Cosmetic Pigments Market Report

RA06390

Cosmetic Pigments Market by Composition (Inorganic Pigments and Organic Pigments), Type (Surface Treated Pigment, Nano Pigment, Special Effect Pigment, and Others), Application (Facial Makeup, Eye Makeup, Lip Makeup, Hair Dye & Hair Coloring, Nail Care, and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2023-2032

Cosmetic Pigments Overview

Cosmetic pigments are pigments that are opted for the manufacturing of various cosmetics and personal care products to enhance their artistic appearance and give them attractive color. Cosmetic pigments are used in such a manner so that they are safe for use on the skin, hair, nails, and other body parts. These are available in variety of formats and packaging according to consumer need. The two main types of cosmetic pigments are inorganic and organic pigments. Mineral-derived compounds are used to create inorganic pigments, which are prized for their stability and resilience to heat, chemicals, and light. The main inorganic pigments used in cosmetics include titanium dioxide, iron oxides, mica, and ultramarines. The fact that organic pigments are made from carbon-based molecules allows them to produce a wider variety of colors and tints than inorganic pigments do. They are mostly used in cosmetics such as lipsticks, eyeshadow, and other products.

Cosmetic pigments offer benefits such as color stability, opacity & transparency, safety, and others. Cosmetic pigments must be stable in different environments, including exposure to light, heat, and chemicals, to maintain their intended color over time. These pigments must meet safety regulations and be approved for use on the skin. Furthermore, some pigments are opaquer, while some are semi-transparent or transparent. The opaqueness of a pigment influences the intensity of the color and the ability to layer it.

Global Cosmetic Pigments Market Analysis

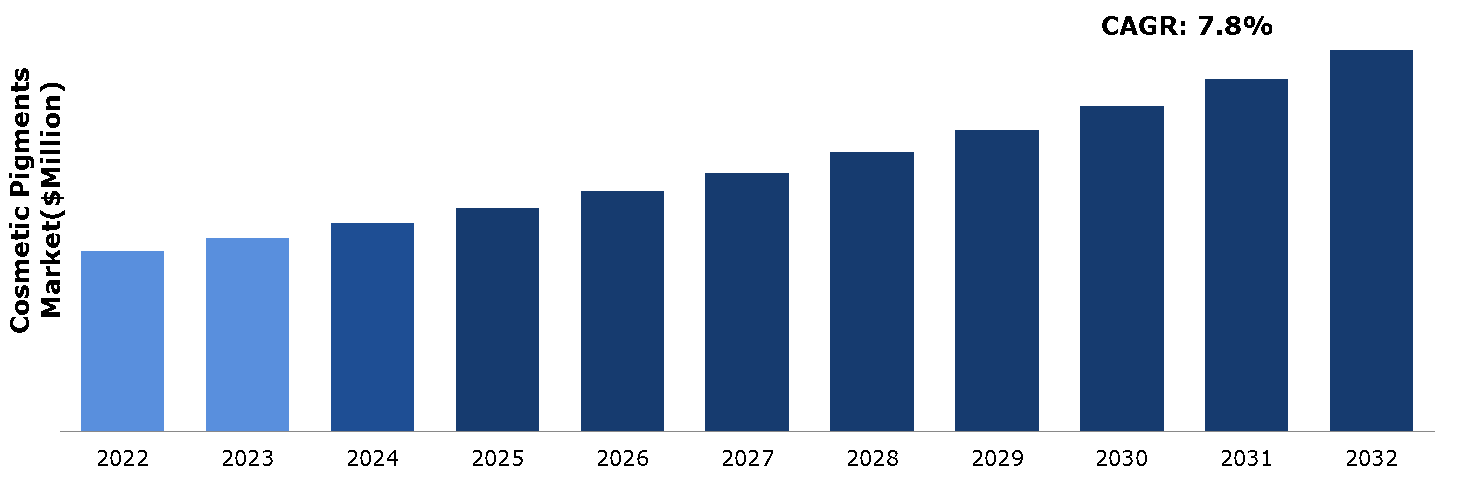

The global cosmetic pigments market size was $2,106.9 million in 2022 and is predicted to grow with a CAGR of 7.8%, by generating a revenue of $4,449.2 million by 2032.

Source: Research Dive Analysis

COVID-19 Impact on Global Cosmetic Pigments Market

Before the COVID-19 pandemic, several such as upgrade to better lifestyles, increasing levels of income, rising concerns over external beauty, and other factors were driving the cosmetic pigments market growth. In addition, the promotional activities of companies now include use of social media platforms such as Instagram, Facebook, and others, to increase engagement with customers. Promotion of products on such platforms is possible with the help of social media influencers.

Since the beginning of the COVID-19 pandemic, the growth of the international cosmetics industry reduced to a great extent. This is because the lockdowns implemented by governments created a shortage of labor which caused manufacturing units of cosmetics to temporarily shut down. Businesses were also forced to reduce the workforce and implement work from home policies which further lowered production of goods. The pandemic also caused closure of many stores which were selling cosmetic and beauty products. In addition, regulatory agencies faced their own challenges during the pandemic, which impacted the approval and certification processes for new pigments. Delays in regulatory approvals affected the introduction of new and innovative pigments in the market.

Rising Demand of Cosmetic Pigment in Personal Care Products to Drive the Market Growth

The adoption of pigments in makeup products offers a wide variety of colors and effects, which attracts consumers to enhance their visual level. The products can be made of both organic or inorganic materials, as their primary motive is to improve the appearance of the nails, skin, or hair by enhancing glow or shine. Products comprising tinted skincare, eye makeup & under-eye care, lip & nail products, and hair care are among those where the cosmetic pigments is majorly used. The personal care industry has been continuously evolving, with trends shifting towards more innovative and diverse product offerings. This includes the use of various types of pigments to create unique and customizable cosmetic products. Cosmetic companies are constantly researching and developing new pigment technologies to provide novel effects, improved longevity, and better formulation compatibility. In addition, the increase in awareness among the population through social media platforms and influencers has led to a surging interest in beauty trends and makeup. This has led more consumers to experiment with alternate effects & colors, further driving the demand for more distinct pigments.

Strict Regulatory Compliance to Restrain the Market Growth

The usage of substances, labeling, and safety evaluations are all governed by different laws in the cosmetic sector. The expansion of the sector is dependent on the compliance with the rules, including those recognized by organizations like the U.S. Food and Drug Administration (FDA) and EU Cosmetic Regulation. Governing bodies such as the U.S. FDA and European Commission set guidelines for the safety and toxicity of cosmetic products, including pigments. To get their products approved for use in cosmetics, cosmetic pigment manufacturers must make sure that their products adhere to certain safety criteria. Cosmetic pigments are regarded as color additives in many nations, and their usage in cosmetics requires special authorization. Manufacturers must make sure that the necessary regulatory bodies have approved the use of their pigments in cosmetics. In addition, accurate labeling of cosmetic items is essential for customer safety and well-informed purchasing decisions, including the contents of pigments. Regulatory compliance involves accurate ingredient declarations on product packaging.

The safety of cosmetic items is a growing concern for consumers. Customers are more inclined to trust and support the development of pigments that have been thoroughly tested for potential allergic responses or skin sensitivities and are declared safe for use on the skin. Natural and organic cosmetic products are in greater demand as consumer awareness of environmental and health issues grows. The use of natural and plant-based pigments rather than synthetic ones has so gained more attention. This is expected to increase regulatory compliance & monitoring and would simultaneously hamper market growth.

Growing Demand of Eco-friendly and Sustainable Pigment to Drive Excellent Opportunities

The opportunity to create cosmetic pigments produced from natural, biodegradable, or recycled materials is expanding along with consumer demand for environmentally friendly and sustainable products. This addresses both the need for novel goods in the cosmetics business as well as environmental concerns. Cosmetic companies are increasingly turning to natural sources for pigments, such as plant extracts, minerals, and even microorganisms. Without utilizing synthetic chemicals, these natural pigments can provide brilliant hues. In addition, some businesses are creating pigments that are environmentally friendly and biodegradable. These pigments degrade more quickly once they have been used, which reduces their lasting presence in the environment.

The possible health concerns of synthetic pigments, such as allergies and skin irritations, are becoming more well known to consumers. Natural pigments that come from mineral, plant, and animal sources are frequently considered as safer substitutes. Customers are looking for products with a lesser environmental effect as the importance of sustainability increases. Natural pigments are often biodegradable and can be sourced sustainably, making them more attractive to environmentally conscious consumers. This is anticipated to boost the demand for organic pigment and create several growth opportunities in the market during the forecast period.

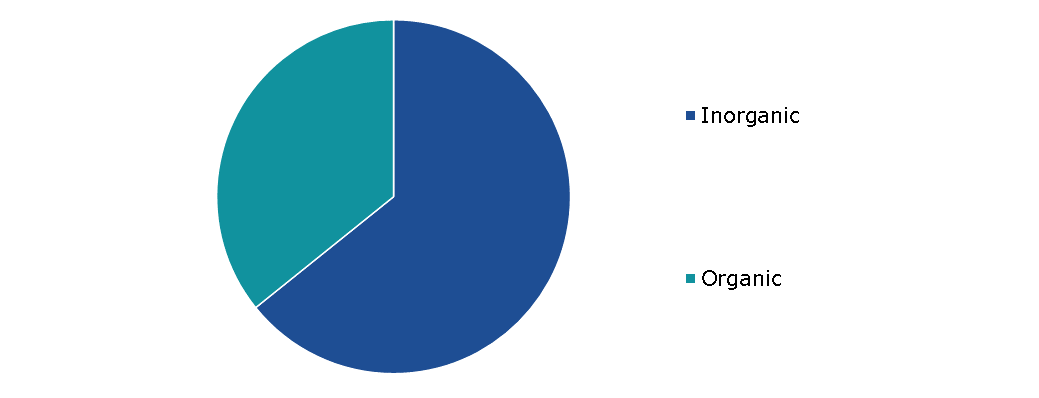

Global Cosmetic Pigments Market Share, by Composition, 2022

Source: Research Dive Analysis

The inorganic sub-segment accounted for the highest market share in 2022. Inorganic pigments are recognized for their durability, resistance to fading, and excellent color possibilities, making them ideal solutions for cosmetics, where color stability and safety are essential. The most primarily used inorganic pigments are iron oxides, titanium oxide, chromium oxide, ultramarines, zinc oxide, chromium hydroxide green, manganese violet, and others. The pigment manufacturers of titanium dioxide opts it to provide whiteness to cosmetics and personal care products that are applied on the skin. These comprise areas like nails, lips, and eyes. Titanium dioxide facilitates minimizing the product formula transparency and increases its opaqueness. Iron oxides are available in three basic shades red, yellow, and black. They are present in numerous cosmetic products like eye shadow or talcum powder. They are safe to use, although the iron oxide used in cosmetics is manufactured synthetically. Iron oxides are made in laboratories since naturally produced ones often have impurities. They do not cause any irritation and are non-allergic in nature. They do not even pose any problem to people with sensitive skin. The benefits like resistance to fading, stability, and vibrant color options make inorganic pigment the widely used pigment.

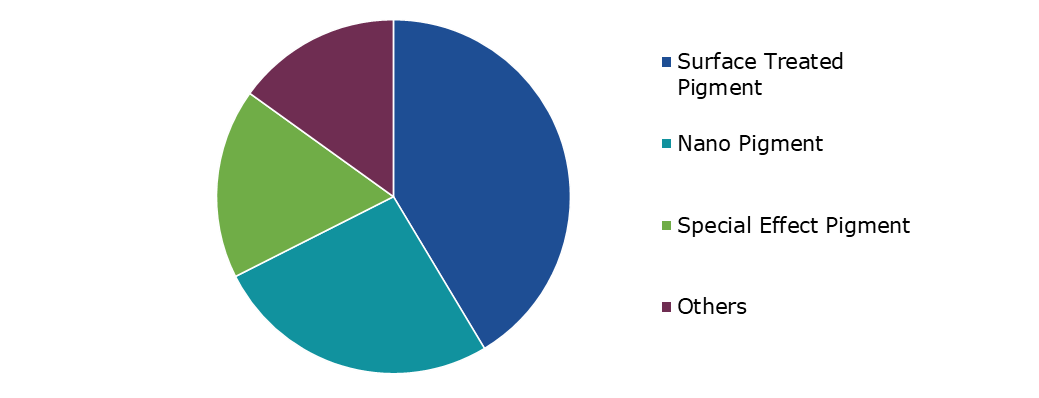

Global Cosmetic Pigments Market Share, by Type, 2022

Source: Research Dive Analysis

The surface treated pigment sub-segment accounted for the highest market share in 2022. Surface-treated pigments are frequently used in a variety of cosmetic products, including foundation, nail polish, blush, lipstick, and eyeshadow. For making high-quality, durable, and visually pleasing products, they are crucial because they provide variety in obtaining various cosmetic effects. In addition, benefits such as improved stability, enhanced color performance, controlled particle size, reduced skin irritation, ease of formulation, and UV protection are raising its adoption. Surface treatment helps protect pigments from degradation due to factors such as light, heat, moisture, and chemical reactions. This enhances the stability and shelf life of cosmetic products, preventing unwanted color changes or deterioration. Surface treatments can enhance the color properties of pigments by improving color intensity, vibrancy, and opacity. This allows cosmetic manufacturers to achieve consistent and vibrant colors in their products. Moreover, surface treatments can control the particle size of pigments, which affects the texture and feel of cosmetic products when applied to the skin. This control helps in achieving desired product qualities such as smoothness and ease of application.

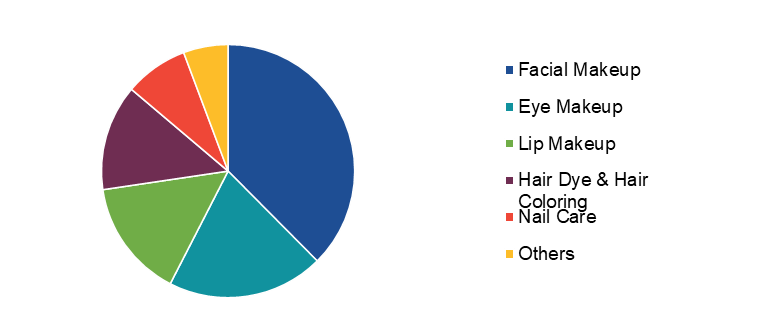

Global Cosmetic Pigments Market Share, by Application, 2022

Source: Research Dive Analysis

The facial makeup sub-segment accounted for the highest market share in 2022. Cosmetic pigments are compounds that offer color to a variety of cosmetic products, such as blush, foundation, lipstick, eyeshadow, and other products used for facial makeup. Customers use these products to accentuate their face characteristics, produce various looks, and attain desired aesthetics. These pigments are essential for creating the desired color and visual effects in cosmetics. In addition, the beauty industry constantly introduces new makeup products, formulas, and technologies that can make makeup application easier, long-lasting, and versatile. This is expected to boost the cosmetic pigments market growth during the forecast period.

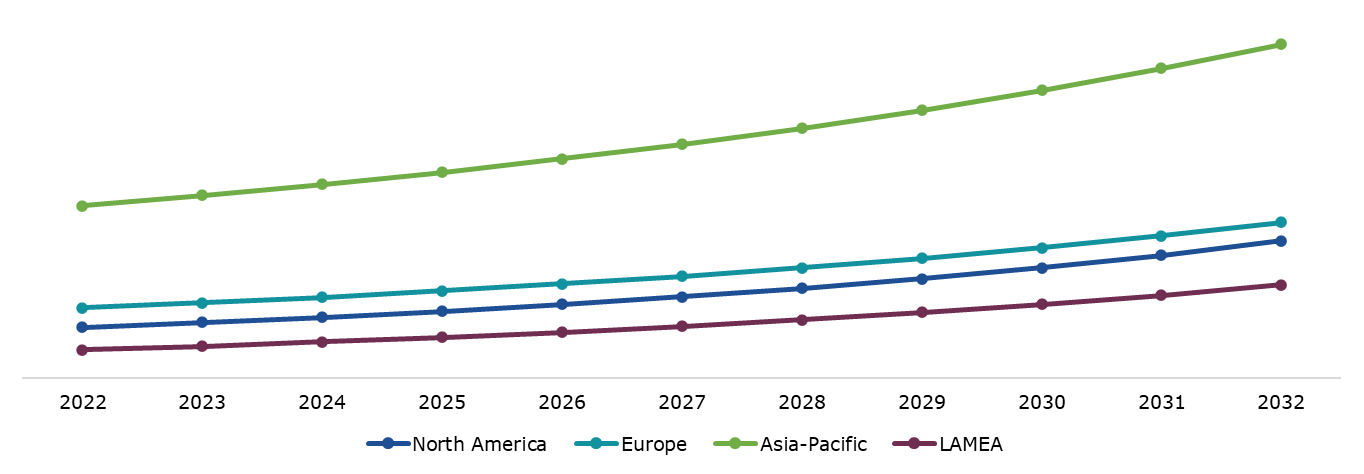

Global Cosmetic Pigments Market Size & Forecast, by Region, 2022-2032 ($Million)

Source: Research Dive Analysis

The Asia-Pacific cosmetic pigments market generated the highest revenue in 2022. The personal care and beauty sector has seen strong growth in Asia-Pacific. There has been a substantial growth in consumer demand for cosmetics and skincare goods in countries such as South Korea, China, Japan, and India. Simultaneously, the demand for cosmetic pigments also increased progressively, as they are used in various formulations, including skincare, cosmetics, and hair care products. South Korea has been at the top of innovation in the color cosmetics industry, planning fresh styles and ideas that have been universally adopted on a global scale. K-beauty trends, such as cushion foundations, gradient lips, and unique color palettes, have driven the demand for a wide range of cosmetic pigments. In several Asian cultures, there is a cultural preference for fair and even-toned skin. This has directed to a high demand for pigments opted in skin whitening products, which are regularly used in the region. These products often require specialized pigments to achieve the desired effects. Moreover, numerous global cosmetic brands have expanded their presence in Asia-Pacific to tap into their growing consumer base. This expansion has led to a higher demand for cosmetic pigments to meet local market preferences and regulatory requirements.

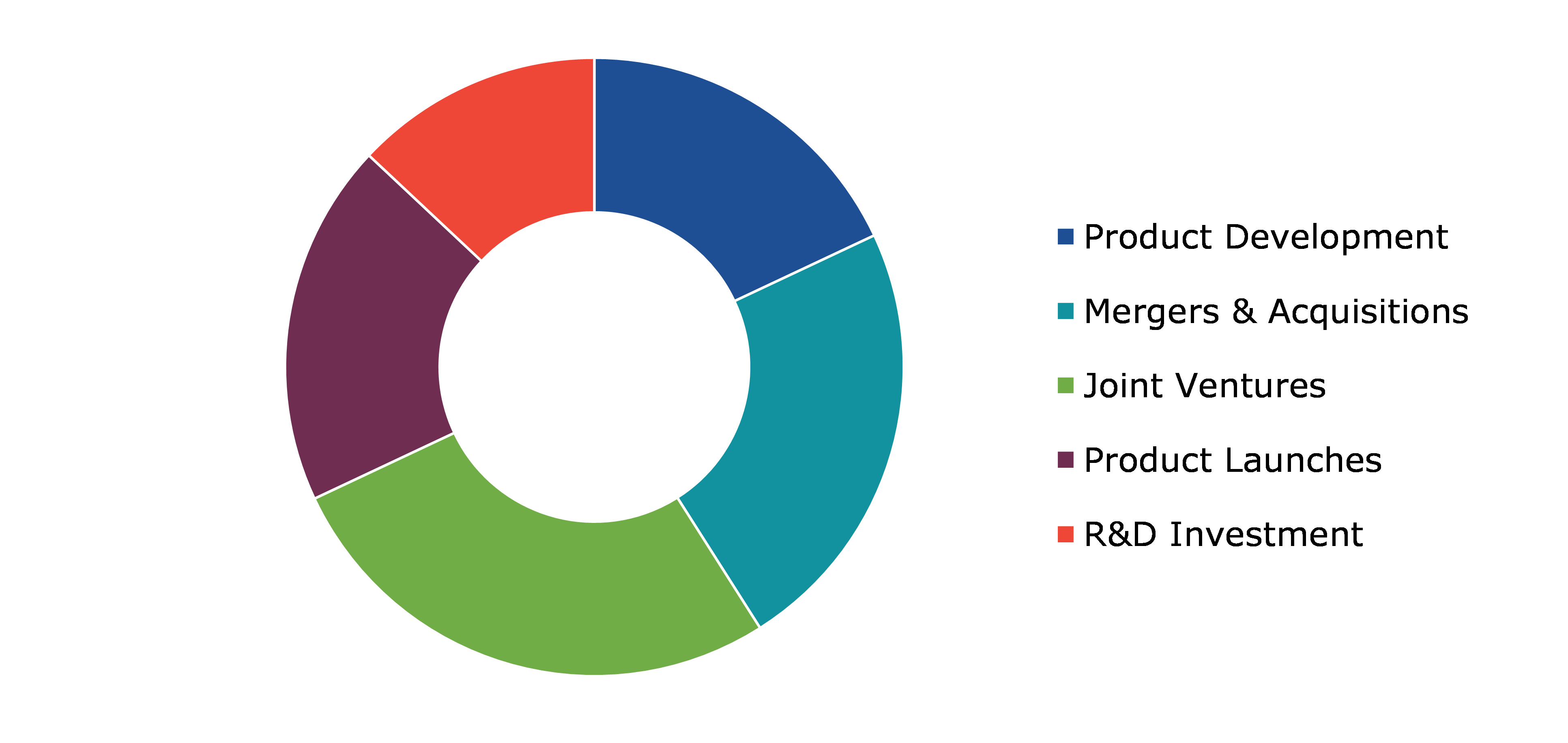

Competitive Scenario in the Global Cosmetic Pigments Market

Product launch, investment, and acquisition are common strategies followed by major market players. For instance, Sun Chemical, a subsidiary of DIC Corporation, is expected to present new effect pigments and highlight its natural ingredients and colorants at In-cosmetics Global 2023. The company would launch SunPRIZMA, a new range of 11 silica-based color travel effect pigments. The product would be offered in two particle size ranges. This innovative line would offer multi-chrome effects, and high coverage for intense glittering color travel and bold looks for striking sparkle finishes. With the SunPRIZMA line of effect pigments, cosmetic product manufacturers will be able to develop chromatic color shifts with special effects in color cosmetics. Sun Chemical is also expected to present its new Reflecks Dimensions Platinum G13CD, a sparkling, silver, metallic-like effect pigment based on borosilicate.

Source: Research Dive Analysis

Some of the leading cosmetic pigments market players are Merck, BASF SE, Koel Colors, Sudarshan Chemical, DIC Corporation, Sun Chemical, SENSIENT COSMETIC TECHNOLOGIES, NEELIKON, Lanxess, and Clariant.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2022 |

| Forecast Timeline for Market Projection | 2023-2032 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Composition |

|

|

Segmentation by Type

|

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global cosmetic pigments market?

A. The size of the global cosmetic pigments market was $2,106.9 million in 2022 and is projected to reach $4,449.2 million by 2032.

Q2. Which are the major companies in the cosmetic pigments market?

A. Merck, BASF SE, Koel Colors, Sudarshan Chemical, DIC Corporation, Sun Chemical, SENSIENT COSMETIC TECHNOLOGIES, NEELIKON, Lanxess, and Clariant are some of the key players in the global cosmetic pigments market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific cosmetic pigments market?

A. The Asia-Pacific cosmetic pigments market is anticipated to grow at 7.7% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Product launches and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Chart Industries, Inc., Linde Plc, and Emerson Electric Co. are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.5. Market size estimation

1.5.1. Top-down approach

1.5.2. Bottom-up approach

2. Report Scope

2.1. Market definition

2.2. Key objectives of the study

2.3. Report overview

2.4. Market segmentation

2.5. Overview of the impact of COVID-19 on global cosmetic pigments market

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Growth impact forces

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.3. Market value chain analysis

4.3.1. List of raw material suppliers

4.3.2. List of manufacturers

4.3.3. List of distributors

4.4. Innovation & sustainability matrices

4.4.1. Technology matrix

4.4.2. Regulatory matrix

4.5. Porter’s five forces analysis

4.5.1. Bargaining power of suppliers

4.5.2. Bargaining power of consumers

4.5.3. Threat of substitutes

4.5.4. Threat of new entrants

4.5.5. Competitive Rivalry Intensity

4.6. PESTLE analysis

4.6.1. Political

4.6.2. Economical

4.6.3. Social

4.6.4. Technological

4.6.5. Environmental

4.7. Impact of COVID-19 on cosmetic pigments market

4.7.1. Pre-covid market scenario

4.7.2. Post-covid market scenario

5. Cosmetic Pigments Market Analysis, by Composition

5.1. Overview

5.2. Inorganic Pigments

5.2.1. Definition, key trends, growth factors, and opportunities

5.2.2. Market size analysis, by region, 2022-2032

5.2.3. Market share analysis, by country, 2022-2032

5.3. Organic Pigments

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2. Market size analysis, by region, 2022-2032

5.3.3. Market share analysis, by country, 2022-2032

5.4. Research Dive Exclusive Insights

5.4.1. Market attractiveness

5.4.2. Competition heatmap

6. Cosmetic Pigments Market Analysis, by Type

6.1. Overview

6.2. Surface Treated Pigment

6.2.1. Definition, key trends, growth factors, and opportunities

6.2.2. Market size analysis, by region, 2022-2032

6.2.3. Market share analysis, by country, 2022-2032

6.3. Nano Pigment

6.3.1. Definition, key trends, growth factors, and opportunities

6.3.2. Market size analysis, by region, 2022-2032

6.3.3. Market share analysis, by country, 2022-2032

6.4. Special Effect Pigment

6.4.1. Definition, key trends, growth factors, and opportunities

6.4.2. Market size analysis, by region, 2022-2032

6.4.3. Market share analysis, by country, 2022-2032

6.5. Others

6.5.1. Definition, key trends, growth factors, and opportunities

6.5.2. Market size analysis, by region, 2022-2032

6.5.3. Market share analysis, by country, 2022-2032

6.6. Research Dive Exclusive Insights

6.6.1. Market attractiveness

6.6.2. Competition heatmap

7. Cosmetic Pigments Market Analysis, by Application

7.1. Overview

7.2. Facial Makeup

7.2.1. Definition, key trends, growth factors, and opportunities

7.2.2. Market size analysis, by region, 2022-2032

7.2.3. Market share analysis, by country, 2022-2032

7.3. Eye Makeup

7.3.1. Definition, key trends, growth factors, and opportunities

7.3.2. Market size analysis, by region, 2022-2032

7.3.3. Market share analysis, by country, 2022-2032

7.4. Lip Makeup

7.4.1. Definition, key trends, growth factors, and opportunities

7.4.2. Market size analysis, by region, 2022-2032

7.4.3. Market share analysis, by country, 2022-2032

7.5. Hair Dye & Hair Coloring

7.5.1. Definition, key trends, growth factors, and opportunities

7.5.2. Market size analysis, by region, 2022-2032

7.5.3. Market share analysis, by country, 2022-2032

7.6. Nail Care

7.6.1. Definition, key trends, growth factors, and opportunities

7.6.2. Market size analysis, by region, 2022-2032

7.6.3. Market share analysis, by country, 2022-2032

7.7. Others

7.7.1. Definition, key trends, growth factors, and opportunities

7.7.2. Market size analysis, by region, 2022-2032

7.7.3. Market share analysis, by country, 2022-2032

7.8. Research Dive Exclusive Insights

7.8.1. Market attractiveness

7.8.2. Competition heatmap

8. Cosmetic Pigments Market, by Region

8.1. North America

8.1.1. U.S.

8.1.1.1. Market size analysis, by Composition, 2022-2032

8.1.1.2. Market size analysis, by Type, 2022-2032

8.1.1.3. Market size analysis, by Application, 2022-2032

8.1.2. Canada

8.1.2.1. Market size analysis, by Composition, 2022-2032

8.1.2.2. Market size analysis, by Type, 2022-2032

8.1.2.3. Market size analysis, by Application, 2022-2032

8.1.3. Mexico

8.1.3.1. Market size analysis, by Composition, 2022-2032

8.1.3.2. Market size analysis, by Type, 2022-2032

8.1.3.3. Market size analysis, by Application, 2022-2032

8.1.4. Research Dive Exclusive Insights

8.1.4.1. Market attractiveness

8.1.4.2. Competition heatmap

8.2. Europe

8.2.1. Germany

8.2.1.1. Market size analysis, by Composition, 2022-2032

8.2.1.2. Market size analysis, by Type, 2022-2032

8.2.1.3. Market size analysis, by Application, 2022-2032

8.2.2. UK

8.2.2.1. Market size analysis, by Composition, 2022-2032

8.2.2.2. Market size analysis, by Type, 2022-2032

8.2.2.3. Market size analysis, by Application, 2022-2032

8.2.3. France

8.2.3.1. Market size analysis, by Composition, 2022-2032

8.2.3.2. Market size analysis, by Type, 2022-2032

8.2.3.3. Market size analysis, by Application, 2022-2032

8.2.4. Spain

8.2.4.1. Market size analysis, by Composition, 2022-2032

8.2.4.2. Market size analysis, by Type, 2022-2032

8.2.4.3. Market size analysis, by Application, 2022-2032

8.2.5. Italy

8.2.5.1. Market size analysis, by Composition, 2022-2032

8.2.5.2. Market size analysis, by Type, 2022-2032

8.2.5.3. Market size analysis, by Application, 2022-2032

8.2.6. Rest of Europe

8.2.6.1. Market size analysis, by Composition, 2022-2032

8.2.6.2. Market size analysis, by Type, 2022-2032

8.2.6.3. Market size analysis, by Application, 2022-2032

8.2.7. Research Dive Exclusive Insights

8.2.7.1. Market attractiveness

8.2.7.2. Competition heatmap

8.3. Asia-Pacific

8.3.1. China

8.3.1.1. Market size analysis, by Composition, 2022-2032

8.3.1.2. Market size analysis, by Type, 2022-2032

8.3.1.3. Market size analysis, by Application, 2022-2032

8.3.2. Japan

8.3.2.1. Market size analysis, by Composition, 2022-2032

8.3.2.2. Market size analysis, by Type, 2022-2032

8.3.2.3. Market size analysis, by Application, 2022-2032

8.3.3. India

8.3.3.1. Market size analysis, by Composition, 2022-2032

8.3.3.2. Market size analysis, by Type, 2022-2032

8.3.3.3. Market size analysis, by Application, 2022-2032

8.3.4. Australia

8.3.4.1. Market size analysis, by Composition, 2022-2032

8.3.4.2. Market size analysis, by Type, 2022-2032

8.3.4.3. Market size analysis, by Application, 2022-2032

8.3.5. South Korea

8.3.5.1. Market size analysis, by Composition, 2022-2032

8.3.5.2. Market size analysis, by Type, 2022-2032

8.3.5.3. Market size analysis, by Application, 2022-2032

8.3.6. Rest of Asia-Pacific

8.3.6.1. Market size analysis, by Composition, 2022-2032

8.3.6.2. Market size analysis, by Type, 2022-2032

8.3.6.3. Market size analysis, by Application, 2022-2032

8.3.7. Research Dive Exclusive Insights

8.3.7.1. Market attractiveness

8.3.7.2. Competition heatmap

8.4. LAMEA

8.4.1. Brazil

8.4.1.1. Market size analysis, by Composition, 2022-2032

8.4.1.2. Market size analysis, by Type, 2022-2032

8.4.1.3. Market size analysis, by Application, 2022-2032

8.4.2. UAE

8.4.2.1. Market size analysis, by Composition, 2022-2032

8.4.2.2. Market size analysis, by Type, 2022-2032

8.4.2.3. Market size analysis, by Application, 2022-2032

8.4.3. South Africa

8.4.3.1. Market size analysis, by Composition, 2022-2032

8.4.3.2. Market size analysis, by Type, 2022-2032

8.4.3.3. Market size analysis, by Application, 2022-2032

8.4.4. Argentina

8.4.4.1. Market size analysis, by Composition, 2022-2032

8.4.4.2. Market size analysis, by Type, 2022-2032

8.4.4.3. Market size analysis, by Application, 2022-2032

8.4.5. Rest of LAMEA

8.4.5.1. Market size analysis, by Composition, 2022-2032

8.4.5.2. Market size analysis, by Type, 2022-2032

8.4.5.3. Market size analysis, by Application, 2022-2032

8.4.6. Research Dive Exclusive Insights

8.4.6.1. Market attractiveness

8.4.6.2. Competition heatmap

9. Competitive Landscape

9.1. Top winning strategies, 2022

9.1.1. By strategy

9.1.2. By year

9.2. Strategic overview

9.3. Market share analysis, 2022

10. Company Profiles

10.1. Merck

10.1.1. Overview

10.1.2. Business segments

10.1.3. Product portfolio

10.1.4. Financial performance

10.1.5. Recent developments

10.1.6. SWOT analysis

10.2. BASF SE

10.2.1. Overview

10.2.2. Business segments

10.2.3. Product portfolio

10.2.4. Financial performance

10.2.5. Recent developments

10.2.6. SWOT analysis

10.3. Koel Colors

10.3.1. Overview

10.3.2. Business segments

10.3.3. Product portfolio

10.3.4. Financial performance

10.3.5. Recent developments

10.3.6. SWOT analysis

10.4. Sudarshan Chemical

10.4.1. Overview

10.4.2. Business segments

10.4.3. Product portfolio

10.4.4. Financial performance

10.4.5. Recent developments

10.4.6. SWOT analysis

10.5. DIC Corporation

10.5.1. Overview

10.5.2. Business segments

10.5.3. Product portfolio

10.5.4. Financial performance

10.5.5. Recent developments

10.5.6. SWOT analysis

10.6. Sun Chemical

10.6.1. Overview

10.6.2. Business segments

10.6.3. Product portfolio

10.6.4. Financial performance

10.6.5. Recent developments

10.6.6. SWOT analysis

10.7. SENSIENT COSMETIC TECHNOLOGIES

10.7.1. Overview

10.7.2. Business segments

10.7.3. Product portfolio

10.7.4. Financial performance

10.7.5. Recent developments

10.7.6. SWOT analysis

10.8. NEELIKON

10.8.1. Overview

10.8.2. Business segments

10.8.3. Product portfolio

10.8.4. Financial performance

10.8.5. Recent developments

10.8.6. SWOT analysis

10.9. Lanxess

10.9.1. Overview

10.9.2. Business segments

10.9.3. Product portfolio

10.9.4. Financial performance

10.9.5. Recent developments

10.9.6. SWOT analysis

10.10. Clariant

10.10.1. Overview

10.10.2. Business segments

10.10.3. Product portfolio

10.10.4. Financial performance

10.10.5. Recent developments

10.10.6. SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com