Airborne Sensors Market Report

RA08351

Airborne Sensors Market by Type (Non-scanning and Scanning), Application (Defense Aircraft, Commercial Aircraft, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2030

Global Airborne Sensors Market Analysis

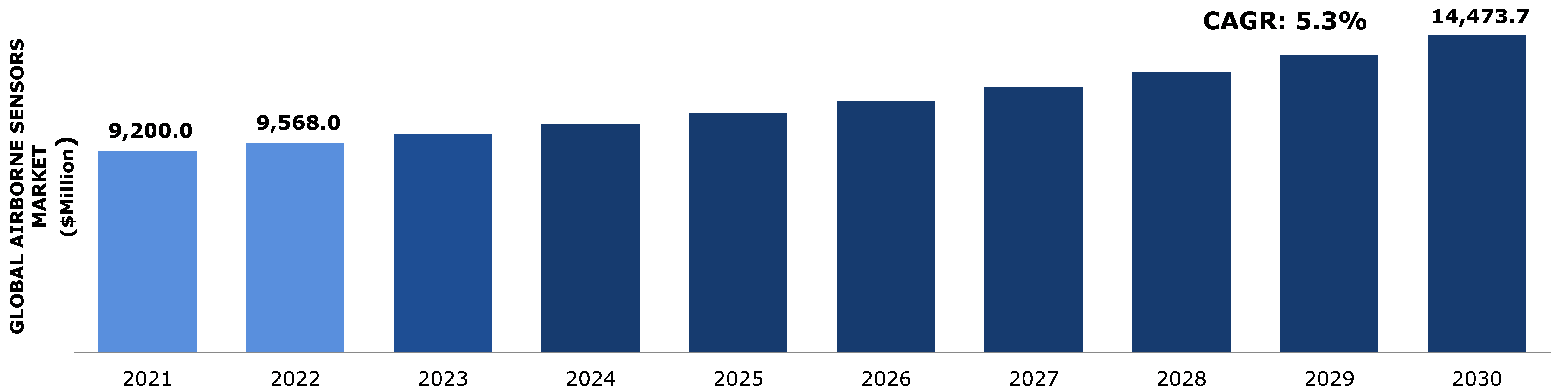

The global airborne sensors market size is predicted to garner a revenue of $14,473.7 million in the 2022–2030 timeframe, growing from $9,200.0 million in 2021, at a healthy CAGR of 5.3%.

Market Synopsis

The airborne sensors industry will experience rapid growth, owing primarily to the increased use of airborne sensors in the defense sector. Airborne sensors can help military missions with surveillance, intelligence, and reconnaissance collection. Furthermore, the rise in terrorist attacks in various countries is expected to drive the market for airborne sensors. According to the Stockholm International Peace Research Institute (SIPRI), the United States increased defense investment by approximately 6.6% in 2019 compared to 2018, and China increased investment by approximately 6.6% in 2019. These factors will increase demand for innovative solutions for the military and defense sectors, potentially driving the global airborne sensors market during the forecast period.

A notable key factor that can restrain the market of airborne sensors globally is the high cost investment in infrastructure and research & development because there are some technical standards and certification by aviation safety agencies for manufacturing of airborne sensors. Such factors are expected to create a negative impact on the airborne sensors market during the forecast period.

According to the regional outlook, the Asia-Pacific airborne sensors market is expected to create massive growth opportunities for market investors by growing at a CAGR of 5.9% during the review period.

Airborne Sensors Overview

Airborne sensors are mounted on aircraft to capture images of the earth's surface. These sensors are extremely useful in a wide range of applications, including defense, agriculture, forestry, the environment, mining, mapping & surveying, infrastructure & urbanization, and much more. Furthermore, airborne sensors can provide images with a spatial resolution of 20 cm or less. Airplanes, UAS (Unmanned Aerial System), helicopters, high-altitude aircraft, and free-floating balloons are examples of airborne platforms. These platforms can range from slow-moving aircraft to low-flying aircraft that hover at less than 30,000 feet. Slow-moving aircrafts with light twin or single engines are useful for capturing large-scale images of the surface. Fast-moving aircrafts also include jets or twin-engine turboprops, which are used to capture images over a large area. Some fascinating facts about airborne platforms include the fact that they provide 50 km of remote sensing data, which is used to obtain pinpoint locations and atmospheric data. Furthermore, reports on infrastructure maintenance, agriculture, mapping, emergency response, and environmental monitoring are included in the remote sensing data.

COVID-19 Impact on Airborne Sensors Market

The global airborne sensors market is expected to grow slowly in comparison to previous years during the COVID-19 pandemic, owing to disruptions in supply chains and factory shutdowns. The government and businesses both launched initiatives to combat or mitigate the economic impact of the pandemic. For example, the United States military announced in November 2020 that it is developing airborne sensors capable of detecting pathogens and viruses such as COVID-19 in minutes or seconds. The project's name is SenSARS, and its main goal is to develop a sensor that can monitor the SARS-CoV-2 virus in the air for public health safety. All these factors are expected to accelerate the growth of the market in the forecast period and new developments in upcoming years.

There were several companies that were completely operational during the pandemic. For instance, in May 2020, Hexagon announced that they are completely operational during the coronavirus pandemic and their HxGN Content Program is helping the U.S. government & other NGOs for monitoring the COVID-19 outbreak by providing aerial images that can be used in geo-information, data products, create maps, and view the objects on street level. Thus, demand for airborne sensors is expected to rise in the upcoming years. These key factors may generate investment opportunities in the airborne sensors market.

Increasing Demand for Airborne Sensors in the Defense Sector has Fueled the Growth of the Market

The airborne sensors industry will expand rapidly, owing to increased use of airborne sensors in the defense sector. Airborne sensors can aid military missions by collecting surveillance, intelligence, and reconnaissance data. Furthermore, the rise in terrorist attacks in various countries is expected to drive the market for airborne sensors. Battlespace situational awareness is critical for defense forces because it allows them to track enemy movements and decipher hidden information. It is also crucial for detecting adversarial threats in complex operational environments. The nature of the challenges confronting defense forces around the world has changed dramatically. Situational awareness has become critical to ensuring the security of defense personnel in the increasingly networked digital and data-heavy battlespace. Sensor systems such as airborne sensors are increasingly being used by military forces to improve the capabilities of defense equipment. Airborne sensors provide defense forces with instantaneous and continuous coverage of the entire battlefield by providing full-motion videos and intuitive operator interfaces to gain real-time situational awareness.

Furthermore, to carry out defense missions, modern military systems rely heavily on complex software and interconnectivity. Advanced features of cyber-enabled military systems, such as digital attack, airborne sensors systems, and communication systems, start giving equipped armed services a strategic advantage against the implacable enemy force or even during key processes in a harsh atmosphere. Therefore, all such aspects and developments are projected to gain traction for airborne sensors.

To know more about global airborne sensors market trends, get in touch with our analysts here.

High Cost involved with the Deployment of Airborne Sensors Might Restrict the Global Airborne Sensors Market Growth

There are many crucial applications of for airborne sensors for multiple industries, although they are facing issues such as high cost associated with the deployment of airborne sensors is further anticipated to decrease the demand airborne sensors system, which may eventually decline the global market growth, during the forecast period. Due to the high cost of UAVs, their adoption is limited to developed nations with large defense budgets. During the forecast period, this factor is expected to impede the growth of the global airborne sensors market. Also, strict government rules for aviation safety are further anticipated to obstruct the global market growth, in the forecast period.

Growing Presence of Airborne Sensors in the Public Domain Opportunities in the Airborne Sensors Market

The airborne sensors industry has expanded its reach into a variety of commercial sectors, including construction, mining, power supply, and agriculture for crop monitoring, pipeline, power line mapping, and geographical survey. Furthermore, it is useful in the public safety and security sector in firefighting operations and law enforcement for investigation. Furthermore, the global airborne sensors industry is expanding rapidly as a result of increased R&D and technological expansion by industry leaders such as Thales Group. Thales Group, for example, announced in August 2020 the launch of I-Master, an airborne surveillance radar. Radar has a ground and maritime moving target indication mode that can track the movement from land to sea in real time. As a result, it is the ideal type of surveillance in a shore environment. In the coming years, this type of product development and innovation could provide lucrative opportunities for the global airborne sensors market.

Furthermore, key market participants are pursuing strategies to innovate the combination of airborne sensors and signal intelligence technology. For example, IAI, a leader in the defense, aerospace, and commercial markets, has launched ELTA's ELl-3001 airborne signal intelligence system, which is the mission platform designed for modern theatre electronic signal warfare challenges. The system provides high-endurance and long-range signal intelligence (SIGINT) missions, as well as tactical and strategic intelligence on board and on the ground for real-time and off-line analysis. Thus, such factors create an opportunity to gain major pull in the coming years for airborne sensors market.

To know more about global airborne sensors market opportunities, get in touch with our analysts here.

Global Airborne Sensors Market, by Type

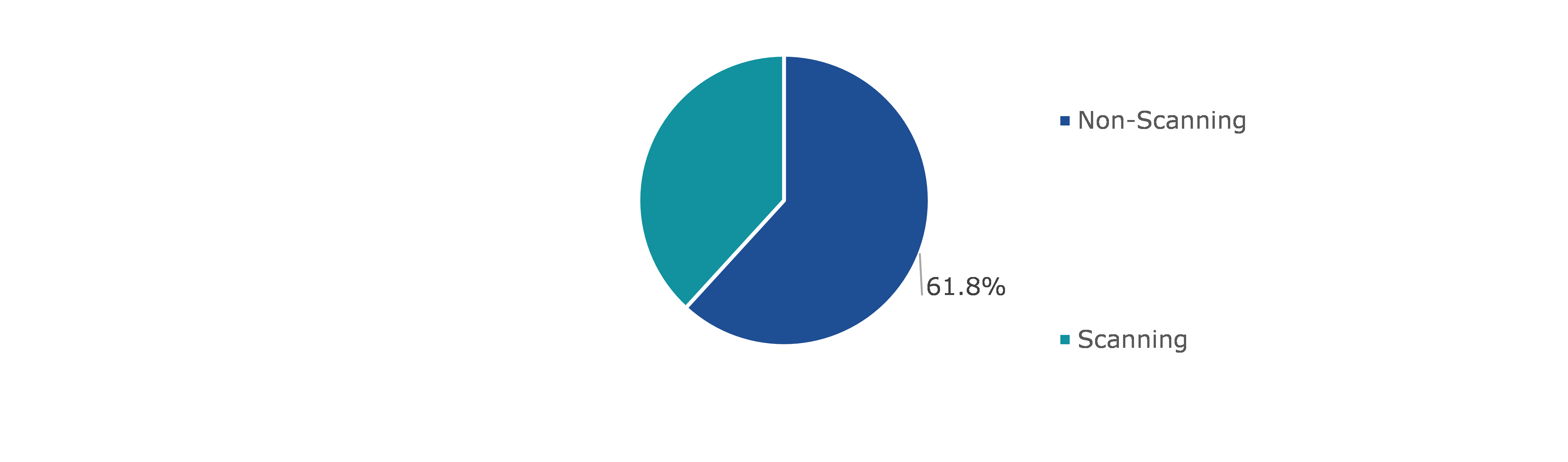

Based on type, the airborne sensors market has been segmented into non-scanning and scanning airborne sensors of which non-scanning sub-segment is expected to have the dominant share during the forecast period.

Global Airborne Sensors Market Share, By Type, 2021

Source: Research Dive Analysis

In 2030, the global non-scanning airborne sensors sub-segment will be worth more than $8,845.9 million. Non-Scanning airborne sensors are passive sensors and it is the non-imaging method of profile recorder. Non scanning airborne sensor is an aerial survey camera such as on board Russian COSMOS satellite. Most of the airborne sensors are flown by on board by pilot, but few of them are unmanned and it can be remotely controlled. The increased number of air passengers in emerging economies is expected to have a significant impact on the growth of the sub-segment. Furthermore, technological advancements, as well as the availability of different classes of airborne sensors such as seaplanes, gliders, and kites, is one of the key factors driving demand for airborne sensors in the global market over the forecast period. Non-scanning airborne sensors can also detect and respond to input from the outside environment. Furthermore, they collect target data information using vibration, heat, or other phenomena and radiation that transmits the signal. Electric field sensing, chemical, seismic, photographic, and thermal sensors are examples of non-scanning airborne sensors. Furthermore, the enormous growth of the airborne sensors market is primarily attributed to the widely increasing use of airborne sensors across multiple industries, as well as the growing emphasis on the development of advanced airborne sensors, which will drive the growth of sub-segment in the coming years.

Global Airborne Sensors Market, by Application

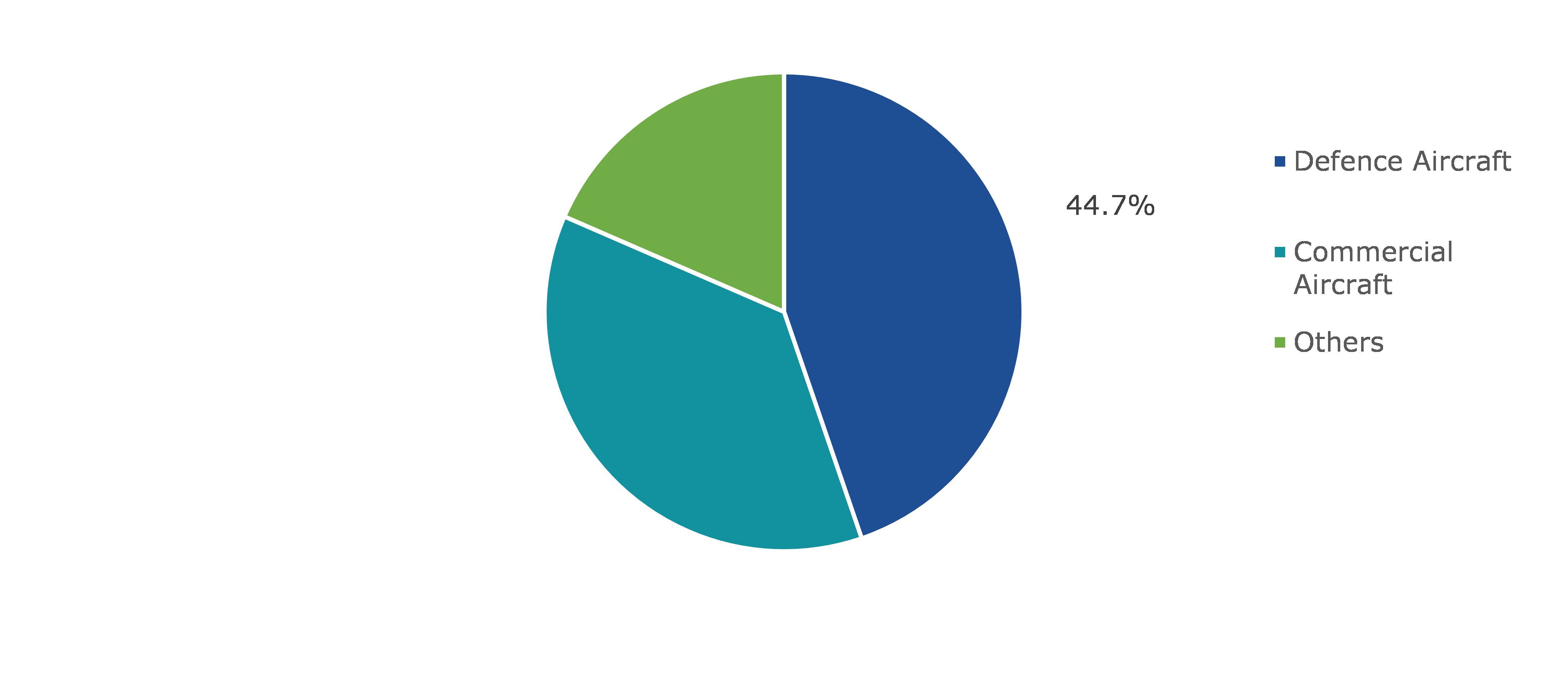

Based on application, the airborne sensors market has been sub-segmented into defense aircraft, commercial aircraft, and others of which defense aircraft sub-segment is expected to have the dominant share as well as the fastest growth during the forecast period.

Global Airborne Sensors Market Share, By Application, 2021

Source: Research Dive Analysis

In 2030, the global defense aircraft sub-segment will be worth more than $6,672.0 million. The expansion is contingent on key market players emerging in the aviation industry and pursuing new strategies to manufacture airborne sensors for defense use. For example, Leonardo, an Italian company that is a key player in aerospace, defense, and security, now offers a variety of airborne sensors solutions, including radar, infrared, and optical sensor systems, as well as multiple airborne management systems. Furthermore, the government's increased defense and military budget has increased demand for airborne sensors in the defense sector. For example, the Taiwanese government announced in August 2020 that it has increased defense budgeting for the coming years, as China revealed details of its recent combat drills near the democratic island. All such factors are expected to promote the adoption of airborne sensors by large enterprises growth during the forecast period.

Global Airborne Sensors Market, Regional Insights:

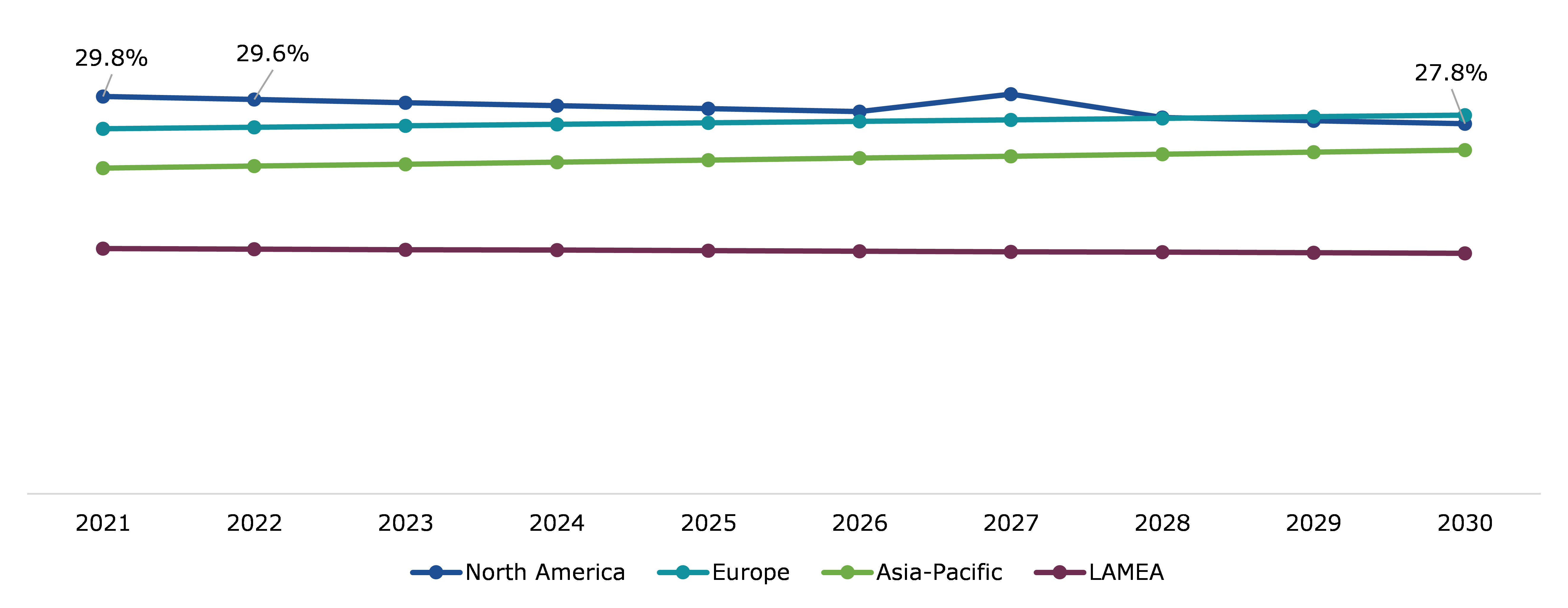

The airborne sensors market was inspected across North America, Europe, Asia-Pacific, and LAMEA.

Global Airborne Sensors Market Size & Forecast, By Region, 2021-2030 (USD Million)

Source: Research Dive Analysis

The Market for Airborne Sensors in Europe to Hold the Maximum Revenue

Europe airborne sensors market is anticipated to generate maximum revenue during the forecast time period and reach $4,110.5 million by 2030, with a CAGR of 5.7%. The importance of airborne sensors has grown significantly in European countries such as Spain, the United Kingdom, Luxembourg, and Denmark. The increasing use of fixed-wing aircraft for air travel will drive the Europe airborne sensors market. Furthermore, airborne sensors platform providers in Europe are pursuing strategic collaborations to drive novel technological innovation and gain a dominant position in the market. For example, in March 2020, TE Connectivity Ltd, Switzerland, announced the acquisition of 78% of the shares of First Sensor AG, the world's largest sensor supplier. As a result, a broader range of products and innovative sensors will be available. All of these elements will drive the Europe airborne sensors market in the coming years. Moving forward, the Ministry of Defense announced in May 2020 that the Defense and Security Accelerator (DASA) has been awarded 13 contracts for the development of electro-optics and infrared (EOIR) sensor capability. EOIR sensors are primarily used in the military for target acquisition, threat warning, target detection, reconnaissance, and surveillance, among other things. This type of government initiative will increase airborne sensors adoption in European countries and accelerate the market for airborne sensors. All such factors are expected to drive the Europe airborne sensors market and witness noticeable growth.

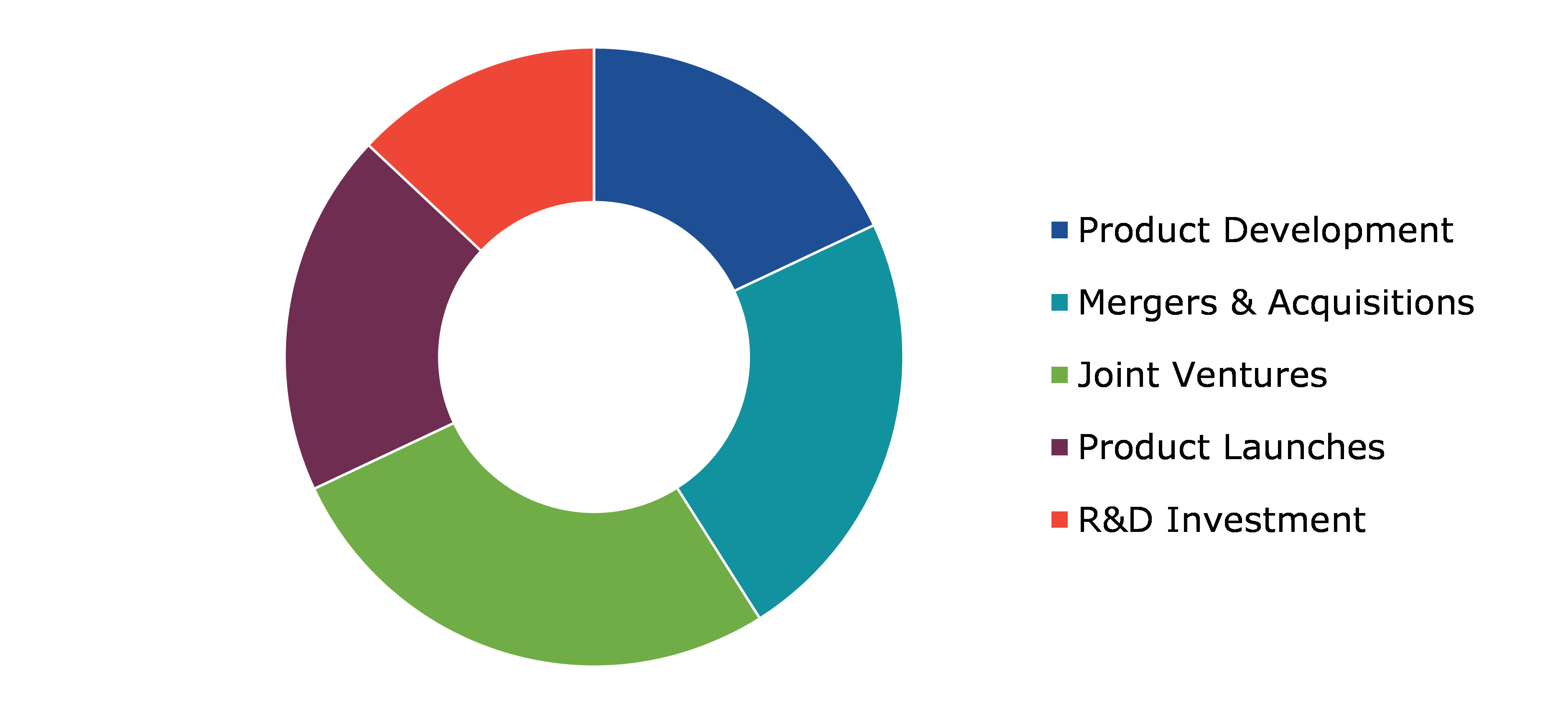

Competitive Scenario in the Global Airborne Sensors Market

Product launches and mergers & acquisitions are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading airborne sensors market players are HEXAGON, Thales Group, Raytheon Technologies, Lockheed Martin Corporation, Information Systems Laboratories (ISL), Teledyne Optech, General Dynamics Corporation, Honeywell International Inc., ITT INC., and AVT Airborne Sensing GmbH.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2030 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global airborne sensors market?

A. The size of the global airborne sensors market is expected to be $14,473.7 million in the year 2030, growing from $9,200.0 million in 2021.

Q2. Which are the major companies in the airborne sensors market?

A. HEXAGON and Thales Group are some of the key players in the global airborne sensors market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific airborne sensors market?

A. Asia-Pacific airborne sensors market is anticipated to grow at 5.9% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. New product development and strategic partnerships are the key strategies opted by the operating companies in this market.

Q6. Which industries are expected to drive the growth of the airborne sensors market in the next 5 years?

A. Defense aircraft is expected to drive the growth of the airborne sensors market in the next 5 years.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global airborne sensors market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on airborne sensors market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Airborne Sensors Market Analysis, by Type

5.1.Overview

5.2.Non-Scanning

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region

5.2.3.Market share analysis, by country

5.3.Scanning

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region

5.3.3.Market share analysis, by country

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Airborne Sensors Market Analysis, by Application

6.1.Defense Aircraft

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region

6.1.3.Market share analysis, by country

6.2.Commercial Aircraft

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region

6.2.3.Market share analysis, by country

6.3.Others

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region

6.3.3.Market share analysis, by country

6.4.Research Dive Exclusive Insights

6.4.1.Market attractiveness

6.4.2.Competition heatmap

7.Airborne Sensors Market, by Region

7.1.North America

7.1.1.U.S.

7.1.1.1.Market size analysis, by Type

7.1.1.2.Market size analysis, by Application

7.1.2.Canada

7.1.2.1.Market size analysis, by Type

7.1.2.2.Market size analysis, by Application

7.1.3.Mexico

7.1.3.1.Market size analysis, by Type

7.1.3.2.Market size analysis, by Application

7.1.4.Research Dive Exclusive Insights

7.1.4.1.Market attractiveness

7.1.4.2.Competition heatmap

7.2.Europe

7.2.1.Germany

7.2.1.1.Market size analysis, by Type

7.2.1.2.Market size analysis, by Application

7.2.2.UK

7.2.2.1.Market size analysis, by Type

7.2.2.2.Market size analysis, by Application

7.2.3.France

7.2.3.1.Market size analysis, by Type

7.2.3.2.Market size analysis, by Application

7.2.4.Spain

7.2.4.1.Market size analysis, by Type

7.2.4.2.Market size analysis, by Application

7.2.5.Italy

7.2.5.1.Market size analysis, by Type

7.2.5.2.Market size analysis, by Application

7.2.6.Rest of Europe

7.2.6.1.Market size analysis, by Type

7.2.6.2.Market size analysis, by Application

7.2.7.Research Dive Exclusive Insights

7.2.7.1.Market attractiveness

7.2.7.2.Competition heatmap

7.3.Asia Pacific

7.3.1.China

7.3.1.1.Market size analysis, by Type

7.3.1.2.Market size analysis, by Application

7.3.2.Japan

7.3.2.1.Market size analysis, by Type

7.3.2.2.Market size analysis, by Application

7.3.3.India

7.3.3.1.Market size analysis, by Type

7.3.3.2.Market size analysis, by Application

7.3.4.Australia

7.3.4.1.Market size analysis, by Type

7.3.4.2.Market size analysis, by Application

7.3.5.South Korea

7.3.5.1.Market size analysis, by Type

7.3.5.2.Market size analysis, by Application

7.3.6.Rest of Asia Pacific

7.3.6.1.Market size analysis, by Type

7.3.6.2.Market size analysis, by Application

7.3.7.Research Dive Exclusive Insights

7.3.7.1.Market attractiveness

7.3.7.2.Competition heatmap

7.4.LAMEA

7.4.1.Brazil

7.4.1.1.Market size analysis, by Type

7.4.1.2.Market size analysis, by Application

7.4.2.Saudi Arabia

7.4.2.1.Market size analysis, by Type

7.4.2.2.Market size analysis, by Application

7.4.3.UAE

7.4.3.1.Market size analysis, by Type

7.4.3.2.Market size analysis, by Application

7.4.4.South Africa

7.4.4.1.Market size analysis, by Type

7.4.4.2.Market size analysis, by Application

7.4.5.Rest of LAMEA

7.4.5.1.Market size analysis, by Type

7.4.5.2.Market size analysis, by Application

7.4.6.Research Dive Exclusive Insights

7.4.6.1.Market attractiveness

7.4.6.2.Competition heatmap

8.Competitive Landscape

8.1.Top winning strategies, 2021

8.1.1.By strategy

8.1.2.By year

8.2.Strategic overview

8.3.Market share analysis, 2021

8.4.Top Five Players Market Overview

8.5.Airborne sensors Market, By Company

9.Company Profiles

9.1.HEXAGON

9.1.1.Overview

9.1.2.Business segments

9.1.3.Product portfolio

9.1.4.Financial performance

9.1.5.Recent developments

9.1.6.SWOT analysis

9.2.Thales Group

9.2.1.Overview

9.2.2.Business segments

9.2.3.Product portfolio

9.2.4.Financial performance

9.2.5.Recent developments

9.2.6.SWOT analysis

9.3.Raytheon Technologies

9.3.1.Overview

9.3.2.Business segments

9.3.3.Product portfolio

9.3.4.Financial performance

9.3.5.Recent developments

9.3.6.SWOT analysis

9.4.Lockheed Martin Corporation

9.4.1.Overview

9.4.2.Business segments

9.4.3.Product portfolio

9.4.4.Financial performance

9.4.5.Recent developments

9.4.6.SWOT analysis

9.5.ISL

9.5.1.Overview

9.5.2.Business segments

9.5.3.Product portfolio

9.5.4.Financial performance

9.5.5.Recent developments

9.5.6.SWOT analysis

9.6.Teledyne Optech

9.6.1.Overview

9.6.2.Business segments

9.6.3.Product portfolio

9.6.4.Financial performance

9.6.5.Recent developments

9.6.6.SWOT analysis

9.7.General Dynamics Corporation

9.7.1.Overview

9.7.2.Business segments

9.7.3.Product portfolio

9.7.4.Financial performance

9.7.5.Recent developments

9.7.6.SWOT analysis

9.8.Honeywell International Inc.

9.8.1.Overview

9.8.2.Business segments

9.8.3.Product portfolio

9.8.4.Financial performance

9.8.5.Recent developments

9.8.6.SWOT analysis

9.9.ITT INC.

9.9.1.Overview

9.9.2.Business segments

9.9.3.Product portfolio

9.9.4.Financial performance

9.9.5.Recent developments

9.9.6.SWOT analysis

9.10.AVT Airborne Sensing GmbH

9.10.1.Overview

9.10.2.Business segments

9.10.3.Product portfolio

9.10.4.Financial performance

9.10.5.Recent developments

9.10.6.SWOT analysis

10.Appendix

10.1.Parent & peer market analysis

10.2.Premium insights from industry experts

10.3.Related reports

The escalating terrorism problem is pushing government bodies to get on their toes and do every possible thing to avert a terrorist attack. The defence sector is integrating all the topmost technologies to tackle terrorists and predict their attacks beforehand. One of the prominent technologies being used in the military and defence sector is an airborne sensor.

What is Airborne Remote Sensing?

In airborne remote sensing, sideward or downward looking facing sensors are fixed on an airplane to capture images of the surface of the earth. One of the key benefit of airborne remote sensing, as compared to satellite remote sensing, is its ability to provide enhanced spatial resolution images (20 cm or less).

Why is the Demand for Airborne Sensors Mounting?

Airborne sensors play a crucial role in intelligence departments, support surveillance, and investigation gathering activities in army operations. As the terrorist attacks across several nations is rapidly rising, the need for efficient remote sensing devices has also surged. The airborne sensor industry is witnessing a gigantic growth chiefly owing to an upsurge in implementation of airborne sensors in the defence and military sector. Apart from this, the airborne sensors market has been extending its reach in numerous application areas like in commercial industries, construction activities, mining operations, power supply, and farming for observing the crops, power line mapping, pipeline, and geographical inspection. All this specifies that the airborne sensors market is going to have a rewarding scope in the coming years.

Latest Trends in the Airborne Sensors Market

As per a report by Research Dive, the global airborne sensors market is expected to grow from $9,200.0 million in 2019 to $14,473.7 million by 2030. The airborne sensors market in Europe is the most dominant and anticipated to grow speedily with a CAGR of 5.3% from 2022–2030. This is mainly owing to the rising tactical partnerships amongst the market players and launch of numerous innovative airborne sensors in this region. The region is deliberated as the most rewarding market for the airborne sensors, due to growing significance of airborne sensors in Spain, Luxembourg, the United Kingdom, and Denmark.

Market players are significantly investing in research and development to cater the swelling demand for airborne sensors. Some of the notable players of the airborne sensors market are Teledyne Optech, HEXAGON, Thales Group, Lockheed Martin Corporation, Information Systems Laboratories (ISL), Honeywell International Inc., ITT INC., General Dynamics Corporation, AVT Airborne Sensing GmbH., Raytheon Technologies, and others. These players are focused on forming strategies, for example, mergers and acquisitions, partnerships, novel developments, and collaborations to achieve a prominent position in the global market.

For instance,

- In January 2018, CyberOptics Corporation, a foremost global designer and producer of high precision 3D sensing technologies, launched a next-generation Airborne Particle Sensor technology (APS3) 300mm with novel ParticleSpectrum™ software.

- In August 2020, Teledyne Optech, a Canada-based advanced Lidar sensors firm, extended its Galaxy product-line to include the CM2000, an airborne lidar sensor particularly developed for corridor mapping.

- In September 2020, Applanix, a developer and manufacturer of a line of Inertial Navigation System products., launched the Trimble® AP+ Air OEM solution for Direct Geo-referencing of airborne sensor data. The solution allows users to precisely and competently generate maps and 3D models without using ground control points.

COVID-19 Impact on the Airborne Sensors Market

The abrupt rise of the coronavirus pandemic in 2020 has curbed the growth of the global airborne sensors market. This is mainly due to the cessation of airborne sensor manufacturing factories due to the implementation of lockdown during the pandemic period. Also, a significant drop in the agriculture activates, due to lockdown restrictions during the pandemic, has declined the use of airborne sensors; which has hindered the market growth. However, as the worldwide economy is recovering with the easing of pandemic, the airborne sensors market is expected to gain momentum with a remarkable increase in defence and agricultural activities worldwide. This is likely to boost the airborne sensors market in the upcoming years.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com