Silicone Coatings Market Report

RA08127

Silicone Coatings Market by Type (Silicone Additives, Silicone Polymers, 100% Silicone, and Silicone Water Repellents), Technology (Solvent-based, Water-based, and Powder-based), End Use (Construction, Automotive, Electrical & Electronics, Paints & Coatings, Marine, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Silicone Coatings Overview

Silicone coatings are adaptable and inventive solutions. Due to their unique qualities and remarkable performance characteristics, they have found significant use across a wide range of sectors. Silicone coatings are derived from silicon, a chemical element common in nature, and are generated through a sophisticated synthesis process that results in a durable and flexible material with several applications. Silicone is fundamentally a synthetic polymer made up of silicon, oxygen, carbon, and hydrogen atoms organized in constant chemical sequence. This molecular structure gives silicone coatings extraordinary qualities, such as resistance to severe temperatures, UV radiation, and weathering. Silicone coatings are exceptionally thermally stable, withstanding both high and low temperatures. Because of this, they are useful in sectors where high temperature changes are prevalent. Silicone-coated materials provide dependable performance even in the hardest weather conditions, from automobile components to electrical equipment. Silicone coatings are also used in the manufacture of cookware and bakeware due to their ability to tolerate heat. Silicone coatings' adaptation extends to the medical area, where their biocompatibility and hypoallergenic characteristics make them appropriate for a variety of applications.

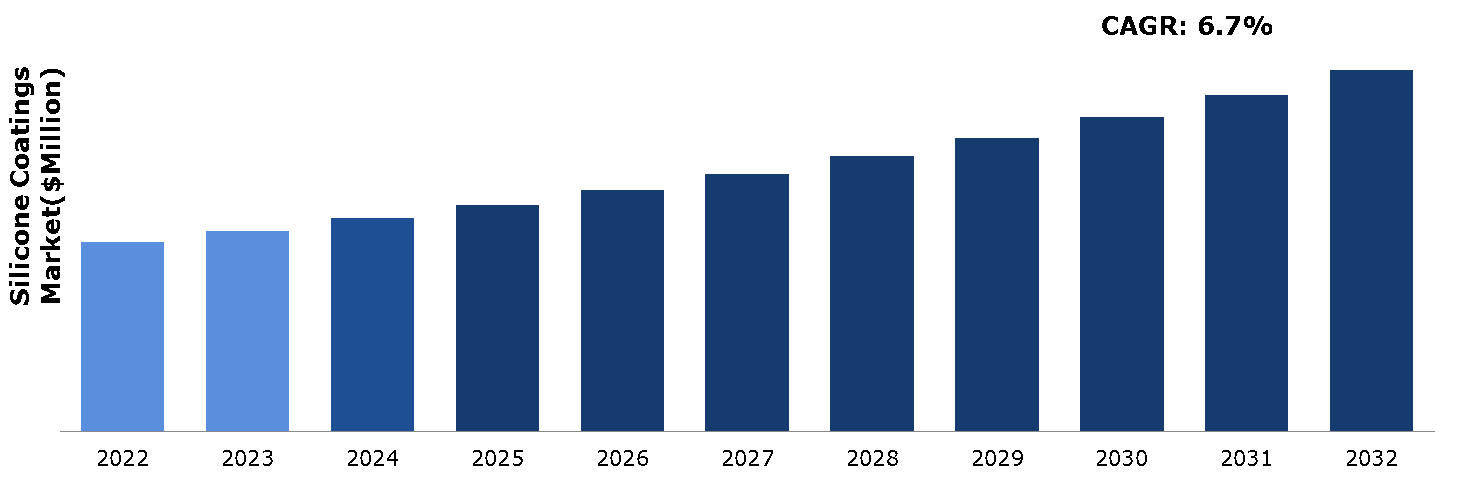

Global Silicone Coatings Market Analysis

The global silicone coatings market size was $5,283.8 million in 2022 and is predicted to grow with a CAGR of 6.7%, by generating a revenue of $10,098.9 million by 2032.

Source: Research Dive Analysis

High Resistance to Chemical Contaminants to Drive the Market Growth

One of the key benefits of silicone coatings is their ability to successfully withstand chemical impurities. Silicone coating is essential in various sectors such as, automotive systems, industrial machinery, or electronic gadgets. Silicone coatings offer a strong protective shell that protects the components from the harmful effects of numerous chemical contaminants. This resistance to chemical pollutants is essential in maintaining vehicle functionality and longevity, guaranteeing maximum performance even under difficult settings. Silicone coatings' chemical resistance is due to the unusual molecular structure of silicones. Silicones are polymers made up of repeating units of silicon and oxygen atoms that have organic groups attached to them. Silicone coatings serve an important role in protecting electronic components from the corrosive effects of road salts, automotive fluids, and ambient contaminants in automobile applications. The electrical systems in automobiles, which are controlled by advanced systems, are vulnerable to harm from dampness and pollutants. Silicone coatings operate as a trustworthy barrier, keeping these corrosive chemicals from penetrating the sensitive electronic components and impairing their performance. This resistance to chemical pollutants improves the dependability and longevity adding to the overall efficiency and safety of cars.

Adhesion Limitations of Silicone Coatings to Restrain the Market Growth

The intrinsic low surface energy of silicone materials is a significant barrier to adhesion in silicone coatings. Owing to the low surface energy, traditional adhesives and coatings struggle to create strong connections with silicone surfaces. The silicone molecules have a distinct structure that provides hydrophobic qualities, resulting in poor wetting and adherence. This constraint presents difficulties in applications requiring high adhesion, such as the automotive and aerospace sectors, where coatings are subjected to harsh climatic conditions and mechanical strains. Furthermore, the presence of release agents and mold release compounds on silicone surfaces makes adhesion much more difficult. These compounds are often used during the production process to help silicone goods release easily from molds. While these release agents are necessary for the manufacturing process, they form a barrier that prevents subsequent coatings or adhesives from attaching. This constraint makes the use of secondary coatings or the bonding of silicone-based materials in a variety of industrial contexts more difficult. Silicone coatings have additional difficulties due to their restricted compatibility with specific substrates. While silicone bonds effectively to other silicone materials, its adherence to substrates such as metals, plastics, or glass can be weak. This constraint limits the possible uses of silicone coatings in situations where different materials must be bonded or coated together.

Developing Construction Industry to Drive Excellent Opportunities

Technological improvements have been vital in boosting the use of silicone coatings in the construction industry. Manufacturers are continually modifying the composition of silicone coatings to improve their performance attributes via continuing R&D. Improvements in adhesion, flexibility, and UV resistance make silicone coatings a most preferred choice for construction applications. The development of self-cleaning and self-healing qualities in silicone coatings adds to its appeal, delivering long-term benefits such as lower maintenance costs and extended building structure longevity. As technology advances, the construction sector is set to capitalize on these advances, creating a favorable environment for the widespread usage of silicone coatings. Regulatory assistance and compliance requirements also play an important part in adoption of silicone coatings in the construction industry. As governments throughout the world step up their efforts to regulate building materials and procedures, the use of environmentally friendly and compatible goods becomes increasingly important. The legislative push for environmentally friendly and energy-efficient buildings creates a need for materials that fulfil particular performance standards. Silicone coatings are well-positioned to meet these demands due to their proven track record in energy efficiency, weather resilience, and compliance with severe environmental rules.

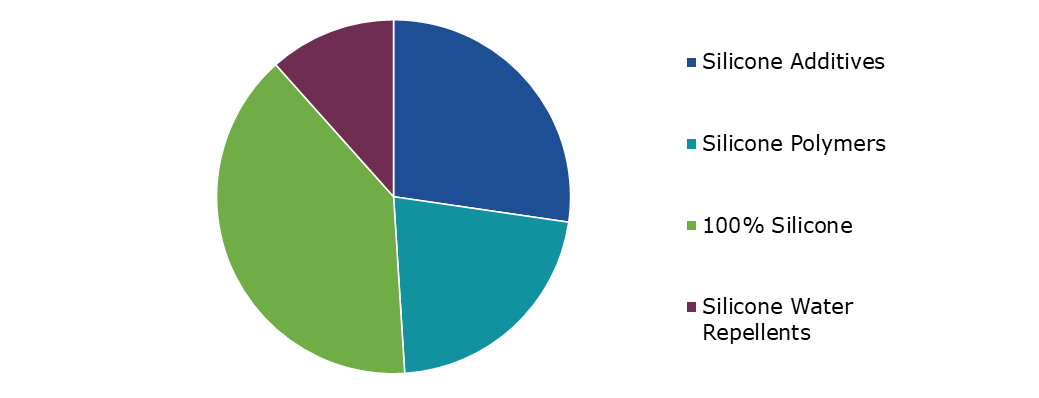

Global Silicone Coating Market Share, by Type, 2022

Source: Research Dive Analysis

The 100% silicone sub-segment accounted for the highest market share in 2022. The remarkable weather resilience of 100% silicone in silicone coatings is one of the key driving factors behind its adoption. When exposed to adverse environmental conditions such as UV radiation, high temperatures, and dampness, silicone demonstrates remarkable endurance. Because of this robustness, silicone coatings retain their integrity and protective properties over time, making them excellent for external applications such as building exteriors, bridges, and automobile surfaces. 100% silicone coatings' ability to withstand weathering adds greatly to their popularity in areas where long-term performance is essential. Another important driving factor is silicone coatings' high-water repellency. Silicone is naturally hydrophobic, generating a tight molecular barrier that keeps water out. Because of this property, silicone coatings are extremely successful in protecting surfaces from water damage, corrosion, and mold formation. Water-resistant features of 100% silicone coatings serve industries ranging from construction to marine applications, assuring the longevity and structural integrity of coated objects.

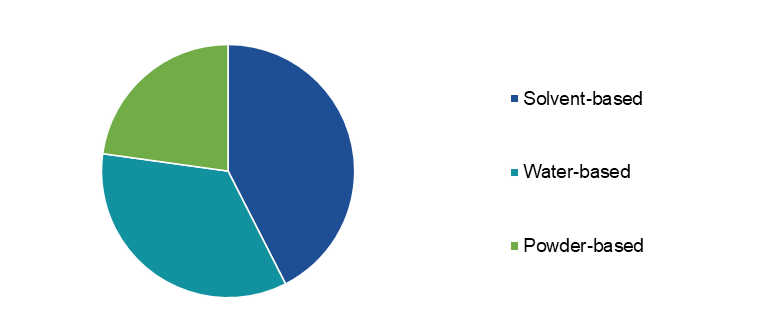

Global Silicone Coating Market Share, by Technology, 2022

Source: Research Dive Analysis

The solvent-based sub-segment accounted for the highest market share in 2022. The exceptional endurance of solvent-based silicone coatings is one of the main reasons driving their adoption. These coatings withstand abrasion, solvents, and extreme environmental conditions with ease. Because of the inherent molecular structure of silicone polymers, the coatings may endure prolonged contact to hostile chemicals without losing their protective qualities. Because of their endurance, solvent-based silicone coatings are ideal for applications requiring long-term performance and resistance to wear, in industrial settings, automotive components, and shipping constructions. Heat resistance is a vital driving element in the selection of solvent-based silicone coatings in high-temperature situations. Silicone polymers have exceptional heat stability by nature, allowing coatings to retain their integrity and protective characteristics even at high temperatures. This qualifies them for use in sectors such as aerospace, automobile production, and metal processing, where heat is a major concern. The ability of solvent-based silicone coatings to withstand severe temperatures without degrading increases their applicability in a variety of industries.

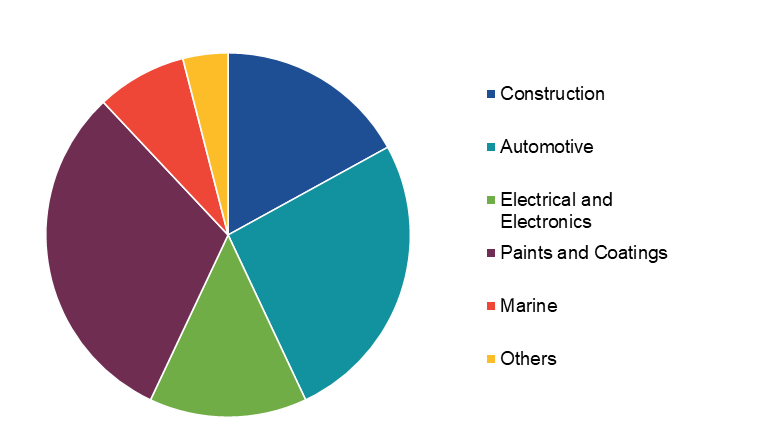

Global Silicone Coating Market Share, by End Use, 2022

Source: Research Dive Analysis

The paints & coatings sub-segment accounted for the highest market share in 2022. Silicone coatings are well-known for their high heat resilience. This distinguishing feature helps them to retain structural integrity and performance under high-temperature circumstances. Silicone coatings are increasingly being used to improve the heat resistance of surfaces in industries such as automotive, aerospace, and industrial production, where exposure to high temperatures is prevalent. This aspect makes silicone coatings a popular choice for applications needing heat stability, increasing their demand in the paints & coatings sector. Ongoing R&D activities in formulation technologies are resulting in continuing advances in silicone coatings. Manufacturers are investing in R&D to improve the performance features of silicone-based products such as adhesion, flexibility, and simplicity of application. These developments help to broaden the variety of silicone coating applications, driving their acceptance in the paints & coatings industry.

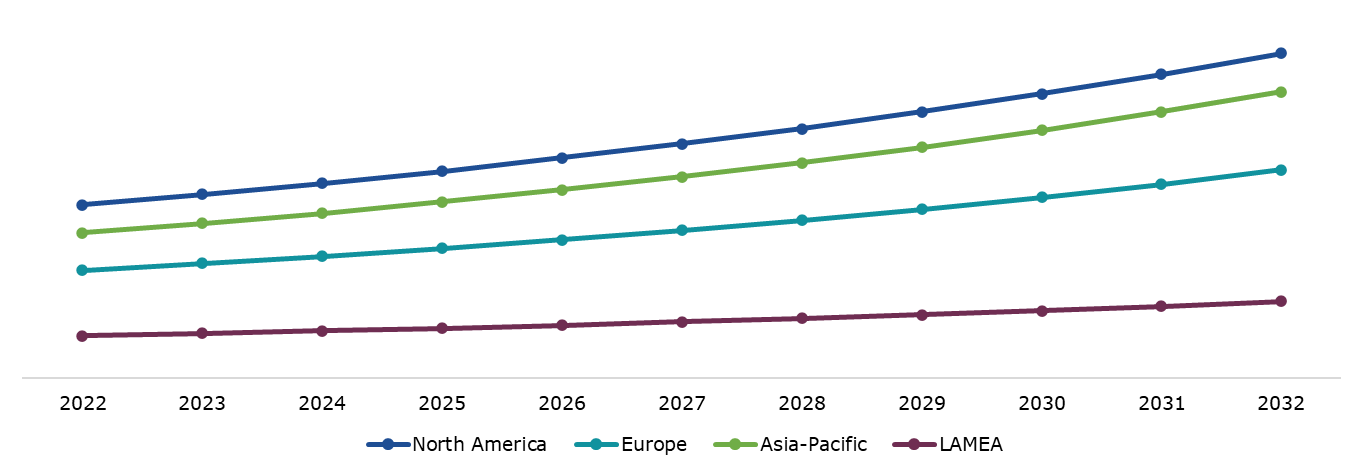

Global Silicone Coating Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The North America silicone coating market generated the highest revenue in 2022. The rapid rise in the construction sector is a significant driving element. Construction activities across North America have increased as a result of urbanization, infrastructural expansion, and rising demand for energy-efficient buildings. Silicone coatings are critical in protecting structures from severe weather, UV radiation, and environmental toxins. Silicone coatings' exceptional weatherability and durability make them perfect for external applications, adding to the lifetime and aesthetics of structures. Demand for silicone coatings, which are recognized for their eco-friendliness, is increasing as sustainable building techniques gain hold. Furthermore, the use of silicone coatings is increasing in the textiles and healthcare industries. These coatings are used in textiles to improve fabric qualities including water repellency, stain resistance, and durability. Silicone coatings are used in healthcare for medical devices and equipment due to its biocompatibility, non-toxicity, and resistance to microbial development. Silicone coatings' broad uses across sectors lead to their extensive use in North America.

Competitive Scenario in the Global Silicone Coating Market

Product innovation & development and market expansion are common strategies followed by major market players. For instance, on September 4, 2023, Evonik launched a new UV LED (TEGO RC 2000 LCF) made using recycled silicone feedstocks. The released coating can be cured using either the less energy intensive UV LED or traditional UV Arc lamps.

Source: Research Dive Analysis

Some of the leading silicone coating market players are Evonik Industries AG, Wacker Chemie AG, Carboline Company, OMG Borchers GmbH, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials Inc, DOW Corning Corporation, ACC Silicones Ltd., MAPEI SpA, and Sika AG.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by Technology |

|

| Segmentation by End Use |

|

| Key Companies Profiled |

|

Q1. What is the size of the global silicone coating market?

A. The size of the global silicone coating market was $5,283.8 million in 2022 and is projected to reach $10,098.9 million by 2032.

Q2. Which are the major companies in the silicone coating market?

A. Evonik Industries AG, Wacker Chemie AG, Carboline Company, OMG Borchers GmbH, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials Inc, DOW Corning Corporation, ACC Silicones Ltd., MAPEI SpA, and Sika AG are some of the key players in the global silicone coating market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific silicone coating market?

A. The Asia-Pacific silicone coating market is anticipated to grow at 7.1% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Market expansion and product innovation & development are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. DOW Corning Corporation and Carboline Company are the companies investing more on R&D activities for developing new products and technologies

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global silicone coatings market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry Intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Legal

4.6.6. Environmental

4.7. Impact of COVID-19 on silicone coatings market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Silicone Coatings Market Analysis, By Type

5.1. Overview

5.2. Silicone Additives

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. Silicone Polymers

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. 100% Silicone

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2022-2032

5.4.3. Market share analysis, by country, 2022-2032

5.5. Silicone Water Repellents

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2. Market size analysis, by region, 2022-2032

5.5.3. Market share analysis, by country, 2022-2032

5.6. Research Dive Exclusive Insights

5.6.1. Market attractiveness

5.6.2. Competition heatmap

6. Silicone Coatings Market Analysis, by Technology

6.1. Overview

6.2. Solvent-based

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Water-based

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2022-2032

6.3.3. Market share analysis, by country, 2022-2032

6.4. Powder-based

6.4.1. Definition, key trends, growth factors, and opportunities

6.4.2. Market size analysis, by region, 2022-2032

6.4.3. Market share analysis, by country, 2022-2032

6.5. Research Dive Exclusive Insights

6.5.1. Market attractiveness

6.5.2. Competition heatmap

7. Silicone Coatings Market Analysis, by End Use

7.1. Overview

7.2. Construction

7.2.1. Definition, key trends, growth factors, and opportunities

7.2.2. Market size analysis, by region, 2022-2032

7.2.3. Market share analysis, by country, 2022-2032

7.3. Automotive

7.3.1. Definition, key trends, growth factors, and opportunities

7.3.2. Market size analysis, by region, 2022-2032

7.3.3. Market share analysis, by country, 2022-2032

7.4. Electrical & Electronics

7.4.1. Definition, key trends, growth factors, and opportunities

7.4.2. Market size analysis, by region, 2022-2032

7.4.3. Market share analysis, by country, 2022-2032

7.5. Paints & Coatings

7.5.1. Definition, key trends, growth factors, and opportunities

7.5.2. Market size analysis, by region, 2022-2032

7.5.3. Market share analysis, by country, 2022-2032

7.6. Marine

7.6.1. Definition, key trends, growth factors, and opportunities

7.6.2. Market size analysis, by region, 2022-2032

7.6.3. Market share analysis, by country, 2022-2032

7.7. Others

7.7.1. Definition, key trends, growth factors, and opportunities

7.7.2. Market size analysis, by region, 2022-2032

7.7.3. Market share analysis, by country, 2022-2032

7.8. Research Dive Exclusive Insights

7.8.1. Market attractiveness

7.8.2. Competition heatmap

8. Silicone Coatings Market, by Region

8.1. North America

8.1.1. U.S.

8.1.1.1. Market size analysis, by Type, 2022-2032

8.1.1.2. Market size analysis, by Technology, 2022-2032

8.1.1.3. Market size analysis, by End Use, 2022-2032

8.1.2. Canada

8.1.2.1. Market size analysis, by Type, 2022-2032

8.1.2.2. Market size analysis, by Technology, 2022-2032

8.1.2.3. Market size analysis, by End Use, 2022-2032

8.1.3. Mexico

8.1.3.1. Market size analysis, by Type, 2022-2032

8.1.3.2. Market size analysis, by Technology, 2022-2032

8.1.3.3. Market size analysis, by End Use, 2022-2032

8.1.4. Research Dive Exclusive Insights

8.1.4.1. Market attractiveness

8.1.4.2. Competition heatmap

8.2. Europe

8.2.1. Germany

8.2.1.1. Market size analysis, by Type, 2022-2032

8.2.1.2. Market size analysis, by Technology, 2022-2032

8.2.1.3. Market size analysis, by End Use, 2022-2032

8.2.2. UK

8.2.2.1. Market size analysis, by Type, 2022-2032

8.2.2.2. Market size analysis, by Technology, 2022-2032

8.2.2.3. Market size analysis, by End Use, 2022-2032

8.2.3. France

8.2.3.1. Market size analysis, by Type, 2022-2032

8.2.3.2. Market size analysis, by Technology, 2022-2032

8.2.3.3. Market size analysis, by End Use, 2022-2032

8.2.4. Spain

8.2.4.1. Market size analysis, by Type, 2022-2032

8.2.4.2. Market size analysis, by Technology, 2022-2032

8.2.4.3. Market size analysis, by End Use, 2022-2032

8.2.5. Italy

8.2.5.1. Market size analysis, by Type, 2022-2032

8.2.5.2. Market size analysis, by Technology, 2022-2032

8.2.5.3. Market size analysis, by End Use, 2022-2032

8.2.6. Rest of Europe

8.2.6.1. Market size analysis, by Type, 2022-2032

8.2.6.2. Market size analysis, by Technology, 2022-2032

8.2.6.3. Market size analysis, by End Use, 2022-2032

8.2.7. Research Dive Exclusive Insights

8.2.7.1. Market attractiveness

8.2.7.2. Competition heatmap

8.3. Asia-Pacific

8.3.1. China

8.3.1.1. Market size analysis, by Type, 2022-2032

8.3.1.2. Market size analysis, by Technology, 2022-2032

8.3.1.3. Market size analysis, by End Use, 2022-2032

8.3.2. Japan

8.3.2.1. Market size analysis, by Type, 2022-2032

8.3.2.2. Market size analysis, by Technology, 2022-2032

8.3.2.3. Market size analysis, by End Use, 2022-2032

8.3.3. India

8.3.3.1. Market size analysis, by Type, 2022-2032

8.3.3.2. Market size analysis, by Technology, 2022-2032

8.3.3.3. Market size analysis, by End Use, 2022-2032

8.3.4. Australia

8.3.4.1. Market size analysis, by Type, 2022-2032

8.3.4.2. Market size analysis, by Technology, 2022-2032

8.3.4.3. Market size analysis, by End Use, 2022-2032

8.3.5. Indonesia

8.3.5.1. Market size analysis, by Type, 2022-2032

8.3.5.2. Market size analysis, by Technology, 2022-2032

8.3.5.3. Market size analysis, by End Use, 2022-2032

8.3.6. Rest of Asia-Pacific

8.3.6.1. Market size analysis, by Type, 2022-2032

8.3.6.2. Market size analysis, by Technology, 2022-2032

8.3.6.3. Market size analysis, by End Use, 2022-2032

8.3.7. Research Dive Exclusive Insights

8.3.7.1. Market attractiveness

8.3.7.2. Competition heatmap

8.4. LAMEA

8.4.1. Brazil

8.4.1.1. Market size analysis, by Type, 2022-2032

8.4.1.2. Market size analysis, by Technology, 2022-2032

8.4.1.3. Market size analysis, by End Use, 2022-2032

8.4.2. UAE

8.4.2.1. Market size analysis, by Type, 2022-2032

8.4.2.2. Market size analysis, by Technology, 2022-2032

8.4.2.3. Market size analysis, by End Use, 2022-2032

8.4.3. South Africa

8.4.3.1. Market size analysis, by Type, 2022-2032

8.4.3.2. Market size analysis, by Technology, 2022-2032

8.4.3.3. Market size analysis, by End Use, 2022-2032

8.4.4. Argentina

8.4.4.1. Market size analysis, by Type, 2022-2032

8.4.4.2. Market size analysis, by Technology, 2022-2032

8.4.4.3. Market size analysis, by End Use, 2022-2032

8.4.5. Rest of LAMEA

8.4.5.1. Market size analysis, by Type, 2022-2032

8.4.5.2. Market size analysis, by Technology, 2022-2032

8.4.5.3. Market size analysis, by End Use, 2022-2032

8.4.6. Research Dive Exclusive Insights

8.4.6.1. Market attractiveness

8.4.6.2. Competition heatmap

9. Competitive Landscape

9.1. Top winning strategies, 2022

9.1.1. By strategy

9.1.2. By year

9.2. Strategic overview

9.3. Market share analysis, 2022

10. Company Profiles

10.1. Evonik Industries AG

10.1.1. Overview

10.1.2. Business segments

10.1.3. Product portfolio

10.1.4. Financial performance

10.1.5. Recent developments

10.1.6. SWOT analysis

10.2. Wacker Chemie AG

10.2.1. Overview

10.2.2. Business segments

10.2.3. Product portfolio

10.2.4. Financial performance

10.2.5. Recent developments

10.2.6. SWOT analysis

10.3. Carboline Company

10.3.1. Overview

10.3.2. Business segments

10.3.3. Product portfolio

10.3.4. Financial performance

10.3.5. Recent developments

10.3.6. SWOT analysis

10.4. OMG Borchers GmbH

10.4.1. Overview

10.4.2. Business segments

10.4.3. Product portfolio

10.4.4. Financial performance

10.4.5. Recent developments

10.4.6. SWOT analysis

10.5. Shin-Etsu Chemical Co., Ltd.

10.5.1. Overview

10.5.2. Business segments

10.5.3. Product portfolio

10.5.4. Financial performance

10.5.5. Recent developments

10.5.6. SWOT analysis

10.6. Momentive Performance Materials Inc.

10.6.1. Overview

10.6.2. Business segments

10.6.3. Product portfolio

10.6.4. Financial performance

10.6.5. Recent developments

10.6.6. SWOT analysis

10.7. DOW Corning Corporation

10.7.1. Overview

10.7.2. Business segments

10.7.3. Product portfolio

10.7.4. Financial performance

10.7.5. Recent developments

10.7.6. SWOT analysis

10.8. ACC Silicones Ltd.

10.8.1. Overview

10.8.2. Business segments

10.8.3. Product portfolio

10.8.4. Financial performance

10.8.5. Recent developments

10.8.6. SWOT analysis

10.9. MAPEI SpA

10.9.1. Overview

10.9.2. Business segments

10.9.3. Product portfolio

10.9.4. Financial performance

10.9.5. Recent developments

10.9.6. SWOT analysis

10.10. Sika AG

10.10.1. Overview

10.10.2. Business segments

10.10.3. Product portfolio

10.10.4. Financial performance

10.10.5. Recent developments

10.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com