Digital Vault Market Report

RA05497

Digital Vault Market by Component (Solution and Service), Deployment (On Premise and Cloud), Enterprise Size (Large Enterprises and Small & Medium Enterprises), End Use (BFSI, IT & Telecom, Manufacturing, Government, Healthcare, Healthcare, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022–2031

Global Digital Vault Market Analysis

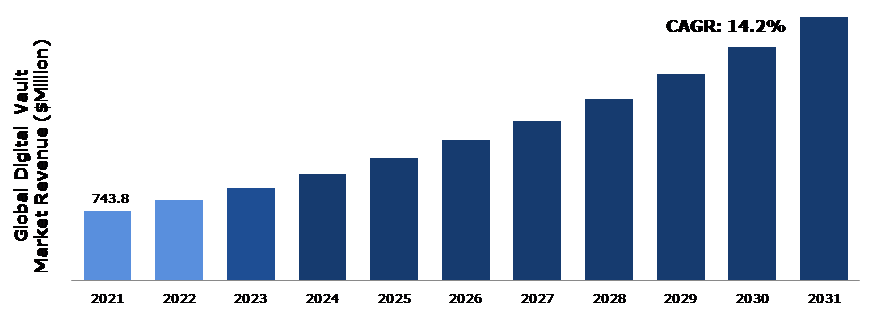

The Global Digital Vault Market Share was 743.8 million in 2021and is predicted to grow with a CAGR of 14.2%, by generating a revenue of $2,850.7 million by 2031.

Global Digital Vault Market Synopsis

A digital vault is a system that provides encryption and access control techniques to secure data on a system so that fraudsters cannot access it. The digital vault technologies offer customizable dashboards for real-time tracking and safeguarding repositories along with storing data for an organization and centralizing credentials. The rise in requirement for stringent compliance across various industries is expected to drive global digital vault market. The global digital vault market is anticipated to further expand because of government initiatives to create regulations to secure highly sensitive data for any enterprise. Moreover, a growing number of connected devices worldwide are producing a lot of data and the need to store this data is fueling the growth of the global digital vault market.

However, digital vault market growth is anticipated to be hampered due to the shortage of experts, professionals, and skilled personnel required to design digital vaults. Another significant challenge that the sector may face is implementing the best information technology security solution. Modern technology is not always used by providers of digital vault services. If one of these digital vaults is set up and selected at random, important data could be in danger of being lost. These elements can hamper the market growth for digital vaults.

The rise in demand for long-term data security is anticipated to offer lucrative growth opportunities to the global digital vault market players. Many companies are adopting data vaults due to their growing concerns about data loss, which could result in huge losses for businesses. This is resulting in a growing need for digital vaults. The use of cloud services, which will increase demand for cloud-based security solutions, is another factor that is anticipated to generate growth opportunities for the global digital vault market.

According to regional analysis, the Asia-Pacific digital vault market accounted for the highest market share in 2021. A significant factor anticipated to propel the expansion of the global digital vault market in Asia-Pacific is the high adoption of digital vaults by China and India to safeguard and store massive amounts of data.

Digital Vault Market Overview

A digital vault is a robust and secure data storage system that is guarded by access control, firewall, and encryption technologies. The benefits of a digital vault include long-term storage, extremely secure networks regardless of the physical topology of the network, the ability to manage virtual digital credentials and documents as attachments or secure notes, etc. It can store some of the most sensitive data of the company, including privileged user credentials, audit data, and access control policies.

COVID-19 Impact on Digital Vault Market

The COVID-19 outbreak has created many problems for businesses across the globe. The demand for digital vaults increased dramatically during the pandemic due to the shift by many companies to digital infrastructure. The rising number of cyberattacks has increased the need for safe storage services, breach protection, and data security solutions. Rapid digitization raised the threat of cyberattacks and jeopardized the security of firms. Hence, the need to protect personal information and data has increased significantly during the pandemic. Due to all these factors, the demand for digital vaults increased dramatically. during the COVID-19 pandemic. However, there is a need for increasing awareness among people about data security to increase the use of digital vaults.

Digital vaults solve all the issues of keeping essential documents and maintaining the data. It is one of the most pivotal technological advancements that help in eliminating the danger of unlawful usage of important documents. In the upcoming years, digital vault technology is anticipated to witness more innovations and advancements. Also, the resurgence of COVID-19 is further expected to increase the investment of organizations in digital vault technology.

Growing Data Protection Concerns are Expected to Drive the Digital Vault Market Growth

The global demand for digital vaults is increasing as internet usage as well as the adoption of internet-connected gadgets increases across the globe. Numerous governments are increasing their efforts to safeguard both national security and individual data privacy due to the rising threats and risks associated with data protection in the public and private sectors. Many companies are also increasingly adopting digital vault technologies to maintain their systems and keep data safe from cyberattacks. In addition, organizations often collect data from their customers and use it for various business strategies. Protecting this data is extremely important for businesses to keep confidence in their customers. Hence, the need for the digital vault is anticipated to increase significantly in the upcoming years.

The Lack of Availability of Expert Professionals is Anticipated to Restrain Digital Vault Market Growth

The lack of availability of expert professionals to build high-security digital vaults is anticipated to restrain digital vault market growth during the forecast period. The selection of the best information technology security solution is another challenge that the market may encounter. Not every digital vault service provider uses cutting-edge technology. Critical data may be in danger if such digital vaults are installed and used. In addition, the lack of awareness in developing nations about digital vaults is also a major concern.

Increasing Digitalization is Anticipated to Offer Lucrative Growth Opportunities to Digital Vault Market Players

Increasing digitalization worldwide is anticipated to augment the need for high-level cyber security solutions. Many firms are undergoing digitalization to work more quickly and efficiently with clients, suppliers, and coworkers. Moreover, due to the COVID-19 pandemic, there has been a dramatic upsurge in digitalization worldwide. However, the surge in digitalization is likely to result in a rise in data loss, hacking, and other issues. This and all other mentioned factors are expected to generate excellent opportunities for digital vault market growth during the forecast period.

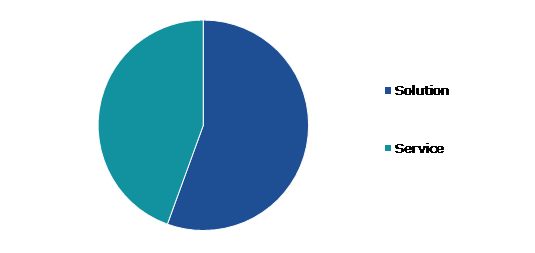

Global Digital Vault Market, by Component

Based on component, the market is further divided into solution and service. Among this service sub-segment is anticipated to show a fastest CAGR during the forecast period.

Global Digital Vault Market Size, by Component, 2021

The service sub-segment is anticipated to show the fastest CAGR during the forecast period. The advantages of digital vault services include data protection, monitoring, and centralized visibility of the company’s data landscape against illegal access, exposure, and theft. The digital vault is one of the key technologies for the digitalization of various end-user industries including the financial service sector. It can change the way businesses collect, organize, and store client documents. Digital Vault platform is most commonly cloud-based and offers the advantages such as data availability, redundancy, and cost-effectiveness. Due to all these factors, the demand for digital vault services is expected to increase during the forecast period.

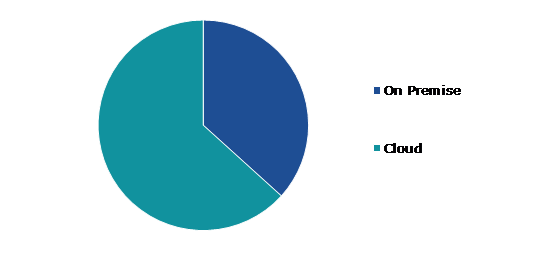

Global Digital Vault Market, by Deployment

Based on deployment, the global digital vault market has been divided into on premise and cloud. Among these, the cloud sub-segment accounted for the highest digital vault market share in 2021 and is projected to maintain its dominance during the forecast period.

Global Digital Vault Market Trends, by Deployment, 2021

The cloud sub-segment is expected to have the fastest growth as well as the highest revenue during the forecast period. The demand for cloud-based data security is increasing as the importance of cloud data security is increasingly recognized by organizations. Since cloud-based solutions are less expensive than on-premises ones, the demand for organizational data security and cloud security solutions is growing as data centers, business processes, and other services have moved to cloud-based technology.

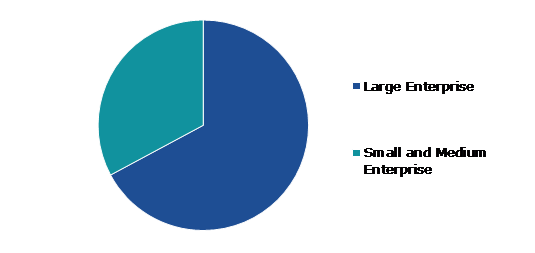

Global digital Vault Market, by Enterprise size

Based on enterprise size, the global digital vault market has been divided into large enterprise and small and medium enterprise. Among these, small & medium enterprises sub-segment is anticipated to have the fastest growth during the forecast period.

Global Digital Vault Market Share, by Enterprise Size, 2021

The small & medium enterprises sub-segment is expected to have the fastest growth during the forecast period. Data security is necessary for organizations since it helps to safeguard all information systems and to safeguard an organization against data loss. The need for solutions that safeguard data and limit access by unauthorized users is expanding, and this is particularly the case of small and medium-size enterprises which are more concerned about the security of their data.

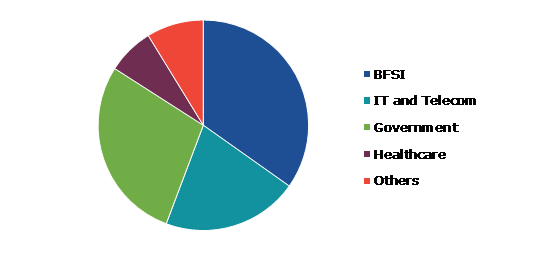

Global Digital Vault Market, by End Use

Based on end use, the global digital vault market has been divided into BFSI, IT & telecom, manufacturing, government, healthcare, and others. Among these, healthcare sub-segment is expected to show a highest CAGR during the forecast period.

Global Digital vault Market Value, by End-user Type, 2021

The healthcare sub-segment is expected to be the fastest growing during the forecast period. Due to the surge in cyberattacks on healthcare companies and the development of incredibly advanced techniques by cybercriminals, healthcare data security is more crucial than ever. Additionally, laws such as HIPAA require that institutions that are covered by the law put in place the proper physical, administrative, and technical measures to guarantee the availability, confidentiality, and integrity of electronically protected health information.

The BFSI sub-segment is projected to hold largest digital vault market share during the forecast period. In the last decade, the BFSI sector has increasingly started adopting digital technologies and with the augmentation of the smartphones and internet, digital banking has emerged and transformed the way people use banking services. To increase more customer base, the banks are offering unique services and products, through online banking systems. However, these efforts are increasing the chances of online fraud all over the world. This in turn is augmenting the demand for digital vaults in the BFSI sector.

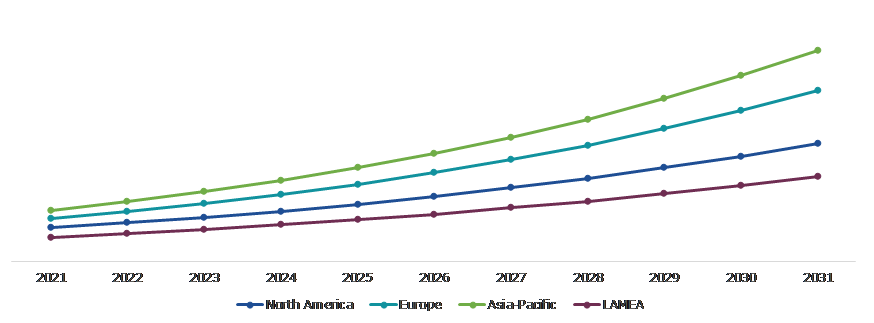

Global Digital Vault Market, Regional Insights

The Digital vault market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Digital Vault Market Size & Forecast, by Region, 2021-2031 (USD Million)

The Digital Vault Market in North America to be the Most Dominant

The Asia-Pacific region is expected to dominate the global digital vault market during the forecast period. This region is experiencing a rise in demand for digital vaults as a result of the region's numerous industry- and medium-specific data security regulations. In developing economies such as China, India, Thailand, Vietnam, Singapore, etc the various digital program makes government services available in digital form. Many government services have been digitalized via the use of digital vaults that saves personal information so customers are not required to manually enter their information when doing online banking transactions.

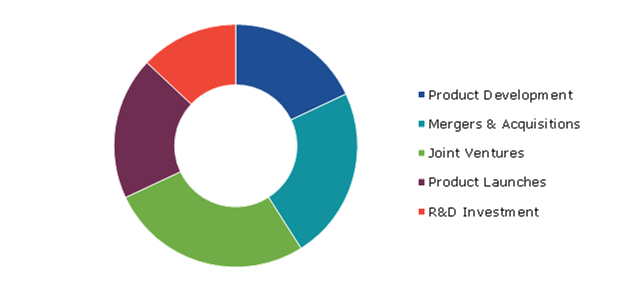

Global Digital Vault Market Competitive Scenario

Joint ventures, investment, merger & acquisition, product development, and technological development are the common strategies followed by major digital vault market players. For instance, in October 2021, Prisidio a provider of the cloud-based vault announced an additional $3.5 million in seed funding for the development of its digital vault, which will allow users to safely store, manage, and access important information.

Some of the leading players in digital vault market are Keeper Security, Inc., Multicert, Hitachi Vantara LLC, Fiserv, Inc., Microfocus, Johnson Controls, CyberArk Software Ltd., Microsoft, IBM Corporation, and Oracle.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Component

|

|

| Segmentation by Deployment |

|

| Segmentation by Enterprise Size |

|

| Segmentation by End Use |

|

| Key Companies Profiled |

|

Q1. What is the size of the digital vault market?

A. The global digital vault market size was over $743.8 million in 2021 ¬¬and is anticipated to reach $2,850.7 million by 2031.

Q2. Which are the leading companies in the digital vault market?

A. Oracle, IBM Corporation, and Microsoft are some of the key players in the global digital vault market.

Q3. Which region possesses greater investment opportunities in the coming future?

A. Asia-Pacific possesses great investment opportunities for investors to witness the most promising market growth in the coming years.

Q4. What is the growth rate of the Asia-Pacific market?

A. The Asia-Pacific digital vault market is anticipated to grow at 15.0% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Product innovations, business expansions, and technological advancements are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Multicert, Keeper Security, Inc., and Microfocus are investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global digital vault market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Digital Vault market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Digital Vault Market Analysis, by Component

5.1.Overview

5.2.Solution

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region

5.2.3.Market share analysis, by country

5.3.Service

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region

5.3.3.Market share analysis, by country

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Digital Vault Market Analysis, by Deployment

6.1.On Premise

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region

6.1.3.Market share analysis, by country

6.2.Cloud

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region

6.2.3.Market share analysis, by country

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Digital Vault Market Analysis, by Enterprise Size

7.1.Overview

7.2.Large Enterprise

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region

7.2.3.Market share analysis, by country

7.3.Small and Medium Enterprise

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region

7.3.3.Market share analysis, by country

7.4.Research Dive Exclusive Insights

7.4.1.Market attractiveness

7.4.2.Competition heatmap

8.Digital Vault Market Analysis, by End Use

8.1.Overview

8.2.BFSI

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region

8.2.3.Market share analysis, by country

8.3.IT & Telecomm

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region

8.3.3.Market share analysis, by country

8.4.Manufacturing

8.4.1.Definition, key trends, growth factors, and opportunities

8.4.2.Market size analysis, by region

8.4.3.Market share analysis, by country

8.5.Government

8.5.1.Definition, key trends, growth factors, and opportunities

8.5.2.Market size analysis, by region

8.5.3.Market share analysis, by country

8.6.Healthcare

8.6.1.Definition, key trends, growth factors, and opportunities

8.6.2.Market size analysis, by region

8.6.3.Market share analysis, by country

8.7.Others

8.7.1.Definition, key trends, growth factors, and opportunities

8.7.2.Market size analysis, by region

8.7.3.Market share analysis, by country

8.8.Research Dive Exclusive Insights

8.8.1.Market attractiveness

8.8.2.Competition heatmap

9.Digital Vault Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Component

9.1.1.2.Market size analysis, by Deployment

9.1.1.3.Market size analysis, by Enterprise Size

9.1.1.4.Market size analysis, by End Use

9.1.2.Canada

9.1.2.1.Market size analysis, by Component

9.1.2.2.Market size analysis, by Deployment

9.1.2.3.Market size analysis, by Enterprise Size

9.1.2.4.Market size analysis, by End Use

9.1.3.Mexico

9.1.3.1.Market size analysis, by Component

9.1.3.2.Market size analysis, by Deployment

9.1.3.3.Market size analysis, by Enterprise Size

9.1.3.4.Market size analysis, by End Use

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Component

9.2.1.2.Market size analysis, by Deployment

9.2.1.3.Market size analysis, by Enterprise Size

9.2.1.4.Market size analysis, by End Use

9.2.2.UK

9.2.2.1.Market size analysis, by Component

9.2.2.2.Market size analysis, by Deployment

9.2.2.3.Market size analysis, by Enterprise Size

9.2.2.4.Market size analysis, by End Use

9.2.3.France

9.2.3.1.Market size analysis, by Component

9.2.3.2.Market size analysis, by Deployment

9.2.3.3.Market size analysis, by Enterprise Size

9.2.3.4.Market size analysis, by End Use

9.2.4.Spain

9.2.4.1.Market size analysis, by Component

9.2.4.2.Market size analysis, by Deployment

9.2.4.3.Market size analysis, by Enterprise Size

9.2.4.4.Market size analysis, by End Use

9.2.5.Italy

9.2.5.1.Market size analysis, by Component

9.2.5.2.Market size analysis, by Deployment

9.2.5.3.Market size analysis, by Enterprise Size

9.2.5.4.Market size analysis, by End Use

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Component

9.2.6.2.Market size analysis, by Deployment

9.2.6.3.Market size analysis, by Enterprise Size

9.2.6.4.Market size analysis, by End Use

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Component

9.3.1.2.Market size analysis, by Deployment

9.3.1.3.Market size analysis, by Enterprise Size

9.3.1.4.Market size analysis, by End Use

9.3.2.Japan

9.3.2.1.Market size analysis, by Component

9.3.2.2.Market size analysis, by Deployment

9.3.2.3.Market size analysis, by Enterprise Size

9.3.2.4.Market size analysis, by End Use

9.3.3.India

9.3.3.1.Market size analysis, by Component

9.3.3.2.Market size analysis, by Deployment

9.3.3.3.Market size analysis, by Enterprise Size

9.3.3.4.Market size analysis, by End Use

9.3.4.Australia

9.3.4.1.Market size analysis, by Component

9.3.4.2.Market size analysis, by Deployment

9.3.4.3.Market size analysis, by Enterprise Size

9.3.4.4.Market size analysis, by End Use

9.3.5.South Korea

9.3.5.1.Market size analysis, by Component

9.3.5.2.Market size analysis, by Deployment

9.3.5.3.Market size analysis, by Enterprise Size

9.3.5.4.Market size analysis, by End Use

9.3.6.Rest of Asia Pacific

9.3.6.1.Market size analysis, by Component

9.3.6.2.Market size analysis, by Deployment

9.3.6.3.Market size analysis, by Enterprise Size

9.3.6.4.Market size analysis, by End Use

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Component

9.4.1.2.Market size analysis, by Deployment

9.4.1.3.Market size analysis, by Enterprise Size

9.4.1.4.Market size analysis, by End Use

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Component

9.4.2.2.Market size analysis, by Deployment

9.4.2.3.Market size analysis, by Enterprise Size

9.4.2.4.Market size analysis, by End Use

9.4.3.UAE

9.4.3.1.Market size analysis, by Component

9.4.3.2.Market size analysis, by Deployment

9.4.3.3.Market size analysis, by Enterprise Size

9.4.3.4.Market size analysis, by End Use

9.4.4.South Africa

9.4.4.1.Market size analysis, by Component

9.4.4.2.Market size analysis, by Deployment

9.4.4.3.Market size analysis, by Enterprise Size

9.4.4.4.Market size analysis, by End Use

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Component

9.4.5.2.Market size analysis, by Deployment

9.4.5.3.Market size analysis, by Enterprise Size

9.4.5.4.Market size analysis, by End Use

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.Keeper Security, Inc.

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.Multicert

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.Hitachi Vantara LLC

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.Fiserv, Inc.

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.Microfocus

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.Johnson Controls

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.CyberArk Software Ltd.

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.Microsoft

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.IBM Corporation

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Oracle

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

A digital vault is a highly secure online software platform that enables an individual to gather, supervise, and maintain crucial & confidential digital information such as credentials, assets, documents, and many more. Various things like logins of bank accounts, cryptocurrency accounts, crucial personal documentation, confidential company information, etc. can be stored in a digital vault. The demand for the digital vault is growing rapidly due to the outburst of COVID-19, which has forced many organizations to adapt rapidly to new realities for smooth working with customers, suppliers, and colleagues.

Forecast Analysis of the Global Digital Vault Market

The global digital vault market is projected to witness an exponential growth during the forecast period, owing to the growing digitization across the globe, which has created an increased need for high-level cyber security solutions. Conversely, the lack of expertise and privacy compliance challenges associated with digital vaults are the factors expected to hamper the market growth in the projected timeframe.

The increasing demand & dependency on the internet and the growing adoption of the internet-connected devices along with the growing concerns about protecting data generated from connected devices are the significant factors and digital vault market trends estimated to bolster the growth of the global market in the coming future. According to a latest report published by Research Dive, the global digital vault market is anticipated to rise at a CAGR of 14.2%, and will reach up to $2,850.7 million by the end of 2031.

Digital Vault Market Trends and Developments

Some of the foremost players in the digital vault market are Johnson Controls International PLC, CyberArk Software Ltd., Microsoft, IBM, Oracle Corporation, Keeper Security, Multicert, Hitachi Limited, Fiserv, Micro Focus, and others. These players are focused on planning and devising tactics such as mergers and acquisitions, collaborations, novel advances, and partnerships to reach a notable position in the global market. For instance:

- In May 2021, Johnson Controls, the global leader for smart and sustainable buildings, announced a partnership with DigiCert, the global leading provider of digital certificate services & PKI solutions, in order to take advantage of IoT Device Manager to improve smart building cybersecurity, PKI (Public Key Infrastructure), and management of digital identities. Built on ONE digital certificate platform of DigiCert, this device manager provides advanced secure connectivity in smart building solutions.

- In April 2022, FutureVault, a leading provider of secure document exchange & Digital Vault solutions, entered into a partnership with Envestnet|Yodlee, a data analytics and data aggregation platform powering dynamic, with an aim to enhance FutureVault’s connectivity, productivity, and experience between financial services advisors, organizations, and end-clients within the platform.

- In June 2022, Prisidio, a digital vault that helps people to easily and securely store, organize, and share information, announced the launch of its web and mobile applications (Android and iOS). The company solves the “digital dilemma,” in which digital assets, critical documents, and personal information of people are spread across digital and physical locations, but they don’t have a centralized, convenient digital access point for all of it.

Most Profitable Region

The Asia-Pacific digital vault market is expected to observe dominant growth in the years to come. This is because the region is experiencing a rising demand for digital vaults owing to the region’s numerous industry- & medium-specific data security regulations. The government services are available in digital form with the help of various digital platforms in the developing economies, such as India, China, Thailand, and others. Moreover, many government services are digitalized with the help of the using digital vaults that helps in saving personal information of customers when doing online banking transactions.

Impact of COVID-19 on the Market

The outbreak of COVID-19 across the globe has positively impacted the global digital vault market. This is mainly because the digital infrastructure has witnessed a dramatic increase in the demand due to pandemic. Despite the shutting down of offices and other facility closures, the global businesses are continuing to operate online, which has increased the risk of cyber-attacks, data breaches, and other problems. With cyber-security the top priority, the leading companies are highly focusing on security and risk management by ensuring that their companies’ digital platforms and online services are resistant to cyber-attacks. All these factors are boosting the demand for digital vaults, thereby accelerating the growth of the global market during the pandemic period.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com