Industrial Sludge Treatment Chemical Market Report

RA00065

Industrial Sludge Treatment Chemical Market, by Type (Flocculants, Disinfectants, Coagulants, Others), Sludge type (Activated Sludge, Primary Sludge, Mixed Sludge, Others), Process Treatment (Dewatering & Drying Treatment, Conditioning & Stabilization Treatment, Thickening Treatment, Digestion Treatment), End Use (Pulp & paper, Oil & gas, Personal care & chemicals, Metal processing, Food & beverage, Paints & coatings, Mining, Automotive, Others), Regional Analysis (North America, Europe, Asia-Pacific, LAMEA): Global Opportunity Analysis and Industry Forecast, 2019–2026

Update Available On-Demand

Global Industrial Sludge Treatment Chemical Market Overview 2026:

The industrial sludge treatment chemical market forecast will be $7,727.7 million by 2026, at a 5.9% CAGR, and has been increasing from $4,885.2 million in 2018. Asia-Pacific market is growing at a rate of 6.3% and is expected to garner $2,287.4 million by 2026. North American region dominated the overall industrial sludge treatment chemical market in 2018, and anticipated to account for $2,194.7 million by 2026.

Industrial sludge treatment chemicals are used to remove harmful chemicals and substances from the sludge generating from various industries including manufacturing industry, pulp & paper, metal processing and others. These effluents contain micro-organisms, waste water and heavy metals and this sludge should not be dumped in the water bodies and lands. In order to treat industrial sludge, particular type of chemicals is required on the basis of type of effluent present in the sludge.

Key Driving Force Of The Industrial Sludge Treatment Chemical Market:

Growing industrialization & urbanization and increasing demands for working environment are giving significant boost to the growth of global industrial sludge treatment chemical market

Growing requirement of industrial sludge removal and the rapid increase of end users due to industrialization are significant factors for the growth of the industrial sludge treatment chemical market. In manufacturing and production industries, the wastewater treatment process produces heavy amounts of industrial sludge; it contains significant concentrations of heavy metals, micro-organisms and hazardous chemical constituents that are considered as pollutants to the environment. Such pollutants can be minimized through converting wastewater into sludge. The generated sludge is further subjected to a process to reduce the volume and neutralize the pH. The usage of these chemicals used for pH neutralization will boost the industrial sludge treatment chemicals market growth over forecast period. Residual waste water from research laboratories and other industries can be dangerous to people and it release pollutants into the atmosphere. These dangerous residual wastes require chemical treatment to remove the toxins. These sludge treatment chemicals reduce the volume of the wastes and breaks down harmful chemical constituents; this is expected to drive the industrial sludge treatment market growth.

Market Restraints:

Cost of the sludge treatment is a significant restraint factor for the growth of Industrial sludge treatment chemical market

The global industrial sludge treatment chemical market is majorly restrained by the cost associated with the treatment methods. In addition, developments in the waste water treatment methods to reduce wastewater by certain companies are resulting in less sludge being generated, hampering the growth of the market.

Investment Opportunities for the Growth of Global Market:

Converting sludge into agricultural fertilizer will be a significant investment opportunity for the growth of industrial sludge treatment chemical market

Sludge may contain nitrogen, potash and phosphorous, which are important nutrients for plants and play a major role in plants growth. In recent times, researchers have found that sludge can be converted into agricultural fertilizers; this concept will be creating numerous growth opportunities for the industrial sludge treatment chemical market in the near future.

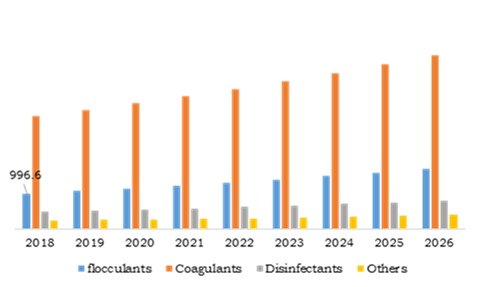

Industrial Sludge Treatment Chemical Market, by Type

Flocculants type is predicted to be most lucrative till the end of 2026

Source: Research Dive Analysis

Flocculants type segment is accounted for $996.6 million in 2018 and is projected to experience significant growth during the forecast time. The flocculants are widely used for the treatment process of isolation of insoluble pollutants. This is the agglomeration of destabilized particles into large size particles, which are easy to separate by simple sedimentation; due to the adoption of agglomeration process, there is an increase in the demand of flocculants from industries such as food & beverages, paper & pulp and production industries. The market for flocculants type is projected to account for $1,684.6 million during the forecast period. Coagulants type held the highest industrial sludge treatment chemical market size in 2018, it is accounted for $3,170.5 million and is projected to account for $4,868.4 million by 2026. Coagulation is the chemical process of destabilization of colloids by addition of chemical substances, that neutralize the charge by vigorous mixing., These coagulants are majorly used in the paper & pulp industry.

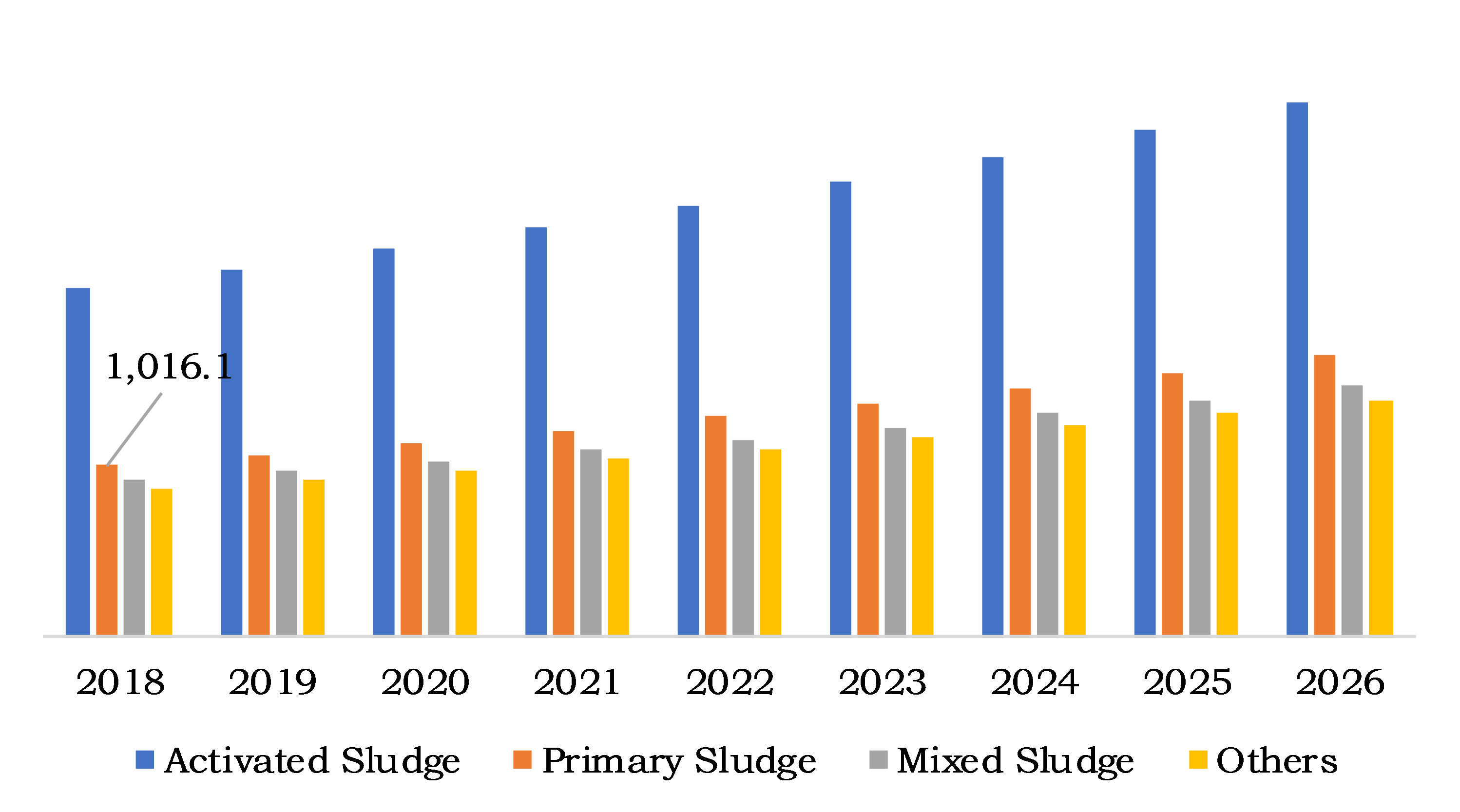

Industrial Sludge Treatment Chemical Market, by Sludge Type

Primary sludge type is predicted to be most lucrative till the end of 2026

Source: Research Dive Analysis

Primary treatment type is anticipated to experience noteworthy growth over forecast time period and is projected to account for $1,669.1 million by 2026 and is increasing from $1,016.1 million in 2018. This treatment eliminates most of the pollutants like organic phosphorus, heavy metals and some organic nitrogen. Activated sludge type held the highest industrial sludge treatment chemical market size and generated a revenue of $2,066.4 million in 2018. The activated sludge is an aeration process that involves conversion of soluble organic matter into biological flocculants and their removal as secondary sludge. The market for activated sludge type is expected to register $3,160.6 million during the projected period.

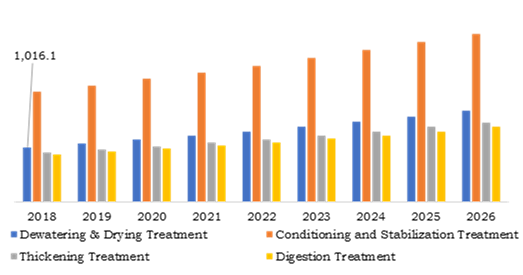

Industrial Sludge Treatment Chemical Market, by Process Treatment

Dewatering & Drying process treatment is predicted to be most lucrative till the end of 2026

Source: Research Dive Analysis

Dewatering & drying treatment market will experience substantial growth in the coming years, due their increasing usage in food & beverage and chemical industries. This process is simple gravitation settling method.Due to adoption of this method, the market is projected to reach $1,700.1 million by 2026 and is increasing from $1,016.1 million in 2018. Conditioning & stabilization treatment led the industrial sludge treatment chemical market share of 42.3% in 2018 and is accounted for $2,066.4 million and is expected to reach $3,145.1 million, at a CAGR of 5.4% over the forecast period. The wide usage of conditioning & stabilization treatment in end use industries to remove pathogens present in the sludge is expected to increase the growth of the market.

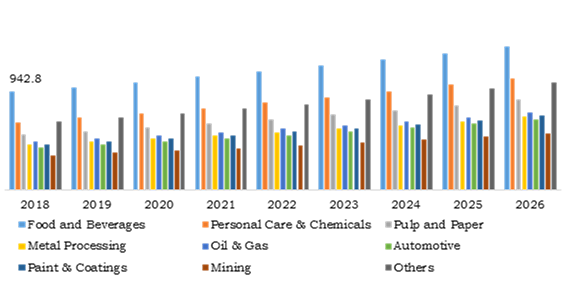

Industrial sludge treatment chemical market, by End use

Food & Beverages segment generated highest amount of revenue and will grow at a CAGR of 4.8% during the projected period

Source: Research Dive Analysis

Personal care & chemical segment will witness a noteworthy growth over the forecast period and is accounted for second highest market size in 2018, it was generated $651.2 million. This is majorly due to increasing the number of chemical production plants that are generating huge amounts of waste water is directly impacting the use of sludge treatment chemicals. In addition, increasing the usage of personal care products is further expected to drive the market growth. Food & beverage segment held majority of the industrial sludge treatment chemical market share which was of 19.3% and is accounted for $942.8 million in 2018, projecting to reach $1,074.1 million by 2026. The food & beverage industry generates massive amounts of waste water compared with other industries. This will lead to drive the demands of the industrial sludge treatment chemical market in food & beverages industry during the coming years.

Industrial Sludge Treatment Chemical Market, by Region:

Asia-Pasific Industrial Sludge Treatment Chemical Market Summary 2026:

Asia-Pacific region will have enormous opportunities for the market investors to grow over the coming years

The Asia Pacific market is projected to grow fast and is anticipated to capture substantial revenue, producing tremendous opportunities over the forecast period. The industrial sludge treatment chemical market for Asia-Pacific is growing at a rate of 6.3% and is expected to account $2,287.4 million by 2026, increasing from $1,406.9 million in 2018. This growth is attributed to the increase in the number of manufacturing and production industries producing large quantities of sludge across.

North America Industrial Sludge Treatment Chemical Market Outlook 2026:

North America region dominated the overall industrial sludge treatment chemical market in 2018, it is accounted for $1,470.4 million and is anticipated to account for $2,194.7 million by 2026. This dominance is due to existence of well-established waste water treatment plants along with industrial revolution in the North America region.

Key Participants in Global Industrial Sludge Treatment Chemical Market:

Product development and joint ventures are the most common strategies followed by the market players

Source: Research Dive Analysis

Top industrial sludge treatment chemical market players include The Dow Chemical Company, Accepta Water Treatment, Kamira OYJ, Kurita Water Industries Ltd., BASF SE, Amcon Inc., Ecolab Incorporated, GE Water & Process Technologies, Hubbard-Hall Inc., Beckart Environment, and Ovivo Inc. among others. These market players are concentrating on the new product launches as the important developing strategies to increase their market size in the global industrial sludge treatment chemical industry. For instance, in 2019, Kurita Water Industries Ltd., delivered a demonstration on “Japanese Experiment Module-Kibo”, which is elemental technology and treatment methods for water recycling technology system at International Space Station (ISS).

| Aspect | Particulars |

| Historical Market Estimations | 2016-2018 |

| Base Year for Market Estimation | 2018 |

| Forecast timeline for Market Projection | 2019-2026 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Sludge Type |

|

| Segmentation by Process Treatment |

|

| Segmentation by End Use |

|

| Key Countries Covered | U.S., Canada, Germany, France, Spain, Russia, Japan, China, India, South Korea, Australia, Brazil, and Saudi Arabia |

| Key Companies Profiled |

|

Source: Research Dive Analysis

Q1. What is the size of industrial sludge treatment chemical market?

A. The global industrial sludge treatment chemical market size was over $4,885.2 million in 2018, and is further anticipated to reach $7,727.7 million by 2026.

Q2. Which are the leading companies in the industrial sludge treatment chemical market?

A. The Dow Chemical Company, Kurita Water Industries Ltd., BASF SE and Beckart Environment are some of the key players in the global industrial sludge treatment chemical market.

Q3. Which region possesses greater investment opportunities in the coming future?

A. Asia-Pacific possess great investment opportunities for the investors to witness the most promising growth in the coming years.

Q4. What is the growth rate of Asia-Pacific Market?

A. Asia Pacific industrial sludge treatment chemical market is projected to grow at 6.3% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Product development, and joint ventures are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. The Dow Chemical Company, Kurita Water Industries Ltd., and BASF SE are investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.4.1. Assumptions

1.4.2. Forecast parameters

1.5. Data sources

1.5.1. Primary

1.5.2. Secondary

2. Executive Summary

2.1. 360° summary

2.2. Type trends

2.3. Sludge type trends

2.4. Process treatment trends

2.5. End use trends

3. Market Overview

3.1. Market segmentation & definitions

3.2. key takeaways

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.3. Porter’s five forces analysis

3.3.1. Bargaining power of consumers

3.3.2. Bargaining power of suppliers

3.3.3. Threat of new entrants

3.3.4. Threat of substitutes

3.3.5. Competitive rivalry in the market

3.4. Market dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Technology landscape

3.6. Regulatory landscape

3.7. Patent landscape

3.8. Pricing overview

3.8.1. By type

3.8.2. By sludge type

3.8.3. By treatment process

3.8.4. By end use

3.8.5. By region

3.9. Market value chain analysis

3.9.1. Stress point analysis

3.9.2. Distribution channel analysis

3.9.3. Operating vendors

3.9.3.1. Raw material suppliers

3.9.3.2. Product manufacturers

3.9.3.3. Product distributors

3.10. Strategic overview

4. Industrial Sludge Treatment Chemical Market, by Type

4.1. Flocculants

4.1.1. Market size and forecast, by region, 2016-2028

4.1.2. Comparative market share analysis, 2018 & 2028

4.2. Disinfectants

4.2.1. Market size and forecast, by region, 2016-2028

4.2.2. Comparative market share analysis, 2018 & 2028

4.3. Coagulants

4.3.1. Market size and forecast, by region, 2016-2028

4.3.2. Comparative market share analysis, 2018 & 2028

4.4. Others

4.4.1. Market size and forecast, by region, 2016-2028

4.4.2. Comparative market share analysis, 2018 & 2028

4.4.3. Biocides

4.4.3.1. Market size and forecast, by region, 2016-2028

4.4.3.2. Comparative market share analysis, 2018 & 2028

4.4.4. Defoamers

4.4.4.1. Market size and forecast, by region, 2016-2028

4.4.4.2. Comparative market share analysis, 2018 & 2028

4.4.5. Others

4.4.5.1. Market size and forecast, by region, 2016-2028

4.4.5.2. Comparative market share analysis, 2018 & 2028

5. Industrial Sludge Treatment Chemical Market, by Sludge Type

5.1. Activated sludge

5.1.1. Market size and forecast, by region, 2016-2028

5.1.2. Comparative market share analysis, 2018 & 2028

5.2. Primary sludge

5.2.1. Market size and forecast, by region, 2016-2028

5.2.2. Comparative market share analysis, 2018 & 2028

5.3. Mixed sludge

5.3.1. Market size and forecast, by region, 2016-2028

5.3.2. Comparative market share analysis, 2018 & 2028

5.4. Others

5.4.1. Market size and forecast, by region, 2016-2028

5.4.2. Comparative market share analysis, 2018 & 2028

6. Industrial Sludge Treatment Chemical Market, by Process Treatment

6.1. Dewatering & Drying Treatment

6.1.1. Market size and forecast, by region, 2016-2028

6.1.2. Comparative market share analysis, 2018 & 2028

6.2. Conditioning and Stabilization Treatment

6.2.1. Market size and forecast, by region, 2016-2028

6.2.2. Comparative market share analysis, 2018 & 2028

6.3. Thickening Treatment

6.3.1. Market size and forecast, by region, 2016-2028

6.3.2. Comparative market share analysis, 2018 & 2028

6.4. Digestion Treatment

6.4.1. Market size and forecast, by region, 2016-2028

6.4.2. Comparative market share analysis, 2018 & 2028

7. Industrial Sludge Treatment Chemical Market, by End Use

7.1. Pulp & paper

7.1.1. Market size and forecast, by region, 2016-2028

7.1.2. Comparative market share analysis, 2018 & 2028

7.2. Oil & gas

7.2.1. Market size and forecast, by region, 2016-2028

7.2.2. Comparative market share analysis, 2018 & 2028

7.3. Personal care & chemicals

7.3.1. Market size and forecast, by region, 2016-2028

7.3.2. Comparative market share analysis, 2018 & 2028

7.4. Metal processing

7.4.1. Market size and forecast, by region, 2016-2028

7.4.2. Comparative market share analysis, 2018 & 2028

7.5. Food & beverages

7.5.1. Market size and forecast, by region, 2016-2028

7.5.2. Comparative market share analysis, 2018 & 2028

7.6. Paints & coatings

7.6.1. Market size and forecast, by region, 2016-2028

7.6.2. Comparative market share analysis, 2018 & 2028

7.7. Mining

7.7.1. Market size and forecast, by region, 2016-2028

7.7.2. Comparative market share analysis, 2018 & 2028

7.8. Automotive

7.8.1. Market size and forecast, by region, 2016-2028

7.8.2. Comparative market share analysis, 2018 & 2028

7.9. Others

7.9.1. Market size and forecast, by region, 2016-2028

7.9.2. Comparative market share analysis, 2018 & 2028

8. Industrial Sludge Treatment Chemical Market, by Region

8.1. North America

8.1.1. Market size and forecast, by type, 2016-2028

8.1.2. Market size and forecast, by sludge type, 2016-2028

8.1.3. Market size and forecast, by process treatment, 2016-2028

8.1.4. Market size and forecast, by end use, 2016-2028

8.1.5. Market size and forecast, by country, 2016-2028

8.1.6. Comparative market share analysis, 2018 & 2028

8.1.7. U.S.

8.1.7.1. Market size and forecast, by type, 2016-2028

8.1.7.2. Market size and forecast, by sludge type, 2016-2028

8.1.7.3. Market size and forecast, by process treatment, 2016-2028

8.1.7.4. Market size and forecast, by end use, 2016-2028

8.1.7.5. Comparative market share analysis, 2018 & 2028

8.1.8. Canada

8.1.8.1. Market size and forecast, by type, 2016-2028

8.1.8.2. Market size and forecast, by sludge type, 2016-2028

8.1.8.3. Market size and forecast, by process treatment, 2016-2028

8.1.8.4. Market size and forecast, by end use, 2016-2028

8.1.8.5. Comparative market share analysis, 2018 & 2028

8.1.9. Mexico

8.1.9.1. Market size and forecast, by type, 2016-2028

8.1.9.2. Market size and forecast, by sludge type, 2016-2028

8.1.9.3. Market size and forecast, by process treatment, 2016-2028

8.1.9.4. Market size and forecast, by end use, 2016-2028

8.1.9.5. Comparative market share analysis, 2018 & 2028

8.2. Europe

8.2.1. Market size and forecast, by type, 2016-2028

8.2.2. Market size and forecast, by sludge type, 2016-2028

8.2.3. Market size and forecast, by process treatment, 2016-2028

8.2.4. Market size and forecast, by end use, 2016-2028

8.2.5. Market size and forecast, by country, 2016-2028

8.2.6. Comparative market share analysis, 2018 & 2028

8.2.7. UK

8.2.7.1. Market size and forecast, by type, 2016-2028

8.2.7.2. Market size and forecast, by sludge type, 2016-2028

8.2.7.3. Market size and forecast, by process treatment, 2016-2028

8.2.7.4. Market size and forecast, by end use, 2016-2028

8.2.7.5. Comparative market share analysis, 2018 & 2028

8.2.8. Germany

8.2.8.1. Market size and forecast, by type, 2016-2028

8.2.8.2. Market size and forecast, by sludge type, 2016-2028

8.2.8.3. Market size and forecast, by process treatment, 2016-2028

8.2.8.4. Market size and forecast, by end use, 2016-2028

8.2.8.5. Comparative market share analysis, 2018 & 2028

8.2.9. France

8.2.9.1. Market size and forecast, by type, 2016-2028

8.2.9.2. Market size and forecast, by sludge type, 2016-2028

8.2.9.3. Market size and forecast, by process treatment, 2016-2028

8.2.9.4. Market size and forecast, by end use, 2016-2028

8.2.9.5. Comparative market share analysis, 2018 & 2028

8.2.10. Spain

8.2.10.1. Market size and forecast, by type, 2016-2028

8.2.10.2. Market size and forecast, by sludge type, 2016-2028

8.2.10.3. Market size and forecast, by process treatment, 2016-2028

8.2.10.4. Market size and forecast, by end use, 2016-2028

8.2.10.5. Comparative market share analysis, 2018 & 2028

8.2.11. Italy

8.2.11.1. Market size and forecast, by type, 2016-2028

8.2.11.2. Market size and forecast, by sludge type, 2016-2028

8.2.11.3. Market size and forecast, by process treatment, 2016-2028

8.2.11.4. Market size and forecast, by end use, 2016-2028

8.2.11.5. Comparative market share analysis, 2018 & 2028

8.2.12. Rest of Europe

8.2.12.1. Market size and forecast, by type, 2016-2028

8.2.12.2. Market size and forecast, by sludge type, 2016-2028

8.2.12.3. Market size and forecast, by process treatment, 2016-2028

8.2.12.4. Market size and forecast, by end use, 2016-2028

8.2.12.5. Comparative market share analysis, 2018 & 2028

8.3. Asia Pacific

8.3.1. Market size and forecast, by type, 2016-2028

8.3.2. Market size and forecast, by sludge type, 2016-2028

8.3.3. Market size and forecast, by process treatment, 2016-2028

8.3.4. Market size and forecast, by end use, 2016-2028

8.3.5. Market size and forecast, by country, 2016-2028

8.3.6. Comparative market share analysis, 2018 & 2028

8.3.7. China

8.3.7.1. Market size and forecast, by type, 2016-2028

8.3.7.2. Market size and forecast, by sludge type, 2016-2028

8.3.7.3. Market size and forecast, by process treatment, 2016-2028

8.3.7.4. Market size and forecast, by end use, 2016-2028

8.3.7.5. Comparative market share analysis, 2018 & 2028

8.3.8. Japan

8.3.8.1. Market size and forecast, by type, 2016-2028

8.3.8.2. Market size and forecast, by sludge type, 2016-2028

8.3.8.3. Market size and forecast, by process treatment, 2016-2028

8.3.8.4. Market size and forecast, by end use, 2016-2028

8.3.8.5. Comparative market share analysis, 2018 & 2028

8.3.9. India

8.3.9.1. Market size and forecast, by type, 2016-2028

8.3.9.2. Market size and forecast, by sludge type, 2016-2028

8.3.9.3. Market size and forecast, by process treatment, 2016-2028

8.3.9.4. Market size and forecast, by end use, 2016-2028

8.3.9.5. Comparative market share analysis, 2018 & 2028

8.3.10. Australia

8.3.10.1. Market size and forecast, by type, 2016-2028

8.3.10.2. Market size and forecast, by sludge type, 2016-2028

8.3.10.3. Market size and forecast, by process treatment, 2016-2028

8.3.10.4. Market size and forecast, by end use, 2016-2028

8.3.10.5. Comparative market share analysis, 2018 & 2028

8.3.11. South Korea

8.3.11.1. Market size and forecast, by type, 2016-2028

8.3.11.2. Market size and forecast, by sludge type, 2016-2028

8.3.11.3. Market size and forecast, by process treatment, 2016-2028

8.3.11.4. Market size and forecast, by end use, 2016-2028

8.3.11.5. Comparative market share analysis, 2018 & 2028

8.3.12. Rest of Asia Pacific

8.3.12.1. Market size and forecast, by type, 2016-2028

8.3.12.2. Market size and forecast, by sludge type, 2016-2028

8.3.12.3. Market size and forecast, by process treatment, 2016-2028

8.3.12.4. Market size and forecast, by end use, 2016-2028

8.3.12.5. Comparative market share analysis, 2018 & 2028

8.4. LAMEA

8.4.1. Market size and forecast, by type, 2016-2028

8.4.2. Market size and forecast, by sludge type, 2016-2028

8.4.3. Market size and forecast, by process treatment, 2016-2028

8.4.4. Market size and forecast, by end use, 2016-2028

8.4.5. Market size and forecast, by country, 2016-2028

8.4.6. Comparative market share analysis, 2018 & 2028

8.4.7. Brazil

8.4.7.1. Market size and forecast, by type, 2016-2028

8.4.7.2. Market size and forecast, by sludge type, 2016-2028

8.4.7.3. Market size and forecast, by process treatment, 2016-2028

8.4.7.4. Market size and forecast, by end use, 2016-2028

8.4.7.5. Comparative market share analysis, 2018 & 2028

8.4.8. Saudi Arabia

8.4.8.1. Market size and forecast, by type, 2016-2028

8.4.8.2. Market size and forecast, by sludge type, 2016-2028

8.4.8.3. Market size and forecast, by process treatment, 2016-2028

8.4.8.4. Market size and forecast, by end use, 2016-2028

8.4.8.5. Comparative market share analysis, 2018 & 2028

8.4.9. South Africa

8.4.9.1. Market size and forecast, by type, 2016-2028

8.4.9.2. Market size and forecast, by sludge type, 2016-2028

8.4.9.3. Market size and forecast, by process treatment, 2016-2028

8.4.9.4. Market size and forecast, by end use, 2016-2028

8.4.9.5. Comparative market share analysis, 2018 & 2028

8.4.10. Rest of LAMEA

8.4.10.1. Market size and forecast, by type, 2016-2028

8.4.10.2. Market size and forecast, by sludge type, 2016-2028

8.4.10.3. Market size and forecast, by process treatment, 2016-2028

8.4.10.4. Market size and forecast, by end use, 2016-2028

8.4.10.5. Comparative market share analysis, 2018 & 2028

9. Company Profiles

9.1. The Dow Chemical Company

9.1.1. Business overview

9.1.2. Financial performance

9.1.3. Product portfolio

9.1.4. Recent strategic moves & developments

9.1.5. SWOT analysis

9.2. Accepta Water Treatment

9.2.1. Business overview

9.2.2. Financial performance

9.2.3. Product portfolio

9.2.4. Recent strategic moves & developments

9.2.5. SWOT analysis

9.3. Kamira OYJ

9.3.1. Business overview

9.3.2. Financial performance

9.3.3. Product portfolio

9.3.4. Recent strategic moves & developments

9.3.5. SWOT analysis

9.4. Kurita Water Industries Ltd.

9.4.1. Business overview

9.4.2. Financial performance

9.4.3. Product portfolio

9.4.4. Recent strategic moves & developments

9.4.5. SWOT analysis

9.5. BASF SE

9.5.1. Business overview

9.5.2. Financial performance

9.5.3. Product portfolio

9.5.4. Recent strategic moves & developments

9.5.5. SWOT analysis

9.6. Amcon Inc.

9.6.1. Business overview

9.6.2. Financial performance

9.6.3. Product portfolio

9.6.4. Recent strategic moves & developments

9.6.5. SWOT analysis

9.7. Ecolab Incorporated

9.7.1. Business overview

9.7.2. Financial performance

9.7.3. Product portfolio

9.7.4. Recent strategic moves & developments

9.7.5. SWOT analysis

9.8. GE Water & Process Technologies

9.8.1. Business overview

9.8.2. Financial performance

9.8.3. Product portfolio

9.8.4. Recent strategic moves & developments

9.8.5. SWOT analysis

9.9. Hubbard-Hall Inc.

9.9.1. Business overview

9.9.2. Financial performance

9.9.3. Product portfolio

9.9.4. Recent strategic moves & developments

9.9.5. SWOT analysis

9.10. Beckart Environment

9.10.1. Business overview

9.10.2. Financial performance

9.10.3. Product portfolio

9.10.4. Recent strategic moves & developments

9.10.5. SWOT analysis

9.11. Ovivo Inc.

9.11.1. Business overview

9.11.2. Financial performance

9.11.3. Product portfolio

9.11.4. Recent strategic moves & developments

9.11.5. SWOT analysis

Introduction

Combating Industrial sludge is a major challenge in a huge quotient of chemical industries worldwide. This industrial sludge affects the environment drastically. Environmental initiatives are taken in many countries in a large-scale, which has resulted in firm environmental regulations on industrial wastewater discharge. The operators have looked at installing the industrial wastewater treatment systems to meet their respective local regulations. Safe and secure methods for industrial wastewater disposal hold a huge importance for the environment. This is where industrial sludge treatment chemicals come into existence.

Industrial wastewater treatment is implemented mainly in mining, manufacturing, energy and petrochemical companies, which are struggling to diminish the amount of their liquid discharge into the environment. This process benefits the environment and, most importantly, helps the big companies save money by recycling and re-using large water volumes in their industrial processes.

Major Growth Drivers

Growing industrialization, urbanization, and increasing demands for working environment are giving significant boost to the growth of global industrial sludge treatment chemical market. In manufacturing and production industries, the wastewater treatment process produces heavy amounts of industrial sludge, it contains significant concentrations of heavy metals, micro-organisms and hazardous chemicals constituents and these are considered as pollutants to the environment. Following are the major growth drivers.

- Industrialization

Wastewater effluents work as major contributors to multiple water pollution problems. Research found, most cities of developing countries generate on the average 30–70 mm3 of wastewater per person per year. Owing to the improper wastewater treatment facilities, wastewater and its effluents are often discharged into surface water sources, which are containers for domestic and industrial wastes, resulting to pollution. The poor quality of wastewater effluents is responsible for the degradation of the receiving surface water body. Wastewater effluent should be treated efficiently to avert adverse health risks to the user of surface water resources and the aquatic ecosystem.

- Urbanization

It is well known that population growth and industrial activities are drivers of water quality change. Surface water quality deterioration is a serious problem in several rapidly urbanizing catchments in developing countries. Suitable water management measures, however, may also be included in the urbanization process to mediate water quality deterioration such as installing wastewater infrastructure such as wastewater treatment plant (WWTP) and urban drainage system to increase wastewater treatment capacity.

Recent Developments

In recent years, sewage sludge has become an international topic of importance with numerous conferences and, in the case of the EU, interstate coordinated research and scientific committees focusing on various common problems. This activity reflects the growing realization that while world sludge production is on a relentless growth curve, environmental quality requirements for sludge are becoming increasingly stringent, disposal outlets are decreasing and yet economic pressures still require low-cost solutions to sludge disposal problems.

Future Perspective

According to a report published by Research Dive, the key players of the market include The Dow Chemical Company, Accepta Water Treatment, Kamira OYJ, Kurita Water Industries Ltd., BASF SE, Amcon Inc., Ecolab Incorporated, GE Water & Process Technologies, Hubbard-Hall Inc., Beckart Environment, and Ovivo Inc. among others. These market players are focused on the new product launches as well as the important development strategies to increase their market size in the global industrial sludge treatment chemical industry. In 2019, Kurita Water Industries Ltd. delivered a demonstration on “Japanese Experiment Module-Kibo”, which introduced an elemental technology and other treatment methods for water recycling technology system at International Space Station (ISS). The report also predicts that the market is going to reach $7,727.7 million by 2026, from $4,885.2 million in 2018 at a CAGR of 5.9%.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com