7.2.Competition heatmap

6.AI Accelerator Chip Market Analysis, by Processing Type

6.1.Edge

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region

6.1.3.Market share analysis, by country

6.2.Cloud

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region

6.2.3.Market share analysis, by country

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heat map

7.AI Accelerator Chip Market Analysis, by Application

7.1.Natural Language Processing (NLP)

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region

7.1.3.Market share analysis, by country

7.2.Computer Vision

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region

7.2.3.Market share analysis, by country

7.3.Robotics

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region

7.3.3.Market share analysis, by country

7.4.Network Security

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region

7.4.3.Market share analysis, by country

7.5.Research Dive Exclusive Insights

7.5.1.Market attractiveness

7.5.2.Competition heat map

8.AI Accelerator Chip Market Analysis, by Industry Vertical

8.1.Financial Services

8.1.1.Definition, key trends, growth factors, and opportunities

8.1.2.Market size analysis, by region

8.1.3.Market share analysis, by country

8.2.Automotive and Transportation

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region

8.2.3.Market share analysis, by country

8.3.Healthcare

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region

8.3.3.Market share analysis, by country

8.4.Retail

8.4.1.Definition, key trends, growth factors, and opportunities

8.4.2.Market size analysis, by region

8.4.3.Market share analysis, by country

8.5.Telecom

8.5.1.Definition, key trends, growth factors, and opportunities

8.5.2.Market size analysis, by region

8.5.3.Market share analysis, by country

8.6.Others

8.6.1.Definition, key trends, growth factors, and opportunities

8.6.2.Market size analysis, by region

8.6.3.Market share analysis, by country

8.7.Research Dive Exclusive Insights

8.7.1.Market attractiveness

8.7.2.Competition heat map

9.AI Accelerator Chip Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Chip Type

9.1.1.2.Market size analysis, by Processing Type

9.1.1.3.Market size analysis, by Application

9.1.1.4.Market size analysis, by Industry Vertical

9.1.2.Canada

9.1.2.1.Market size analysis, by Chip Type

9.1.2.2.Market size analysis, by Processing Type

9.1.2.3.Market size analysis, by Application

9.1.2.4.Market size analysis, by Industry Vertical

9.1.3.Mexico

9.1.3.1.Market size analysis, by Chip Type

9.1.3.2.Market size analysis, by Processing Type

9.1.3.3.Market size analysis, by Application

9.1.3.4.Market size analysis, by Industry Vertical

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Chip Type

9.2.1.2.Market size analysis, by Processing Type

9.2.1.3.Market size analysis, by Application

9.2.1.4.Market size analysis, by Industry Vertical

9.2.2.UK

9.2.2.1.Market size analysis, by Chip Type

9.2.2.2.Market size analysis, by Processing Type

9.2.2.3.Market size analysis, by Application

9.2.2.4.Market size analysis, by Industry Vertical

9.2.3.France

9.2.3.1.Market size analysis, by Chip Type

9.2.3.2.Market size analysis, by Processing Type

9.2.3.3.Market size analysis, by Application

9.2.3.4.Market size analysis, by Industry Vertical

9.2.4.Spain

9.2.4.1.Market size analysis, by Chip Type

9.2.4.2.Market size analysis, by Processing Type

9.2.4.3.Market size analysis, by Application

9.2.4.4.Market size analysis, by Industry Vertical

9.2.5.Italy

9.2.5.1.Market size analysis, by Chip Type

9.2.5.2.Market size analysis, by Processing Type

9.2.5.3.Market size analysis, by Application

9.2.5.4.Market size analysis, by Industry Vertical

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Chip Type

9.2.6.2.Market size analysis, by Processing Type

9.2.6.3.Market size analysis, by Application

9.2.6.4.Market size analysis, by Industry Vertical

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia-Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Chip Type

9.3.1.2.Market size analysis, by Processing Type

9.3.1.3.Market size analysis, by Application

9.3.1.4.Market size analysis, by Industry Vertical

9.3.2.Japan

9.3.2.1.Market size analysis, by Chip Type

9.3.2.2.Market size analysis, by Processing Type

9.3.2.3.Market size analysis, by Application

9.3.2.4.Market size analysis, by Industry Vertical

9.3.3.India

9.3.3.1.Market size analysis, by Chip Type

9.3.3.2.Market size analysis, by Processing Type

9.3.3.3.Market size analysis, by Application

9.3.3.4.Market size analysis, by Industry Vertical

9.3.4.Australia

9.3.4.1.Market size analysis, by Chip Type

9.3.4.2.Market size analysis, by Processing Type

9.3.4.3.Market size analysis, by Application

9.3.4.4.Market size analysis, by Industry Vertical

9.3.5.South Korea

9.3.5.1.Market size analysis, by Chip Type

9.3.5.2.Market size analysis, by Processing Type

9.3.5.3.Market size analysis, by Application

9.3.5.4.Market size analysis, by Industry Vertical

9.3.6.Rest of Asia-Pacific

9.3.6.1.Market size analysis, by Chip Type

9.3.6.2.Market size analysis, by Processing Type

9.3.6.3.Market size analysis, by Application

9.3.6.4.Market size analysis, by Industry Vertical

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Chip Type

9.4.1.2.Market size analysis, by Processing Type

9.4.1.3.Market size analysis, by Application

9.4.1.4.Market size analysis, by Industry Vertical

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Chip Type

9.4.2.2.Market size analysis, by Processing Type

9.4.2.3.Market size analysis, by Application

9.4.2.4.Market size analysis, by Industry Vertical

9.4.3.UAE

9.4.3.1.Market size analysis, by Chip Type

9.4.3.2.Market size analysis, by Processing Type

9.4.3.3.Market size analysis, by Application

9.4.3.4.Market size analysis, by Industry Vertical

9.4.4.South Africa

9.4.4.1.Market size analysis, by Chip Type

9.4.4.2.Market size analysis, by Processing Type

9.4.4.3.Market size analysis, by Application

9.4.4.4.Market size analysis, by Industry Vertical

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Chip Type

9.4.5.2.Market size analysis, by Processing Type

9.4.5.3.Market size analysis, by Application

9.4.5.4.Market size analysis, by Industry Vertical

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.NVIDIA Corporation

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.Intel Corporation

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.Qualcomm Technologies, Inc.

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.International Business Machines Corporation

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.Micron Technology, Inc.

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.Microsoft Corporation

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.Alphabet Inc. (Google Inc.)

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.NXP Semiconductors N.V.

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.Advanced Micro Devices, Inc. (AMD)

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Graphcore Limited

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

12.Appendix

12.1.Parent & peer market analysis

12.2.Premium insights from industry experts

12.3.Related reports

AI accelerator chips, also known as AI hardware, are high-performance, widely parallel deep learning neural network computational chips that are specially designed for carrying artificial neural network (ANN) based applications. The hardware components of AI accelerator chips include three main parts: computing, storage, and networking, which are used for optimizing the power and performance of a chip with no human intervention. AI accelerator chips are used for a wide range of applications, such as the internet of things, algorithms for robotics, and various other data-intensive or sensor-driven tasks.

Forecast Analysis of the Global AI Accelerator Chip Market

The increasing use of AI accelerator chips with artificial neural networks (ANN) in the healthcare industry to improve the medical data mining quality and the physician decision-making process is predicted to bolster the growth of the AI accelerator chip market throughout the analysis timeframe. Moreover, the growing use of AI accelerator chips to provide industry-specific end-to-end solutions, innovation, and the creation of new software ecosystems is expected to create incredible growth opportunities for the market during the estimated timeframe. However, the lack of a skilled AI accelerator chip workforce may hamper the growth of the market over the analysis period.

According to a report published by Research Dive, the global AI accelerator chip market is anticipated to garner a revenue of $332,142.7 million and grow at a healthy CAGR of 39.3% over the estimated period from 2022 to 2031. The major players of the market include Graphcore Limited, NVIDIA Corporation, Advanced Micro Devices, Inc. (AMD), Intel Corporation, NXP Semiconductors N.V., Qualcomm Technologies, Inc., Alphabet Inc. (Google Inc.), International Business Machines Corporation, Microsoft Corporation, Micron Technology, Inc., and many more.

AI Accelerator Chip Market Trends and Developments

The key companies operating in the industry are adopting various growth strategies & business tactics, such as partnerships, collaborations, mergers & acquisitions, and product launches to maintain a robust position in the overall market, which is subsequently helping the global AI accelerator chip market to grow exponentially. For instance:

- In January 2021, Qualcomm Technologies, Inc., a designer, and manufacturer of advanced semiconductors for mobile phones and commercial wireless systems announced its acquisition of NUVIA, a leading developer of semiconductor components and high-performance processors designed for compute-intensive devices and applications. With this acquisition, the companies aimed to develop high-performance processors for powering flagship smartphones, next-generation laptops, Advanced Driver Assistance Systems (ADAS), digital cockpits, and various advanced networking solutions.

- In August 2021, IBM, an American multinational technology corporation launched its new processor, namely, “IBM Telum Processor”, which is specifically designed to address fraud in real-time with the integration of deep learning. This is the first processor from IBM that contains an AI accelerator chip. “Telum” is designed to help customers worldwide to achieve business insights at a larger scale across banking, trading, insurance applications, and customer interactions.

- In October 2022, Oracle Corp, a leading cloud technology company announced its partnership with Nvidia Corp, an American multinational technology company. With this partnership, Oracle aimed to boost AI-related computational work in its cloud platform by adding thousands of Nvidia's AI accelerator chips as AI is rising across many organizations.

Most Profitable Region

The North America region of the AI accelerator chip market is predicted to hold the largest share of the market due to the strong existence of AI accelerator chip producers in this region. Additionally, the leading players of this region are continuously working on the development of new technologies in AI accelerators which is predicted to increase the regional growth of the market throughout the estimated period.

Covid-19 Impact on the AI Accelerator Chip Market

The outbreak of the Covid-19 pandemic has had a negative impact on the AI accelerator chip market, likewise, on several other industries. This is mainly due to the decreasing supply of cable and the reduced production of semiconductors during the pandemic. Moreover, the Covid-19 norms and regulations have limited the number of employees in the manufacturing unit which has further impacted the supply chain of chipsets across various countries. All these factors have declined the market growth over the pandemic period.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com