Recycled Plastics Market Report

RA06991

Recycled Plastics Market by Type (Polyethylene Terephthalate (PET), High Density Polyethylene (HDPE), Polypropylene (PP), and Others), End-use Industry (Agriculture, Farming & Gardening, Building & Construction, Packaging, Automotive, Electrical & Electronics, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Recycled Plastics Overview

Recycled plastics refer to plastic materials that have undergone a process of recycling which involves collecting used or discarded plastic products and transforming them into new plastic products or raw materials. Recycling plastic helps reduce the environmental impact of plastic waste by diverting it from landfills or incineration and giving it a new life. Used plastic products such as bottles, containers, packaging, and other items are collected from households, businesses, and other sources.

The recycled plastic pellets can be used to produce a wide range of products including new plastic containers, packaging, textiles, furniture, construction materials and more. Recycling plastic prevents plastic waste from piling up in landfills or polluting the environment. The process of recycling often requires less energy than producing new plastic from raw materials which helps reduce greenhouse gas emissions. Recycling plastic can contribute to a reduction in carbon dioxide emissions compared to producing new plastic.

Global Recycled Plastics Market Analysis

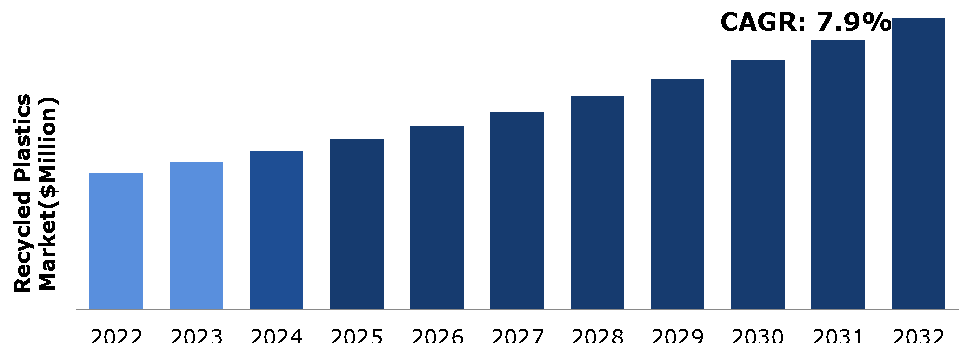

The global recycled plastics market size was $66,730.00 million in 2022 and is predicted to grow with a CAGR of 7.9%, by generating a revenue of $141,942.10 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Recycled Plastics Market

The pandemic disrupted global supply chains, affecting the collection, sorting, and processing of recycled plastics. Lockdowns, restrictions on movement, and labor shortages hindered the operations of recycling facilities and impacted the availability of recycled plastics. Many industries that are significant consumers of recycled plastics such as automotive, construction, and consumer goods, experienced a slowdown in demand due to lockdowns and reduced consumer spending. This reduced demand for products containing recycled plastics, which in turn affected the demand for recycled plastic materials. The price of virgin plastics is influenced by the price of crude oil. Early in the pandemic, there was a sharp drop in oil prices, which made virgin plastics cheaper in comparison to recycled plastics. This pricing dynamic could affected the competitiveness of recycled plastics. The increased use of single-use plastics, such as personal protective equipment (PPE) and packaging for takeaway food, due to hygiene concerns during the pandemic, altered the composition of plastics entering the recycling stream. The focus on health and safety during the pandemic temporarily shifted attention away from sustainability and environmental concerns, potentially impacting the prioritization of recycled plastics in various industries. Some governments delayed or reprioritized environmental policies and initiatives in response to the pandemic. However, some regions also recognized the importance of sustainable practices and invested in circular economy strategies to promote recycling and reduce plastic waste.

Increase in Environmental Awareness and Sustainability to Drive the Market Growth

The alarming level of plastic pollution in oceans and waterways have gained widespread attention. Images of marine life entangled in or ingesting plastics have raised public awareness and prompted a call for action to reduce plastic waste. This has pushed governments, industries, and individuals to seek solutions such as recycling to address the issue. Moreover, single-use plastics, like disposable packaging and utensils have come under scrutiny due to their short usage lifespan and long-lasting environmental impact. Awareness campaigns, documentaries and news coverage have shed light on the detrimental effects of these plastics on ecosystems, wildlife, and human health. This has prompted consumers and businesses to seek alternatives, including recycled plastics to minimize their ecological footprint. Furthermore, people are becoming more conscious of their environmental impact and are making informed choices to align with sustainable practices. This includes opting for products and packaging made from recycled materials. Consumers are increasingly seeking out products that align with their sustainability values. Businesses that use recycled plastics in their products can attract environmentally conscious consumers giving them a competitive edge in the market. This approach reduces the need for virgin resources, conserves energy, and minimizes waste generation. The economic and environmental benefits of adopting circular economy principles have pushed industries to incorporate recycled plastics into their supply chains. Many countries and organizations are striving to transition towards a circular economy where resources are used more efficiently, waste is minimized, and products are designed for reuse and recycling. Recycled plastics play a crucial role in achieving these goals by providing a sustainable source of material for manufacturing.

Quality and Consistency Issues to Restrain the Market Growth

The recycling process often involves multiple heating and cooling cycles which can lead to degradation of the polymer chains in plastics. This degradation can result in a loss of mechanical properties such as strength and durability. The quality of recycled plastics may not meet the requirements for certain high-performance applications, limiting their potential uses. Moreover, contamination is a significant concern in the recycled plastics market. For instance, chemicals from contaminants might leach into food packaging made from recycled plastics, posing health risks. Moreover, the lack of standardized methods for recycling different types of plastics can lead to inconsistency in quality and properties across different recycling processes and facilities. This lack of standardization makes it difficult to ensure consistent quality in the resulting recycled materials. Developing and implementing advanced recycling technologies, sorting methods, and cleaning processes require significant investments. If the cost of recycling exceeds the value of the recycled material, it can be challenging to establish a sustainable business model. Effective recycling requires consumer participation in proper waste separation and disposal. Lack of awareness or motivation to recycle, as well as inconsistent recycling behaviors, can limit the availability of high-quality recycled plastics, which is anticipated to hamper the recycled plastics market growth.

Innovations in Recycling Technologies and Circular Economy Initiatives to Drive Excellent Opportunities

Advanced recycling technologies can enhance the quality and purity of recycled plastics. This is crucial for manufacturers who require consistent and high-quality materials for their products. High-quality recycled plastics can be used in a wider range of applications or including those that demand strict performance and safety standards. Moreover, with improved sorting, cleaning, and processing techniques, it is becoming possible to recycle a broader range of plastic types. This means that previously non-recyclable plastics can now be processed and reused, reducing the overall plastic waste burden on the environment. Moreover, as the quality of recycled plastics improves, manufacturers can use them as alternatives to virgin plastics. This not only reduces the demand for new plastic production but also helps decrease the environmental impact associated with extracting and processing fossil fuels. Furthermore, the production of recycled plastics generally has a lower carbon footprint compared to virgin plastics. Recycling requires less energy and resources than producing plastics from scratch, resulting in fewer greenhouse gas emissions. Circular economy initiatives encourage the development of new technologies and processes for recycling and reusing plastics. This can drive innovation in areas such as plastic sorting, cleaning, and processing methods, leading to more efficient and effective recycling practices.

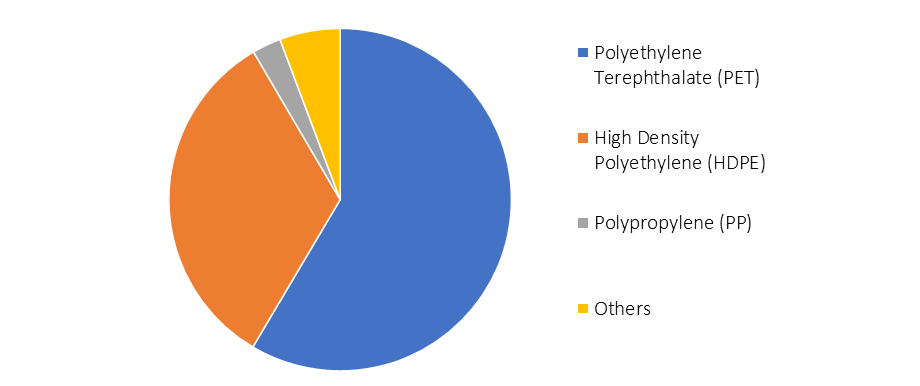

Global Recycled Plastics Market Share, by Type, 2022

Source: Research Dive Analysis

The polyethylene terephthalate (PET) sub-segment accounted for the highest market share in 2022. With increasing awareness about plastic pollution and environmental degradation, there is a growing demand for sustainable and eco-friendly materials. Recycled PET offers a more environmentally friendly option compared to virgin PET as it reduces the need for new plastic production and helps divert plastic waste from landfills and oceans. Moreover, many governments and regulatory bodies around the world are implementing stricter regulations and targets to reduce plastic waste and increase recycling rates. This often involves encouraging or mandating the use of recycled plastics in various applications, including PET. These regulations drive the demand for recycled PET as companies strive to meet these requirements. Advances in recycling technologies have made it possible to process and purify recycled PET to a quality comparable to virgin PET. Improved recycling techniques contribute to the availability of high-quality recycled PET, making it more attractive to manufacturers. The PET segment in the recycled plastics market is driven by a combination of environmental concerns, regulatory actions, market demand for sustainable materials, technological advancements, and various initiatives focused on circular economy principles and corporate sustainability.

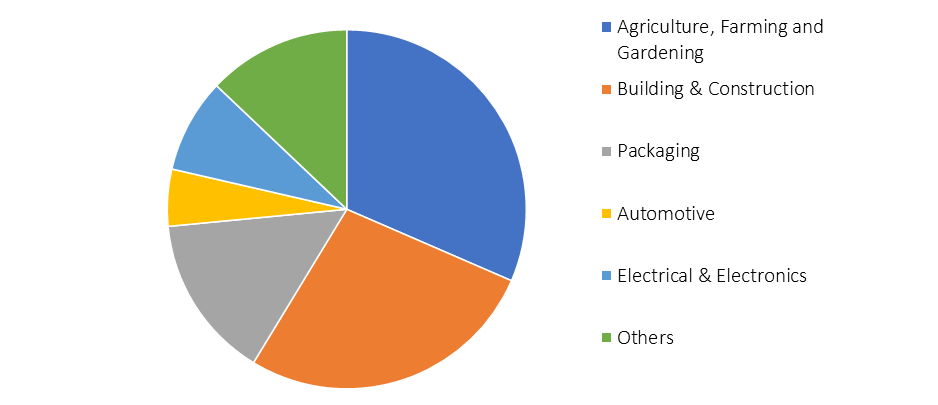

Global Recycled Plastics Market Share by End-Use Industry, 2022

Source: Research Dive Analysis

The agriculture, farming & gardening sub-segment accounted for the highest market share in 2022. The agricultural sector often uses a significant number of plastic materials for applications such as mulching, irrigation systems, greenhouse covers, and more. However, the disposal of traditional plastics can lead to pollution and environmental damage. Using recycled plastics helps address these concerns by reducing the demand for new plastic production and minimizing plastic waste in landfills and ecosystems. Moreover, using recycled plastics in agricultural and gardening applications can enhance a brand's image and reputation, showing a commitment to sustainability. Many consumers and businesses prefer to support environmentally responsible practices which can lead to increased customer loyalty and market share. Furthermore, using recycled plastics in agriculture and gardening can help conserve natural resources. By diverting plastic waste from landfills and incorporating it into production processes, the demand for virgin plastic materials can be reduced, leading to decreased resource consumption. The circular economy model aims to reduce waste and make the most of the existing resources. Incorporating recycled plastics into agricultural applications supports this concept by extending the life cycle of plastics and reducing the need for new plastic production.

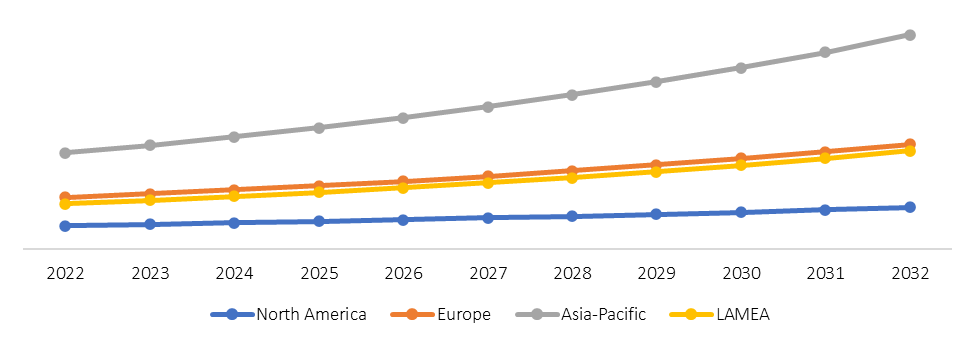

Global Recycled Plastics Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Asia-Pacific recycled plastics market generated the highest revenue in 2022. The Asia-Pacific region is a hub for manufacturing and consumption of various plastic products from packaging to consumer goods. This high demand for plastic creates a substantial amount of plastic waste, leading to a need for efficient recycling solutions. Moreover, increasing concern about plastic pollution and its impact on the environment has led to greater awareness and demand for sustainable practices, including recycling. Governments, businesses, and consumers alike have been pushing for more environmentally friendly alternatives, boosting the demand for recycled plastics. Moreover, many countries in the Asia-Pacific region were implementing stricter regulations and policies aimed at reducing plastic waste and promoting recycling. These regulations often include mandates for higher levels of recycled content in products, waste management targets, and restrictions on single-use plastics. Furthermore, advances in recycling technologies have made it more feasible and cost-effective to process and recycle different types of plastics. These technologies include improved sorting methods, better processing techniques, and innovative ways to reuse recycled plastics.

Competitive Scenario in the Global Recycled Plastics Market

Investment and agreement are common strategies followed by major market players. In April 2022, Faurecia, a company under the FORVIA Group, and Veolia entered into a collaborative Research and Cooperation Agreement. Their goal is to work together on creating new and advanced materials for car interior components. The primary aim of this collaboration is to incorporate an average of 30% recycled materials into these components by the year 2026. This partnership is focused on expediting the adoption of sustainable solutions in Europe, particularly in instrument panels, door panels, and center consoles. Veolia is set to initiate the production of these secondary raw materials at their existing recycling facilities in France, commencing in 2024.

Source: Research Dive Analysis

Some of the leading recycled plastics market players are KW Plastics, Veolia, Green Line Polymers, Custom Polymers, Clear Path Recycling, B. Schoenberg & Co., Jayplas, Plastipak Holdings, Ultra Poly Corporation, and Joes Plastics Inc.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Type |

|

| Segmentation by End-use Industry |

|

| Key Companies Profiled |

|

Q1. What is the size of the global recycled plastics market?

A. The size of the global recycled plastics market was over $66,730.000 million in 2022 and is projected to reach $141,942.100 million by 2032

Q2. Which are the major companies in the recycled plastics market?

A. KW Plastics, Veolia, and Green Line Polymers are some of the key players in the global recycled plastics market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. The Asia-Pacific region possesses great investment opportunities for investors in the future

Q4. What will be the growth rate of the Asia-Pacific recycled plastics market?

A. Asia-Pacific recycled plastics market is anticipated to grow at 8.4% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market

Q6. Which companies are investing more on R&D practices?

A. Custom Polymers, B. Schoenberg & Co., and Plastipak Holdings are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global recycled plastics market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive rivalry intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on recycled plastics market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Recycled Plastics Market Analysis, by Type

5.1. Overview

5.2. Polyethylene Terephthalate (PET)

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. High Density Polyethylene (HDPE)

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. Polypropylene (PP)

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2. Market size analysis, by region, 2022-2032

5.4.3. Market share analysis, by country, 2022-2032

5.5. Others

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2. Market size analysis, by region, 2022-2032

5.5.3. Market share analysis, by country, 2022-2032

5.6. Research Dive Exclusive Insights

5.6.1. Market attractiveness

5.6.2. Competition heatmap

6. 5. Recycled Plastics Market Analysis, by End-use Industry

6.1. Agriculture, Farming & Gardening

6.1.1. Definition, key trends, growth factors, and opportunities

6.1.2. Market size analysis, by region, 2022-2032

6.1.3. Market share analysis, by country, 2022-2032

6.2. Building & Construction

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Packaging

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2022-2032

6.3.3. Market share analysis, by country, 2022-2032

6.4. Automotive

6.4.1. Definition, key trends, growth factors, and opportunities

6.4.2. Market size analysis, by region, 2022-2032

6.4.3. Market share analysis, by country, 2022-2032

6.5. Electrical & Electronics

6.5.1. Definition, key trends, growth factors, and opportunities

6.5.2. Market size analysis, by region, 2022-2032

6.5.3. Market share analysis, by country, 2022-2032

6.6. Others

6.6.1. Definition, key trends, growth factors, and opportunities

6.6.2. Market size analysis, by region, 2022-2032

6.6.3. Market share analysis, by country, 2022-2032

6.7. Research Dive Exclusive Insights

6.7.1. Market attractiveness

6.7.2. Competition heatmap

7. Recycled Plastics Market, by Region

7.1. North America

7.1.1. U.S.

7.1.1.1. Market size analysis, by Type, 2022-2032

7.1.1.2. Market size analysis, by End-use Industry, 2022-2032

7.1.2. Canada

7.1.2.1. Market size analysis, by Type, 2022-2032

7.1.2.2. Market size analysis, by End-use Industry, 2022-2032

7.1.3. Mexico

7.1.3.1. Market size analysis, by Type, 2022-2032

7.1.3.2. Market size analysis, by End-use Industry, 2022-2032

7.1.4. Research Dive Exclusive Insights

7.1.4.1. Market attractiveness

7.1.4.2. Competition heatmap

7.2. Europe

7.2.1. Germany

7.2.1.1. Market size analysis, by Type, 2022-2032

7.2.1.2. Market size analysis, by End-use Industry, 2022-2032

7.2.2. UK

7.2.2.1. Market size analysis, by Type, 2022-2032

7.2.2.2. Market size analysis, by End-use Industry, 2022-2032

7.2.3. France

7.2.3.1. Market size analysis, by Type, 2022-2032

7.2.3.2. Market size analysis, by End-use Industry, 2022-2032

7.2.4. Spain

7.2.4.1. Market size analysis, by Type, 2022-2032

7.2.4.2. Market size analysis, by End-use Industry, 2022-2032

7.2.5. Italy

7.2.5.1. Market size analysis, by Type, 2022-2032

7.2.5.2. Market size analysis, by End-use Industry, 2022-2032

7.2.6. Rest of Europe

7.2.6.1. Market size analysis, by Type, 2022-2032

7.2.6.2. Market size analysis, by End-use Industry, 2022-2032

7.2.7. Research Dive Exclusive Insights

7.2.7.1. Market attractiveness

7.2.7.2. Competition heatmap

7.3. Asia-Pacific

7.3.1. China

7.1.1.1. Market size analysis, by Type, 2022-2032

7.1.1.2. Market size analysis, by End-use Industry, 2022-2032

7.1.2. Japan

7.1.2.1. Market size analysis, by Type, 2022-2032

7.1.2.2. Market size analysis, by End-use Industry, 2022-2032

7.1.3. India

7.1.3.1. Market size analysis, by Type, 2022-2032

7.1.3.2. Market size analysis, by End-use Industry, 2022-2032

7.1.4. Australia

7.1.4.1. Market size analysis, by Type, 2022-2032

7.1.4.2. Market size analysis, by End-use Industry, 2022-2032

7.1.5. South Korea

7.1.5.1. Market size analysis, by Type, 2022-2032

7.1.5.2. Market size analysis, by End-use Industry, 2022-2032

7.1.6. Rest of Asia-Pacific

7.1.6.1. Market size analysis, by Type, 2022-2032

7.1.6.2. Market size analysis, by End-use Industry, 2022-2032

7.1.7. Research Dive Exclusive Insights

7.1.7.1. Market attractiveness

7.1.7.2. Competition heatmap

7.2. LAMEA

7.2.1. Brazil

7.2.1.1. Market size analysis, by Type, 2022-2032

7.2.1.2. Market size analysis, by End-use Industry, 2022-2032

7.2.2. Saudi Arabia

7.2.2.1. Market size analysis, by Type, 2022-2032

7.2.2.2. Market size analysis, by End-use Industry, 2022-2032

7.2.3. UAE

7.2.3.1. Market size analysis, by Type, 2022-2032

7.2.3.2. Market size analysis, by End-use Industry, 2022-2032

7.2.4. South Africa

7.2.4.1. Market size analysis, by Type, 2022-2032

7.2.4.2. Market size analysis, by End-use Industry, 2022-2032

7.2.5. Rest of LAMEA

7.2.5.1. Market size analysis, by Type, 2022-2032

7.2.5.2. Market size analysis, by End-use Industry, 2022-2032

7.2.6. Research Dive Exclusive Insights

7.2.6.1. Market attractiveness

7.2.6.2. Competition heatmap

8. Competitive Landscape

8.1. Top winning strategies, 2022

8.1.1. By strategy

8.1.2. By year

8.2. Strategic overview

8.3. Market share analysis, 2022

9. Company Profiles

9.1. KW Plastics

9.1.1. Overview

9.1.2. Business segments

9.1.3. Product portfolio

9.1.4. Financial performance

9.1.5. Recent developments

9.1.6. SWOT analysis

9.2. Veolia

9.2.1. Overview

9.2.2. Business segments

9.2.3. Product portfolio

9.2.4. Financial performance

9.2.5. Recent developments

9.2.6. SWOT analysis

9.3. Green Line Polymers

9.3.1. Overview

9.3.2. Business segments

9.3.3. Product portfolio

9.3.4. Financial performance

9.3.5. Recent developments

9.3.6. SWOT analysis

9.4. Custom Polymers

9.4.1. Overview

9.4.2. Business segments

9.4.3. Product portfolio

9.4.4. Financial performance

9.4.5. Recent developments

9.4.6. SWOT analysis

9.5. Clear Path Recycling

9.5.1. Overview

9.5.2. Business segments

9.5.3. Product portfolio

9.5.4. Financial performance

9.5.5. Recent developments

9.5.6. SWOT analysis

9.6. B. Schoenberg & Co.

9.6.1. Overview

9.6.2. Business segments

9.6.3. Product portfolio

9.6.4. Financial performance

9.6.5. Recent developments

9.6.6. SWOT analysis

9.7. Jayplas

9.7.1. Overview

9.7.2. Business segments

9.7.3. Product portfolio

9.7.4. Financial performance

9.7.5. Recent developments

9.7.6. SWOT analysis

9.8. Plastipak Holdings

9.8.1. Overview

9.8.2. Business segments

9.8.3. Product portfolio

9.8.4. Financial performance

9.8.5. Recent developments

9.8.6. SWOT analysis

9.9. Ultra Poly Corporation

9.9.1. Overview

9.9.2. Business segments

9.9.3. Product portfolio

9.9.4. Financial performance

9.9.5. Recent developments

9.9.6. SWOT analysis

9.10. Joes Plastics Inc.

9.10.1. Overview

9.10.2. Business segments

9.10.3. Product portfolio

9.10.4. Financial performance

9.10.5. Recent developments

9.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com