Steam Boiler Market Report

RA08529

Steam Boiler Market by Type (Water-tube and Fire-tube), Fuel Type (Coal-fired, Oil-fired, Gas-fired, and Others), End-user (Chemicals, Power Generation, Oil & Gas, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2021–2028

Global Steam Boiler Market Analysis

The global steam boiler market size is predicted to garner $21,931.1 million in the 2021–2028 timeframe, growing from $14,774.8 million in 2020, at a healthy CAGR of 5.2%.

Market Synopsis

The growing electricity demand has fueled investment in the power generation industry. This trend has increased the demand for steam boilers, worldwide. Additionally, increasing power plant capacity addition is driving the demand for steam boilers in the global market.

However, the high installation cost is expected to restrict the market growth over the forecast period.

According to the regional analysis, the Asia-Pacific steam boiler market is anticipated to grow during the review period and generate a revenue of $8,553.1 million in 2028, with a CAGR of 5.7%, due to increasing power plant capacity addition in the region.

Steam Boiler Overview

The steam boiler is a closed container in which water is boiled to form steam. The industrial steam boiler is a system that has parallel tubes through which water passes, suspended above a furnace. Water is heated in a closed container by burning fossil fuel, coal, gas, or electricity to generate steam. These steam boilers are used for producing high-pressure steam to run steam turbines used in power generation.

Impact Analysis of COVID-19 on the Global Steam Boiler Market

The novel coronavirus pandemic has affected several industries across the globe, and the steam boiler industry is among the hardest hit. Due to complete lockdowns and fear of spreading coronavirus, many companies were working with limited workforce, affecting the growth of the steam boiler manufacturing industry. Furthermore, steam boiler manufacturers had limited orders, severely affecting the growth of the steam boiler industry.

Before the pandemic, the global market for steam boilers was expected to exceed USD 19 billion by 2025. These numbers reflect the growing demand for steam boilers in chemical, power generation, oil & gas, and sugar mills, among others, with power plants being one of the biggest end-users.

Despite this strong outlook, the pandemic has significantly impacted the growth of the steam and boiler industry. With social distancing and lockdowns in place, worldwide, many steam boiler maintenance companies have been unable to provide services such as routine inspections and maintenance.

Surging Demand for Electricity is Anticipated to Fuel the Market Growth

The global electricity demand is growing at 2.1% per year. The growing electricity demand is attributed to rapid urbanization and industrialization, especially in developing countries. Moreover, the increasing penetration of IoT and the Internet has led to an increase in demand for connected appliances and devices.

The industry 4.0 revolution has led to an increase in the adoption of cyber security, additive manufacturing, autonomous robot, system integration, and simulation, among others. These trends have driven strong electricity demand. According to the International Energy Agency (IEA), electricity’s share in total final energy consumption was 19% in 2018 and is expected to reach 24% by 2040.

To meet the growing electricity demand, countries such as China and India have increased investment in Brownfield and Greenfield expansion of power plants. As per the Carbon Brief Ltd, since 2000, the world has doubled the coal-fired power capacity to 2,045 gigawatts (GW) after explosive growth in China and India.

To know more about global steam boiler market drivers, get in touch with our analysts here.

High Cost of Installation to Restrain the Market Growth

The cost of a steam boiler varies based on the design and working mechanism, among other aspects. The large capacity high-end industrial steam boiler costs around $255 to $345 per horsepower. Furthermore, budget steam boilers have a shorter life span, shorter warranties, and lower customer service support compared to high-end steam boilers. Installation of steam boiler is a critical process and requires high capital investment. As per the analysis, the companies pay around $8000 - 9000 or 10% to 15% of the actual steam boiler cost for installing a high-end steam boiler. These factors are expected to restrain the market growth.

The Growing Chemical, Pulp & Paper, and Pharmaceutical Industries to Create Massive Investment Opportunities

The growing chemical, pulp & paper, and pharmaceutical industries are projected to provide growth opportunities for the steam boiler market over the forecast period. For an instant, India's pharmaceutical industry is among the leading producers of generic medicine and vaccines. This industry supplies 20% of generic drugs and 62% of vaccines to the global market.

According to an Economic survey, the Indian pharmaceutical market is projected to grow three times in the next decade. In 2021, India's pharmaceutical is valued at $41 billion and is expected to reach $65 billion by 2024 and $120-130 billion by 2030. Additionally, a growing number of the biopharmaceutical industry in Asia-Pacific and Europe is further expected to provide growth opportunities for the steam boiler market.

To know more about global steam boiler market opportunities, get in touch with our analysts here.

Based on type, the market has been divided into Water-tube steam boiler and fire-tube steam boiler of which Water-tube sub-segment is projected to generate the maximum revenue during the forecast period. Download PDF Sample ReportSteam Boiler Market

By Type

Source: Research Dive Analysis

The water- tube segment is predicted to have a dominating market share in the global market. The sub-segment is expected to register a revenue of $18,548.1 million during the forecast period. Water-tube boilers provide higher efficiency, owing to which they are used in power generation. Growing demand for electricity has resulted in increasing capacity expansion of power plants. To meet the growing demand for electricity, countries are investing in the power generation sector, driving the demand for water-tube steam boilers over the forecast period.

Steam Boiler Market

By Fuel TypeOn the basis of fuel type, the market has been sub-segmented into coal-fired, oil-fired, gas-fried, and others. Among the mentioned sub-segments, the gas-fried sub-segment is predicted to show the fastest growth during the forecast.

Source: Research Dive Analysis

The gas-fired sub-segment of the global steam boiler market is projected to have the fastest growth. It is also projected to surpass $3,737.0 million by 2028, with an increase from $2,179.2 million in 2020. Gas-fired steam boilers have higher efficiency. In addition, gas steam boiler possesses advantages such as faster steam production, less greenhouse gas emissions, better operational performance, high efficiency, and others. This resulted in fueling the demand for gas-fired steam boilers during the forecast period.

Steam Boiler Market

By End UserOn the basis of end-user, the market has been sub-segmented into Chemicals, power generation, oil & gas, and others. Among the mentioned sub-segments, the Chemicals sub-segment is predicted to show the fastest growth over the forecast period.

Source: Research Dive Analysis

The chemicals sub-segment of the global steam boiler market is projected to have the fastest growth from 2021 to 2028 timeframe. It is also projected to surpass $9,081.5 million by 2028, with an increase from $5,903.5 million in 2020. The boilers are used for generating a large quantity of high-quality, high-temperature steam for production. The growing number of chemical companies in the Asia-Pacific region is expected to fuel the demand for steam boilers during the forecast period.

Steam Boiler Market

By RegionThe steam boiler market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The Market for Steam Boiler in Asia-Pacific to be the Most Dominant

Asia-Pacific was the highest revenue contributor, accounting for $5,555.3 million in 2020, and is estimated to reach $8,553.1 million by 2028, with a CAGR of 5.7%. Asia-pacific has the highest number of steam boilers in the world. China dominates the Asia-Pacific steam boiler market with a 34.4% market share in 2020. Growing demand for electricity along with the number of chemical companies are expected to drive the steam boiler market during the forecast period.

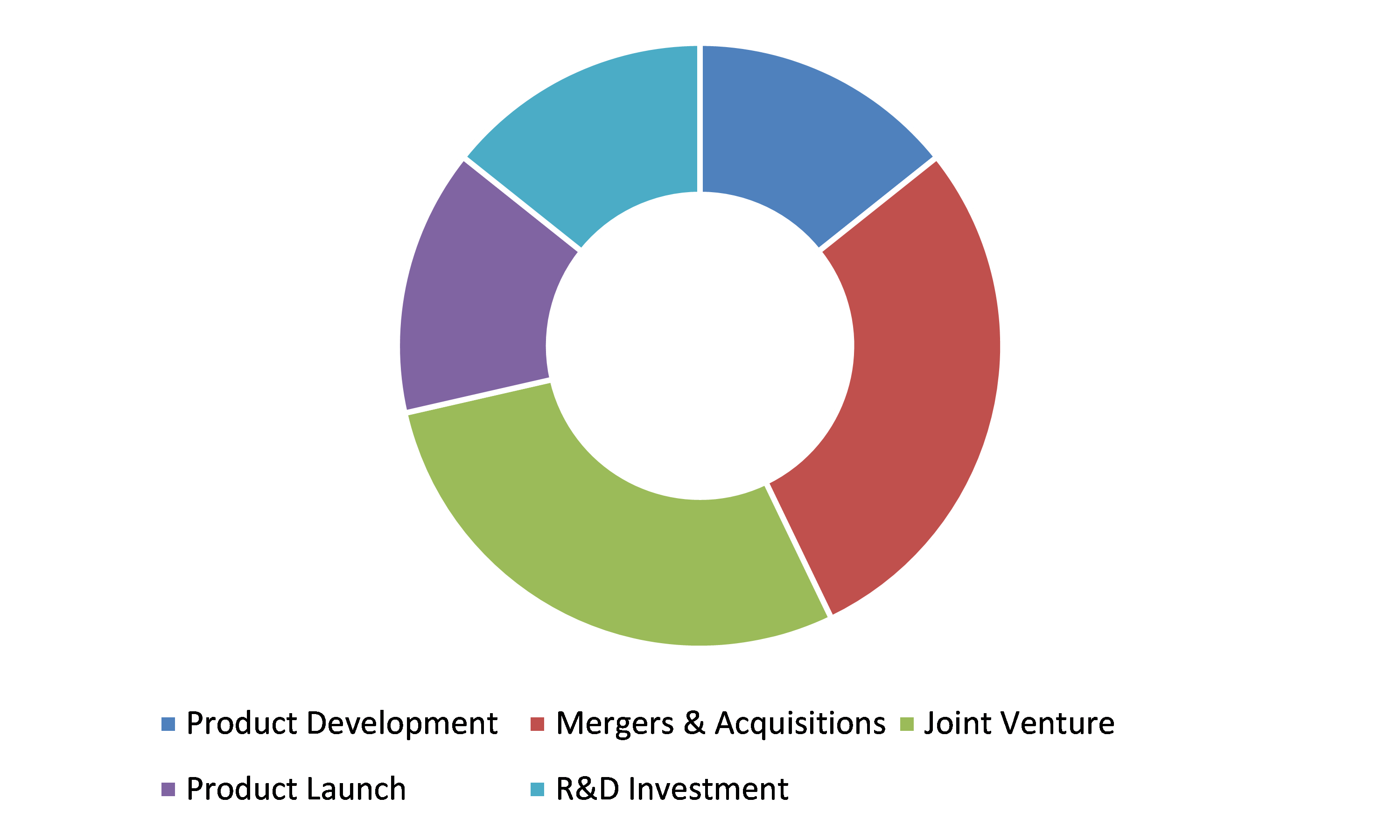

Competitive Scenario in the Global Steam Boiler Market

Product launches and mergers & acquisitions are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading steam boiler market players are Alfa Laval, Babcock & Wilcox Enterprises, Inc., Viessmann Limited, Forbes Marshall, Thermax Limited, IHI Corporation, Mitsubishi Heavy Industries, Ltd, The Fulton Companies, Larsen & Toubro Limited, and Hurst Boiler & Welding Co, Inc.

Porter’s Five Forces Analysis for the Global Steam Boiler Market:

- Bargaining Power of Suppliers: Suppliers in this industry include companies that manufacture parts and accessories for boiler and heat exchanger equipment such as valves, control instrumentation, steam traps, pipes & tubes, fans, actuators, and pressure relief valves. The supplier industry is highly competitive owing to the presence of many suppliers of raw materials.

Thus, the bargaining power of suppliers is low. - Bargaining Power of Buyers: The global steam boiler market is the highly competitive due to presence of many manufacturers. Furthermore, the buyer can switch from one manufacturing to another due to the low switching cost.

Thus, the bargaining power of the buyers is high. - Threat of New Entrants: The initial investment is high, thereby creating a unique entry barrier for the steam boiler. In addition, the switching cost for customers is usually nil.

Thus, the threat of the new entrants is low. - Threat of Substitutes: Food processors are shifting towards thermal fluid or hot oil heaters with unfired steam generators. The elimination of water treatment and the reduction of maintenance functions are two reasons for replacing a steam boiler with a thermal fluid system.

Thus, the threat of substitutes is high. - Competitive Rivalry in the Market: The competitive rivalry among industry players is rather intense, especially between the mid-price steam boiler. These manufacturers provide value-added services to strengthen the footprint worldwide.

Therefore, competitive rivalry in the market is high.

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2020 |

| Forecast Timeline for Market Projection | 2021-2028 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Fuel Type |

|

| Segmentation by End-user |

|

| Key Companies Profiled |

|

Q1. What is the size of the global steam boiler market?

A. The global steam boiler market was valued at $14,774.8 million in 2020, and is projected to reach $21,931.1 million by 2028, registering a CAGR of 5.2%.

Q2. What is the purpose of a steam boiler?

A. The steam boilers are designed to provide superheated steam required for industrial operations.

Q3. Which are the major companies in the steam boiler market?

A. Alfa Laval, Babcock & Wilcox Enterprises, Inc., Viessmann Limited, Thermax Limited, and Hurst Boiler & Welding Co, Inc. are some of the key players in the global steam boiler market.

Q4. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific possesses great investment opportunities for investors to witness the most promising growth in the future.

Q5. What are the strategies opted by the leading players in this market?

A. Product innovation and partnership are the two key strategies opted by the operating companies in this market.

CHAPTER 1:RESEARCH METHODOLOGY

1.1.Desk research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1. Assumptions

1.4.2. Forecast parameters

CHAPTER 2:EXECUTIVE SUMMARY

2.1.360° summary

2.2.Type

2.3.Fuel Type

2.4.End-Users

CHAPTER 3:MARKET OVERVIEW

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.2.2.1 Top winning strategies, by year, 2020-2028*

3.2.2.2 Top winning strategies, by development, 2020-2028*(%)

3.2.2.3 Top winning strategies, by company, 2020-2028*

3.3.Porters five forces analysis

3.4.Market dynamics

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Market value chain analysis

3.9.Strategic overview

3.10.Impact of key regulations

CHAPTER 4:IMPACT OF COVID-19 ON STEAM BOILER MARKET

4.1.Introduction

4.2.COVID-19 health assessment

4.3.Impact of COVID-19 on global economy

4.4.Impact of COVID-19 on STEAM BOILER market

4.4.1. Social impact

4.4.2. Technological impact

4.4.3. Investment scenario

4.5.Steam boiler market size and forecast, by region, 2020-2028

CHAPTER 5:STEAM BOILER MARKET BY TYPE

5.1.OVERVIEW

5.1.1. Market size and forecast, by Type

5.2. WATER TUBE

5.2.1. Key market trends, growth factors and opportunities

5.2.2. Market size and forecast, by region

5.2.3. Market share analysis, by country

5.3. FIRE TUBE

5.3.1. Key market trends, growth factors and opportunities

5.3.2. Market size and forecast, by region

5.3.3. Market share analysis, by country

CHAPTER 6:STEAM BOILER MARKET BY FUEL TYPE

6.1.OVERVIEW

6.1.1. Market size and forecast, by Fuel Type

6.2. COAL FIRED

6.2.1. Key market trends, growth factors and opportunities

6.2.2. Market size and forecast, by region

6.2.3. Market share analysis, by country

6.3. OIL FIRED

6.3.1. Key market trends, growth factors and opportunities

6.3.2. Market size and forecast, by region

6.3.3. Market share analysis, by country

6.4. GAS FIRED

6.4.1. Key market trends, growth factors and opportunities

6.4.2. Market size and forecast, by region

6.4.3. Market share analysis, by country

6.5. OTHERS

6.5.1. Key market trends, growth factors and opportunities

6.5.2. Market size and forecast, by region

6.5.3. Market share analysis, by country

CHAPTER 7:STEAM BOILER MARKET BY END-USERS

7.1.OVERVIEW

7.1.1. Market size and forecast, by end-users

7.2. CHEMICALS

7.2.1. Key market trends, growth factors and opportunities

7.2.2. Market size and forecast, by region

7.2.3. Market share analysis, by country

7.3. POWER GENERATION

7.3.1. Key market trends, growth factors and opportunities

7.3.2. Market size and forecast, by region

7.3.3. Market share analysis, by country

7.4. OIL & GAS

7.4.1. Key market trends, growth factors and opportunities

7.4.2. Market size and forecast, by region

7.4.3. Market share analysis, by country

7.5 OTHERS

7.5.1. Key market trends, growth factors and opportunities

7.5.2. Market size and forecast, by region

7.5.3. Market share analysis, by country

CHAPTER 8:STEAM BOILER MARKET BY REGION

8.1.OVERVIEW

8.1.1. Market size and forecast, by region

8.2.NORTH AMERICA

8.2.1. Key market trends and opportunities

8.2.2. Market size and forecast, by Type

8.2.3. Market size and forecast, by Fuel Type

8.2.4. Market size and forecast, by end-users

8.2.5. Market size and forecast, by Country

8.2.6. U.S.

8.2.6.1. Key market trends and opportunities

8.2.6.2. Market size and forecast, by Type

8.2.6.3. Market size and forecast, by Fuel Type

8.2.6.4. Market size and forecast, by end-users

8.2.7.Canada

8.2.7.1. Key market trends and opportunities

8.2.7.2. Market size and forecast, by Type

8.2.7.3. Market size and forecast, by Fuel Type

8.2.7.4. Market size and forecast, by end-users

8.2.8.Mexico

8.2.8.1. Key market trends and opportunities

8.2.8.2. Market size and forecast, by Type

8.2.8.3. Market size and forecast, by Fuel Type

8.2.8.4. Market size and forecast, by end-users

8.3.EUROPE

8.3.1. Key market trends and opportunities

8.3.2. Market size and forecast, by Type

8.3.3. Market size and forecast, by Fuel Type

8.3.4. Market size and forecast, by end-users

8.3.5. Market size and forecast, by Country

8.3.6. Germany

8.3.6.1. Key market trends and opportunities

8.3.6.2. Market size and forecast, by Type

8.3.6.3. Market size and forecast, by Fuel Type

8.3.6.4. Market size and forecast, by end-users

8.3.7.UK

8.3.7.1. Key market trends and opportunities

8.3.7.2. Market size and forecast, by Type

8.3.7.3. Market size and forecast, by Fuel Type

8.3.7.4. Market size and forecast, by end-users

8.3.8.France

8.3.8.1. Key market trends and opportunities

8.3.8.2. Market size and forecast, by Type

8.3.8.3. Market size and forecast, by Fuel Type

8.3.8.4. Market size and forecast, by end-users

8.3.9.Spain

8.3.9.1. Key market trends and opportunities

8.3.9.2. Market size and forecast, by Type

8.3.9.3. Market size and forecast, by Fuel Type

8.3.9.4. Market size and forecast, by end-users

8.3.10.Italy

8.3.10.1. Key market trends and opportunities

8.3.10.2. Market size and forecast, by Type

8.3.10.3. Market size and forecast, by Fuel Type

8.3.10.4. Market size and forecast, by end-users

8.3.11.Rest of Europe

8.3.11.1. Key market trends and opportunities

8.3.11.2. Market size and forecast, by Type

8.3.11.3. Market size and forecast, by Fuel Type

8.3.11.4. Market size and forecast, by end-users

8.4.ASIA-PACIFIC

8.4.1. Key market trends and opportunities

8.4.2. Market size and forecast, by Type

8.4.3. Market size and forecast, by Fuel Type

8.4.4. Market size and forecast, by end-users

8.4.5. Market size and forecast, by Country

8.4.6. China

8.4.6.1. Key market trends and opportunities

8.4.6.2. Market size and forecast, by Type

8.4.6.3. Market size and forecast, by Fuel Type

8.4.6.4. Market size and forecast, by end-users

8.4.7.Japan

8.4.7.1. Key market trends and opportunities

8.4.7.2. Market size and forecast, by Type

8.4.7.3. Market size and forecast, by Fuel Type

8.4.7.4. Market size and forecast, by end-users

8.4.8.India

8.4.8.1. Key market trends and opportunities

8.4.8.2. Market size and forecast, by Type

8.4.8.3. Market size and forecast, by Fuel Type

8.4.8.4. Market size and forecast, by end-users

8.4.9.South Korea

8.4.9.1. Key market trends and opportunities

8.4.9.2. Market size and forecast, by Type

8.4.9.3. Market size and forecast, by Fuel Type

8.4.9.4. Market size and forecast, by end-users

8.4.10.Australia

8.4.10.1. Key market trends and opportunities

8.4.10.2. Market size and forecast, by Type

8.4.10.3. Market size and forecast, by Fuel Type

8.4.10.4. Market size and forecast, by end-users

8.4.11.Rest of Asia-Pacific

8.4.11.1. Key market trends and opportunities

8.4.11.2. Market size and forecast, by Type

8.4.11.3. Market size and forecast, by Fuel Type

8.4.11.4. Market size and forecast, by end-users

8.5.LAMEA

8.5.1. Key market trends and opportunities

8.5.2. Market size and forecast, by Type

8.5.3. Market size and forecast, by Fuel Type

8.5.4. Market size and forecast, by end-users

8.5.5. Market size and forecast, by Country

8.5.6. Latin America

8.5.6.1. Key market trends and opportunities

8.5.6.2. Market size and forecast, by Type

8.5.6.3. Market size and forecast, by Fuel Type

8.5.6.4. Market size and forecast, by end-users

8.5.7.Middle East

8.5.7.1. Key market trends and opportunities

8.5.7.2. Market size and forecast, by Type

8.5.7.3. Market size and forecast, by Fuel Type

8.5.7.4. Market size and forecast, by end-users

8.5.8.Africa

8.5.8.1. Key market trends and opportunities

8.5.8.2. Market size and forecast, by Type

8.5.8.3. Market size and forecast, by Fuel Type

8.5.8.4. Market size and forecast, by end-users

CHAPTER 9:COMPANY PROFILES

9.1. ALFA LAVAL

9.1.1.Company overview

9.1.2.Key executives

9.1.3.Company snapshot

9.1.4.Operating business segments

9.1.5.Type portfolio

9.1.6.R&D expenditure

9.1.7.Business performance

9.1.8.Key strategic moves and developments

9.2. BABCOCK & WILCOX ENTERPRISES, INC.

9.2.1.Company overview

9.2.2.Key executives

9.2.3.Company snapshot

9.2.4.Operating business segments

9.2.5.Type portfolio

9.2.6.R&D expenditure

9.2.7.Business performance

9.2.8.Key strategic moves and developments

9.3. VIESSMANN LIMITED

9.3.1.Company overview

9.3.2.Key executives

9.3.3.Company snapshot

9.3.4.Operating business segments

9.3.5.Type portfolio

9.3.6.R&D expenditure

9.3.7.Business performance

9.3.8.Key strategic moves and developments

9.4. FORBES MARSHALL

9.4.1.Company overview

9.4.2.Key executives

9.4.3.Company snapshot

9.4.4.Operating business segments

9.4.5.Type portfolio

9.4.6.R&D expenditure

9.4.7.Business performance

9.4.8.Key strategic moves and developments

9.5. THERMAX LIMITED

9.5.1.Company overview

9.5.2.Key executives

9.5.3.Company snapshot

9.5.4.Operating business segments

9.5.5.Type portfolio

9.5.6.R&D expenditure

9.5.7.Business performance

9.5.8.Key strategic moves and developments

9.6. IHI CORPORATION

9.6.1.Company overview

9.6.2.Key executives

9.6.3.Company snapshot

9.6.4.Operating business segments

9.6.5.Type portfolio

9.6.6.R&D expenditure

9.6.7.Business performance

9.6.8.Key strategic moves and developments

9.7. MITSUBISHI HEAVY INDUSTRIES, LTD

9.7.1.Company overview

9.7.2.Key executives

9.7.3.Company snapshot

9.7.4.Operating business segments

9.7.5.Type portfolio

9.7.6.R&D expenditure

9.7.7.Business performance

9.7.8.Key strategic moves and developments

9.8. THE FULTON COMPANIES

9.8.1.Company overview

9.8.2.Key executives

9.8.3.Company snapshot

9.8.4.Operating business segments

9.8.5.Type portfolio

9.8.6.R&D expenditure

9.8.7.Business performance

9.8.8.Key strategic moves and developments

9.9. LARSEN & TOUBRO LIMITED

9.9.1.Company overview

9.9.2.Key executives

9.9.3.Company snapshot

9.9.4.Operating business segments

9.9.5.Type portfolio

9.9.6.R&D expenditure

9.9.7.Business performance

9.9.8.Key strategic moves and developments

9.10. HURST BOILER & WELDING CO, INC.

9.10.1.Company overview

9.10.2.Key executives

9.10.3.Company snapshot

9.10.4.Operating business segments

9.10.5.Type portfolio

9.10.6.R&D expenditure

9.10.7.Business performance

9.10.8.Key strategic moves and developments

Steam Boiler is a container in which water is heated by burning coal, gas, fossil fuel or electricity to produce steam. An industrial steam boiler is a system that consists of parallel tubes through water passes, and it is often suspended above a furnace. Steam boilers are extensively used to produce high-pressure, high-quality steam in order to run steam turbines which is then used for power generation.

Forecast Analysis of the Global Steam Boiler Market

Rising demand for electricity due to significant surge in industrialization across the globe is expected to drive the growth of the market. In addition, growing internet penetration and increasing prevalence of IOT is further expected to bolster the growth of the global steam boiler market during the forecast period. Furthermore, increasing application of steam boilers in the booming pharmaceutical industries expected to create ample opportunities for the growth of the steam boiler market during the forecast period. However, high cost of steam boiler is expected to hinder the growth of the global steam boiler market during the forecast period.

According to the report published by Research Dive, the global steam boiler market is expected to generate a revenue of $21,931.1 million by 2028, growing rapidly at a CAGR of 5.2% during the forecast period 2021-2028. The major players of the market include The Fulton Companies, Larsen & Toubro Limited, and Hurst Boiler & Welding Co, Inc., Alfa Laval, Babcock & Wilcox Enterprises, Inc., Viessmann Limited, Forbes Marshall, Thermax Limited, IHI Corporation, Mitsubishi Heavy Industries, Ltd, and many more.

Key Developments

The key companies operating in the industry are adopting various growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, which is subsequently helping the global steam boiler market to grow exponentially.

For instance, in August 2021, Babcock Wanson, an international provider of industrial boilers industrial, process heating equipment, servicing and training, acquired Steam Plant Engineering (SPE), an innovative provider of industrial boiler services, in order to strengthen Babcock Wanson’s position in the UK steam boiler business.

In January 2002, ZOZEN, an experienced industrial boiler manufacturer with more than 30 years of history, collaborated with Libbey Inc., the global glassware industry giant, in order to produce low NOx gas-fired boilers so as to reduce the greenhouse emissions and improve the atmospheric environment.

In August 2020, Miura Co. Ltd., a prestigious company that manufactures, inspects, and maintains industrial boilers and related equipment, expanded their manufacturing of efficient, safe, and sustainable industrial steam boilers to the Chinese market, in order to strengthen their growth potential.

Most Profitable Region

The Asia Pacific region is expected to be most lucrative, and generate a revenue of $8,553.1 million during the forecast period. Rising demand for electricity due to rapid urbanization in this region is expected to stimulate the growth of the market during the forecast period. In addition, immense presence of prominent players of the market in this region is further expected to bolster the growth of the regional steam boiler market during the forecast period.

COVID-19 Impact on the Market

The outbreak of COVID-19 has had a negative impact on the growth of the global steam boiler market, owing to the presence of lockdowns in numerous countries across the globe. Stringent restrictions imposed by the government on social distancing during lockdowns led companies to work with limited workforce which affected productivity. Moreover, steam boiler manufacturers received fewer orders during the pandemic due to the shut down of various end-use industries across the globe which led to their decreased demand.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com