Revenue Assurance Market Report

RA00265

Revenue Assurance Market by Component (Solutions and Services), Deployment Type (Cloud and On-Premise), Application (BFSI, Telecom & IT, Government, Hospitality, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022–2031

Global Revenue Assurance Market Analysis

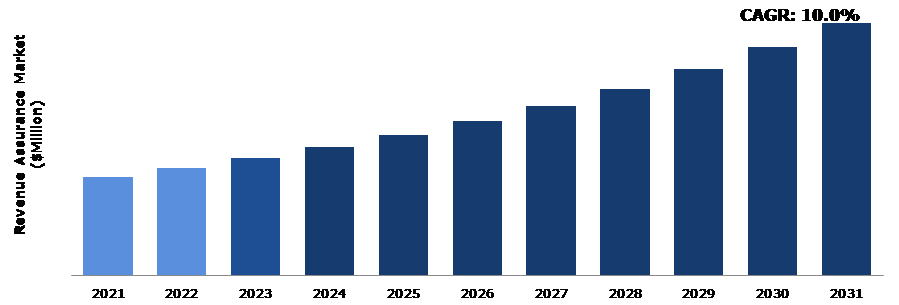

The Global Revenue Assurance Market Size was $507 million in 2021 and is predicted to grow with a CAGR of 10.0% by generating a revenue of $1,300 million by 2031.

Global Revenue Assurance Market Synopsis

Revenue assurance is the process by which an operator assures that revenues for services delivered to consumers and other parties are appropriately billed, accounted for, and collected. It is an umbrella term for the operations that a corporation engages in to guarantee that its procedures and processes minimize revenue leakage. Leakages occur when revenue received by the company and services delivered to the customer are lost on their route to billing systems and the client is never billed. Therefore, one of the primary reasons likely to drive the market during the forecast period is the increasing prevalence of revenue leakages. Changes in internal customer objectives, a mismatch between solution expectations and deliverables due to implementation challenges or poor communication, and unknown or unanticipated invoicing and billing errors are just a few of the factors that contribute to revenue leakage. Revenue assurance solutions help telecom providers get revenue for services they deliver but are unable to charge for due to inadequate back-office practices including regulatory compliance, maintaining records, and accounting.

The revenue assurance business is an extremely tightly controlled sector and organizations participating in this sector need to follow rigid rules and regulations. The continually changing regulatory landscape is a fundamental constraint for the revenue assurance sector. Companies need to verify that their revenue assurance practices conform with new laws and regulations when they are implemented. Failure to comply with these rules can result in high penalties and legal consequences, which can have a major effect on an organization's earnings and credibility. These factors are projected to hamper the market growth during the forecast period.

The global revenue assurance market is anticipated to expand significantly during the forecast period owing to the rising demand for real-time information, a structured process for data delivery from developers, and the efficient management of hierarchical master data produced across various verticals. In addition, the market development is anticipated to be driven by the increasing need to ensure regulatory compliance and the rising adoption of IoT devices during the forecast period.

According to regional analysis, North America revenue assurance market is anticipated to experience the fastest growth by 2031. The market in North America is driven by the increasing demand for revenue assurance solutions from various industries such as telecommunications, banking, and healthcare.

Revenue Assurance Overview

Revenue assurance is a method used by enterprises to discover, analyze, reduce, and prevent revenue loss through a variety of measures. Its goal is to limit the likelihood of losses due to mistakes, negligence, or fraud. It also assists firms in identifying chances to enhance revenues and maximize profits. Revenue assurance involves more than just managing revenue-generating activities like invoicing and collections. It is also involved with identifying potential chances for cost optimization and streamlining operations. This might include automating billing operations or enhancing inter-departmental communication by implementing new technology such as digital billing or enhanced consumer service systems.

COVID-19 Impact on Global Revenue Assurance Market

The COVID-19 pandemic had a major impact on the revenue assurance market resulting in an increase in a shift toward digital technologies. The pandemic accelerated the development of digital technologies and remote employment in numerous businesses, including the revenue assurance market. Organizations have been forced to adapt to new ways of working due to the pandemic, which has raised the demand for cloud-based revenue assurance systems that can be monitored and administered remotely. Cloud-based revenue assurance solutions provide various advantages to businesses, including lower expenses, better flexibility, and improved scalability. They also permit remote access, which was critical in the pandemic situation where many employees worked from home. Therefore, there has been a rapid increase in demand for revenue assurance solutions during the COVID-19 pandemic.

Increasing Demand for Revenue Assurance Solutions in the Telecommunications Industry to Drive the Market Growth

The digital revolution has generated a major wave of disruption, and most sectors are now forced to create new revenue-protection measures. The telecom industry has been encountering challenges owing to several developments that have a direct influence on income streams. Although revenue assurance can benefit a variety of businesses, it is especially beneficial to the telecom industry. The emergence of connected devices is rapidly changing the technology landscape of the telecommunications sector and redefining the role of telecommunications operators. Therefore, revenue assurance has become even more important in the telecom industry.. Consumer behavior is being influenced by innovation and cutting-edge technology, which will continue to drive demand for new services. The billing scenario gets more complex as a result of new agreements with partners who can provide revenue assurance services , as well as new business models and related income streams. These new services generate complex pricing systems, such as revenue sharing, sponsored and zero-rated services, elastic pricing, prorated services, and others. There are numerous technologies, systems, items, and procedures in the typical telecom revenue chain.

To know more about global revenue assurance market drivers, get in touch with our analysts here.

High Cost of Implementing Revenue Assurance Solutions is Expected to Hamper the Revenue Assurance Industry

The high cost of installing revenue assurance solutions is a significant barrier for the revenue assurance business. The cost of deploying revenue assurance solutions can be significant, especially for small and medium-sized enterprises (SMEs) that may not have the resources to invest in these solutions. This can limit the adoption of revenue assurance solutions and restrain the industry growth. This is one of the major factors anticipated to hinder the revenue assurance market growth in the upcoming years.

Emergence of New Technologies Such as Artificial Intelligence and Machine Learning to Drive Excellent Opportunities in The Market

Revenue assurance solutions for the telecom industry ensure that billing and contracts appropriately reflect the contractual agreement between the customer and the service provider. Improving data procedures and data quality that power revenue assurance solutions can increase margins, earnings, and cash flow demand and decrease revenue risk. As the telecom industry continues to undergo digital transformation, Artificial Intelligence (AI) and Machine Learning (ML) technologies are used to improve functionality of revenue assurance and fraud management systems. In the telecom business, artificial intelligence applications use powerful algorithms to search for patterns in data, assisting in the detection and prediction of network anomalies, manually sifting through all of it error-free would be nearly impossible. To fully use the potential of the massive volumes of data created, specialized tools and algorithms must be used. AI and ML in telecom have emerged as preferred techniques for dealing with such vast amounts of complicated data in order to deliver superior insights.

To know more about global revenue assurance market opportunities, get in touch with our analysts here.

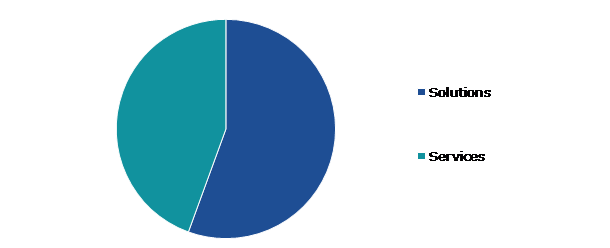

Global Revenue Assurance Market, by Component

Based on component, the market has been divided into solution and services. Among these, the solution sub-segment accounted for the highest market share in 2021, whereas the services sub-segment is estimated to show the fastest growth during the forecast period.

Global Revenue Assurance Market Size, by Component, 2021

Source: Research Dive Analysis

The solutions segment accounted for a dominant market share in 2021. The solutions segment includes various revenue assurance solutions such as risk management, fraud detection, and revenue recovery. These solutions are utilized by businesses across a variety of industries, including banking, telecommunications, healthcare, and retail. The solutions segment's dominance is due to the rising demand for revenue assurance solutions across industries as businesses attempt to strengthen their revenue management systems and maintain regulatory compliance. Also, the growth of the solutions segment can be attributed to the emergence of new technologies, such as artificial intelligence and machine learning, which are being integrated into revenue assurance solutions to improve their effectiveness and efficiency.

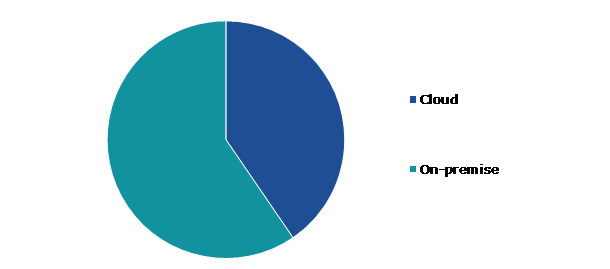

Global Revenue Assurance Market, by Deployment Type

Based on deployment type, the market has been divided into cloud and on-premise. Among these, the on-premise sub-segment accounted for the highest revenue share in 2021.

Global Revenue Assurance Market Share, by Deployment Type, 2021

Source: Research Dive Analysis

The on-premise segment accounted for a dominant market in 2021. Currently, on-premises software is in demand as many organizations are switching from manual to automated systems to carry out different tasks. Many businesses are choosing on-premises deployment due to the improved security features. In addition, some corporate revenue assurance systems can be easily customized to the requirements of the company and operate without an Internet connection. These factors are anticipated to drive the on-premises segment expansion steadily during the forecast period.

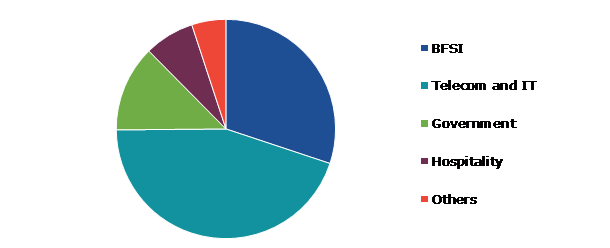

Global Revenue Assurance Market, by Application

Based on application, the market has been divided into BFSI, telecom & IT, government, hospitality, and others. Among these, the telecom & IT sub-segment accounted for the highest revenue share in 2021.

Global Revenue Assurance Market Trends, by Application, 2021

Source: Research Dive Analysis

The telecom & IT segment accounted for a dominant market share in 2021. Telecommunications operators, Internet service providers (ISPs), and other IT service providers are key customers of revenue assurance systems. Telecom operators, in particular, are a large market for revenue assurance solutions, as they face significant revenue leakage risks due to the complexity of their networks and services. Revenue assurance solutions assist these operators in monitoring and analyzing revenue sources, detecting and preventing revenue leakage, and ensuring compliance with regulatory requirements. The IT sector is also a key user of revenue assurance solutions, as organizations in this sector frequently have sophisticated IT systems and networks that require continuous monitoring and management. Revenue assurance solutions can assist these businesses in detecting and preventing revenue loss while also improving revenue efficiency.

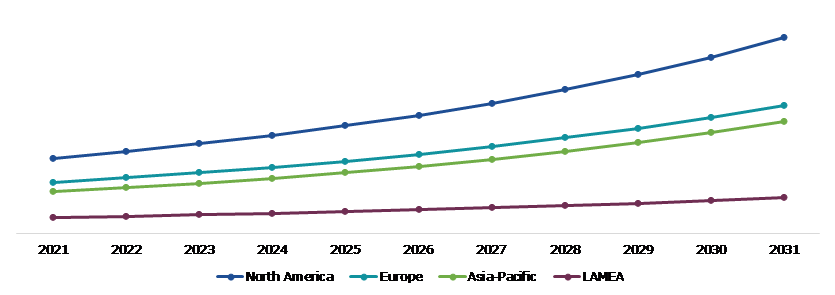

Global Revenue Assurance Market, Regional Insights

The revenue assurance market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Revenue Assurance Market Size & Forecast, by Region, 2021-2031 (USD Million)

Source: Research Dive Analysis

The Market for Revenue Assurance in North America was the Most Dominant

The North America market accounted for a dominant market share in 2021. North America has significant numbers of established revenue assurance solution providers, both large international corporations and small startups. One of the primary factors driving the growth of the revenue assurance market in North America is the rising need for actual time revenue monitoring and administration in the telecommunications industry, which is being driven by the increasing number of new technologies and services. This has resulted in an increase in demand for advanced revenue assurance solutions that can monitor and analyze income streams across numerous systems and networks while also maintaining regulatory compliance. All these factors are anticipated to boost the revenue assurance market in North America.

Competitive Scenario in the Global Revenue Assurance Market

Investment and agreement are common strategies followed by major market players. For instance, in August 2022, Subex, a pioneer in driving AI-led Digital Trust, announced that Ethio Telecom had selected it to deploy its Fraud Management solution. The solution, which was built on Subex’s AI orchestration platform, HyperSense, replaced Ethio Telecom’s existing legacy fraud management system, thereby enabling them to move from a traditional rules-based approach to an AI-first approach.

Source: Research Dive Analysis

Some of the leading revenue assurance market players are Amdocs, Araxxe, Cartesian, Itron Inc, Hewlett Packard Enterprise Development LP, Subex Ltd, Wedo Technologies, Sandvine, Sigos, and Tata Consultancy Services Limited (India).

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Component |

|

| Segmentation by Deployment Type |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global revenue assurance market?

A. The size of the global revenue assurance market was over $507 million in 2021 and is projected to reach $1,300 million by 2031.

Q2. Which are the major companies in the revenue assurance market?

A. Amdocs, Araxxe, and Cartesian are some of the key players in the global revenue assurance market.

Q3. Which region, among others, possesses greater investment opportunities in the future?

A. Asia-Pacific possesses great investment opportunities for investors in the future.

Q4. What will be the growth rate of the Asia-Pacific revenue assurance market?

A. Asia-Pacific revenue assurance market is anticipated to grow at 10.5% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Agreement and investment are the two key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Hewlett Packard Enterprise Development LP, Subex Ltd, and Wedo technologies are the companies investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Revenue Assurance market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Revenue Assurance market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Revenue Assurance Market Analysis, by Component

5.1.Overview

5.2.Solutions

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2021-2031

5.2.3.Market share analysis, by country, 2021-2031

5.3.Services

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2021-2031

5.3.3.Market share analysis, by country, 2021-2031

5.4.Research Dive Exclusive Insights

5.4.1.Market Attractiveness

5.4.2.Competition heatmap

6.Revenue Assurance Market Analysis, by Deployment Type

6.1. Cloud

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2021-2031

6.1.3.Market share analysis, by country, 2021-2031

6.2.On-premise

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2021-2031

6.2.3.Market share analysis, by country, 2021-2031

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Revenue Assurance Market Analysis, by Application

7.1.BFSI

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region, 2021-2031

7.1.3.Market share analysis, by country, 2021-2031

7.2.Telecom & IT

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2021-2031

7.2.3.Market share analysis, by country, 2021-2031

7.3.Government

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region, 2021-2031

7.3.3.Market share analysis, by country, 2021-2031

7.4.Hospitality

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region, 2021-2031

7.4.3.Market share analysis, by country, 2021-2031

7.5.Others

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region, 2021-2031

7.5.3.Market share analysis, by country, 2021-2031

7.6.Research Dive Exclusive Insights

7.6.1.Market attractiveness

7.6.2.Competition heatmap

8.Revenue Assurance Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Component, 2021-2031

8.1.1.2.Market size analysis, by Deployment Type, 2021-2031

8.1.1.3.Market size analysis, by Application, 2021-2031

8.1.2.Canada

8.1.2.1.Market size analysis, by Component, 2021-2031

8.1.2.2.Market size analysis, by Deployment Type, 2021-2031

8.1.2.3.Market size analysis, by Application, 2021-2031

8.1.3.Mexico

8.1.3.1.Market size analysis, by Component, 2021-2031

8.1.3.2.Market size analysis, by Deployment Type, 2021-2031

8.1.3.3.Market size analysis, by Application, 2021-2031

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Component, 2021-2031

8.2.1.2.Market size analysis, by Deployment Type, 2021-2031

8.2.1.3.Market size analysis, by Application, 2021-2031

8.2.2.UK

8.2.2.1.Market size analysis, by Component, 2021-2031

8.2.2.2.Market size analysis, by Deployment Type, 2021-2031

8.2.2.3.Market size analysis, by Application, 2021-2031

8.2.3.France

8.2.3.1.Market size analysis, by Component, 2021-2031

8.2.3.2.Market size analysis, by Deployment Type, 2021-2031

8.2.3.3.Market size analysis, by Application, 2021-2031

8.2.4.Spain

8.2.4.1.Market size analysis, by Component, 2021-2031

8.2.4.2.Market size analysis, by Deployment Type, 2021-2031

8.2.4.3.Market size analysis, by Application, 2021-2031

8.2.5.Italy

8.2.5.1.Market size analysis, by Component, 2021-2031

8.2.5.2.Market size analysis, by Deployment Type, 2021-2031

8.2.5.3.Market size analysis, by Application, 2021-2031

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Component, 2021-2031

8.2.6.2.Market size analysis, by Deployment Type, 2021-2031

8.2.6.3.Market size analysis, by Application, 2021-2031

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia-Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Component, 2021-2031

8.3.1.2.Market size analysis, by Deployment Type, 2021-2031

8.3.1.3.Market size analysis, by Application, 2021-2031

8.3.2.Japan

8.3.2.1.Market size analysis, by Component, 2021-2031

8.3.2.2.Market size analysis, by Deployment Type, 2021-2031

8.3.2.3.Market size analysis, by Application, 2021-2031

8.3.3.India

8.3.3.1.Market size analysis, by Component, 2021-2031

8.3.3.2.Market size analysis, by Deployment Type, 2021-2031

8.3.3.3.Market size analysis, by Application, 2021-2031

8.3.4.Australia

8.3.4.1.Market size analysis, by Component, 2021-2031

8.3.4.2.Market size analysis, by Deployment Type, 2021-2031

8.3.4.3.Market size analysis, by Application, 2021-2031

8.3.5.South Korea

8.3.5.1.Market size analysis, by Component, 2021-2031

8.3.5.2.Market size analysis, by Deployment Type, 2021-2031

8.3.5.3.Market size analysis, by Application, 2021-2031

8.3.6.Rest of Asia-Pacific

8.3.6.1.Market size analysis, by Component, 2021-2031

8.3.6.2.Market size analysis, by Deployment Type, 2021-2031

8.3.6.3.Market size analysis, by Application, 2021-2031

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Component, 2021-2031

8.4.1.2.Market size analysis, by Deployment Type, 2021-2031

8.4.1.3.Market size analysis, by Application, 2021-2031

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Component, 2021-2031

8.4.2.2.Market size analysis, by Deployment Type, 2021-2031

8.4.2.3.Market size analysis, by Application, 2021-2031

8.4.3.UAE

8.4.3.1.Market size analysis, by Component, 2021-2031

8.4.3.2.Market size analysis, by Deployment Type, 2021-2031

8.4.3.3.Market size analysis, by Application, 2021-2031

8.4.4.South Africa

8.4.4.1.Market size analysis, by Component, 2021-2031

8.4.4.2.Market size analysis, by Deployment Type, 2021-2031

8.4.4.3.Market size analysis, by Application, 2021-2031

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Component, 2021-2031

8.4.5.2.Market size analysis, by Deployment Type, 2021-2031

8.4.5.3.Market size analysis, by Application, 2021-2031

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Amdocs

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Araxxe

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.Cartesian

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Itron Inc

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Hewlett Packard Enterprise Development LP

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Subex Ltd

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.Wedo technologies

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.Wandvine

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.Sigos

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.Tata Consultancy Services Limited (India)

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com