Managed Services Market Report

RA00388

Managed Services Market by Organization Size (SME and Large), Deployment Type (Cloud and On-premise), Service Type (Security Services, Network Services, Data Center & IT Infra Services, Communication & Collaboration Services, Mobility Services, and Information Services), Industry Vertical (Telecom, IT, BFSI, Consumer Goods & Retail, Manufacturing, Healthcare, Education, Energy & Utilities, Media & Entertainment, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2031

Global Managed Services Market Analysis

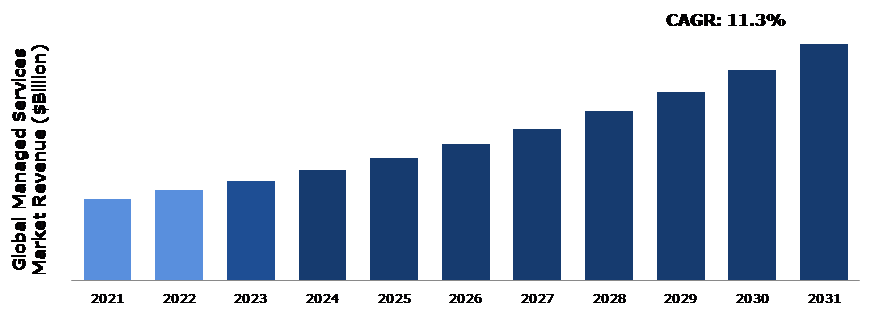

The Global Managed Services Market Size was $205.5 billion in 2021 and is predicted to grow with a CAGR of 11.3%, by generating a revenue of $594.8 billion by 2031.

Global Managed Services Market Synopsis

The rising demand for IT services is a major factor driving the managed services market demand. The complexity of IT infrastructure has increased substantially as businesses have become more dependent on technology, and managing numerous devices and apps may be difficult. To help businesses manage their IT requirements more effectively and efficiently, managed services providers offer expertise and resources. Managed services providers can offer services such as security, data backup and recovery, network monitoring, and help desk support in addition to managing IT infrastructure. Businesses that lack the internal resources or ability to accomplish these duties on their own may find these services to be greatly beneficial. As businesses become more dependent on technology, there will certainly be an increase in demand for IT services. As more businesses opt for managed services providers to help them in managing their IT requirements, this is likely to drive the growth of the managed services industry. These factors are anticipated to boost the managed services market expansion in the upcoming years.

However, the lack of skilled talent is a significant disadvantage for managed services providers. The need for knowledgeable IT workers has increased as technology has developed, but there has not been a comparable rise in the number of these individuals. This has led to a skill scarcity in the sector, making it challenging for managed services providers to find and maintain the staff they need to offer their clients high-quality services. It could increase competition for the limited amount of available talent, making it difficult for smaller suppliers to compete with bigger ones. It could force service providers to hire less qualified or experienced employees, which might lower the standard of the services provided. All these factors are anticipated to hamper the market revenue growth during the forecast period.

The managed services' major benefit for companies is its scalability. Managed services are readily scaled up or down to meet the demands of developing and evolving businesses. This implies that companies can avoid the expenses and hazards related to having to manage their IT infrastructure or hire and educate personnel to perform these responsibilities. Providers of managed services often offer a variety of services, ranging from straightforward monitoring and upkeep to more sophisticated assistance and control. This enables companies to select the service level that best meets their requirements and to modify that level as those requirements change over time. In addition, managed services providers often have the resources and expertise to quickly deploy new technology or upgrade existing systems, which can help businesses stay competitive in a rapidly changing market.

According to regional analysis, the North America managed services market accounted for the highest market share in 2021. A considerable shift towards managed security services is also being seen in the North American market, owing to rising cyber security risks and rules. Organizations may reduce cyber threats and comply with regulations with the aid of managed security services. The demand for managed services is anticipated to remain high in North America across a variety of sectors, including manufacturing, financial services, healthcare, and retail.

Managed Services Overview

Managed services is a business model where a third-party service provider manages and maintains a company's technology and infrastructure on an ongoing basis. This allows businesses to outsource their IT operations and focus on their core business functions. Managed services can encompass a wide range of services, including monitoring and maintaining servers, networks, and applications, providing help desk and technical support, managing security and backups, and providing consulting and strategic planning services.

COVID-19 Impact on Global Managed Services Market

The COVID-19 pandemic had a significant impact on the managed services market. The pandemic led to an increase in the demand for managed services in certain areas, such as cloud computing and security. The shift to remote work and the increase in use of cloud services led to an increase in demand for managed services related to cloud computing and cybersecurity. Many organizations were looking to outsource their operations and focus on their core business, which increased the demand for managed services. The pandemic accelerated the digital transformation of businesses, which increased the demand for managed services related to digitalization. It had also negatively impacted the market in other areas, such as on-premises managed services. The pandemic negatively impacted the market for on-premises managed services, as many organizations shifted to cloud-based services. The economic downturn caused by the pandemic led to budget cuts, which affected the demand for managed services. The supply chain disruptions caused by the pandemic impacted the delivery of managed services, leading to delays in services and increased costs.

The COVID-19 pandemic accelerated the adoption of managed services, and this trend is likely to continue in the post-pandemic pandemic. While the COVID-19 pandemic had both positive and negative impacts on the managed services market, the trend towards digitalization and the increasing need for cybersecurity are expected to drive the growth of the market in the upcoming years.

Rising Adoption of Cloud Computing Services to Drive the Market Growth

The rising adoption of cloud computing services is a major growth factor of the managed services market. Several managed service providers (MSPs) now offer cloud services between Amazon Web Services (AWS), Microsoft Azure, and Google Compute Platform (GCP), as well as migration services to help customers move from private to public clouds. MSPs can sell the cloud services, administer and optimize cloud services, and assist in moving the apps to the cloud. The industry is expanding quickly, and there are a lot of mergers and acquisitions (M&A) activities as MSPs compete to offer unique cloud-managed services that allow them to assist businesses in entering new markets more quickly, effectively, and affordably. Businesses are concentrating on their core operations, which leads to higher use of cloud-managed services. Major categories in the market for cloud-managed services include business services, security services, network services, data center services, and mobility services. The use of these services will increase productivity while also assisting businesses in lowering their IT and operational expenditures. These factors are anticipated to drive the managed services industry growth in the upcoming years.

To know more about global managed services market drivers, get in touch with our analysts here.

Data Security Concerns to Restrain the Market Growth

The amount of data being generated and stored is continuing to increase tremendously as organizations depend more on technology to manage their operations. Data security is a crucial part of managed services. Various types of data security concerns such as data loss, data breaches, third-party risks, and others are expected to hamper the market growth. Data breaches may result when there is unauthorized access to private data. System malfunctions, unintentional deletion, and natural disasters are a few examples of the many causes of data loss. Moreover, MSPs usually employ third-party vendors to offer services to their clients. This also increases the chances of data breaches. These factors are projected to hinder the market revenue growth during the forecast period.

Increasing Digitalization and Adoption of Advanced Technologies to Offer Excellent Opportunities

The rising need for digital transformation and adoption of technology is likely to drive considerable development in the managed services industry in the upcoming years. Cloud computing, cybersecurity, network administration, and data analytics are just a few of the services that managed service providers offer to organizations to help them become more productive, save money, and perform better. The rise of remote work and the need for secure and reliable IT infrastructure has further accelerated the demand for managed services. Businesses have a lot of options to save money with managed services. Businesses may make use of the economies of scale and specialized service providers' knowledge by outsourcing their IT operations to third-party service providers instead of investing in costly infrastructure or employing and training in-house workers. Network administration, cloud services, security, data backup and recovery, and help desk assistance are provided by managed services companies. Businesses may save operating expenses, optimize their IT infrastructure, and boost overall operational effectiveness by utilizing the knowledge and experience of managed services providers.

To know more about global managed services market opportunities, get in touch with our analysts here.

Global Managed Services Market, by Organization Size

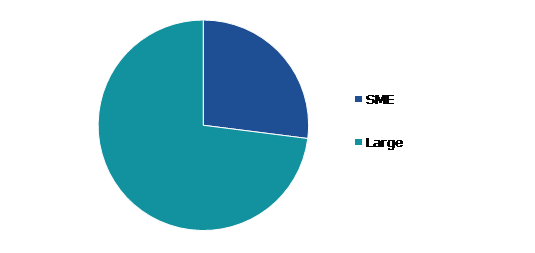

Based on organization size, the market has been divided into SME and large. Among these, the large sub-segment accounted for the highest market share in 2021 and the SME sub-segment is estimated to show the fastest growth during the forecast period.

Global Managed Services Market Size, by Organization Size, 2021

Source: Research Dive Analysis

The large sub-segment accounted for the highest market share in 2021. Large enterprises need intensive administration of their systems, networks, and applications due to their complex IT infrastructures. To assist major businesses, optimize their operations and cut costs, managed services providers offer end-to-end services that cover planning, designing, implementation, and administration of IT systems. Scalability and flexibility are essential for large businesses. Businesses must be able to scale their IT infrastructure efficiently and swiftly as they expand. Cloud solutions are one of the many services that managed service providers provide, allowing major businesses to grow their IT resources in accordance with their operational requirements. Large enterprises need ongoing monitoring and assistance to make sure their IT systems are performing at their best since they cannot afford downtime or interruption. The seamless operation of major enterprises depends on the 24/7 monitoring and assistance that managed services providers provide.

Global Managed Services Market, by Deployment Type

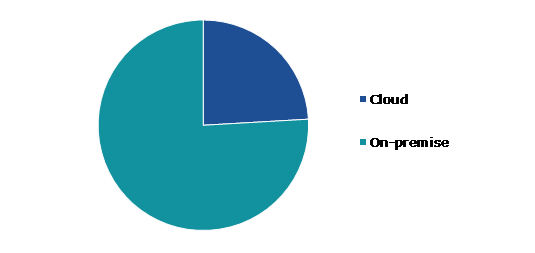

Based on deployment type, the market has been divided into cloud and on-premise. Among these, the on-premise sub-segment accounted for highest revenue share in 2021 and the cloud sub-segment is anticipated to show the fastest growth rate during the forecast period.

Global Managed Services Market Growth, by Deployment Type, 2021

Source: Research Dive Analysis

The cloud sub-segment is anticipated to show the fastest growth rate during the forecast period. Businesses now have the ability to access data and apps from any device or location without the need for on-premises infrastructure because of cloud-based managed services. This makes it possible for businesses to streamline their operations and cut down on the expense of managing and maintaining their IT infrastructure. Cloud managed service providers additionally offer a variety of services, such as cloud migration, cloud security, cloud monitoring, and cloud backup and disaster recovery, allowing organizations to concentrate on their core skills while the provider handles their cloud infrastructure. The demand for cloud-based managed services is rising rapidly, leading to an increase in the number of providers offering cloud-based solutions. This competitive market is driving innovation and service improvements, which is beneficial for businesses looking to leverage cloud-based managed services to achieve their strategic goals. These factors are anticipated to boost the growth of the cloud sub-segment during the forecast years.

Global Managed Services Market, by Service Type

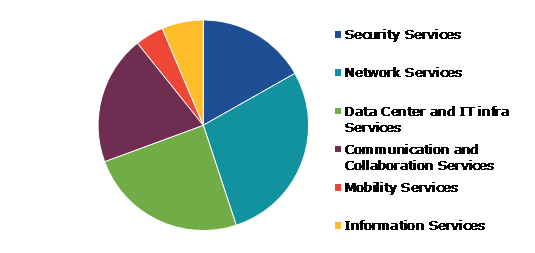

Based on service type, the market has been divided into security services, network services, data center & IT infra services, communication & collaboration services, mobility services, and information services. Among these, the network services sub-segment accounted for highest revenue share in 2021 and the security services sub-segment is anticipated to show highest CAGR during the forecast period.

Global Managed Services Market Analysis, by Service Type, 2021

Source: Research Dive Analysis

The security services sub-segment is anticipated to show the highest CAGR during the forecast period. Outsourced management and monitoring of security systems and devices are included in a managed security service. Managed Security Service Providers (MSSPs) are third-party organizations that provide services to businesses. Intrusion detection, vulnerability scanning, managed firewalls, anti-viral services, and other similar services are available. MSSP employs high-availability security operation centers to provide 24-hour-a-day services with the goal of lowering the number of operational security professionals that a corporation must acquire, train, and retain in order to maintain an acceptable security posture.

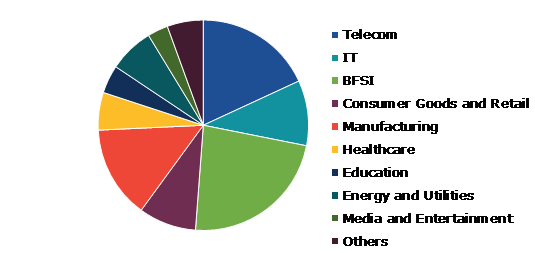

Global Managed Services Market, by Industry Vertical

Based on industry vertical, the market has been divided into telecom, IT, BFSI, consumer goods & retail, manufacturing, healthcare, education, energy & utilities, media & entertainment, and others. Among these, the BFSI sub-segment accounted for the highest revenue share in 2021.

Global Managed Services Market Share, by Industry Vertical, 2021

Source: Research Dive Analysis

The BFSI sub-segment accounted for the highest market share in 2021. Banks are finding it challenging to monitor and maintain their systems as IT infrastructure becomes more complicated. Managed service providers (MSPs) are used by businesses to provide a variety of services such as network monitoring, data backup, security management, and help desk support. MSPs help banks improve their capabilities and business operations. Furthermore, MSPs enable banks to reduce in-house IT costs, restructure IT systems, and automate business operations, enabling them to meet their objectives.

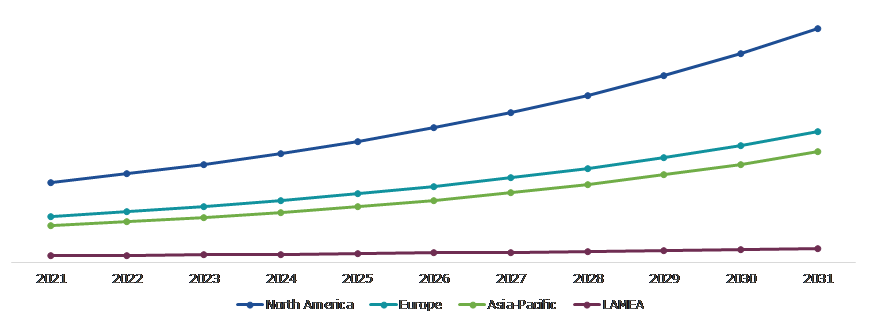

Global Managed Services Market, Regional Insights

The managed services market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Managed Services Market Size & Forecast, by Region, 2021-2031 (USD Billion)

Source: Research Dive Analysis

The Market for Managed Services in North America was the Most Dominant

The North America managed services market accounted for the highest market share in 2021. North America represents a sizable market for managed services due to the existence of both major enterprises and SMEs in the region. Growth drivers for the market include the requirement for affordable and effective IT operations, a growing concentration on key business functions, and rising cloud technology use. The need for managed services is rising as the trend of outsourcing IT services increases in North America. In addition, the region is home to several leading managed service providers (MSPs) that are continuously innovating and offering new services to meet the changing needs of their clients. These MSPs are also investing heavily in technologies such as automation, artificial intelligence (AI), and machine learning (ML) to improve their service offerings and differentiate themselves in the market.

Competitive Scenario in the Global Managed Services Market

Investment and agreement are common strategies followed by major market players. For instance, in June 2021, the Internal Business Machines Corporation officially unveiled the IBM Centre for Government Cybersecurity to address the cybersecurity requirements of government agencies.

Source: Research Dive Analysis

Some of the leading managed services market players are IBM, HCL, TCS, Atos, AT&T, Cisco, Fujitsu, Ericsson, Accenture, and Dimension Data.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Organization Size |

|

| Segmentation by Deployment type |

|

| Segmentation by Service Type |

|

| Segmentation by Industry Vertical |

|

| Key Companies Profiled |

|

Q1. What is the size of the global managed services market?

A. The size of the global managed services market was over $205.5 billion in 2021 and is projected to reach $594.8 billion by 2031.

Q2. Which are the major companies in the managed services market?

A. IBM, HCL, and TCS are some of the key players in the global managed services market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific managed services market?

A. Asia-Pacific managed services market is anticipated to grow at 11.9% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Atos, AT&T, and Cisco are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Managed Services market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Legal

4.6.6.Environmental

4.7.Impact of COVID-19 on Managed Services market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Managed Services Market Analysis, by Organization Size

5.1.Overview

5.2.SME

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2031

5.2.3.Market share analysis, by country,2021-2031

5.3.Large

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2031

5.3.3.Market share analysis, by country,2021-2031

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Managed Services Market Analysis, by Deployment Type

6.1.Cloud

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region,2021-2031

6.1.3.Market share analysis, by country,2021-2031

6.2.On-premise

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2031

6.2.3.Market share analysis, by country,2021-2031

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Managed Services Market Analysis, by Service Type

7.1.Overview

7.2.Security Services

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2031

7.2.3.Market share analysis, by country,2021-2031

7.3.Network Services

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2031

7.3.3.Market share analysis, by country,2021-2031

7.4.Data Center & IT Infra-Services

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region,2021-2031

7.4.3.Market share analysis, by country,2021-2031

7.5.Communication & Collaboration Services

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region,2021-2031

7.5.3.Market share analysis, by country,2021-2031

7.6.Mobility Services

7.6.1.Definition, key trends, growth factors, and opportunities

7.6.2.Market size analysis, by region,2021-2031

7.6.3.Market share analysis, by country,2021-2031

7.7.Information Services

7.7.1.Definition, key trends, growth factors, and opportunities

7.7.2.Market size analysis, by region,2021-2031

7.7.3.Market share analysis, by country,2021-2031

7.8.Research Dive Exclusive Insights

7.8.1.Market attractiveness

7.8.2.Competition heatmap

8.Managed Services Market Analysis, by Industry Vertical

8.1.Overview

8.2.Telecom

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region,2021-2031

8.2.3.Market share analysis, by country,2021-2031

8.3.IT

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region,2021-2031

8.3.3.Market share analysis, by country,2021-2031

8.4.BFSI

8.4.1.Definition, key trends, growth factors, and opportunities

8.4.2.Market size analysis, by region,2021-2031

8.4.3.Market share analysis, by country,2021-2031

8.5.Consumer Goods & Retail

8.5.1.Definition, key trends, growth factors, and opportunities

8.5.2.Market size analysis, by region,2021-2031

8.5.3.Market share analysis, by country,2021-2031

8.6.Manufacturing

8.6.1.Definition, key trends, growth factors, and opportunities

8.6.2.Market size analysis, by region,2021-2031

8.6.3.Market share analysis, by country,2021-2031

8.7.Healthcare

8.7.1.Definition, key trends, growth factors, and opportunities

8.7.2.Market size analysis, by region,2021-2031

8.7.3.Market share analysis, by country,2021-2031

8.8.Education

8.8.1.Definition, key trends, growth factors, and opportunities

8.8.2.Market size analysis, by region,2021-2031

8.8.3.Market share analysis, by country,2021-2031

8.9.Research Dive Exclusive Insights

8.10.Energy & Utilities

8.10.1.Definition, key trends, growth factors, and opportunities

8.10.2.Market size analysis, by region,2021-2031

8.10.3.Market share analysis, by country,2021-2031

8.11.Media & Entertainment

8.11.1.Definition, key trends, growth factors, and opportunities

8.11.2.Market size analysis, by region,2021-2031

8.11.3.Market share analysis, by country,2021-2031

8.12.Others

8.12.1.Definition, key trends, growth factors, and opportunities

8.12.2.Market size analysis, by region,2021-2031

8.12.3.Market share analysis, by country,2021-2031

8.13.Research Dive Exclusive Insights

8.13.1.Market attractiveness

8.13.2.Competition heatmap

9.Managed Services Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Organization Size

9.1.1.2.Market size analysis, by Deployment Type

9.1.1.3.Market size analysis, by Service Type

9.1.1.4.Market size analysis, by Industry Vertical

9.1.2.Canada

9.1.2.1.Market size analysis, by Organization Size

9.1.2.2.Market size analysis, by Deployment Type

9.1.2.3.Market size analysis, by Service Type

9.1.2.4.Market size analysis, by Industry Vertical

9.1.3.Mexico

9.1.3.1.Market size analysis, by Organization Size

9.1.3.2.Market size analysis, by Deployment Type

9.1.3.3.Market size analysis, by Service Type

9.1.3.4.Market size analysis, by Industry Vertical

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Organization Size

9.2.1.2.Market size analysis, by Deployment Type

9.2.1.3.Market size analysis, by Service Type

9.2.1.4.Market size analysis, by Industry Vertical

9.2.2.UK

9.2.2.1.Market size analysis, by Organization Size

9.2.2.2.Market size analysis, by Deployment Type

9.2.2.3.Market size analysis, by Service Type

9.2.2.4.Market size analysis, by Industry Vertical

9.2.3.France

9.2.3.1.Market size analysis, by Organization Size

9.2.3.2.Market size analysis, by Deployment Type

9.2.3.3.Market size analysis, by Service Type

9.2.3.4.Market size analysis, by Industry Vertical

9.2.4.Spain

9.2.4.1.Market size analysis, by Organization Size

9.2.4.2.Market size analysis, by Deployment Type

9.2.4.3.Market size analysis, by Service Type

9.2.4.4.Market size analysis, by Industry Vertical

9.2.5.Italy

9.2.5.1.Market size analysis, by Organization Size

9.2.5.2.Market size analysis, by Deployment Type

9.2.5.3.Market size analysis, by Service Type

9.2.5.4.Market size analysis, by Industry Vertical

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Organization Size

9.2.6.2.Market size analysis, by Deployment Type

9.2.6.3.Market size analysis, by Service Type

9.2.6.4.Market size analysis, by Industry Vertical

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia-Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Organization Size

9.3.1.2.Market size analysis, by Deployment Type

9.3.1.3.Market size analysis, by Service Type

9.3.1.4.Market size analysis, by Industry Vertical

9.3.2.Japan

9.3.2.1.Market size analysis, by Organization Size

9.3.2.2.Market size analysis, by Deployment Type

9.3.2.3.Market size analysis, by Service Type

9.3.2.4.Market size analysis, by Industry Vertical

9.3.3.India

9.3.3.1.Market size analysis, by Organization Size

9.3.3.2.Market size analysis, by Deployment Type

9.3.3.3.Market size analysis, by Service Type

9.3.3.4.Market size analysis, by Industry Vertical

9.3.4.Australia

9.3.4.1.Market size analysis, by Organization Size

9.3.4.2.Market size analysis, by Deployment Type

9.3.4.3.Market size analysis, by Service Type

9.3.4.4.Market size analysis, by Industry Vertical

9.3.5.South Korea

9.3.5.1.Market size analysis, by Organization Size

9.3.5.2.Market size analysis, by Deployment Type

9.3.5.3.Market size analysis, by Service Type

9.3.5.4.Market size analysis, by Industry Vertical

9.3.6.Rest of Asia-Pacific

9.3.6.1.Market size analysis, by Organization Size

9.3.6.2.Market size analysis, by Deployment Type

9.3.6.3.Market size analysis, by Service Type

9.3.6.4.Market size analysis, by Industry Vertical

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Organization Size

9.4.1.2.Market size analysis, by Deployment Type

9.4.1.3.Market size analysis, by Service Type

9.4.1.4.Market size analysis, by Industry Vertical

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Organization Size

9.4.2.2.Market size analysis, by Deployment Type

9.4.2.3.Market size analysis, by Service Type

9.4.2.4.Market size analysis, by Industry Vertical

9.4.3.UAE

9.4.3.1.Market size analysis, by Organization Size

9.4.3.2.Market size analysis, by Deployment Type

9.4.3.3.Market size analysis, by Service Type

9.4.3.4.Market size analysis, by Industry Vertical

9.4.4.South Africa

9.4.4.1.Market size analysis, by Organization Size

9.4.4.2.Market size analysis, by Deployment Type

9.4.4.3.Market size analysis, by Service Type

9.4.4.4.Market size analysis, by Industry Vertical

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Organization Size

9.4.5.2.Market size analysis, by Deployment Type

9.4.5.3.Market size analysis, by Service Type

9.4.5.4.Market size analysis, by Industry Vertical

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.IBM

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.2.HCL

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.3.TCS

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.4.Atos

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.5.AT&T

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.6.Cisco

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.7.Fujitsu

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.8.Ericsson

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.9.Accenture

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.10.Dimension Data

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

With the rapid growth of technology and the rising complexity of company operations, organizations are looking for efficient and cost-effective solutions for managing their IT infrastructure and services. Thus, to solve these issues, many organizations have turned to various solutions and strategies. This is where the managed services solution comes in.

Managed service is a business model in which a third-party service provider continuously controls and maintains a company's technology and infrastructure. The managed services market is the industry that provides organizations with outsourced IT support and management services. It can include a wide range of services, such as monitoring and maintaining networks, servers, and applications; providing consulting and strategic planning services, managing security and backups; and offering help desk and technical support.

Recent Trends in the Managed Services Market

The managed services market is continuously evolving with new technologies and trends. Cloud computing adoption has continued to increase, resulting in an upsurge in the demand for cloud managed services. Many businesses outsource the operation of their cloud infrastructure, including networking, storage, and applications, to specialized MSPs (managed service providers). In addition, automation and artificial intelligence (AI) technologies are being used by managed service providers to streamline their service delivery. These technologies aided in proactive monitoring, swift issue resolution, and intelligent data analysis, resulting in increased productivity and cost savings.

Newest Insights in the Managed Services Market

As per a report by Research Dive, the global managed services market is expected to grow at a CAGR of 11.3% and generate revenue of $594.8 billion by 2031. The primary factors driving the growth of the market are the increasing use of cloud computing services, rising digitalization and uptake of innovative technology, growth of remote work, and expanding demand for safe and dependable IT infrastructure. However, a lack of skilled workers and data security concerns related to managed services solutions are expected to hinder the market growth.

The managed services market in North America is expected to remain dominant in the coming years. The region's high revenue in 2021 was driven by the need for efficient and cheap IT operations, an increased emphasis on significant company procedures, and a rise in cloud technology usage. This has led to a rising demand for dependable managed services providers to support businesses' IT operations and infrastructure.

How are Market Players Responding to the Rising Demand for Managed Services?

Market players are responding to the rising demand for managed services by investing in research and development to create more innovative and efficient managed services solutions. They are also increasing their service portfolios in order to provide a wider variety of managed services to their consumers.

In addition, market players are increasingly focusing on strategic partnerships and collaborations with other players in the industry to leverage their strengths and expand their reach. Some of the foremost players in the managed services market are Dimension Data, HCL, TCS, IBM, Atos, Cisco, AT&T, Fujitsu, Accenture, Ericsson, and others. These players are focused on implementing strategies such as mergers and acquisitions, novel developments, collaborations, and partnerships to reach a leading position in the global market.

For instance:

- In May 2022, Finastra, a provider of financial software, announced the launch of FMS (Finastra Managed Services) on AWS (Amazon Web Services) to allow financial institutions and banks access to FMS in the AWS cloud. A prominent international U.S. bank on the West Coast was able to put out its lending solution with the help of FMS, which already has the advantage of being accessible in the AWS cloud.

- In November 2022, Tata Consultancy Services, a pioneer in IT services, announced the start of TCS Managed Services for Security with SAP, expanding its line of products that aid businesses in setting up and operating safe SAP systems on Microsoft Azure.

- In April 2023, Aeries Technology, a leading provider of professional services and consultancy to corporate management teams, private equity investors, and their portfolio firms, launched its cyber security managed services offering, delivering businesses with access to top-tier cyber security services and ISMS (Information Security Management Systems) built to meet and exceed the standards of an enterprise-level Chief Information Security Officer at a fraction of the cost of hiring in-house specialists.

COVID-19 Impact on the Global Managed Services Market

The COVID-19 pandemic had an adverse impact on the global managed services market. During the pandemic, the economic slump resulted in budget cuts, which impacted the demand for managed services. The pandemic had an influence on the market for on-premises managed services, as many organizations migrated to cloud-based services. Moreover, the pandemic's supply chain disruptions harmed managed service delivery, causing service delays and increased expenses. However, the pandemic raised the need for managed services in specific industries, including cloud computing and security. In addition, the move to remote work and increased use of cloud services resulted in an increase in demand for managed cloud computing and cybersecurity services. Many organizations wanted to outsource their operations so they could focus on their main businesses, which created demand for managed services. These factors had a significant impact on the managed services market growth amidst the pandemic.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com