Workforce Management Market Report

RA00330

Workforce Management Market by Component (Solution and Services), Deployment Mode (On-premise and Cloud), Organization Size (Large Enterprises and Small & Medium Enterprises), End User (BFSI, Manufacturing, Healthcare, Government, Retail & E-Commerce, IT & Telecom, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2020–2027

Global Workforce Management Market Analysis

The global workforce management market is projected to gain $9,580.3 million in the 2019–2027 timeframe, growing from $4,219.2 million in 2019 at a healthy CAGR of 10.6%.

Market SynopsisGrowing need for optimization of human resource management practices in organizations globally is expected to accelerate the growth of the workforce management market.

However, low awareness about upgradation to modern workforce management solutions can hamper the growth of the market.

According to the regional analysis of the market, the North America workforce management market is expected to grow at a CAGR of 10.6% by generating a revenue of $9,580.3 million during the forecast period.

Workforce Management Overview

Workforce management (WFM) refers to adoption of advance human resource practices to optimize the productivity of employees in an organization. It involves forecasting of labor demand, scheduling of the staff, time, attendance, and other processes. The introduction workforce management software for human resource management in organizations has aided the productivity of employees as well as the organization.

Impact Analysis of COVID-19 on the Global Workforce Management Market

The workforce management market has experienced a healthy growth during the COVID-19 pandemic. The pandemic has enforced businesses around the world to launch remote working of their operations and adopt an effective management system for their employees to improve the productivity and sustain the growth of their organization during the pandemic.

In addition to this, many companies operating in the workforce management domain have launched new solutions for effective human resource management solutions in businesses. For example, in December 2019, Salesforce.com, Inc., an American cloud-based software company, launched “Service Cloud Workforce Engagement", a new product in the domain of workforce planning that will enable businesses to organize their workforce from anywhere and allocate the right work to the right people based on skills and service channel. The launch of the new products and services has helped the corporations to mitigate the effect of the COVID-19 pandemic.

Increasing Demand for Upgraded Human Resource Management Practices to Surge the Market Growth

The global workforce management market is expected to witness a healthy growth mainly due increasing utilization of modern practices that are integrated with technology for human resource management. The workforce management software for enterprise has advantages such as it acts as a single solution for diverse HRM processes such as recruitment, documentation, performance management, and others. These advantages are laying the foundation for the market growth.

Moreover, the companies providing workforce management solutions are launching new products for gaining the maximum share of the global workforce management market. For example, in February 2019, Oracle, an Austin, Texas based American multinational computer technology corporation, launched Return-to-Workplace Package with the name of “Oracle Fusion Cloud HCM’s Employee Care Package" as organizations are planning to reopen their workplaces post the Covid-19 pandemic settles. This package guides employees through a series of key steps to promote workforce safety and ease the process of returning to in-office routines. This includes reviewing new safety procedures, completing regular wellness checks, taking mask and safety protocol training, booking a COVID-19 test with preferred testing providers, and others. The product developments for providing better workforce management services to corporations is anticipated to drive the growth of this market.

To know more about global workforce management market drivers, get in touch with our analysts here.

The Low Awareness of Workforce Management Tools to Restrain the Market Growth

The low awareness for adoption of workforce management software in the developing economies especially in the small and medium enterprises can hamper the growth of the global market during the forecast period.

Implementation of technologies such as IOT (Internet of Things) and Artificial Intelligence (AI) to Create Substantial Investment Opportunities

The workforce management market is anticipated to grow in the forecast period and witness new domains of expansion due to adoption of technologies such as artificial intelligence (AI) and Internet of Things (IOT). The implementation of internet of things helps in providing an in-depth understanding of working pattern of the employees and artificial intelligence in workforce management as it facilitates the process of tracking and analysis of relevant employee data.

In addition to this, the adoption of new innovative technologies for workforce management are driving the growth of the market. For example in July 2019, a major American software technology firm IBM, launched “Watson Works", a software solution that utilizes “Watson artificial intelligence (AI) models” and applications for helping companies to manage their workplace during the COVID-19 pandemic. This software is designed to help companies manage facilities and optimize space allocation by using real-time data, monitor employee health by enabling evidence-based decisions, and maximize the effectiveness of contact tracing, among others. Such key developments may further lead to beneficial market opportunities for market players in the market in the upcoming years.

To know more about global workforce management market opportunities, get in touch with our analysts here.

Global Workforce Management Market, by Component

Based on component, the market has been divided into solution and service sub-segment. The solution sub-segment is anticipated to generate the maximum revenue.

Source: Research Dive Analysis

The solution sub-segment is predicted to have a dominating market share in the global market and is estimated to register a revenue of $4,962.7 million during the forecast period.

The increasing deployment of different software across different industries such as healthcare, retail and e-commerce, manufacturing, and others for human resource management applications is growing the demand for the solution subsegment. The utilization of workforce management solutions in corporations have advantages such as reduction in employee operations cost, better productivity, and greater employee satisfaction. These factors are expected to aid growth of this segment during the forecast period.

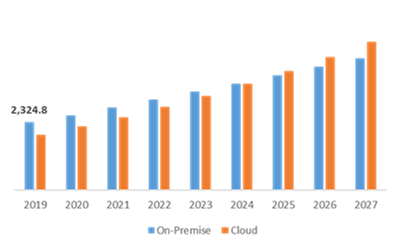

Global Workforce Management Market, by Deployment Mode

On the basis of deployment mode, the market has been sub-segmented into on-premise and cloud. Among the mentioned sub-segments, the cloud sub-segment is projected to have the fastest growth.

Source: Research Dive Analysis

The cloud sub-segment of the global workforce management market is anticipated to have the fastest growth and also the most dominating subsegment it is estimated to exceed $ 5,067.8 million by 2027, with an increase from $ 1,894.5 million in 2019. The growing adoption of SaaS (software as a service) workforce management solutions in the diverse sectors such as healthcare, retail and e-commerce, manufacturing and others. The cloud based deployment has advantages such as they are more cost effective as they are deployed on subscription model and doesn’t require large data storage infrastructure. These factors are expected to increase the demand for services and further surge the market growth.

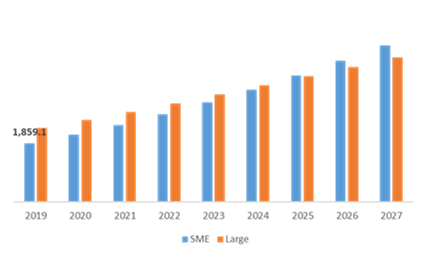

Global Workforce Management Market, by Organization Size:

Based on organization size this market the analysis has been divided into large enterprises and small & medium enterprises. Out of these, the small & medium enterprises are predicted to have the fastest growth.

Source: Research Dive Analysis

The small & medium enterprise sub-segment of the global workforce management market is predicted to have fastest growth and also the most dominating sub segment it is expected to surpass $ 4,987.2 million by 2027, with an increase from $ 1,859.1 million in 2019 and it is growing with a healthy CAGR of 12.9% in the forecast period. The growth is due to increasing need for decrease in cost for employee performance management process, improving employee engagement and productivity, generating data-based insights for individual and organization performance and the increasing scalability potential of the small and medium-sized enterprises (SMEs) in the future. These factors are expected to grow this sub segment in the forecast period.

Global Workforce Management Market, by End User:

Based on end user this market the analysis has been sub categorized in to BFSI, manufacturing, healthcare, government, retail & e-commerce, IT & telecom and others. Out of these, the IT & telecom sub-segment is anticipated to hold the maximum revenue share in the global market.

Source: Research Dive Analysis

The IT & telecom sub-segment is predicted to have a dominating market share in the global market and is projected to record a revenue of $ 1,784.7 million in 2027 growing from $756.8 million in 2019 during the forecast period. The growth is due to the wide spread utilization of technology related to software and communication surging the demand of services from information technology (IT) and telecommunications (Telecom) sector. To manage this demand, the IT and telecom have one of the largest number of employees and has increased the utilization of workforce management solutions from the SMEs to the large-scale organization in the telecom and IT industry. These factors are expected to grow this sub-segment.

Global Workforce Management Market, Regional Insights:

The workforce management market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The Market for Workforce Management in Europe to be the Most Dominant

The European workforce management market reported $1,267.1 million in 2019 and is projected to register a revenue of $2,958.6 million by 2027. The growth of the European workforce management market is mostly propelling due is promoting the growth workforce management market in this region. The growing need for improved productivity to maintain viable advantage and the increasing complexity of workforce-related standards the European organizations are witnessing a need for effective workforce management solutions. In addition to this, majority of European companies come under the category of small and medium-sized enterprises (SMEs) and these organizations are expected to be major users of workforce management software modules and contribute to the expansion of the market.

The Asia-Pacific to be the Fastest Growing Market for Workforce Management

The Asia-Pacific workforce management market is expected to grow at a fastest rate with a CAGR of 11.2% and generating a revenue of $2,430.7 million by 2027. The workforce management market in the Asia-Pacific region is estimated to grow due to presence of large number of organizations from small to large scale that require advanced human resource management solutions, growing scale of digitization in the businesses of emerging countries of the region such as China, India, Japan, South Korea, and others. These factors are expected to contribute to the growth of workforce management market in the Asia-Pacific region.

Competitive Scenario in the Global Workforce Management Market

Product development and agreement are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading workforce management market players are IBM, Oracle, SAP SE, ADP, Inc., Workday, Inc., Verint., NICE Ltd., Ceridian HCM, Inc., UKG Inc. and Infor.

Porter’s Five Forces Analysis for the Global Workforce Management Market:

- Bargaining Power of Suppliers: The suppliers in the workforce management market are high in number. Several companies are working on utilization of new technologies like cloud-based software. Thus, there is threat from the suppliers.

Thus, the bargaining power suppliers is moderate. - Bargaining Power of Buyers: Buyers have huge bargaining power; they demand best services at low prices. This increases the pressure on the workforce management test providers to offer the best service in a cost-effective way. Thus, buyers can freely choose the convenient service that best fits their preference.

Thus, the bargaining power of the buyers is high. - Threat of New Entrants: Companies entering the workforce management testing market are adopting technological innovations such as developing an innovative software application to attract clients. Also, these companies are implementing various effective strategies such as offering discounts and value propositions.

Thus, the threat of the new entrants is moderate. - Threat of Substitutes: There is no alternative product for workforce management solutions.

Thus, the threat of substitutes is low. - Competitive Rivalry in the Market: The competitive rivalry among industry leaders is rather intense, especially between the global players including IBM, ADP, Inc., Workday, Inc. These companies are launching their new innovative solutions in the international market and strengthening the footprint worldwide.

Therefore, competitive rivalry in the market is high.

| Aspect | Particulars |

| Historical Market Estimations | 2018-2019 |

| Base Year for Market Estimation | 2019 |

| Forecast Timeline for Market Projection | 2020-2027 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Component |

|

| Segmentation by Deployment Mode |

|

| Segmentation by Organization Size |

|

| Segmentation by End User |

|

| Key Companies Profiled |

|

Q1. What is the size of the global workforce management market?

A. The size of the global workforce management market was over $ 4,219.2 million in 2019 and is projected to reach $9,580.3 million by 2027.

Q2. Which are the major companies in the workforce management market?

A. IBM and Oracle are some of the key players in the global workforce management market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific workforce management market?

A. Asia Pacific workforce management market is anticipated to grow at 11.2% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Technological development and strategic partnerships are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. UKG Inc., and IBM are investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.Component trends

2.3.Component trends

2.4.Organization Size trends

2.5.End-User trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Pricing overview

3.8.1.By component

3.8.2.By deployment mode

3.8.3.By organization size

3.8.4.By end-user

3.8.5.By region

3.9.Market value chain analysis

3.9.1.Stress point analysis

3.9.2.Raw material analysis

3.9.3.Manufacturing process

3.9.4.Distribution channel analysis

3.9.5.Operating vendors

3.9.5.1.Raw material suppliers

3.9.5.2.Component manufacturers

3.9.5.3.Component distributors

3.10.Strategic overview

4.Software Defined Radio Market, by Component

4.1.Solution

4.1.1.Market size and forecast, by region, 2019-2027

4.1.2.Comparative market share analysis, 2019-2027

4.2.Service

4.2.1.Market size and forecast, by region, 2019-2027

4.2.2.Comparative market share analysis, 2019-2027

5.Software Defined Radio Market, by Component

5.1.On-Premise

5.1.1.Market size and forecast, by region, 2019-2027

5.1.2.Comparative market share analysis, 2019-2027

5.2.Cloud

5.2.1.Market size and forecast, by region, 2019-2027

5.2.2.Comparative market share analysis, 2019-2027

6.Software Defined Radio Market, by Organization Size

6.1.Large Enterprises

6.1.1.Market size and forecast, by region, 2019-2027

6.1.2.Comparative market share analysis, 2019-2027

6.2.Small & Medium Enterprises

6.2.1.Market size and forecast, by region, 2019-2027

6.2.2.Comparative market share analysis, 2019-2027

7.Software Defined Radio Market, by End-User

7.1.BFSI

7.1.1.Market size and forecast, by region, 2019-2027

7.1.2.Comparative market share analysis, 2019-2027

7.2.Manufacturing

7.2.1.Market size and forecast, by region, 2019-2027

7.2.2.Comparative market share analysis, 2019-2027

7.3. Healthcare

7.3.1.Market size and forecast, by region, 2019-2027

7.3.2.Comparative market share analysis, 2019-2027

7.4.Government

7.4.1.Market size and forecast, by region, 2019-2027

7.4.2.Comparative market share analysis, 2019-2027

7.5.Retail & E-Commerce

7.5.1.Market size and forecast, by region, 2019-2027

7.5.2.Comparative market share analysis, 2019-2027

7.6.IT & Telecom

7.6.1.Market size and forecast, by region, 2019-2027

7.6.2.Comparative market share analysis, 2019-2027

7.7.Others

7.7.1.Market size and forecast, by region, 2019-2027

7.7.2.Comparative market share analysis, 2019-2027

8.Software Defined Radio Market, by Region

8.1.North Region

8.1.1.Market size and forecast, by Component, 2019-2027

8.1.2.Market size and forecast, by Deployment Mode, 2019-2027

8.1.3.Market size and forecast, by Organization Size, 2019-2027

8.1.4.Market size and forecast, by End- User, 2019-2027

8.1.5.Market size and forecast, by country, 2019-2027

8.1.6.Comparative market share analysis, 2019-2027

8.1.7.U.S

8.1.7.1.Market size and forecast, by Component, 2019-2027

8.1.7.2.Market size and forecast, by Deployment Mode, 2019-2027

8.1.7.3.Market size and forecast, by Organization Size, 2019-2027

8.1.7.4.Market size and forecast, by End-User, 2019-2027

8.1.8.Canada

8.1.8.1.Market size and forecast, by Component, 2019-2027

8.1.8.2.Market size and forecast, by Deployment Mode, 2019-2027

8.1.8.3.Market size and forecast, by Organization Size, 2019-2027

8.1.8.4.Market size and forecast, by End-User, 2019-2027

8.2.Europe

8.2.1.Market size and forecast, by Component, 2019-2027

8.2.2.Market size and forecast, by Deployment Mode, 2019-2027

8.2.3.Market size and forecast, by Organization Size, 2019-2027

8.2.4.Market size and forecast, by End-User, 2019-2027

8.2.5.Market size and forecast, by country, 2019-2027

8.2.6.Comparative market share analysis, 2019-2027

8.2.7.UK

8.2.7.1.Market size and forecast, by Component, 2019-2027

8.2.7.2.Market size and forecast, by Deployment Mode, 2019-2027

8.2.7.3.Market size and forecast, by Organization Size, 2019-2027

8.2.7.4.Market size and forecast, by End-User, 2019-2027

8.2.7.5.Comparative market share analysis, 2019-2027

8.2.8.Germany

8.2.8.1.Market size and forecast, by Component, 2019-2027

8.2.8.2.Market size and forecast, by Deployment Mode, 2019-2027

8.2.8.3.Market size and forecast, by Organization Size, 2019-2027

8.2.8.4.Market size and forecast, by End-User, 2019-2027

8.2.8.5.Comparative market share analysis, 2019-2027

8.2.9.France

8.2.9.1.Market size and forecast, by Component, 2019-2027

8.2.9.2.Market size and forecast, by Deployment Mode,2019-2027

8.2.9.3.Market size and forecast, by Organization Size, 2019-2027

8.2.9.4.Market size and forecast, by End-User, 2019-2027

8.2.9.5.Comparative market share analysis, 2019-2027

8.2.10.Italy

8.2.10.1.Market size and forecast, by Component, 2019-2027

8.2.10.2.Market size and forecast, by Deployment Mode, 2019-2027

8.2.10.3.Market size and forecast, by Organization Size, 2019-2027

8.2.10.4.Market size and forecast, by End-User, 2019-2027

8.2.10.5.Comparative market share analysis, 2019-2027

8.2.11.Rest of Europe

8.2.11.1.Market size and forecast, by Component, 2019-2027

8.2.11.2.Market size and forecast, by Deployment Mode, 2019-2027

8.2.11.3.Market size and forecast, by Organization Size, 2019-2027

8.2.11.4.Market size and forecast, by End-User, 2019-2027

8.2.11.5.Comparative market share analysis, 2019-2027

8.3.Asia-Pacific

8.3.1.Market size and forecast, by Component, 2019-2027

8.3.2.Market size and forecast, by Deployment Mode, 2019-2027

8.3.3.Market size and forecast, by Organization Size, 2019-2027

8.3.4.Market size and forecast, by End-User, 2019-2027

8.3.5.Market size and forecast, by country, 2019-2027

8.3.6.Comparative market share analysis, 2019-2027

8.3.7.China

8.3.8.Market size and forecast, by Component, 2019-2027

8.3.9.Market size and forecast, by Deployment Mode, 2019-2027

8.3.10.Market size and forecast, by Organization Size, 2019-2027

8.3.11.Market size and forecast, by End-User, 2019-2027

8.3.12.Comparative market share analysis, 2019-2027

8.3.13.India

8.3.13.1.Market size and forecast, by Component, 2019-2027

8.3.13.2.Market size and forecast, by Deployment Mode, 2019-2027

8.3.13.3.Market size and forecast, by Organization Size, 2019-2027

8.3.13.4.Market size and forecast, by End-User, 2019-2027

8.3.13.5.Comparative market share analysis, 2019-2027

8.3.14.Japan

8.3.14.1.Market size and forecast, by Component, 2019-2027

8.3.14.2.Market size and forecast, by Deployment Mode, 2019-2027

8.3.14.3.Market size and forecast, by Organization Size, 2019-2027

8.3.14.4.Market size and forecast, by End-User, 2019-2027

8.3.14.5.Comparative market share analysis, 2019-2027

8.3.15.South Korea

8.3.15.1.Market size and forecast, by Component, 2019-2027

8.3.15.2.Market size and forecast, by Deployment Mode, 2019-2027

8.3.15.3.Market size and forecast, by Organization Size, 2019-2027

8.3.15.4.Market size and forecast, by End-User, 2019-2027

8.3.15.5.Comparative market share analysis, 2019-2027

8.3.16.Australia

8.3.16.1.Market size and forecast, by Component, 2019-2027

8.3.16.2.Market size and forecast, by Deployment Mode, 2019-2027

8.3.16.3.Market size and forecast, by Organization Size, 2019-2027

8.3.16.4.Market size and forecast, by End-User, 2019-2027

8.3.16.5.Comparative market share analysis, 2019-2027

8.3.17.Rest of Asia Pacific

8.3.17.1.Market size and forecast, by Component, 2019-2027

8.3.17.2.Market size and forecast, by Deployment Mode, 2019-2027

8.3.17.3.Market size and forecast, by Organization Size, 2019-2027

8.3.17.4.Market size and forecast, by End-User, 2019-2027

8.3.17.5.Comparative market share analysis, 2019-2027

8.4.LAMEA

8.4.1.Market size and forecast, by Component, 2019-2027

8.4.2.Market size and forecast, by Deployment Mode, 2019-2027

8.4.3.Market size and forecast, by Organization Size, 2019-2027

8.4.4.Market size and forecast, by, End-User, 2019-2027

8.4.5.Market size and forecast, by country, 2019-2027

8.4.6.Comparative market share analysis, 2019-2027

8.4.7.Latin America

8.4.7.1.Market size and forecast, by Component, 2019-2027

8.4.7.2.Market size and forecast, by Deployment Mode, 2019-2027

8.4.7.3.Market size and forecast, by Organization Size, 2019-2027

8.4.8.Market size and forecast, by End-User, 2019-2027

8.4.8.2.Comparative market share analysis, 2019-2027

8.4.9.Middle East

8.4.9.1.Market size and forecast, by Component, 2019-2027

8.4.9.2.Market size and forecast, by Deployment Mode, 2019-2027

8.4.9.3.Market size and forecast, by Organization Size, 2019-2027

8.4.9.4.Market size and forecast, by End-User, 2019-2027

8.4.9.5.Comparative market share analysis, 2019-2027

8.4.10.Africa

8.4.10.1.Market size and forecast, by Component, 2019-2027

8.4.10.2.Market size and forecast, by Deployment Mode, 2019-2027

8.4.10.3.Market size and forecast, by Organization Size, 2019-2027

8.4.10.4.Market size and forecast, by End-User, 2019-2027

8.4.10.5.Comparative market share analysis, 2019-2027

9.Company profiles

9.1.IBM

9.1.1.Business overview

9.1.2.Financial performance

9.1.3.Component portfolio

9.1.4.Recent strategic moves & developments

9.1.5.SWOT analysis

9.2.Oracle

9.2.1.Business overview

9.2.2.Financial performance

9.2.3.Component portfolio

9.2.4.Recent strategic moves & developments

9.2.5.SWOT analysis

9.3.SAP SE

9.3.1.Business overview

9.3.2.Financial performance

9.3.3.Component portfolio

9.3.4.Recent strategic moves & developments

9.3.5.SWOT analysis

9.4.ADP, Inc.

9.4.1.Business overview

9.4.2.Financial performance

9.4.3.Component portfolio

9.4.4.Recent strategic moves & developments

9.4.5.SWOT analysis

9.5.Workday, Inc.

9.5.1.Business overview

9.5.2.Financial performance

9.5.3.Component portfolio

9.5.4.Recent strategic moves & developments

9.5.5.SWOT analysis

9.6. Verint.

9.6.1.Business overview

9.6.2.Financial performance

9.6.3.Component portfolio

9.6.4.Recent strategic moves & developments

9.6.5.SWOT analysis

9.7.NICE Ltd.

9.7.1.Business overview

9.7.2.Financial performance

9.7.3.Component portfolio

9.7.4.Recent strategic moves & developments

9.7.5.SWOT analysis

9.8.Ceridian HCM, Inc.

9.8.1.Business overview

9.8.2.Financial performance

9.8.3.Component portfolio

9.8.4.Recent strategic moves & developments

9.8.5.SWOT analysis

9.9.UKG Inc.

9.9.1.Business overview

9.9.2.Financial performance

9.9.3.Component portfolio

9.9.4.Recent strategic moves & developments

9.9.5.SWOT analysis

9.10.Infor.

9.10.1.Business overview

9.10.2.Financial performance

9.10.3.Component portfolio

9.10.4.Recent strategic moves & developments

9.10.5.SWOT analysis

Workforce management (WFM) is a strategy for the employee efficiency. WFM started as a way to improve the accuracy, reliability, and efficiency of call centers, but it has since spread to other sectors and work tasks. Performance and training management, human resource management, recruitment, scheduling, data collection, analytics, budgeting, and planning are all WFM processes and resources that organizations are using to improve operational performance in a strategic manner.

Impact of COVID-19 on the Industry

The coronavirus pandemic has created a chaos in several end-use industries and negatively impacted various markets. However, the global workforce management market has witnessed a remarkable rise in the market growth rate during the COVID-19 pandemic. The pandemic has compelled companies all over the world to begin remote operations and implement an efficient management framework for their workers in order to increase efficiency and maintain the development of their company during the pandemic. Furthermore, several talent management firms have launched new technologies for successful human resource management solutions in enterprises. The introduction of new goods and services has aided companies in mitigating the effects of the COVID-19 pandemic.

Key Developments in the Industry

The key companies operating in the global workforce management market are adopting business tactics & several growth strategies such as partnerships, mergers & acquisitions, launches, and collaborations, to maintain a strong position in the overall market, which is subsequently assisting the market to grow across the world.

For instance, in April 2021, Infor, the business cloud provider, reported that Infor Workforce Management has been named the leader in Nucleus Research’s most recent Technology Value Matrix for WFM. Nucleus Research ranked vendors as ‘Leaders’ because of their power in niche areas, and capabilities, especially around employee experience and schedule optimization.

In May 2021, Penn Highlands Healthcare (PHH), a six-hospital integrated health system located in northwestern Pennsylvania, announced that they have selected Infor Cloverleaf Cloud and Infor CloudSuite Healthcare to advance their future vision. The transition to a more modern cloud architecture approach, which will be implemented in collaboration with key Infor integrated solution Bails, will provide PHH with a clinically linked healthcare operations framework to develop its patient-centric network.

In May 2021, Workday, a pioneer in enterprise cloud applications for finance and human resources, announced that it has been ranked by Gartner, Inc. in the leaders quadrant of the 2021 Gartner Magic Quadrant for cloud core financial management suites for global , large, and midsize enterprises for the fifth year in a row, based on vision completeness and capacity to execute.

Forecast Analysis of Workforce Management Market

The global workforce management market is expected to witness a healthy growth owing to increased adaptation of innovative practices for human resource management that are incorporated with software. The benefits of enterprise workforce management applications include acting as a centralized solution for various HRM processes, such as performance management, documentation, recruiting, and others. These advantages are laying the foundation for the market growth. Furthermore, companies offering workforce management solutions are introducing new products in order to capture the largest share of the global workforce management market. The development of products to provide better workforce management services to companies is expected to drive the growth of this market.

The low awareness regarding the adoption of workforce management software in the developing nations especially in the small and medium organizations is anticipated to hamper the growth of the global workforce management market during the forecast period. The adoption of new innovative technologies for workforce management are estimated to drive the growth of this market.

These aforementioned factors are estimated to surge the growth of the workforce management market, throughout the analysis period. As per a newly published report by Research Dive, the global workforce management market is predicted to garner $9,580.3 million by 2027. Geographically, the Asia Pacific market for workforce management is estimated to dominate the global industry, owing to the existence of a large number of enterprises ranging in size from small to large that need advanced human resource management solutions, as well as the increasing scale of digitization in the companies of the region’s emerging countries such as South Korea, Japan, India, China, and others.

Key Players

- IBM

- Oracle

- SAP SE

- ADP, Inc.

- Workday, Inc.

- Verint.

- NICE Ltd.

- Infor.

- Ceridian HCM, Inc.

- UKG Inc.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com