Residential Heat Pump Market Report

RA03641

Residential Heat Pump Market by Type (Air Source, Water Source, and Geothermal), Power Source (Electric Powered and Gas Powered), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2030

Global Residential Heat Pump Market Analysis

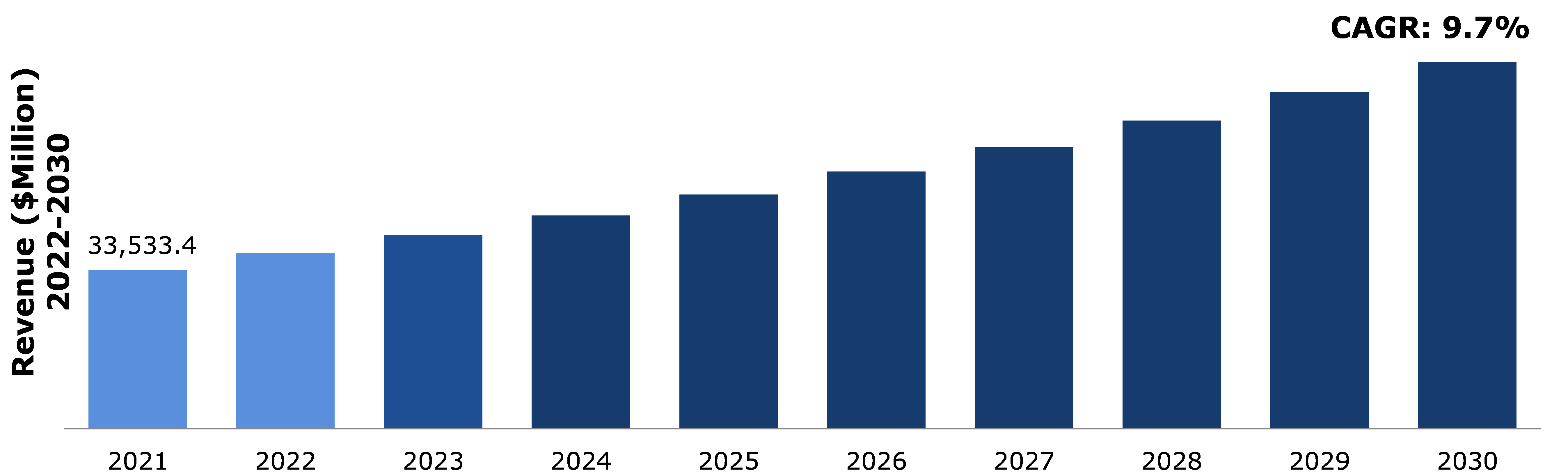

The global residential heat pump market size was $33,533.40 million in 2021 and is predicted to grow with a CAGR of 9.7%, by generating a revenue of $77,459.80 million by 2030.

Source: Research Dive Analysis

Market Synopsis

The desire for energy efficient and sustainable energy sources is driving the growth of the residential heat pump market. Residential heat pump systems are in high demand because of their high efficiency, adaptability, and clean operation. Heat pumps in residential buildings help to reduce carbon emissions. Heat pumps do not generate heat; instead, they transfer heat from one point to another. Currently, decarbonization of heat has become very important along with other renewable energy sources like wind energy and solar energy.

However, installation of residential heat pump is very expensive as the device as well as labor costs is very high. For instance, according to an article published on Angi, an online magazine portal, on February 16, 2022, an average cost of residential heat pump is approximately $5,400. Hence, not everyone can afford such high cost devices. This factor is likely to restrain residential heat pump market size growth in the next few years.

The residential heat pump market growth is expected to boost in the forecast time period due to the rising popularity of home geothermal heat pumps among people. Residential heat pump, also known as ground source heat pump, is majorly used for various purposes such as water heating and space heating. The primary benefit of a home geothermal heat pump is that it focuses on natural heat rather than generating heat through the combustion of fossil fuels. Such wide applications and uses of residential heat pump are anticipated to generate huge market revenues.

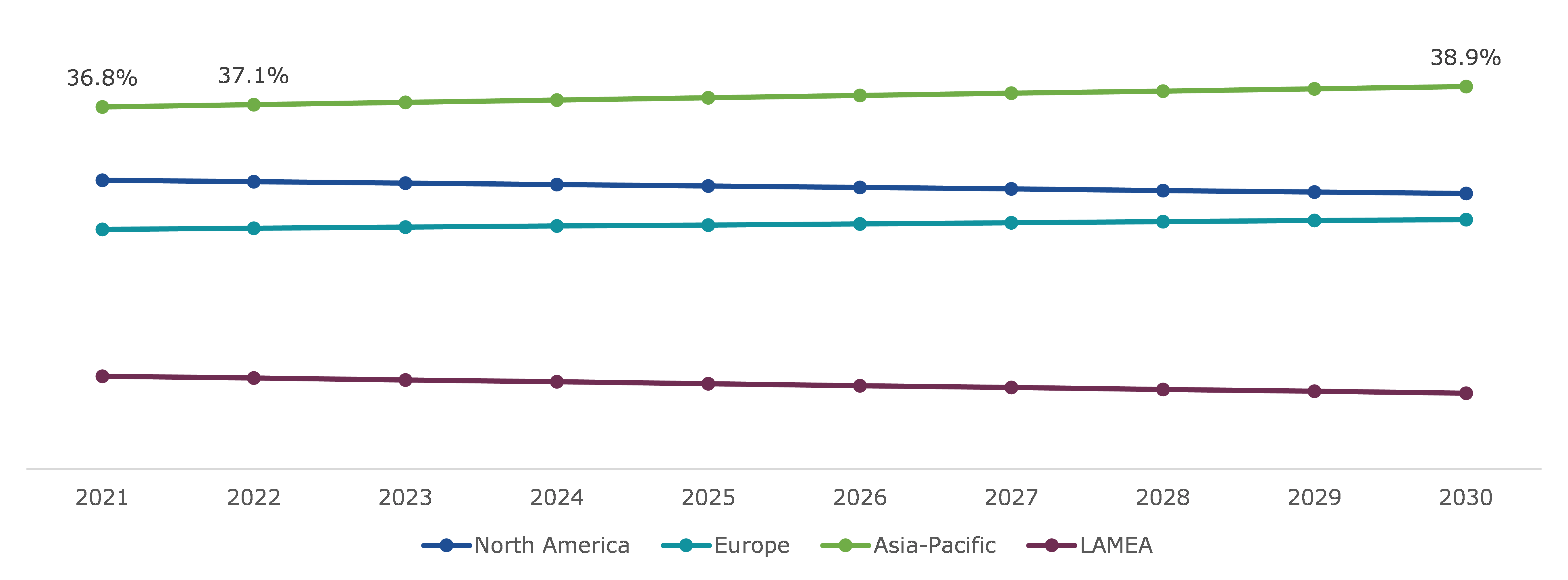

According to regional analysis, the Asia-Pacific residential heat pump market accounted for $12,347.00 million in 2021 and is predicted to grow with a CAGR of 10.3% in the projected timeframe.

Residential Heat Pump Overview

Heat pumps are energy-efficient alternative to classic air conditioners and furnaces that can be used in any climate. Heat pumps take heat from chilly outdoor air and transfer it within to keep indoor spaces warm in cold weather. They facilitate both heating and cooling mechanisms, thereby, eliminating the need for separate heating and cooling systems in homes. Heat pumps are environmentally benign since they do not need fossil fuels for heat generation or transfer. As a result, they vastly contribute towards reducing carbon emissions.

Covid-19 Impact on the Residential Heat Pump Market

The worldwide crisis and commercial uncertainty brought on by the COVID-19 pandemic have had a significant influence on the operations of numerous businesses, impacting revenues. Lockdown limitations implemented across numerous countries, as well as the shutdown of heat pump production operations, had a negative impact on the residential heat pump market growth. Travel restrictions, a closed border, and a ban on import-exports further hampered the supply of raw materials such as iron castings, stainless steel components, and aluminum tubing.

To cope up with declining business growth in COVID-19 pandemic, governments in many countries have taken some initiatives to get the economy back on track and to meet the net zero carbon emission objective in the coming years. For example, as per the news published in Electrical Times, an online news publishing platform, in 2020, the UK government issued a 10-point plan in 2020, to meet its net-zero carbon objective by 2050. The government has planned to install nearly 600,000 heat pumps by the end of 2028, along with investment in renewable energy and other low-carbon technology.

Government Regulations for the Implementation of Energy-efficient Systems to Reduce Carbon Emissions to Drive the Market Growth

Factors like growing demand for renewable energy sources, high demand for space heating, and objective about reducing carbon emissions are driving the expansion of the residential heat pump market, globally. To transport heat, a residential heat pump system uses a minimal amount of power. The carbon dioxide emitted by using electricity is comparatively lower than that emitted by burning fossil fuels. For example, according to the European Heat Pump Association (EHPA), information center for residential heat pump market, residential heat pump systems are highly energy efficient and sustainable because nearly 75% of the energy used by heat pumps comes from renewable sources such as solar, hydro, and wind, and remaining 25% comes from other sources such as electricity.

To know more about global residential heat pump market drivers, get in touch with our analysts here.

High Upfront Cost and Complexities in Installation to Affect the Market Growth

Heat pumps have high upfront costs, and they are difficult to install. This is because a prior study is required to understand the movement of heat, geology especially for residential geothermal heat pump to meet the heating and cooling requirements of residential sector. Moreover, a residential heat pump water heater can have an average cost ranging between $2500 to $5000 for full installation. Additional charges might be applicable for valve alterations or pipes.

New Technologies such as Digitalization and IoT for Residential Heat Pump to Generate Huge Opportunities

The residential heat pump market share is expected to grow due to the introduction of technologies such as digitalization and the internet of things (IoT), which include smart controllers that offer real-time energy efficiency, optimized load profiles, efficient use of electricity, and lower operating costs. The use of IoT in home heat pumps allows for even further decarbonization of heat transport. For example, IoT-enabled heat pumps in both the residential and commercial sectors will drive operational decisions such as predictive maintenance, benchmarking, fine-tuning of operation settings, and more. This can also be connected with building energy management (BEM), and a smart demand & response method can be used to reduce peak load & electricity usage.

To know more about global residential heat pump market opportunities, get in touch with our analysts here.

Global Residential Heat Pump Market, by Type

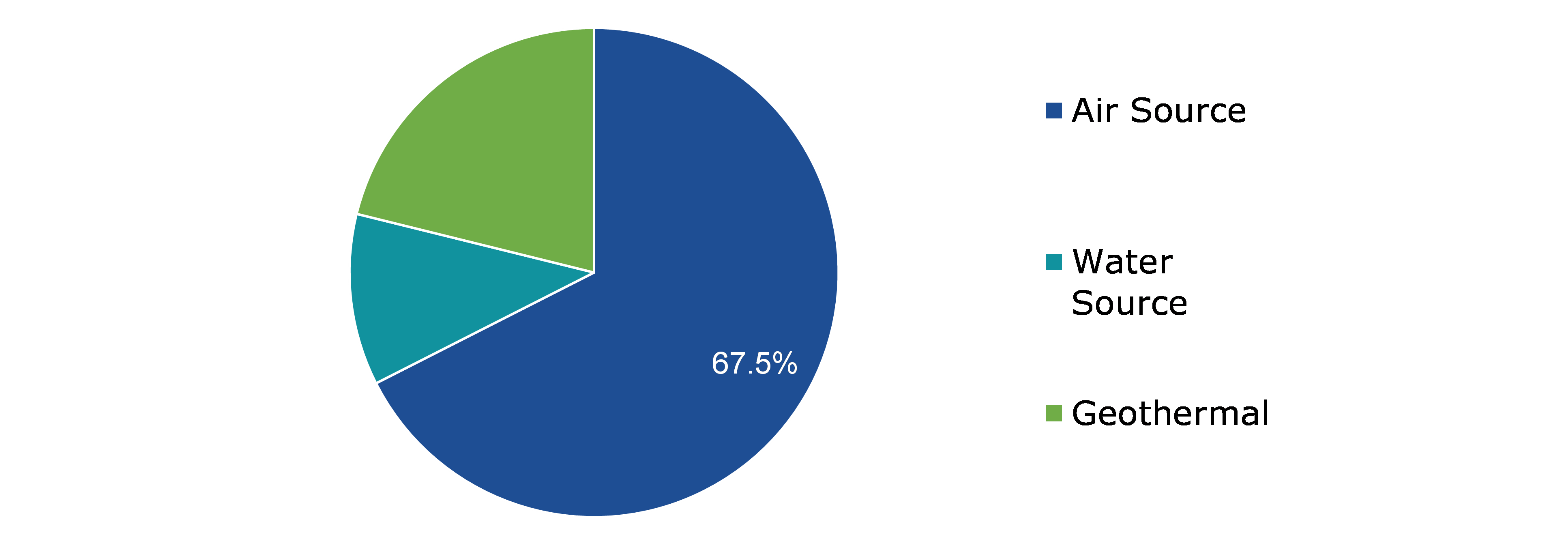

Based on type, the market has been classified into air source, water source, and geothermal. Among these, the air source sub-segment accounted for highest market share in 2021 and it is estimated to show the fastest growth during the forecast period.

Global Residential Heat Pump Market Share, by Type, 2021

Source: Research Dive Analysis

The air source sub-type is anticipated to have a dominant market share and generate a revenue of $54,022.10 million by 2030, growing from $22,641.50 million in 2021. Air source heat pump is a clean way to meet the energy demand for buildings that are free from carbon emissions. Air source heat pumps are suitable for residential sector and low environmental impact projects. These air source heat pumps require low maintenance as the only energy it uses is electricity for powering up the fans & compressors to transfer the heat energy from external environment into the building. Air source heat pumps help in cutting down your energy bills as they are cheaper to run compared to oil boilers or gas boilers. As no fuel is required for operation of air source heat pump, there is no need to manage fuel deliveries and no risk of fuel being stolen at residential places.

Global Residential Heat Pump Market, by Power Source

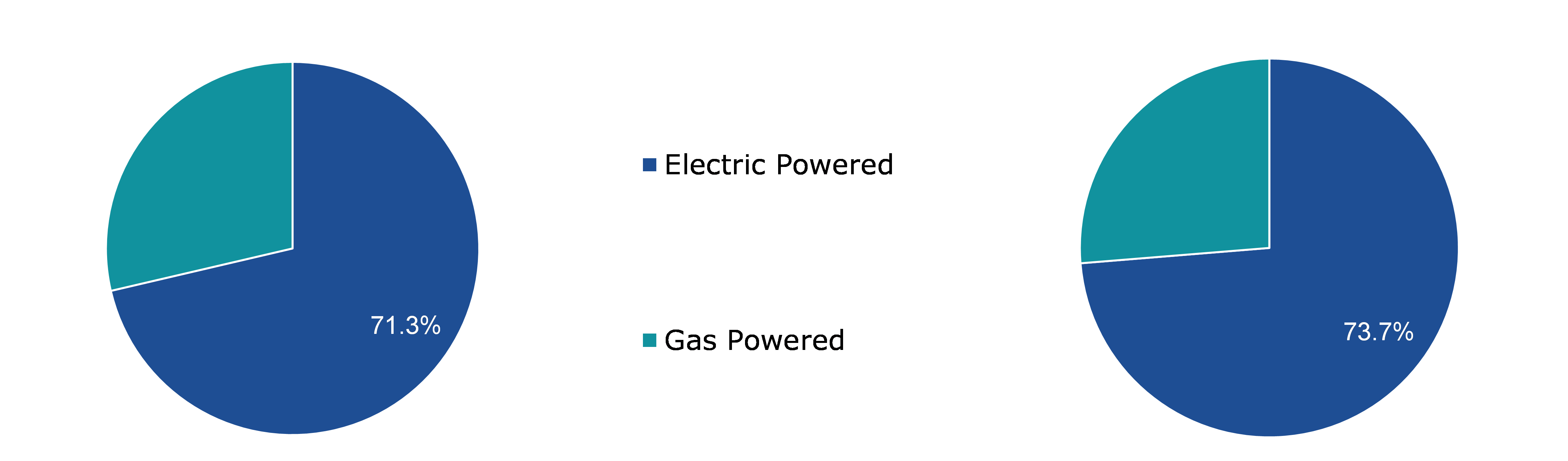

Based on power source, the market has been divided into electric powered and gas powered. Among these, the electric powered sub-segment accounted for the highest residential heat pump market share in 2021 and it is estimated to show the fastest growth during the forecast period.

Global Residential Heat Pump Market Share, by Power Source, 2021 and 2030

Source: Research Dive Analysis

The electric powered sub-segment is anticipated to have a dominant residential heat pump market size and generate a revenue of $57,093.90 million by 2030, growing from $ 23,925.60 million in 2021. The electric powered residential heat pump system is cheaper to run as they operate on electricity. Hence, there is no risk of toxic emissions or danger due to combustible gases. This helps in keeping the indoor clean, healthy, and free from toxic emissions. Also, the electric powered heat pump can transfer 300% more energy than it consumes, and it is highly efficient in various climatic conditions. Due to this, it can serve as both air conditioner and heater.

Global Residential Heat Pump Market, Regional Insights

The residential heat pump market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Residential Heat Pump Market Share, by Power Source, 2021

Source: Research Dive Analysis

The Market for Residential Heat Pump in Asia-Pacific to be the Most Dominant and Fastest Growing

The Asia-Pacific residential heat pump market size accounted for $12,347.00 million in 2021 and is projected to grow with a CAGR of 10.3%. China and Japan have widely deployed heat pumps including both air source heat pumps and residential geothermal heat pumps. This is majorly owing to the support from Chinese government by implementation of policies such as coal-to-electricity project. Hence, in order to cut down the carbon emissions, the Chinese government has shifted from coal incineration to heat pump systems. In China, the air source heat pumps are widely used in individual residential buildings as well as in the rural areas. For instance, as stated on November 24, 2020, by heatpumpingtechnologies.org, the international information service for heat pumps, the ground source heat pumps have been used in China for more than 20 years for heating buildings with central heating demand. In addition, as stated in June 2020, by the International Energy Agency IEA, the Paris-based intergovernmental organization, China has introduced subsidies under the Air Pollution Prevention and Control Action Plan to reduce the upfront installation and equipment costs of heat pumps. For instance, the air source heat pumps to be installed across Tianjin, Beijing, and Shanxi are eligible for subsidies ranging from CNY 24,000 to CNY 29,000 per household. Such initiatives are estimated to boost the residential heat pump market growth in the Asia-Pacific region during the forecast period.

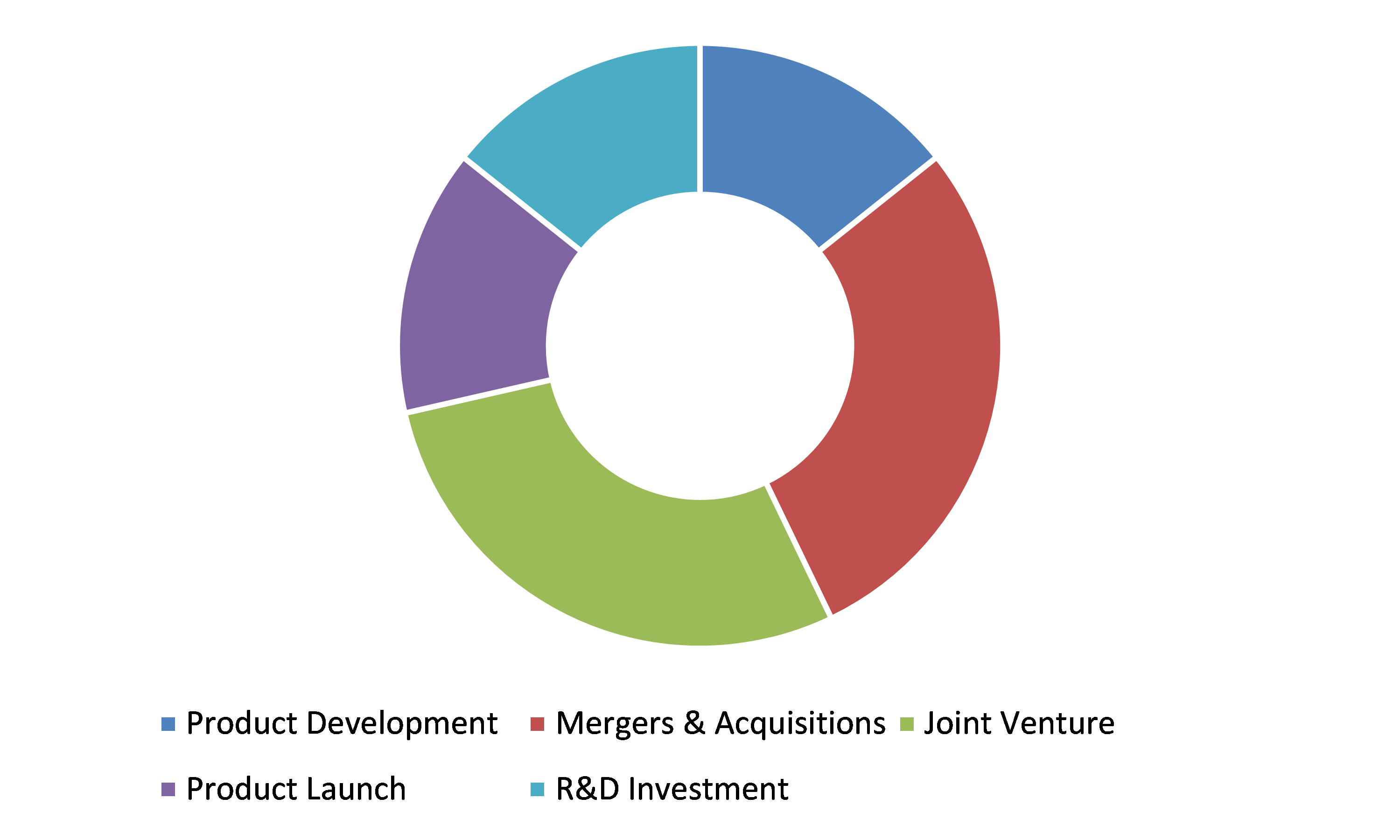

Competitive Scenario in the Global Residential Heat Pump Market

Investment and business expansion are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading residential heat pump market players are Midea Group, Johnson Controls, Daikin, Carrier Corporation, Glen Dimplex, NIBE, Stiebel Eltron, Viessmann, Mitsubishi Electric Corporation, and Danfoss.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2030 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Power Source |

|

| Key Companies Profiled |

|

Q1. What is the size of the global residential heat pump market?

A. The size of the global residential heat pump market was over $33,533.40 million in 2021 and is projected to reach $77,459.80 million by 2030.

Q2. Which are the major companies in the residential heat pump market?

A. Midea Group, Johnson Controls, and Daikin are some of the key players in the global residential heat pump market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific residential heat pump market?

A. Asia-Pacific residential heat pump market is anticipated to grow at 10.3% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Investment and business expansion are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Carrier Corporation, Glen Dimplex, and Stiebel Eltron are the companies investing more on R&D activities for developing new products and technologies.

Q7. What are the disadvantages of a heat pump?

A. The initial installation of heat pumps is costly and getting heat pump system installed in your home should be considered as an investment. In addition, heat pumps might be less efficient in extreme conditions. For instance, in extreme cold, when there is requirement of extra heat to warm up your home, the heat pump may end up working overtime as it will struggle to find necessary heat to warm up your home.

Q8. How much does a residential heat pump cost?

A. The residential heat pump such as geothermal heat pump can cost between $3,000 to $6,000. The gas-fired heat pump can cost between $3,000-$6,000 and ductless mini-split can cost between $1,000-$3,500. There will be additional installation cost involved.

Q9. What is the difference between a heat pump and central air?

A. The major difference between heat pump and central air is that central air does not provide heating, but heat pump does. In short, heat pumps are more efficient as they can function as a heater in winter and air conditioner in summer.

Q10. What is a heat pump HVAC system?

A. Heat pump is a type of heating, ventilation, and air conditioning (HVAC) as it can provide both heating and cooling. Heat pump HVAC system replaces the traditional boilers, electric baseboard, gas furnaces, and split system air conditioners.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.Type trends

2.3.Power Source trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Market value chain analysis

3.9.Strategic overview

4.Residential Heat Pump Market, by Type

4.1.Air source

4.1.1.Market size and forecast, by region, 2021-2030

4.1.2.Comparative market share analysis, 2020 & 2028

4.2.Water Source

4.2.1.Market size and forecast, by region, 2021-2030

4.2.2.Comparative market share analysis, 2020 & 2028

4.3.Geothermal

4.3.1.Market size and forecast, by region, 2021-2030

4.3.2.Comparative market share analysis, 2020 & 2028

5.Residential Heat Pump Market, by Power Source

5.1.Electric Powered

5.1.1.Market size and forecast, by region, 2021-2030

5.1.2.Comparative market share analysis, 2020 & 2028

5.2.Gas Powered

5.2.1.Market size and forecast, by region, 2021-2030

5.2.2.Comparative market share analysis, 2020 & 2028

6.Residential Heat Pump Market, by Region

6.1.North America

6.1.1.Market size and forecast, by Type, 2021-2030

6.1.2.Market size and forecast, by Power Source, 2021-2030

6.1.3.Market size and forecast, by country, 2021-2030

6.1.4.Comparative market share analysis, 2020 & 2028

6.1.5.U.S.

6.1.5.1.Market size and forecast, by Type, 2021-2030

6.1.5.2.Market size and forecast, by Power Source, 2021-2030

6.1.5.3.Comparative market share analysis, 2020 & 2028

6.1.6.Canada

6.1.6.1.Market size and forecast, by Type, 2021-2030

6.1.6.2.Market size and forecast, by Power Source, 2021-2030

6.1.6.3.Comparative market share analysis, 2020 & 2028

6.1.7.Mexico

6.1.7.1.Market size and forecast, by Type, 2021-2030

6.1.7.2.Market size and forecast, by Power Source, 2021-2030

6.1.7.3.Comparative market share analysis, 2020 & 2028

6.2.Europe

6.2.1.Market size and forecast, by Type, 2021-2030

6.2.2.Market size and forecast, by Power Source, 2021-2030

6.2.3.Market size and forecast, by country, 2021-2030

6.2.4.Comparative market share analysis, 2020 & 2028

6.2.5.Germany

6.2.5.1.Market size and forecast, by Type, 2021-2030

6.2.5.2.Market size and forecast, by Power Source, 2021-2030

6.2.5.3.Comparative market share analysis, 2020 & 2028

6.2.6.UK

6.2.6.1.Market size and forecast, by Type, 2021-2030

6.2.6.2.Market size and forecast, by Power Source, 2021-2030

6.2.6.3.Comparative market share analysis, 2020 & 2028

6.2.7.France

6.2.7.1.Market size and forecast, by Type, 2021-2030

6.2.7.2.Market size and forecast, by Power Source, 2021-2030

6.2.7.3.Comparative market share analysis, 2020 & 2028

6.2.8.Italy

6.2.8.1.Market size and forecast, by Type, 2021-2030

6.2.8.2.Market size and forecast, by Power Source, 2021-2030

6.2.8.3.Comparative market share analysis, 2020 & 2028

6.2.9.Spain

6.2.9.1.Market size and forecast, by Type, 2021-2030

6.2.9.2.Market size and forecast, by Power Source, 2021-2030

6.2.9.3.Comparative market share analysis, 2020 & 2028

6.2.10.Rest of Europe

6.2.10.1.Market size and forecast, by Type, 2021-2030

6.2.10.2.Market size and forecast, by Power Source, 2021-2030

6.2.10.3.Comparative market share analysis, 2020 & 2028

6.3.Asia Pacific

6.3.1.Market size and forecast, by Type, 2021-2030

6.3.2.Market size and forecast, by Power Source, 2021-2030

6.3.3.Market size and forecast, by country, 2021-2030

6.3.4.Comparative market share analysis, 2020 & 2028

6.3.5.China

6.3.5.1.Market size and forecast, by Type, 2021-2030

6.3.5.2.Market size and forecast, by Power Source, 2021-2030

6.3.5.3.Comparative market share analysis, 2020 & 2028

6.3.6.Japan

6.3.6.1.Market size and forecast, by Type, 2021-2030

6.3.6.2.Market size and forecast, by Power Source, 2021-2030

6.3.6.3.Comparative market share analysis, 2020 & 2028

6.3.7.India

6.3.7.1.Market size and forecast, by Type, 2021-2030

6.3.7.2.Market size and forecast, by Power Source, 2021-2030

6.3.7.3.Comparative market share analysis, 2020 & 2028

6.3.8.South Korea

6.3.8.1.Market size and forecast, by Type, 2021-2030

6.3.8.2.Market size and forecast, by Power Source, 2021-2030

6.3.8.3.Comparative market share analysis, 2020 & 2028

6.3.9.Australia

6.3.9.1.Market size and forecast, by Type, 2021-2030

6.3.9.2.Market size and forecast, by Power Source, 2021-2030

6.3.9.3.Comparative market share analysis, 2020 & 2028

6.3.10.Rest of Asia Pacific

6.3.10.1.Market size and forecast, by Type, 2021-2030

6.3.10.2.Market size and forecast, by Power Source, 2021-2030

6.3.10.3.Comparative market share analysis, 2020 & 2028

6.4.LAMEA

6.4.1.Market size and forecast, by Type, 2021-2030

6.4.2.Market size and forecast, by Power Source, 2021-2030

6.4.3.Market size and forecast, by country, 2021-2030

6.4.4.Comparative market share analysis, 2020 & 2028

6.4.5.Latin America

6.4.5.1.Market size and forecast, by Type, 2021-2030

6.4.5.2.Market size and forecast, by Power Source, 2021-2030

6.4.5.3.Comparative market share analysis, 2020 & 2028

6.4.6.Middle East

6.4.6.1.Market size and forecast, by Type, 2021-2030

6.4.6.2.Market size and forecast, by Power Source, 2021-2030

6.4.6.3.Comparative market share analysis, 2020 & 2028

6.4.7.Africa

6.4.7.1.Market size and forecast, by Type, 2021-2030

6.4.7.2.Market size and forecast, by Power Source, 2021-2030

6.4.7.3.Comparative market share analysis, 2020 & 2028

7.Company profiles

7.1.Midea Group

7.1.1.Business overview

7.1.2.Financial performance

7.1.3.Product portfolio

7.1.4.Recent strategic moves & developments

7.1.5.SWOT analysis

7.2.Johnson Controls

7.2.1.Business overview

7.2.2.Financial performance

7.2.3.Product portfolio

7.2.4.Recent strategic moves & developments

7.2.5.SWOT analysis

7.3.Daikin

7.3.1.Business overview

7.3.2.Financial performance

7.3.3.Product portfolio

7.3.4.Recent strategic moves & developments

7.3.5.SWOT analysis

7.4.Carrier Corporation

7.4.1.Business overview

7.4.2.Financial performance

7.4.3.Product portfolio

7.4.4.Recent strategic moves & developments

7.4.5.SWOT analysis

7.5.Glen Dimplex

7.5.1.Business overview

7.5.2.Financial performance

7.5.3.Product portfolio

7.5.4.Recent strategic moves & developments

7.5.5.SWOT analysis

7.6.NIBE

7.6.1.Business overview

7.6.2.Financial performance

7.6.3.Product portfolio

7.6.4.Recent strategic moves & developments

7.6.5.SWOT analysis

7.7.Stiebel Eltron

7.7.1.Business overview

7.7.2.Financial performance

7.7.3.Product portfolio

7.7.4.Recent strategic moves & developments

7.7.5.SWOT analysis

7.8.Viessmann

7.8.1.Business overview

7.8.2.Financial performance

7.8.3.Product portfolio

7.8.4.Recent strategic moves & developments

7.8.5.SWOT analysis

7.9.Mitsubishi Electric Corporation

7.9.1.Business overview

7.9.2.Financial performance

7.9.3.Product portfolio

7.9.4.Recent strategic moves & developments

7.9.5.SWOT analysis

7.10.Danfoss

7.10.1.Business overview

7.10.2.Financial performance

7.10.3.Product portfolio

7.10.4.Recent strategic moves & developments

7.10.5.SWOT analysis

A heat pump can regulate the flow of the refrigerant, helping to either heat or cool a home. Heat pump is a highly energy efficient alternative to conventional air conditioners and furnaces that are applicable in all climatic conditions. Heat pumps are completely sustainable and environmental-friendly unlike the furnaces that require the burning of fossil fuel and even air conditioners that release immense amount of CFCs (chlorofluorocarbons) which degrades the environment. Residential heat pumps favor both heating and cooling mechanisms, refraining the need for an instalment of separate or alternative systems.

Impact of COVID-19 on the Market

The outbreak of coronavirus has had a negative impact on the growth of the global residential heat pump market, owing to the prevalence of lockdowns in various countries across the globe. Redundant lockdowns led to the closure various manufacturing units of heat pump, adversely affecting the distribution and supply chain. Stringent import-export restriction imposed by the government during the pandemic made it difficult for companies to procure raw materials required for the production of heat pumps.

Residential Heat Pump Market Trends and Developments

The key companies operating in the residential heat pump market are adopting various growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, which is subsequently helping the global liver disease treatment market to grow exponentially.

For instance, in August 2019, Swegon AB, a Sweden-based company revolving around the products on indoor environment, offering solutions for ventilation, heating, cooling and climate optimization, acquired Klimax AS, a major distributor of products for heating and cooling of indoor climate in Norway, in order to maximize Swegon AB’s presence in the global heat pump market.

In July 2020, Daikin Applied, a global corporation that designs, manufactures and sells heating, ventilation and air conditioning (HVAC) products, systems, parts and services for commercial buildings, launched a new product called Daikin SmartSource® Dedicated Outdoor Air System (DOAS), for cost-effective heating and cooling in all environmental conditions using 100 percent of fresh, outside air.

In August 2020, Carrier, a world leader in high-technology heating, air conditioning and refrigeration solutions, collaborated with ServiceTitan, a dominant company providing all-in-one software and operating system for residential and commercial service and replacement contractors, in order to strategize and streamline workflows of Carrier and Bryant so as to improve their sales opportunities, ameliorate profits, and augment business growth.

Forecast Analysis of Global Residential Heat Pump Market

The global residential heat pump market is anticipated to witness a remarkable growth during the forecast period (2022-2030), owing to the prevalence of stringent restrictions imposed by the government of various countries for the adoption of energy-efficient systems. Heat pumps are extremely sustainable, substantially reducing the carbon emissions than other conventional heating or cooling systems. In addition, persistent technological development and implementation of IOT in residential heat pumps are further expected to create massive opportunities for the growth of the market. However, extortionate installation charges of residential heat pump are expected to impede the growth of the residential heat pump market during the forecast period.

According to the report published by Research Dive, the global residential heat pump market is expected to generate a revenue of $77,459.8 million by 2030, growing expeditiously at a CAGR of 9.7% during the forecast period. The major players of the market include Johnson Controls, Midea Group, Glen Dimplex, Daikin, Danfoss, Stiebel Eltron, Carrier Corporation, Danfoss, Viessmann, Mitsubishi Electric Corporation, NIBE, and many more.

Most Profitable Region

The Asia-Pacific region is expected to have the largest market share, and is expected to grow exponentially with a CAGR of 10.3% during the forecast period. Severe restrictions imposed by the government in this region in order to cut down the carbon emissions and rigorous initiatives on gradual shift from coal incineration to heat pump systems are the factors expected to drive the growth of the regional residential heat pump market. In addition, presence of prominent players of the market in this region is further expected to bolster the growth of the regional market.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com