Vascular Disease Devices Market Report

RA08574

Vascular Disease Devices Market by Product (Stents, Balloons, Catheters, Hemodynamic Flow Alteration Devices, Plaque Modification Devices, and Inferior Vena Cava Filters), End-user (Hospitals & Cardiac Centers and Ambulatory Surgical Center), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2021–2028

Global Vascular Disease Devices Market Analysis

The global vascular disease devices market is predicted to garner $22,610.3 million in the 2021–2028 timeframe, growing from $13,308.2 million in 2020, at a healthy CAGR of 6.9%.

Market Synopsis

Strategic alliances among market players, along with growth in number of cath labs are expected to accelerate the growth of the vascular disease devices market.

However, high set-up cost associated with vascular disease devices is a growth-restricting factor for the market.

According to the regional analysis, the North America vascular disease devices market is anticipated to grow during the review period with revenue of $8,727.6 million in 2028.

Vascular Disease Devices Overview

Vascular disease is the type of disease that affects the blood circulation of the body due to factors such as high blood pressure, cholesterol, and other infections. This disease affects the circulatory system of the body through veins, arteries, and lymph. Vascular disease devices are inserted into the veins or arteries via surgery to treat the vascular malfunction.

Impact Analysis of COVID-19 on the Global Vascular Disease Devices Market

The novel coronavirus pandemic had a devastating effect on several industries including the vascular disease devices market which experienced a negative growth during this period. Due to complete lockdown worldwide, manufacturing capacity of the vascular disease devices got affected; along with this, most of the surgeries got postponed because of strict government regulations regarding performing only critical surgeries of emergency department (ED). All such factors are expected to cause the revenue loss in global vascular disease devices industry. In addition to this, in 2020, according to the Society of Thoracic Surgeons Adult Cardiac Surgery Database, adult cardiac surgery volume reduced by 52.7% in the US. Thus, above-stated factors show that the pandemic affected the global vascular disease devices market.

Increasing Incidence of Atherosclerosis to Surge the Market Growth

The global vascular disease devices industry is witnessing a massive growth mainly due to increasing population suffering from atherosclerosis, a type of disease that is caused due to blockage in arteries due to buildup of cholesterol, fats, and other substances on artery walls. Moreover, according to the International Journal of Epidemiology, in 2019, approximately 75% of the myocardial infarctions occur because of plaque rupture in people aged 45 years or above.

Furthermore, according to a journal published by omicsonline.org, in the US, every 1 out of 58 people has atherosclerosis and 4.6 million people have this disease. Same situation arises in Australia. This type of researche and statistics showcase the demand for vascular disease devices for the treatment of such diseases. These types of initiatives drive the global vascular disease devices market.

To know more about global vascular disease devices market drivers, get in touch with our analysts here.

High Cost of Vascular Disease Devices to Restrain the Market Growth

The high set up cost of vascular disease devices is one of the factors expected to restrain the growth of the global market during the forecast period. In addition to this, lack of awareness regarding the availability of vascular disease devices mostly in developing countries is one of the aspects that may create a negative impact on the growth of the market during the forecast period.

Growing Prevalence of Peripheral Artery Disorders in the Market to Create Massive Investment Opportunities

The global vascular disease devices market is growing at a very fast pace due to increasing population with peripheral artery disorders (PAD). PAD is the condition in which arteries are unable to flow the blood towards the limbs. Moreover, changes in unhealthy dietary habits, smoking, obesity, and changes in lifestyle are some of the factors that increase the chances of developing PAD. For example, according to the American Heart Association, in America, more than 8.5 million people are affected with peripheral artery disease (PAD) yearly. All such aspects are thereby positively affecting the market growth.

Furthermore, certain key vendors operating in vascular disease devices market are adopting certain strategies and innovations for staying upfront in the competitive environment. For instance, in June 2020, Becton, Dickinson and Company, US based medical device company, announced that they have acquired Straub Medical AG, a private company that develops medical thrombectomy and atherectomy devices for the treatment of peripheral arterial disease (PAD) and venous disease. All such types of acquisitions and factors may further lead to lucrative market opportunities for key players in the upcoming years.

To know more about global vascular disease devices market opportunities, get in touch with our analysts here.

Based on product, the market has been divided into Stents, balloons, catheters, hemodynamic flow alteration devices, plaque modification devices, and inferior vena cava filters sub-segments of which the Stents sub-segment is projected to generate the maximum revenue as well as show the fastest growth. Download PDF Sample ReportVascular Disease Devices Market

By Product

Source: Research Dive Analysis

The stents sub-segment is predicted to have a dominating as well as fastest growing market share in the global market and register a revenue of $6,715.3 million during the forecast period. Stents are tiny little tubes placed inside the artery or veins to cure blocks caused by fats or other factors. Stents help arteries to hold the open structure and allow normal blood flow. Moreover, stents’ high accuracy level and reliability are some of the major factors driving the sub-segment growth. These factors may bolster the growth of the sub-segment during the forecast period.

Vascular Disease Devices Market

By End-UserOn the basis of end-user, the market has been sub-segmented into hospitals & cardiac centers and ambulatory surgical center. Among the mentioned sub-segments, the hospitals & cardiac centers sub-segment is predicted to show the fastest growth as well as garner a dominant market share.

Source: Research Dive Analysis

The hospitals & cardiac centers sub-segment of the global vascular disease devices market is projected to have the fastest growth as well as a dominant share and surpass $14,244.5 million by 2028, with an increase from $8,304.3 million in 2020. This growth in the market can be attributed to the rising number of people preferring hospitals & cardiac centers for their surgeries and treatments. The rapid growth of the sub-segment is attributed to better accessibility and expertise of treating diseases in hospitals. Moreover, hospitals & cardiac centers offer advanced devices along with skilled doctors & workforce which is predicted to influence patients to get treated in hospitals & cardiac centers. All such elements may increase the demand for hospitals & cardiac centers and further surge the market growth.

Vascular Disease Devices Market

By RegionThe vascular disease devices market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The Market for Vascular Disease Devices in North America to be the Most Dominant

The North America vascular disease devices market accounted $5,150.3 million in 2020 and is projected to register a revenue of $8,727.6 million by 2028. The extensive growth of the North America vascular disease devices market is mainly driven by high disposable incomes with existence of top leading brands such as Medtronic, Abbott Laboratories, and others augmenting the industry growth in the region. Moreover, in North America, most of the people are suffering from cardiovascular devices and peripheral artery disorder which is fueling the market growth across the region. Furthermore, in 2019, according to the International Journal of Epidemiology, in the US, approximately 610,000 people suffered from heart diseases and 735,000 people experienced heart attacks. These factors will ultimately drive the demand for the vascular disease devices market across the region.

The Market for Vascular Disease Devices in Asia-Pacific to be the Fastest Growing

The share of Asia-Pacific vascular disease devices market is anticipated to grow at a CAGR of 7.7%, by registering a revenue of $5,200.4 million by 2028. The growth shall be a result of increasing trends of unhealthy dietary habits along with obesity, smoking, and lack of physical activities. Also, growing population with peripheral artery disease will increase the demand for vascular disease devices, eventually surging the North America vascular disease devices market growth, in the upcoming years.

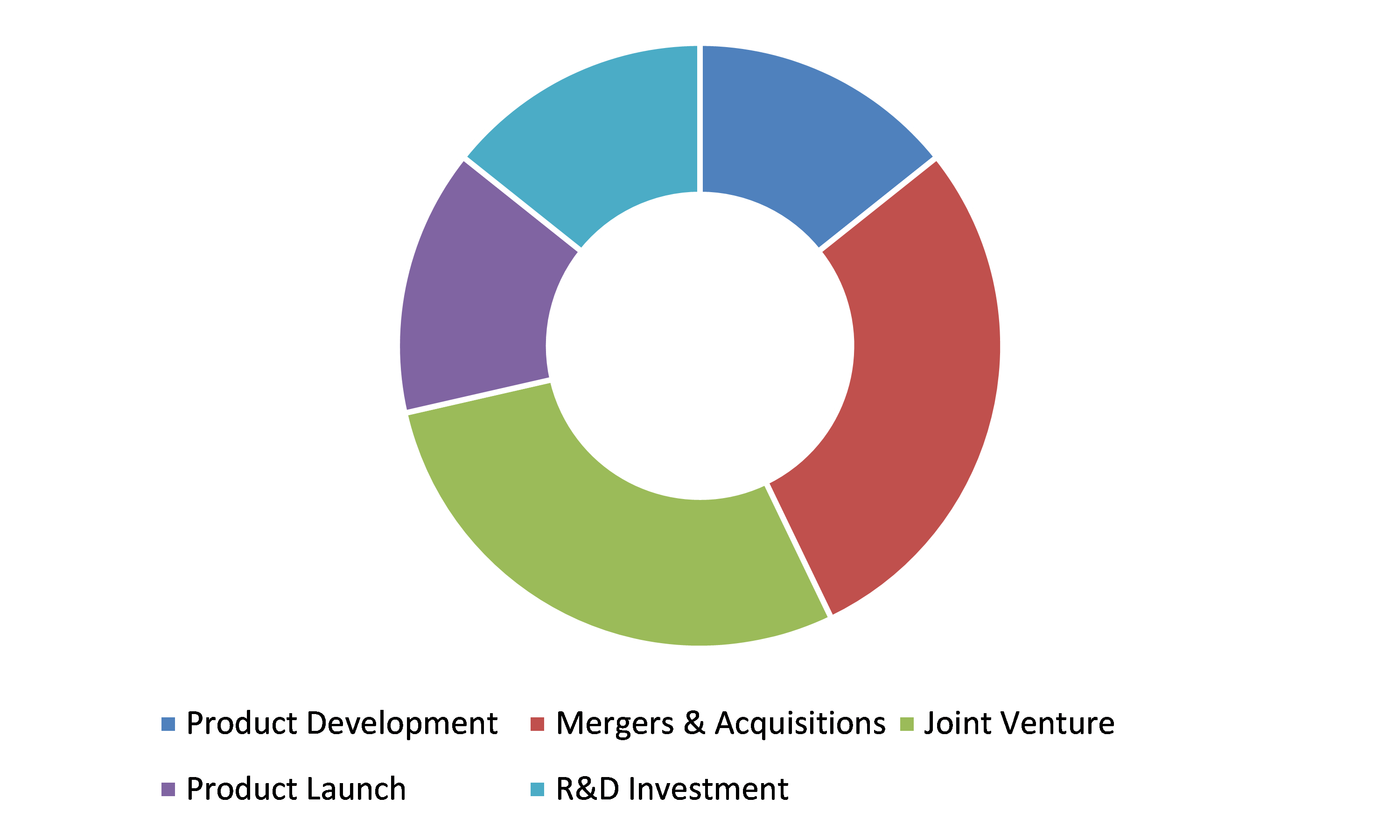

Competitive Scenario in the Global Vascular Disease Devices Market

Product launches and mergers & acquisitions are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading vascular disease devices market players are Medtronic, Abbott Laboratories, Becton, Dickinson and Company, B. Braun Melsungen Ag, Boston Scientific Corporation, Terumo Corporation, Cordis, Ivascular, Merit Medical, and Venus Medtech.

Porter’s Five Forces Analysis for the Global Vascular Disease Devices Market:

- Bargaining Power of Suppliers: The service suppliers of vascular disease devices market are high in number and are larger and more globalized. So, there will be less threat from the suppliers.

Thus, the bargaining power of suppliers is low. - Bargaining Power of Buyers: Buyers demand vascular disease devices that are cost-effective and government approved. This has increased the pressure on the vascular disease devices providers to offer the best product in a cost-effective way. Thus, many suppliers are offering best yet cost–effective vascular disease devices products. This gives the buyers the option to freely choose vascular disease devices that best fit their preferences.

Thus, the bargaining power of the buyers is high. - Threat of New Entrants: Companies entering the vascular disease devices market are adopting various innovations such as developing vascular disease devices that are high tech.

Thus, the threat of the new entrants is moderate. - Threat of Substitutes: The threat of a substitute product or service in vascular disease devices is low because of the presence of highly technical vascular disease devices in the industry.

Thus, the threat of substitutes is low. - Competitive Rivalry in the Market: The competitive rivalry among industry leaders is rather intense, especially between the global players including Medtronic and Abbott Laboratories. These companies are launching their value-added products and services in the international market and strengthening the footprint worldwide.

Therefore, competitive rivalry in the market is high.

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2020 |

| Forecast Timeline for Market Projection | 2021-2028 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product |

|

| Segmentation by End-User |

|

| Key Companies Profiled |

|

Q1. What is the size of the global vascular disease devices market?

A. The size of the global vascular disease devices market was over $13,308.2 million in 2020 and is projected to reach $22,610.3 million by 2028.

Q2. Which are the major companies in the vascular disease devices market?

A. Medtronic and Abbott Laboratories are some of the key players in the global vascular disease devices market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific vascular disease devices market?

A. Asia-Pacific vascular disease devices market is anticipated to grow at 7.7% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Technological development and strategic partnerships are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Medtronic and Abbott Laboratories are investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.By Product trends

2.3.By End-User trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Market value chain analysis

3.8.1.Stress point analysis

3.8.2.Raw material analysis

3.8.3.Manufacturing process

3.8.4.Sales Channel analysis

3.8.5.Operating vendors

3.8.5.1.Raw material suppliers

3.8.5.2.Product manufacturers

3.8.5.3.Product distributors

3.9.Strategic overview

4.Vascular Disease Devices Market, by Product

4.1.Overview

4.1.1.Market size and forecast, by Product

4.2.Stents

4.2.1.Key market trends, growth factors, and opportunities

4.2.2.Market size and forecast, by region, 2020-2028

4.2.3.Market share analysis, by country 2020 & 2028

4.3.Balloons

4.3.1.Key market trends, growth factors, and opportunities

4.3.2.Market size and forecast, by region, 2020-2028

4.3.3.Market share analysis, by country 2020 & 2028

4.4.Catheters

4.4.1.Key market trends, growth factors, and opportunities

4.4.2.Market size and forecast, by region, 2020-2028

4.4.3.Market share analysis, by country 2020 & 2028

4.5.Hemodynamic Flow Alteration Devices

4.5.1.Key market trends, growth factors, and opportunities

4.5.2.Market size and forecast, by region, 2020-2028

4.5.3.Market share analysis, by country 2020 & 2028

4.6.Plaque Modification Devices

4.6.1.Key market trends, growth factors, and opportunities

4.6.2.Market size and forecast, by region, 2020-2028

4.6.3.Market share analysis, by country 2020 & 2028

4.7.Inferior Vena Cava Filters

4.7.1.Key market trends, growth factors, and opportunities

4.7.2.Market size and forecast, by region, 2020-2028

4.7.3.Market share analysis, by country 2020 & 2028

5.Vascular Disease Devices Market, by End-User

5.1.Overview

5.1.1.Market size and forecast, by Sales Channel

5.2.Hospitals and Cardiac Centers

5.2.1.Key market trends, growth factors, and opportunities

5.2.2.Market size and forecast, by region, 2020-2028

5.2.3.Market share analysis, by country 2020 & 2028

5.3.Ambulatory Surgical Center

5.3.1.Key market trends, growth factors, and opportunities

5.3.2.Market size and forecast, by region, 2020-2028

5.3.3.Market share analysis, by country 2020 & 2028

6.Vascular Disease Devices Market, by Region

6.1.Overview

6.1.1.Market size and forecast, by region

6.2.North America

6.2.1.Key market trends, growth factors, and opportunities

6.2.2.Market size and forecast, by Product, 2020-2028

6.2.3.Market size and forecast, by End-User , 2020-2028

6.2.4.Market size and forecast, by country, 2020-2028

6.2.5.U.S.

6.2.5.1.Market size and forecast, by Product, 2020-2028

6.2.6.Market size and forecast, by End-User , 2020-2028

6.2.7.Canada

6.2.7.1.Market size and forecast, by Product, 2020-2028

6.2.8.Market size and forecast, by End-User , 2020-2028

6.2.9.Mexico

6.2.10.Market size and forecast, by End-User , 2020-2028

6.3.Europe

6.3.1.Key market trends, growth factors, and opportunities

6.3.2.Market size and forecast, by Product, 2020-2028

6.3.3.Market size and forecast, by End-User , 2020-2028

6.3.4.Market size and forecast, by country, 2020-2028

6.3.5.Germany

6.3.5.1.Market size and forecast, by Product, 2020-2028

6.3.6.Market size and forecast, by End-User , 2020-2028

6.3.7.UK

6.3.7.1.Market size and forecast, by Product, 2020-2028

6.3.7.2.Market size and forecast, by End-User , 2020-2028

6.3.8.France

6.3.8.1.Market size and forecast, by Product, 2020-2028

6.3.8.2.Market size and forecast, by End-User , 2020-2028

6.3.9.Spain

6.3.9.1.Market size and forecast, by Product, 2020-2028

6.3.9.2.Market size and forecast, by End-User , 2020-2028

6.3.10.Italy

6.3.10.1.Market size and forecast, by Product, 2020-2028

6.3.10.2.Market size and forecast, by End-User , 2020-2028

6.3.11.Rest of Europe

6.3.11.1.Market size and forecast, by Product, 2020-2028

6.3.11.2.Market size and forecast, by End-User , 2020-2028

6.4.Asia Pacific

6.4.1.Key market trends, growth factors, and opportunities

6.4.2.Market size and forecast, by Product, 2020-2028

6.4.3.Market size and forecast, by End-User , 2020-2028

6.4.4.Market size and forecast, by country, 2020-2028

6.4.5.China

6.4.5.1.Market size and forecast, by Product, 2020-2028

6.4.5.2.Market size and forecast, by End-User , 2020-2028

6.4.6.Japan

6.4.6.1.Market size and forecast, by Product, 2020-2028

6.4.6.2.Market size and forecast, by End-User , 2020-2028

6.4.7.India

6.4.7.1.Market size and forecast, by Product, 2020-2028

6.4.7.2.Market size and forecast, by End-User , 2020-2028

6.4.8.South Korea

6.4.8.1.Market size and forecast, by Product, 2020-2028

6.4.8.2.Market size and forecast, by End-User , 2020-2028

6.4.9.Australia

6.4.9.1.Market size and forecast, by Product, 2020 2028

6.4.9.2.Market size and forecast, by End-User , 2020-2028

6.4.9.3.Comparative market share analysis, 2020 & 2028

6.4.10.Rest of Asia Pacific

6.4.10.1.Market size and forecast, by Product, 2020-2028

6.4.10.2.Market size and forecast, by End-User , 2020-2028

6.5.LAMEA

6.5.1.Key market trends, growth factors, and opportunities

6.5.2.Market size and forecast, by Product, 2020-2028

6.5.2.1.Market size and forecast, by End-User , 2020-2028

6.5.3.Market size and forecast, by country, 2020-2028

6.5.4.Latin America

6.5.4.1.Market size and forecast, by Product, 2020-2028

6.5.4.2.Market size and forecast, by End-User , 2020-2028

6.5.5.Middle East

6.5.5.1.Market size and forecast, by Product, 2020-2028

6.5.5.2.Market size and forecast, by End-User , 2020-2028

6.5.6.Africa

6.5.6.1.Market size and forecast, by Product, 2020-2028

6.5.6.2.Market size and forecast, by End-User , 2020-2028

7.Company profiles

7.1. Medtronic

7.1.1.Company overview

7.1.2.Operating business segments

7.1.3.Product portfolio

7.1.4.Financial Performance

7.1.5.Recent strategic moves & developments

7.2.Abbott Laboratories

7.2.1.Company overview

7.2.2.Operating business segments

7.2.3.Product portfolio

7.2.4.Financial Performance

7.2.5.Recent strategic moves & developments

7.3.Becton Dickinson and Company

7.3.1.Company overview

7.3.2.Operating business segments

7.3.3.Product portfolio

7.3.4.Financial Performance

7.3.5.Recent strategic moves & developments

7.4.B. Braun Melsungen Ag

7.4.1.Company overview

7.4.2.Operating business segments

7.4.3.Product portfolio

7.4.4.Financial Performance

7.4.5.Recent strategic moves & developments

7.5.Boston Scientific Corporation

7.5.1.Company overview

7.5.2.Operating business segments

7.5.3.Product portfolio

7.5.4.Financial Performance

7.5.5.Recent strategic moves & developments

7.6.Terumo Corporation

7.6.1.Company overview

7.6.2.Operating business segments

7.6.3.Product portfolio

7.6.4.Financial Performance

7.6.5.Recent strategic moves & developments

7.7.Cordis

7.7.1.Company overview

7.7.2.Operating business segments

7.7.3.Product portfolio

7.7.4.Financial Performance

7.7.5.Recent strategic moves & developments

7.8. Ivascular

7.8.1.Company overview

7.8.2.Operating business segments

7.8.3.Product portfolio

7.8.4.Financial Performance

7.8.5.Recent strategic moves & developments

7.9.Merit Medical

7.9.1.Company overview

7.9.2.Operating business segments

7.9.3.Product portfolio

7.9.4.Financial Performance

7.9.5.Recent strategic moves & developments

7.10.Venus Medtech

7.10.1.Company overview

7.10.2.Operating business segments

7.10.3.Product portfolio

7.10.4.Financial Performance

7.10.5.Recent strategic moves & developments

Although a major part of the world and our lives have been greatly impacted since the outbreak of the coronavirus pandemic, it is promising to know that novel technologies with great potential have dramatically enhanced, especially technologies related to vascular diseases. Vascular diseases devices hold the potential to truly transform the way doctors can avert, analyse, and treat vascular disorders outside of the heart. Vascular disease device makers are developing innovative tools and programs to detect chronic vascular illnesses and perilous diabetic ulcers more keenly to treat the most serious artery blockages in a minimally invasive method, and enhance rehab compliance through novel at-home programs.

The medical industry is eagerly looking forward to bring about huge transformations in existing vascular disease devices, as the number of patient of cardiovascular diseases (CVDs) and related heart disorders is surging at a rapid pace across the globe. CVDs are the foremost reason for death worldwide. Round 17.9 million people expired due to CVDs in 2019, representing 32% of the overall global demises.

Currently, the global vascular disease devices market is perceiving a gigantic growth mostly due to growing number of people falling prey to atherosclerosis disorder, a type of disease that is instigated owing to blockages in arteries owing to build up of fats, cholesterol, and other substances on the walls of arteries.

Latest Trends in the Vascular Disease Devices Market

As per a report by Research Dive, the global vascular disease devices market is expected to grow from $13,308.2 million in 2020 to $22,610.3 million by 2028. Asia-Pacific region is the foremost player in the vascular disease devices market and is expected to grow speedily by garnering a revenue of $5,200.4 million by 2028.

Market players are considerably investing in research and development to cater the mounting demand for vascular disease devices. Some of the leading players of the vascular disease devices market are Dickinson and Company, Abbott Laboratories, Becton, B. Braun Melsungen Ag, Venus Medtech, Boston Scientific Corporation, Medtronic, Terumo Corporation, Ivascular, Merit Medical, Cordis, and others. These players are focused on developing strategies such as mergers and acquisitions, partnerships, novel developments, and collaborations to achieve a prominent position in the global market.

For instance,

- In June 2021, the World Health Organization, a dedicated agency of the United Nations accountable for international public health, launched a list of priority medical devices for the management of cardiovascular ailments and diabetes.

- In November 2021, Otsuka Medical Devices Co., Ltd., a medical device manufacturing company and a completely owned subsidiary of Otsuka Holdings Co., Ltd., introduced the BioMimics 3D Vascular Stent System for patients with peripheral vascular disorders in Japan.

- In September 2021, PocDoc, a digital health platform and personal diagnostics supplier, launched the world’s first smartphone-based test for cardiovascular disorders.

COVID-19 Impact on the Vascular Disease Devices Market

The unexpected rise of the COVID-19 pandemic in 2020 has adversely impacted the global vascular disease devices market. This is mainly owing to the result of the worldwide complete lockdown, and major disruptions in the healthcare sector due to the rising number of COVID-19 patients. Moreover, as several manufacturing industries were ceased amidst the pandemic, the production of the vascular disease devices was severely impacted.

Most of the surgeries got postponed because of strict government regulations regarding performing only critical surgical treatments to avoid spread of COVID-19 infection. All these factors hampered the growth global vascular disease devices market during the pandemic period. However, as the world is recovering with the relaxation of pandemic, the vascular disease devices market is expected to observe notable rise, in the upcoming years, with the growing demand for vascular disease devices owing to rising heart related disorders worldwide.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com