Digital Banking Market Report

RA00053

Digital Banking Market, by Type (Credit Unions, Co-operative Banks, Consumer Bank), by Services (Digital Payments, Digital Sales), Regional Outlook (North America, Europe, Asia-Pacific, LAMEA), Global Opportunity Analysis and Industry Forecast, 2019–2027

Digital Banking Market Overview 2027:

The global digital banking market size was valued at $803.8 Billion in 2018, and is anticipated to reach $ 1610 Billion by 2027, growing at a CAGR of 8.9% during the forecast period. The North America digital banking market reached nearly $376.2 Billion in 2019 and should reach $721.3 Billion by 2027, at a compound annual growth rate (CAGR) of 8.30% for the period of 2019-2027.

Banking is moving online or going digital from the traditional banking program services and activities which were previously only accessible to consumers when present inside of a bank branch. Digital banking is an easy, quick, and convenient method or technology that helps an individual or a business to control and handle everyday finances. The customer simply needs to log in on any internet connected device to transfer funds, pay bills, and check balances. Today most of the banks are offering digital banking services and solutions, but the features and benefits vary from bank to bank.

Market Drivers & Restraints:

Cost efficiency and ease of use in financial transactions is anticipated to boost the growth of digital banking market, while data breaches act as a threat to the market growth

The major digital banking market drivers are cost efficiency and ease of use advantage of digital banking as compared to normal banking system, increasing penetration of electronic gadgets, easy access to the high speed internet services are expected to boost the market during the forecast period. However, the increasing threat of data breaches and cyber-attacks on banking servers may hamper the digital banking market forecast. Moreover, the technological advancements such as integration of block chain technology is further strengthening the global digital banking market.

Future Trends and Market opportunities:

Growing use of mobile phones and internet connections and various government imitative may create more opportunity for the digital banking market

Digital banking market trends leads to the growing use of mobile phones and internet penetration all over the globe, banks are moving toward digital channels to provide their services. Also, they are working in partnership with FinTech corporations and other third-party interfaces to create additional customer-centric products & services, and thereby deliver an enhanced customer experience. Government is also initiating and driving the use of digital banking services by various initiatives globally. The focus of government of various countries to become cashless has led to the initiation of numerous policies such as demonetization which boosts and promotes different traders to integrate digital payments. For example, in November 2019, the government of India proposed a law on companies with annual turnover of over $7.0 million to offer low-cost digital means of payment, which includes Aadhaar Pay, BHIM UPI, debit cards, RTGS, UPI-QR Code, and NEFT, to consumers. Also, no merchant discount rate (MDR) or charges would be levied either on merchants or customers. Hence, such regulations and support offered by governments are expected to further expand the digital banking market globally.

Market Restraints:

High risk of security regarding the personal data of consumer and high belief in the brick and mortar model is consider to be the major threats for the growth of digital banking market

Consumers still believe in the brick and mortar model when it comes to the transaction related to their finances. Still the majority of the population believe in going to banks and transacting their financials. So the customer belief in brick and mortar is considered to be the biggest restraints for the digital banking market. Most of the bank and financial institutions are spending a lot in their cyber security but it need to be out in front, going after the fraudsters and minimizing risks. The majority of the consumers are still not willing to take chances doing the transactions through online which is considered to be the biggest restrains for the growth of the digital banking market.

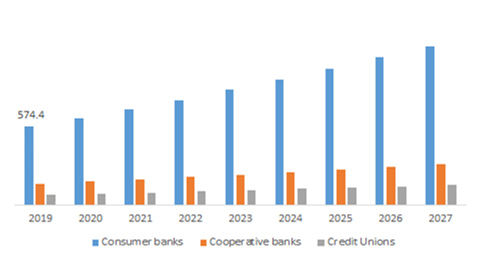

Digital Banking Market by Type:

The Consumer bank is predicted to be most profitable till the end of 2027

Source: Research Dive Analysis

The consumer banks segment accrued the largest share in the digital banking market. The significant growth in the consumer banks segment is highly attributed to the increasing top-line revenue, cost reductions, and moderating risks. Digital banking market size for consumer bank was valued at $574.4 billion in 2019, and is projected to reach $1,661.1 billion by 2027. Credit union was valued at $73.8 billion in 2019, and is projected to reach $146.1 billion by 2027, as most of the Credit Unions are a category of financial cooperatives that run their business as “non-profit” organizations. They are run by the people and for the people. They believe in serving their members as their core value, hence they initially serve their members in their physical branches and now moving completely into digitization.

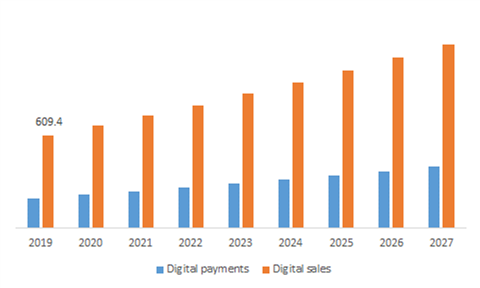

Digital Banking Market, by Services:

Digital payments will possess high investment opportunities in the coming future

Source: Research Dive Analysis

Based on service, the digital payments segment is expected to grow rapidly during the forecast period. The digital payments segment was valued at $194.5 billion in 2019, and is projected to reach $402.5 billion by 2027. The digital payment segment is the largest service segment in the digital banking market and expected to lead the market during the forecast period. The increasing sale of banking products and services through online platforms is driving the digital sales by banks across the globe. The digital sales segment was valued at $609.4 billion in 2019, and is projected to reach $1,207.5 billion by 2027.

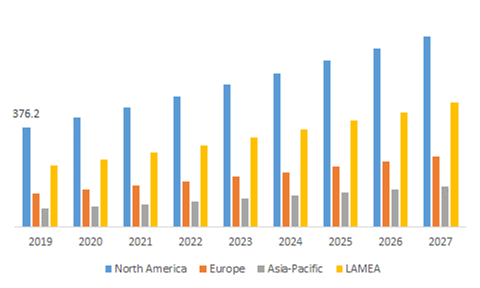

Digital Banking Market by Region

North America region will have enormous opportunities for the market investors to grow over the coming years

Source: Research Dive Analysis

The global digital banking market is examined across North America, Europe, Asia-Pacific, and LAMEA.

North America Digital Banking Market:

North America is expected to dominate the market throughout the forecast period. Preserving a customer for a lifetime is one of the major goals of most of the financial institutions. Hence, major American banks such as Bank of America and others are adopting key developmental strategies such as product launches and others so that they can preserve the customer and customer data to contact their existing customer for improving their sales. North America was valued at $376.2 billion in 2019, and is projected to reach $721.3 billion by 2027.

Asia Pacific Digital Banking Market:

The global digital banking market is largely driven by emerging countries in Asia-Pacific such as China, India and japan. The digital banking prospects in these several countries in Asia-Pacific are due to rising adoption of smartphones and initiatives which includes customer education programs and media promotions for mobile banking have led to this uptrend in Asia-Pacific. The Asia-Pacific regional market was valued at $69.9 billion in 2019, and is projected to reach $153.0 billion by 2027.

Key Participants in Digital Banking Market:

Source: Research Dive Analysis

The key players profiled in the digital banking market report include Industrial and Commercial Bank of China Limited, Bank of China Limited, China Construction Bank, Agricultural Bank of China, Wells Fargo, Bank of America, and Citigroup, JPMorgan Chase, HSBC Group, China Merchants Bank and among others.

Scope of the Market Report:

| Aspect | Particulars |

| Historical Market Estimations | 2017-2019 |

| Base Year for Market Estimation | 2019 |

| Forecast timeline for Market Projection | 2019-2027 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Services |

|

| Key Countries covered | U.S., Canada, Germany, France, UK, Italy, Japan, China, India, South Korea, Australia, Middle west, Africa |

| Key Companies Profiled |

|

Source: Research Dive Analysis

Q1. What is the size of Digital banking market?

A. The global Digital banking market size was over $ 803.8 billion in 2019, and is further anticipated to reach $1,610.00 billion by 2027.

Q2. Who are the leading companies in the Digital banking market?

A. Citi group and Wells Fargo are some of the key players in the global digital banking market.

Q3. Which region possess greater investment opportunities in the coming future?

A. North America possess great investment opportunities for the investors to witness the most promising growth in the coming years.

Q4. What is the growth rate of North America?

A. North America Digital banking market is projected to grow at 8.30% CAGR during the forecast period.

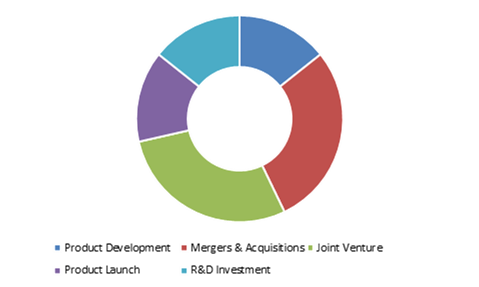

Q5. What are the strategies opted by the leading players in this market?

A. Product development, and joint ventures are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Wells Fargo, Bank of America and Citigroup are the companies investing more on R&D activities for developing new products and technologies.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.4.1. Assumptions

1.4.2. Forecast parameters

1.5. Data sources

1.5.1. Primary

1.5.2. Secondary

2. Executive Summary

2.1. 360° summary

2.2. Component trends

2.3. End-use trends

3. Market Overview

3.1. Market segmentation & definitions

3.2. Key takeaways

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.3. Porter’s five forces analysis

3.3.1. Bargaining power of consumers

3.3.2. Bargaining power of suppliers

3.3.3. Threat of new entrants

3.3.4. Threat of substitutes

3.3.5. Competitive rivalry in the market

3.4. Market dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Technology landscape

3.6. Regulatory landscape

3.7. Patent landscape

3.8. Strategic overview

4. Digital Banking Market, by Type

4.1. Credit union

4.1.1. Market size and forecast, by region, 2017-2028

4.1.2. Comparative market share analysis, 2018 & 2028

4.2. Co-operative Bank

4.2.1. Market size and forecast, by region, 2017-2028

4.2.2. Comparative market share analysis, 2018 & 2028

4.3. Consumer Bank

4.3.1. Market size and forecast, by region, 2017-2028

4.3.2. Comparative market share analysis, 2018 & 2028

5. Digital Banking Market, by Services

5.1. Digital Payments

5.1.1. Market size and forecast, by region, 2017-2028

5.1.2. Comparative market share analysis, 2018 & 2028

5.2. Digital sales

5.2.1. Market size and forecast, by region, 2017-2028

5.2.2. Comparative market share analysis, 2018 & 2028

6. Digital Banking Market, by Region

6.1. North Region

6.1.1. Market size and forecast, by type, 2017-2028

6.1.2. Market size and forecast, by application, 2017-2028

6.1.3. Market size and forecast, by end-use, 2017-2028

6.1.4. Market size and forecast, by country, 2017-2028

6.1.5. Comparative market share analysis, 2018 & 2028

6.1.6. U.S

6.1.6.1. Market size and forecast, by type, 2017-2028

6.1.6.2. Market size and forecast, by application, 2017-2028

6.1.6.3. Market size and forecast, by end-use, 2017-2028

6.1.6.4. Comparative market share analysis, 2018 & 2028

6.1.7. Canada

6.1.7.1. Market size and forecast, by type, 2017-2028

6.1.7.2. Market size and forecast, by application, 2017-2028

6.1.7.3. Market size and forecast, by end-use, 2017-2028

6.1.7.4. Comparative market share analysis, 2018 & 2028

6.2. Europe

6.2.1. Market size and forecast, by type, 2017-2028

6.2.2. Market size and forecast, by application, 2017-2028

6.2.3. Market size and forecast, by end-use, 2017-2028

6.2.4. Market size and forecast, by country, 2017-2028

6.2.5. Comparative market share analysis, 2018 & 2028

6.2.6. UK

6.2.6.1. Market size and forecast, by type, 2017-2028

6.2.6.2. Market size and forecast, by application, 2017-2028

6.2.6.3. Market size and forecast, by end-use, 2017-2028

6.2.6.4. Comparative market share analysis, 2018 & 2028

6.2.7. Germany

6.2.7.1. Market size and forecast, by type, 2017-2028

6.2.7.2. Market size and forecast, by application, 2017-2028

6.2.7.3. Market size and forecast, by end-use, 2017-2028

6.2.7.4. Comparative market share analysis, 2018 & 2028

6.2.8. France

6.2.8.1. Market size and forecast, by type, 2017-2028

6.2.8.2. Market size and forecast, by application, 2017-2028

6.2.8.3. Market size and forecast, by end-use, 2017-2028

6.2.8.4. Comparative market share analysis, 2018 & 2028

6.2.9. Italy

6.2.9.1. Market size and forecast, by type, 2017-2028

6.2.9.2. Market size and forecast, by application, 2017-2028

6.2.9.3. Market size and forecast, by end-use, 2017-2028

6.2.9.4. Comparative market share analysis, 2018 & 2028

6.2.10. Rest of Europe

6.2.10.1. Market size and forecast, by type, 2017-2028

6.2.10.2. Market size and forecast, by application, 2017-2028

6.2.10.3. Market size and forecast, by end-use, 2017-2028

6.2.10.4. Comparative market share analysis, 2018 & 2028

6.3. Asia-Pacific

6.3.1. Market size and forecast, by type, 2017-2028

6.3.2. Market size and forecast, by application, 2017-2028

6.3.3. Market size and forecast, by end-use, 2017-2028

6.3.4. Market size and forecast, by country, 2017-2028

6.3.5. Comparative market share analysis, 2018 & 2028

6.3.6. China

6.3.6.1. Market size and forecast, by type, 2017-2028

6.3.6.2. Market size and forecast, by application, 2017-2028

6.3.6.3. Market size and forecast, by end-use, 2017-2028

6.3.6.4. Comparative market share analysis, 2018 & 2028

6.3.7. India

6.3.7.1. Market size and forecast, by type, 2017-2028

6.3.7.2. Market size and forecast, by application, 2017-2028

6.3.7.3. Market size and forecast, by end-use, 2017-2028

6.3.7.4. Comparative market share analysis, 2018 & 2028

6.3.8. Japan

6.3.8.1. Market size and forecast, by type, 2017-2028

6.3.8.2. Market size and forecast, by application, 2017-2028

6.3.8.3. Market size and forecast, by end-use, 2017-2028

6.3.8.4. Comparative market share analysis, 2018 & 2028

6.3.9. South Korea

6.3.9.1. Market size and forecast, by type, 2017-2028

6.3.9.2. Market size and forecast, by application, 2017-2028

6.3.9.3. Market size and forecast, by end-use, 2017-2028

6.3.9.4. Comparative market share analysis, 2018 & 2028

6.3.10. Australia

6.3.10.1. Market size and forecast, by type, 2017-2028

6.3.10.2. Market size and forecast, by application, 2017-2028

6.3.10.3. Market size and forecast, by end-use, 2017-2028

6.3.10.4. Comparative market share analysis, 2018 & 2028

6.3.11. Rest of Asia Pacific

6.3.11.1. Market size and forecast, by type, 2017-2028

6.3.11.2. Market size and forecast, by application, 2017-2028

6.3.11.3. Market size and forecast, by end-use, 2017-2028

6.3.11.4. Comparative market share analysis, 2018 & 2028

6.4. LAMEA

6.4.1. Market size and forecast, by type, 2017-2028

6.4.2. Market size and forecast, by application, 2017-2028

6.4.3. Market size and forecast, by end-use, 2017-2028

6.4.4. Market size and forecast, by country, 2017-2028

6.4.5. Comparative market share analysis, 2018 & 2028

6.4.6. Latin America

6.4.6.1. Market size and forecast, by type, 2017-2028

6.4.6.2. Market size and forecast, by application, 2017-2028

6.4.6.3. Market size and forecast, by end-use, 2017-2028

6.4.6.4. Comparative market share analysis, 2018 & 2028

6.4.7. Middle East

6.4.7.1. Market size and forecast, by type, 2017-2028

6.4.7.2. Market size and forecast, by application, 2017-2028

6.4.7.3. Market size and forecast, by end-use, 2017-2028

6.4.7.4. Comparative market share analysis, 2018 & 2028

6.4.8. Africa

6.4.8.1. Market size and forecast, by type, 2017-2028

6.4.8.2. Market size and forecast, by application, 2017-2028

6.4.8.3. Market size and forecast, by end-use, 2017-2028

6.4.8.4. Comparative market share analysis, 2018 & 2028

7. Company Profiles

7.1. Industrial and Commercial Bank of China Limited

7.1.1. Business overview

7.1.2. Financial performance

7.1.3. Product portfolio

7.1.4. Recent strategic moves & developments

7.1.5. SWOT analysis

7.2. Bank of China Limited

7.2.1. Business overview

7.2.2. Financial performance

7.2.3. Product portfolio

7.2.4. Recent strategic moves & developments

7.2.5. SWOT analysis

7.3. China Construction Ban

7.3.1. Business overview

7.3.2. Financial performance

7.3.3. Product portfolio

7.3.4. Recent strategic moves & developments

7.3.5. SWOT analysis

7.4. Agricultural Bank of China

7.4.1. Business overview

7.4.2. Financial performance

7.4.3. Product portfolio

7.4.4. Recent strategic moves & developments

7.4.5. SWOT analysis

7.5. Wells Fargo.

7.5.1. Business overview

7.5.2. Financial performance

7.5.3. Product portfolio

7.5.4. Recent strategic moves & developments

7.5.5. SWOT analysis

7.6. Bank of America

7.6.1. Business overview

7.6.2. Financial performance

7.6.3. Product portfolio

7.6.4. Recent strategic moves & developments

7.6.5. SWOT analysis

7.7. Citi Group

7.7.1. Business overview

7.7.2. Financial performance

7.7.3. Product portfolio

7.7.4. Recent strategic moves & developments

7.7.5. SWOT analysis

7.8. HSBC Group

7.8.1. Business overview

7.8.2. Financial performance

7.8.3. Product portfolio

7.8.4. Recent strategic moves & developments

7.8.5. SWOT analysis

7.9. JPMorgan and chase.

7.9.1. Business overview

7.9.2. Financial performance

7.9.3. Product portfolio

7.9.4. Recent strategic moves & developments

7.9.5. SWOT analysis

What is Digital Banking?

Digital banking is the digitization (or going online) of all traditional banking operations and system offerings that have traditionally been accessible only to consumers when they are physically located within a bank branch. It covers things such as Withdrawals, Checking Account, software for applying for Financial Products, Bill Pay, Cash Deposits, Transfers, Management of Savings Account, Management of Debt, Account Services.

Consumer preferences quickly shifted to online and mobile apps, but many financial institutions are struggling to adapt their banking experience to electronic platforms and smaller mobile devices. Sadly, banks can no longer afford to wait to invest in digital innovation as consumers are rapidly willing to switch banking to digital services such as bill pay, mobile payments and loan applications.

The most important difference between digital banking and online banking versus conventional banking is that the interaction between the consumer and the digital bank begins and remains exclusively digitally without the need to enter any physical location. Nevertheless, digital banking is a move further than online banking.

Advantages of Digital Banking

Online banking helps businesses easily transfer expenses to their workers ' bank accounts. Some of the daily transactions can also be streamlined so that practitioners can use their valuable time for something more important.

This involves evaluating how the buyer connects with the company and adjusting those encounters to improve the customer experience. For example, information and context may be adjusted as a consumer transition from a mobile phone to a desktop or from reviewing a brand to making a purchase decision.

Digital banking is making life easier and cheaper. These are also preferred to chart the expenses. There are many benefits of online banking, some of which are, pay your bills electronically, switch funds between bank accounts, secure yourself digitally, anywhere on your device or mobile phone, monitor your transfers, less time consuming, syncing with your finance apps, permanent access to bank data.

Market trends

Government initiatives related to digital banking globally and promoting cashless where the government and the customer can hold each and every person accountable for their finances. The trends in the digital banking market have led to the increasing use of smartphones, the use of the Internet and the government initiative is seen as an opportunity for the market. As the growing population is turning towards technology, banks are also shifting their division into digital channels to offer their services with one contact to the consumer.

The affordability and user-friendliness of digital banking and the increasing use of electronic devices and easy access to internet services are the driving forces of the digital banking industry over the projected period. The technical development in the application of blockchain is a further expansion of the global digital banking industry. Whereas the could threat of data breaches and cyber-attacks can impede the growth of the digital banking industry.

Data breaches serve as a challenge to market growth.

The main drivers of the digital banking industry are cost-efficiency and ease of use of digital banking compared to the normal banking system. Factors such as growth in the adoption rate of electronic gadgets, and convenient access to high-speed Internet networks, are projected to fuel the demand during the forecast period. Nevertheless, the growing threat of data breaches and cyber-attacks on banking servers can impede the forecasting of the digital banking industry. In turn, technological advances, such as the introduction of blockchain technologies, further boost the global digital banking market.

Mobile banking trends are contributing to the growing use of smartphones and Internet adoption across the globe, and banks are shifting into digital channels to provide their services. The government is also promoting and increasing the use of digital banking services across various global initiatives. The aim of the governments of different countries to become cashless has contributed to the introduction of a number of policies, such as demonetization, which promotes and enables different traders to incorporate digital payments. Furthermore, no merchant discount rate (MDR) or taxes would be levied on either retailers or consumers.

As a result, such regulations and government support are expected to further expand the digital banking market worldwide. They are also collaborating in partnership with FinTech Corporations and other third-party applications to create additional user-centric products and services while offering improved customer experience. For eg, in November 2019, the Government of India introduced a regulation on businesses with an annual turnover of more than $7.0 million to offer low-cost digital means of payment through digital mediums, like BHIM UPI, RTGS, NEFT, Aadhaar Pay, debit cards, UPI-QR Code to customers.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com