Global Artificial Intelligence In Construction Market Report

RA00046

Global Artificial Intelligence in Construction Market by Offerings (Solutions and Services), Deployment Type (Cloud and On-premises), Organization Size (Small & Medium-sized Enterprises (SMEs) and Large Enterprises), Industry Type (Residential, Institutional Commercials and Others), and Region (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast 2022–2031

Global Artificial Intelligence in Construction Market Analysis

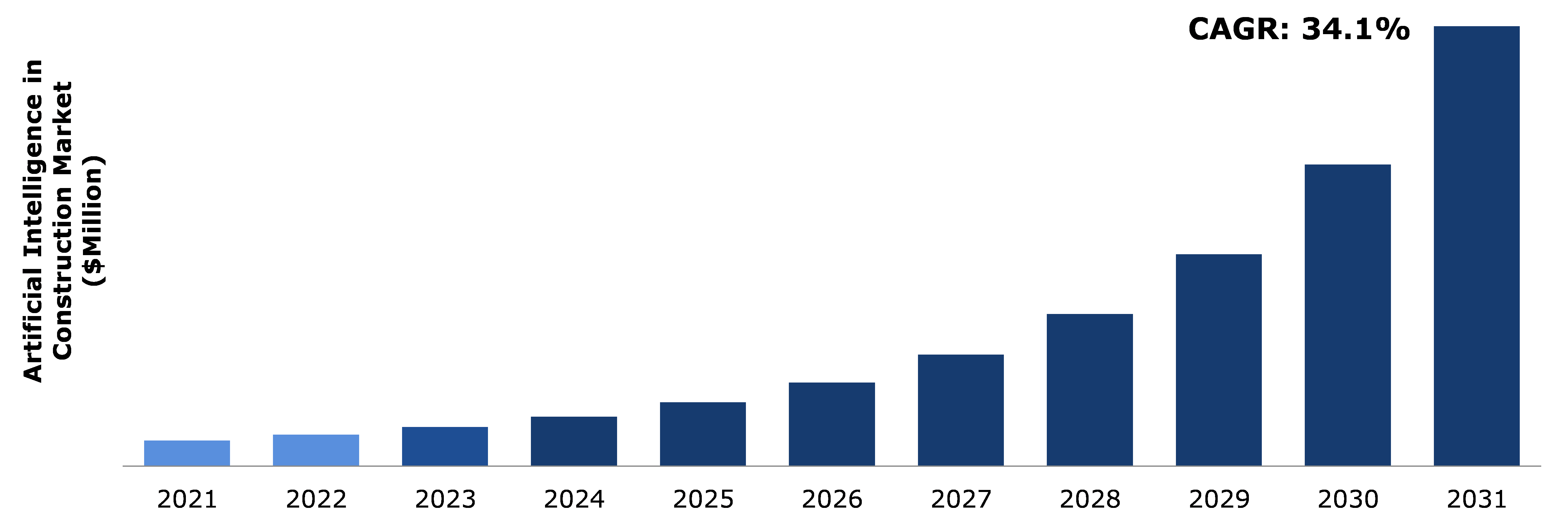

The Global Artificial Intelligence in Construction Market Size was $496.40 million in 2021and is predicted to grow with a CAGR of 34.1%, by generating revenue of $8,545.80 million by 2031.

Global Artificial Intelligence in Construction Market Synopsis

The implementation of artificial intelligence technology to improve worker safety on building sites and lessen health risks in the construction industry is expected to drive the global artificial intelligence in construction market growth in the coming years. By 2020, "one in five worker deaths per year were recorded from the construction sector," according to the Occupational Safety and Health Administration (OSHA), a department of labor of the United States regulating organization. It is important to address the increasing fatality rate at building sites. Construction sites are typically outfitted with safety equipment such as cameras, sensors, and IoT devices that detect various aspects of construction activities and alert the crew if a safety issue is likely to occur. These factors are anticipated to boost the artificial intelligence in construction market share in the upcoming years.

However, one of the main obstacles is regarded as a lack of skilled labor. The work that needs to be done in the construction industry with the aid of artificial intelligence requires both technical and domain knowledge to produce the desired results. If the worker does not have a solid understanding of it, the entire project prediction and off-site construction work fails, which can result in a significant loss for the business and subject the business to a number of project-related challenges. This factor restrains the market growth.

A number of market participants in artificial intelligence (AI) in construction are consistently investing in the R&D division to advance the technology used in AI-integrated building and construction equipment. For instance, in March 2020, The Newmetrix's construction-trained AI engine named "Vinnie" was upgraded with additional features like the ability to detect workers in a group and identify work at height concerns. Such technological developments convince businesses to use artificial intelligence at construction sites to reduce health hazards, enhance job quality, and reduce operational costs, which is predicted to accelerate the artificial intelligence in construction market demand.

According to regional analysis, the North American artificial intelligence in construction accounted for the highest market size in 2021. This is because North America has a huge population base, with high purchasing power, constant investment in the automation, and government initiatives in artificial intelligence in the construction sector.

Artificial Intelligence in Construction Overview

Artificial intelligence (AI) technology is used to streamline tasks and lower their inherent hazards. AI is being used in the construction sector to make job sites safer for human laborers and cut expenses for the business. For engineers and workers to work effectively and to use technology whenever necessary, AI technology is built into the core of the machinery.

COVID-19 Impact on Global Artificial Intelligence in Construction Market

The outbreak of the COVID-19 impact on artificial intelligence in construction market has resulted in the implementation of the worldwide industrial and economic shutdown as well as the lockdown situation. Additionally, the industrial and construction sectors were entirely shut down, which led to a reduction in employment. In addition, it is possible to connect the slowing expansion of the global AI in construction market to the growing need to uphold COVID-19 safety measures such social segregation to stop the virus from spreading. Artificial intelligence in the construction sector has been greatly influenced by COVID-19. Lower market cash flow had a substantial negative influence on the construction industry, which has led to certain construction firms ceasing operations due to a lack of financial liquidity. The potential for the global artificial intelligence (AI) in construction market has been lowered as a result of several industries and enterprises adopting work-from-home models to battle the spread of the COVID-19 pandemic. The importance of industrial enterprises' digital transformation projects, including the AI-enabled machinery in their production units, has decreased as a result of these circumstances. Increasing investments in cutting-edge technologies, like AI, to develop remote operating capabilities, like industrial robots, process automation, autonomous material movement, and predictive maintenance and machinery inspection, has been suggested by a number of AI and automation experts as a way to lower worker density.

Rise in Applications of Artificial Intelligence in Construction Sector to Drive the Market Growth

The construction industry has already seen a considerable impact from AI. AI can help with all phases of a construction project, from design and planning to managing operations and creating safer work areas. In the construction industry, AI is already demonstrating its value with a new degree of automation and workflow efficiency. This element is driving market growth. Additionally, utilizing AI and machine intelligence on construction sites lowers the possibility of accidents. AI systems can anticipate any problems with safety, quality, and productivity since they can swiftly receive and evaluate massive amounts of data in real time. AI is not only capable of seeing risky behavior or potential risks on the job site, but it can also foresee machine malfunctions using sensor data and decide what corrective measures to take. This lowers the likelihood of mishaps and increases worker safety on construction sites.

To know more about global artificial intelligence in construction market drivers, get in touch with our analysts here.

High Cost and High Maintenance Charges to Restrain the Artificial Intelligence in Construction Market Size

The use of artificial intelligence-based robots in the construction sector can be quite expensive because they are extremely complicated pieces of equipment that cost a lot to fix and maintain. To meet the demands of the continuously changing environment, they have software programs that require periodic updating. Using a machine to perform a task is neither simple nor inexpensive. As a result, only large businesses that can afford them will be able to invest. Robots are limited to the tasks they have been designed to complete. Outside of the programming that is contained in their internal circuits and firmware, they are unable to behave any differently. These factors are anticipated to restrain the artificial intelligence in construction industry share in the coming years.

Increase in Need for Intelligent Business Process to Drive Excellent Opportunities

The growth of digital information is another factor fueling the construction industry's expansion. The development of digital knowledge has speed up during the past five years as a result of increased use of building information systems (BIM), security sensors, drones, and machine telematics. This typically motivates construction firms to use cutting-edge analytics tools to fully leverage the enormous amount of digital data and gain insights. Drones, robots, and autonomous vehicles are being used more and more in the construction industry, which is assisting AI's expansion in this sector. Large number of construction companies are using these technologies to map, take aerial photos, assess construction sites, and automate development procedures. This frequently creates a wide range of artificial intelligence in construction market opportunities during the forecast period.

To know more about global artificial intelligence in construction market opportunities, get in touch with our analysts here.

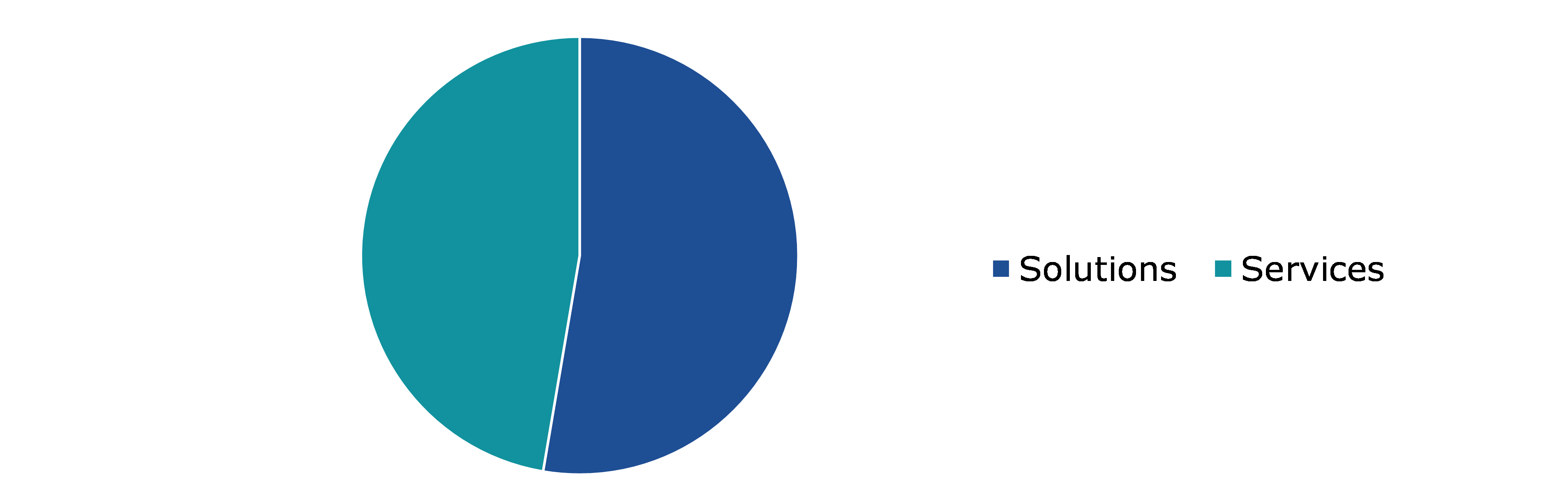

Global Artificial Intelligence in Construction Market, by Offerings

Based on offerings, the market has been divided into solutions and services. Among these, the solutions sub-segment accounted for the highest market share in 2021, whereas the services sub-segment is estimated to show the fastest growth during the forecast period.

Global Artificial Intelligence in Construction Market Size, by Offerings, 2021

Source: Research Dive Analysis

The solutions sub-type is anticipated to have a dominant market share in 2021.The rise is mostly attributable to the market's growing originality, innovation, and accessibility of AI-based building activity solutions. Building and construction companies are increasingly utilizing AI solutions to complete various construction projects. The construction process is becoming more efficient owing to artificial intelligence (AI) solutions, which have important applications in areas like supply chain management, project planning, and risk management. These are predicted to be the major factors driving the artificial intelligence in construction market size during the forecast period.

The services sub-type is anticipated to show the fastest growth during the forecast period. Artificial intelligence in construction services are being used to monitor the interactions between personnel, equipment, and items at the job site in real-time and notify managers of any potential safety hazards, design flaws, or productivity problems. The use of AI services in construction is growing, which increases the demand for worker training services and for proper technology installation and maintenance.

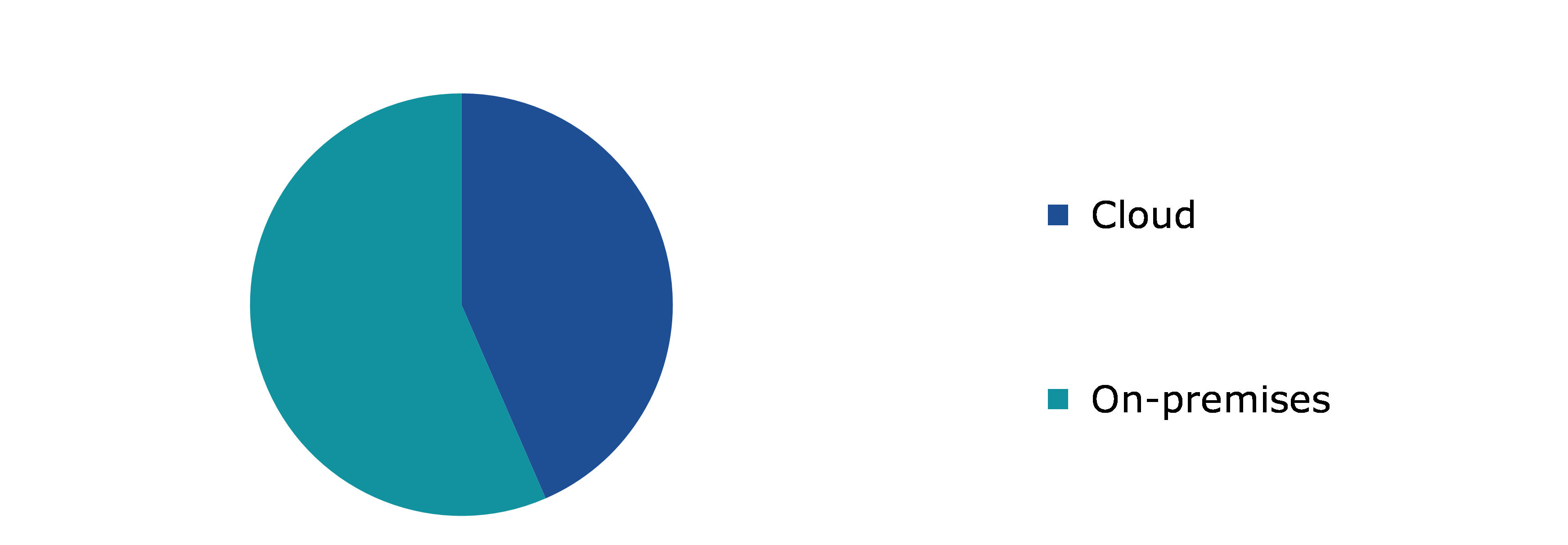

Global Artificial Intelligence in Construction Market, by Deployment Type

Based on deployment type, the market has been divided into cloud and on-premises. Among these, the on-premises sub-segment accounted for the highest market size in 2021 and the cloud sub-segment accounted for fastest growth in 2031.

Global Artificial Intelligence in Construction Market Share, by Deployment Type, 2021

Source: Research Dive Analysis

The cloud sub-segment is anticipated to show the fastest growth during the forecast period. Some of the main benefits of employing a cloud deployment include flexibility, disaster recovery, automated software upgrades, capital expense-free, increased collaboration, work from anywhere, document management, security, competitiveness, and environmental friendliness. Investors are also supporting the creation of computer-aided virtual environments that will provide customers, architects, and builders with a virtual experience of a buildings. These factors are anticipated to boost the growth of cloud sub-segments during the analysis timeframe.

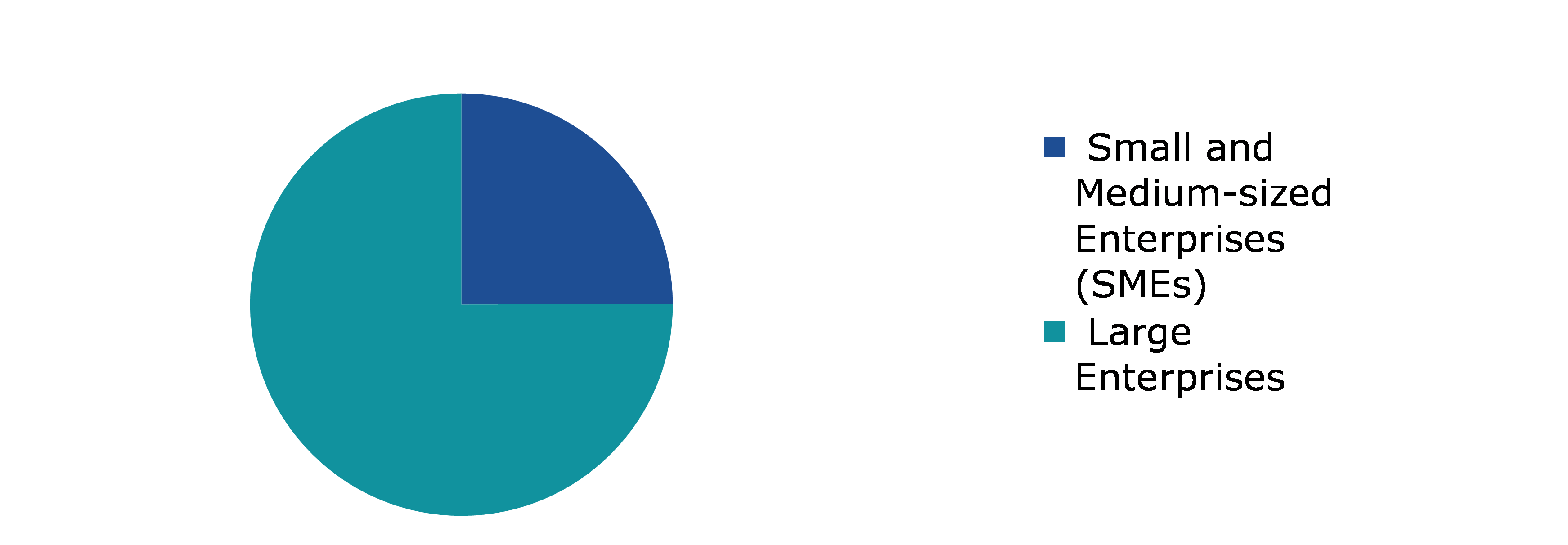

Global Artificial Intelligence in Construction Market, by Organization Size

Based on organization size, the market has been divided into small and medium-sized enterprises (SMEs) and large enterprises. Among these, the large enterprises sub-segment accounted for the highest market share in 2021.

Global Artificial Intelligence in Construction Market Trends, by Organization Size, 2021

Source: Research Dive Analysis

The large enterprises sub-segment accounted for the highest market size in 2021. Large enterprises are anticipated to hold a larger market share as a result of the construction industry's rising investment in artificial intelligence. Many companies have developed artificial intelligence solutions for the large enterprises operating in the construction sector. For instance, Procore Technologies, provides solutions for workers that are enabled by AI. The company provides historical analysis for more accurate forecasts and makes use of machine learning to identify patterns and extract trends from larger information. Customers can take use of the solution's powerful data visualization by using the industry-sourced templates or by developing their own custom reports. These factors are anticipated to boost the growth of large enterprises sub-segment during the analysis timeframe.

Global Artificial Intelligence in Construction Market, by Industry Type

Based on industry type, the market has been divided into residential, institutional commercials and others. Among these, the others sub-segment accounted for the highest market share in 2021.

Global Artificial Intelligence in Construction Market Growth, by Industry Type, 2021

Source: Research Dive Analysis

The others sub-segment accounted for the highest market size in 2021. Buildings such as stadiums, schools, hospitals, malls, libraries, art galleries, and museums are examples of constructions that fall under this category. Public structures, including hospitals, schools, and recreation facilities, largely use artificial intelligence in construction services and solutions to ensure timely complete of projects. These factors are anticipated to boost the growth of the others sub-segment during the analysis timeframe.

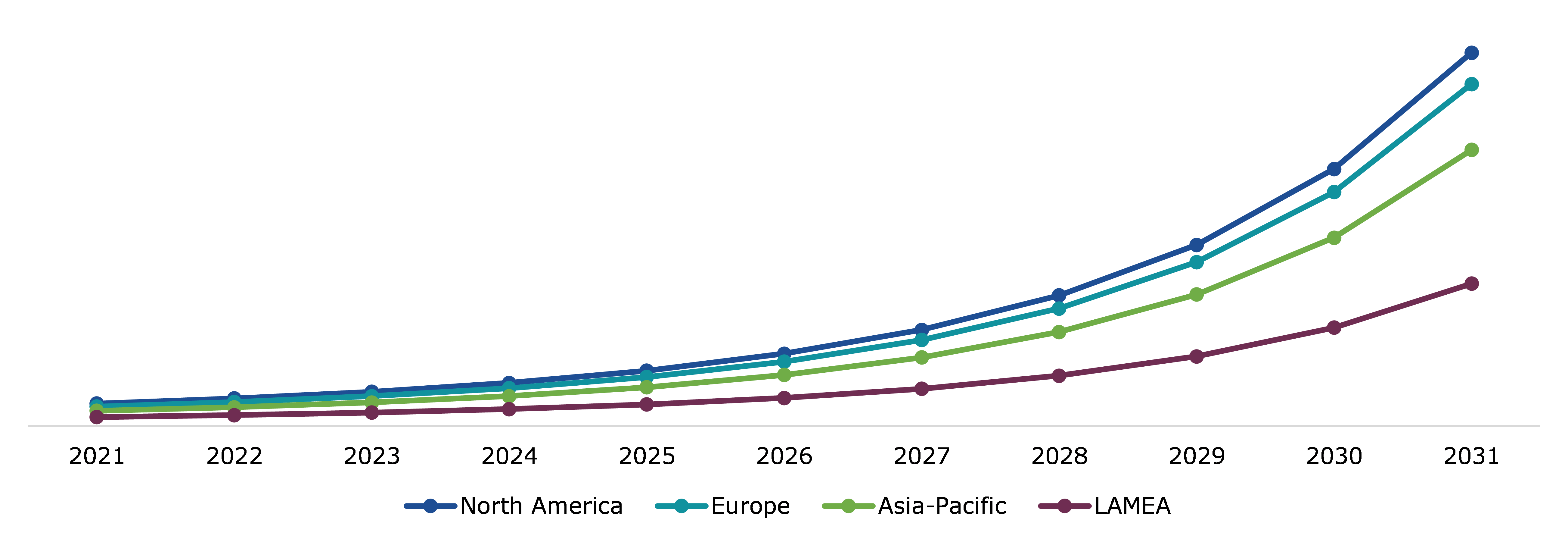

Global Artificial Intelligence in Construction Market, Regional Insights

The artificial intelligence in construction market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Artificial Intelligence in Construction Market Size & Forecast, by Region, 2021-2031 (USD Million)

Source: Research Dive Analysis

The Market for Artificial Intelligence in Construction in North America to be the most Dominant

The North American artificial intelligence in construction market analysis accounted for largest share in 2021. The market has seen significant expenditures from construction corporations in the North American region, as numerous vendors have emerged to serve the fast-expanding sector. Artificial intelligence (AI) technologies are successfully employed in North America for a wide range of applications, including supply chain management, risk management, schedule management, project management, and others (equipment and construction materials management, resource management, subcontractor management, and cost management). Furthermore, the region's dominance is due to its advanced technological infrastructure and the presence of many major AI companies in the area's construction industry. For instance, in April 2021, IBM Corporation, Red Hat Software, and Cobuilder announced a global partnership to co-build a new platform that will be intended to assist in tying the dispersed supply chain of the construction industry. The platform, known as OpenBuilt, is anticipated to provide a cutting-edge digital solution to benefit from innovation and drive safer, more efficient, and sustainable construction projects. The market players operating in the area offer improvements, innovations, and significant market investment that contribute to the overall expansion of the AI in construction market.

The Market for Artificial Intelligence in Construction in Asia-Pacific to Show the Fastest Growth

The growing demand for artificial intelligence in construction in this region is attributed to increase in construction activities in the countries such as China, Japan, India, and others. For instance, in India, increasing infrastructure projects in India is expected to drive the overall construction market. Government in the country has launched many construction projects. For instance, in between 2015 and 2035, The Sagarmala Project, an initiative by the government of India to provide boost the logistics sector. This initiative was launched on 31 July 2015. The Sagarmala Program has implemented more than 610 projects (costing INR 7.78 crores) in the fields of port modernization and new port development, port-linked industry, and coastal community development, port connectivity enhancement.

Competitive Scenario in the Global Artificial Intelligence in Construction Market

Investment and agreement are common strategies followed by major market players. For instance, on April 7, 2022, Deepomatic, the leader in visual automation for telecommunications, announced a partnership with Polish system integrator VECTOR SOLUTIONS to provide its AI-powered image recognition solution to all telecom operators in Poland, accelerating the rollout of fiber optics in the country.

Source: Research Dive Analysis

Some of the leading artificial intelligence in construction market players are Deepomatic, COINS Global, Beyond Limits Inc., Doxel, Askporter, Autodesk, Inc., Renoworks Software, Inc., Building System Planning, Inc., Bentley Systems, Incorporated, and Predii.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Offerings |

|

| Segmentation by Deployment Type |

|

| Segmentation by Organization Size |

|

| Segmentation by Industry Type |

|

| Key Companies Profiled |

|

Q1. What is the size of the global artificial intelligence in construction market?

A. The size of the global artificial intelligence in construction market was over $496.4 million in 2021 and is projected to reach $8,545.8 million by 2031.

Q2. Which are the major companies in the artificial intelligence in construction market?

A. Deepomatic, COINS Global, Beyond Limits Inc., and Doxel are some of the key players in the global artificial intelligence in construction market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific artificial intelligence in construction market?

A. Asia-Pacific artificial intelligence in construction market is anticipated to grow at 34.9% during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Building System Planning, Inc., Bentley Systems, Incorporated, and Predii are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global artificial intelligence in construction market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of service providers

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Patent matrix

4.4.3.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Artificial Intelligence in Construction Market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Artificial Intelligence in Construction Market Analysis, by Offerings

5.1.Overview

5.2.Solutions

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2021-2031

5.2.3.Market share analysis, by country, 2021-2031

5.3.Services

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2021-2031

5.3.3.Market share analysis, by country, 2021-2031

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Artificial Intelligence in Construction Market Analysis, by Deployment Type

6.1.Cloud

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2021-2031

6.1.3.Market share analysis, by country, 2021-2031

6.2.On-premises

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2021-2031

6.2.3.Market share analysis, by country, 2021-2031

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Artificial Intelligence in Construction Market, by Organization Size

7.1.Small and Medium-sized Enterprises (SMEs)

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region, 2021-2031

7.1.3.Market share analysis, by country, 2021-2031

7.2.Large Enterprises

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2021-2031

7.2.3.Market share analysis, by country, 2021-2031

7.3.Research Dive Exclusive Insights

7.3.1.Market attractiveness

7.3.2.Competition heatmap

8.Artificial Intelligence in Construction Market, by Industry type

8.1.Residential

8.1.1.Definition, key trends, growth factors, and opportunities

8.1.2.Market size analysis, by region, 2021-2031

8.1.3.Market share analysis, by country, 2021-2031

8.2. Institutional Commercials

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region, 2021-2031

8.2.3.Market share analysis, by country, 2021-2031

8.3.Others

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region, 2021-2031

8.3.3.Market share analysis, by country, 2021-2031

8.4.Research Dive Exclusive Insights

8.4.1.Market attractiveness

8.4.2.Competition heatmap

9.Artificial Intelligence in Construction Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Offerings, 2021-2031

9.1.1.2.Market size analysis, by Deployment Type, 2021-2031

9.1.1.3.Market size analysis, by Organization Size, 2021-2031

9.1.1.4.Market size analysis, by Industry Type, 2021-2031

9.1.2.Canada

9.1.2.1.Market size analysis, by Offerings, 2021-2031

9.1.2.2.Market size analysis, by Deployment Type, 2021-2031

9.1.2.3.Market size analysis, by Organization Size, 2021-2031

9.1.2.4.Market size analysis, by Industry Type, 2021-2031

9.1.3.Mexico

9.1.3.1.Market size analysis, by Offerings, 2021-2031

9.1.3.2.Market size analysis, by Deployment Type, 2021-2031

9.1.3.3.Market size analysis, by Organization Size, 2021-2031

9.1.3.4.Market size analysis, by Industry Type, 2021-2031

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Offerings, 2021-2031

9.2.1.2.Market size analysis, by Deployment Type, 2021-2031

9.2.1.3.Market size analysis, by Organization Size, 2021-2031

9.2.1.4.Market size analysis, by Industry Type, 2021-2031

9.2.2.UK

9.2.2.1.Market size analysis, by Offerings, 2021-2031

9.2.2.2.Market size analysis, by Deployment Type, 2021-2031

9.2.2.3.Market size analysis, by Organization Size, 2021-2031

9.2.2.4.Market size analysis, by Industry Type, 2021-2031

9.2.3.France

9.2.3.1.Market size analysis, by Offerings, 2021-2031

9.2.3.2.Market size analysis, by Deployment Type, 2021-2031

9.2.3.3.Market size analysis, by Organization Size, 2021-2031

9.2.3.4.Market size analysis, by Industry Type, 2021-2031

9.2.4.Spain

9.2.4.1.Market size analysis, by Offerings, 2021-2031

9.2.4.2.Market size analysis, by Deployment Type, 2021-2031

9.2.4.3.Market size analysis, by Organization Size, 2021-2031

9.2.4.4.Market size analysis, by Industry Type, 2021-2031

9.2.5.Italy

9.2.5.1.Market size analysis, by Offerings, 2021-2031

9.2.5.2.Market size analysis, by Deployment Type, 2021-2031

9.2.5.3.Market size analysis, by Organization Size, 2021-2031

9.2.5.4.Market size analysis, by Industry Type, 2021-2031

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Offerings, 2021-2031

9.2.6.2.Market size analysis, by Deployment Type, 2021-2031

9.2.6.3.Market size analysis, by Organization Size, 2021-2031

9.2.6.4.Market size analysis, by Industry Type, 2021-2031

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia-Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Offerings, 2021-2031

9.3.1.2.Market size analysis, by Deployment Type, 2021-2031

9.3.1.3.Market size analysis, by Organization Size, 2021-2031

9.3.1.4.Market size analysis, by Industry Type, 2021-2031

9.3.2.Japan

9.3.2.1.Market size analysis, by Offerings, 2021-2031

9.3.2.2.Market size analysis, by Deployment Type, 2021-2031

9.3.2.3.Market size analysis, by Organization Size, 2021-2031

9.3.2.4.Market size analysis, by Industry Type, 2021-2031

9.3.3.India

9.3.3.1.Market size analysis, by Offerings, 2021-2031

9.3.3.2.Market size analysis, by Deployment Type, 2021-2031

9.3.3.3.Market size analysis, by Organization Size, 2021-2031

9.3.3.4.Market size analysis, by Industry Type, 2021-2031

9.3.4.Australia

9.3.4.1.Market size analysis, by Offerings, 2021-2031

9.3.4.2.Market size analysis, by Deployment Type, 2021-2031

9.3.4.3.Market size analysis, by Organization Size, 2021-2031

9.3.4.4.Market size analysis, by Industry Type, 2021-2031

9.3.5.South Korea

9.3.5.1.Market size analysis, by Offerings, 2021-2031

9.3.5.2.Market size analysis, by Deployment Type, 2021-2031

9.3.5.3.Market size analysis, by Organization Size, 2021-2031

9.3.5.4.Market size analysis, by Industry Type, 2021-2031

9.3.6.Rest of Asia-Pacific

9.3.6.1.Market size analysis, by Offerings, 2021-2031

9.3.6.2.Market size analysis, by Deployment Type, 2021-2031

9.3.6.3.Market size analysis, by Organization Size, 2021-2031

9.3.6.4.Market size analysis, by Industry Type, 2021-2031

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Offerings, 2021-2031

9.4.1.2.Market size analysis, by Deployment Type, 2021-2031

9.4.1.3.Market size analysis, by Organization Size, 2021-2031

9.4.1.4.Market size analysis, by Industry Type, 2021-2031

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Offerings, 2021-2031

9.4.2.2.Market size analysis, by Deployment Type, 2021-2031

9.4.2.3.Market size analysis, by Organization Size, 2021-2031

9.4.2.4.Market size analysis, by Industry Type, 2021-2031

9.4.3.UAE

9.4.3.1.Market size analysis, by Offerings, 2021-2031

9.4.3.2.Market size analysis, by Deployment Type, 2021-2031

9.4.3.3.Market size analysis, by Organization Size, 2021-2031

9.4.3.4.Market size analysis, by Industry Type, 2021-2031

9.4.4.South Africa

9.4.4.1.Market size analysis, by Offerings, 2021-2031

9.4.4.2.Market size analysis, by Deployment Type, 2021-2031

9.4.4.3.Market size analysis, by Organization Size, 2021-2031

9.4.4.4.Market size analysis, by Industry Type, 2021-2031

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Offerings, 2021-2031

9.4.5.2.Market size analysis, by Deployment Type, 2021-2031

9.4.5.3.Market size analysis, by Organization Size, 2021-2031

9.4.5.4.Market size analysis, by Industry Type, 2021-2031

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.Deepomatic

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.COINS Global

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.Beyond Limits Inc.

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.Doxel

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.Askporter

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.Autodesk, Inc.

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.Renoworks Software Inc.

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.Building System Planning, Inc.

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.Bentley Systems, Incorporated

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Predii

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

Artificial Intelligence (AI) is revolutionizing various industries, and the construction industry is no exception. The construction industry has traditionally been labor-intensive and has lagged behind other industries in adopting new technologies. However, with the advancement of AI, the construction industry is now embracing the use of intelligent systems, which has led to improved efficiency, increased productivity, and reduced costs. AI-powered systems can optimize the design process in the construction industry by analyzing vast amounts of data, identifying patterns and trends, and recommending the most efficient designs. This can help architects and engineers make better decisions and produce more effective designs.

Forecast Analysis of the Global Artificial Intelligence in Construction Market

The increasing applications of AI in the construction industry such as designing and planning, managing operations, and anticipating the massive amount of data in real-time are expected to fortify the growth of the artificial intelligence in construction market during the estimated period. Besides, the growing utilization of AI and machine intelligence on construction sites reduces the possibility of accidents and provides safer work areas for laborers which is expected to augment the growth of the market over the analysis timeframe. Moreover, the increasing need for intelligent business processes in the construction sector such as the use of building information systems (BIM), machine telematics, security sensors, and many more are predicted to create huge growth opportunities for the market during the forecast period. However, the high cost and maintenance charges of artificial intelligence robots in the construction industry may hamper the growth of the market throughout the analysis period.

According to the report published by Research dive, the global artificial intelligence in construction market is envisioned to garner $8,545.80 million and rise at an incredible CAGR of 34.1% over the forecast period from 2022 to 2031. The major players of the market include Autodesk, Inc., Askporter, Renoworks Software, Inc., Doxel, Building System Planning, Inc., Beyond Limits Inc., Bentley Systems, Incorporated, COINS Global, Predii, Deepomatic, and many more.

Artificial Intelligence in Construction Market Developments

The key companies operating in the industry are adopting various growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, which is subsequently helping the global artificial intelligence in construction market to grow exponentially. For instance:

- In May 2021, Procore Technologies, Inc., a renowned provider of construction management software, announced its acquisition of INDUS.AI, the world’s most advanced construction intelligence solution. This acquisition would add computer vision capabilities to the Procure platform, and help owners and contractors to realize greater efficiencies, safety, and profitability.

- In March 2022, Slate Technologies, the world's first understanding-driven data aggregation, analytics, and collaboration platform for the construction industry launched a digital assistant for the construction sector. This would promote the productivity of construction professionals by improving the decision-making process to keep building projects on time while maximizing revenue.

- In October 2022, ConstructConnect, a leading provider of software solutions announced its partnership with Togal.AI, a leading provider of takeoff software powered by deep machine learning. With this partnership, the companies aimed to expand the use of machine learning artificial intelligence in nonresidential preconstruction.

Most Profitable Region

The North America region of the artificial intelligence in construction market generated the highest revenue in 2021 and is predicted to continue a steady growth during the forecast period. This is mainly due to the increasing incorporation of AI in this region in a variety of applications including supply chain management, schedule management, risk management, and others. Additionally, the strong existence of major AI companies in the areas of construction industry and the presence of advanced technological infrastructure are expected to drive the regional growth of the market over the analysis timeframe.

Covid-19 Impact on the Artificial Intelligence in Construction Market

The outbreak of the Covid-19 pandemic has badly affected the artificial intelligence in construction market, likewise various other industries. This is mainly due to the shutdown of industrial and construction sectors owing to the spontaneous spread of the deadly virus. Moreover, the growing adoption of the work-from-home model by several enterprises and industries has lowered the potential of AI-enabled machinery in various production units. All these factors have declined the growth of the market over the period of crisis.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com