Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

FO21028344 |

Pages: 180 |

Apr 2021 |

The global confectionery market is predicted to garner $227.4 billion in the 2020–2027 timeframe, growing from $189.9 billion in 2019 at a healthy CAGR of 3.7%.

Strategic alliances among market players along with the launching of innovative confectioneries to meet changing consumer demands, is expected to accelerate the growth of the confectionery market.

However, rising awareness of harmful effects of consuming foods with high sugar content like confectioneries is a growth-restricting factor for the market.

According to the regional analysis of the market, the Asia-Pacific confectionery market is anticipated to grow at a CAGR of 4.8% by generating a revenue of $60 billion in 2027 during the review period.

Confectionery involves food items that are rich in carbohydrates and sugars. It includes a wide range of products such as cookies, chocolates, bars, mints, gummies, and others. Confectioneries are mostly popular as welcome gifts and as well as in celebration such as Christmas, Valentine’s Day, Easter, and Halloween, among others.

The novel coronavirus pandemic has had a severe impact on several industries and the confectionery market has been found to experience slow growth during this period. Confectionery industry is intensely affected by the pandemic because the consumption, global trade, production, and manufacturing have all come to a halt. Moreover, reduction in household incomes could translate into lower demand for confectioneries in terms of consumptions. All such factors and close down of restaurants, hotels, coffee shops, and offices have had an adverse impact on the global confectionery demand.

In addition to this, several companies, with their strategic steps, are helping the society to recover from the chaotic situation that COVID-19 has brought with itself. For instance, in March 2020, Mondelēz International Inc., multinational confectionery company in America, announced that they are working on production lines to remain operational during the pandemic and their distributional channel will work efficiently while following all the government guidelines to serve the demands of the public. The above-stated support extended to the society and other company developments, amid the COVID-19 crisis.

The global confectionery industry is witnessing massive growth mainly due to increasing demand for convenient alternatives for sugar-loaded carbohydrates such as sugar-free confections. Moreover, changing lifestyles and health concern such as diabetes, obesity will increase the demand for foods that are high in nutritional value with lower fats and carbohydrates. Such key factors may surge the demand for sugar-free confectioneries and accelerate the growth of global confectionery market.

Moreover, leading market players are adopting various strategies like product innovation for the people with diabetes and those with health consciousness. For example, in April 2018, The Hershey Company, America based chocolate and cocoa products company, announced that their sugar-free confectioneries such as chocolate candy, gums, mints and pastries are trending, as they are using natural sugars from fruits and vegetables, such as polyglucitol and maltitol instead of sugar. Such type of initiatives by manufacturers to use natural sweeteners in confectioneries, may boost the global market for confectionery.

To know more about global confectionery market drivers, get in touch with our analysts here.

The high cost of raw materials such as sugar, cocoa butter, almonds, vanilla and other raw material needed for producing confectionery items is expected to restrain the growth of the global market during the forecast period.

The global confectionery market is growing at a very fast pace due to increasing appeals of snacking that are healthier, tastier and more convenient to eat, will rise the trend of organic chocolates consumption. Also, increasing urbanization with trend of gifting confectionery products will drive the global confectionery market. Moreover, key players involved in the confectionary offer product variation and innovations to attract customers. For instance, Barry Callebaut, world's leading manufacturer of high-quality chocolate and cocoa products, announced in February 2020, that they have launched ‘Milk Chocolate’, it is 100% dairy free chocolate with plant-based indulgence. It is specially designed for the people with preference of healthy confectioneries. These factors are expected to contribute to the market growth globally.

To know more about global confectionery market opportunities, get in touch with our analysts here.

Source: Research Dive Analysis

The chocolate confectionery sub-segment is predicted to have a dominating as well as the fastest growing market in the global market and is expected to register a revenue of $126.5 billion during the forecast period. Chocolate confectioneries are widely consumed and are the most preferred confectioneries across the world, by almost all the age groups. Moreover, gifting chocolate confectioneries are trending as they are important part of the festivals in U.S. The consumption of confectionery such as chocolate treats is associated with many festivals, events, and holidays all over the year such as Halloween, Valentine's Day, Easter, Christmas and Thanksgiving. Furthermore, according to a recent press release on Mar 2021, by NCA (National Confectioners Association), more than 87% of the people in Easter celebration use themed and seasonal chocolates and approximately half of the Americans loves to consume chocolates as their favorite Easter treats. These type of elements and figures may bolster the growth of segment during the forecast period.

Source: Research Dive Analysis

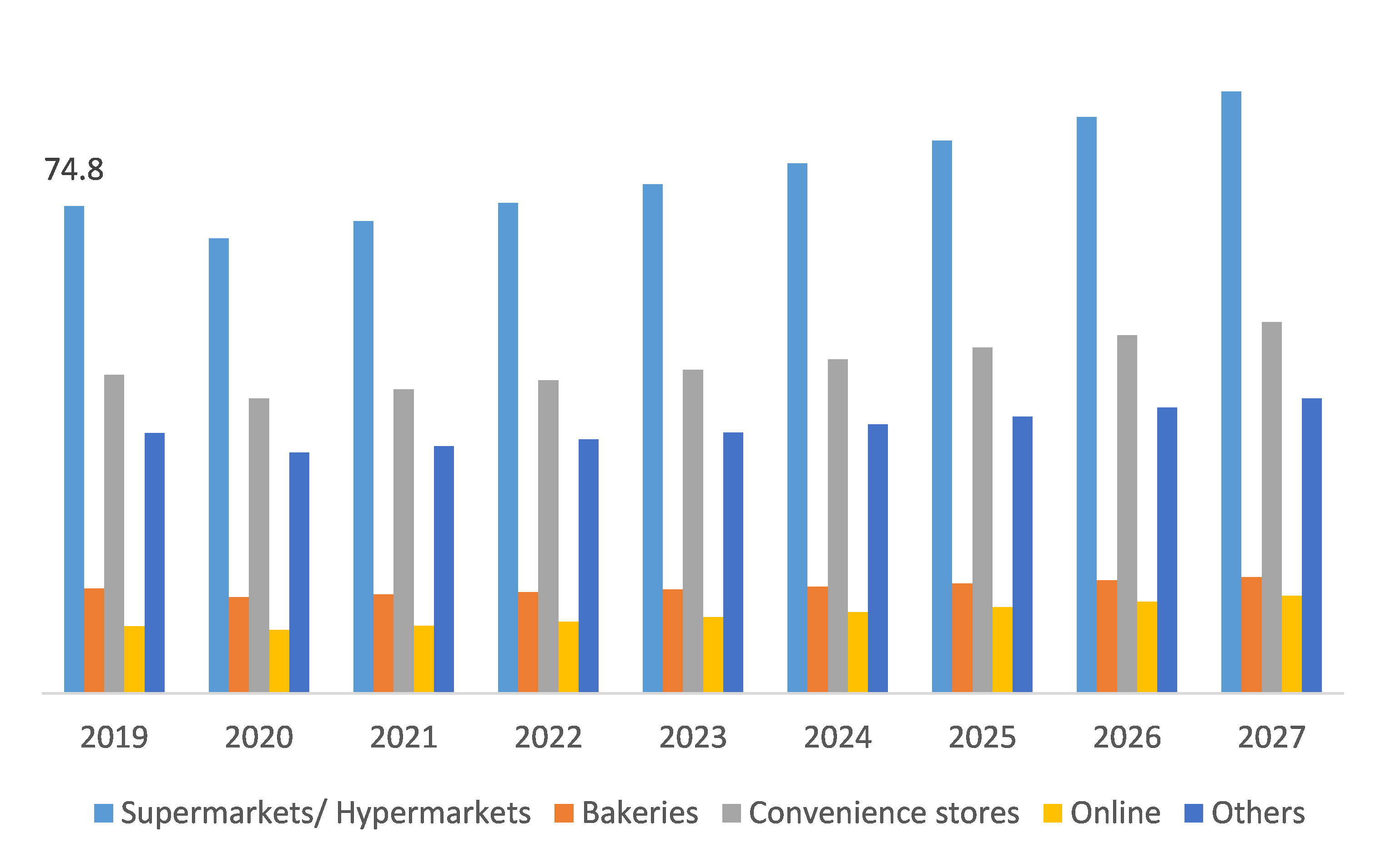

The online sub-segment of the global confectionery market is predicted to have rapid growth and it is expected to surpass $15 billion by 2027, with an increase from $10.3 billion in 2019 owing to increasing working professionals and busy lifestyles; most of the people find it convenient to order confectioneries online. Moreover, online platforms offer a wide range of discounts on online purchase of confectionery for attracting more customers. Furthermore, buying confectioneries online are gaining popularity due to ease of ordering products within less time. For instance, Hershey, American multinational food company, announced on April 2020, that they have experienced higher growth in their online businesses and it was 60% in January and February versus 120% in March 2020. All such factors is expected to flourish the global confectionery market in upcoming years.

The supermarkets/hypermarkets sub-segment is predicted to have a leading market share in confectioneries globally and it is forecast to register a revenue of $92.4 billion during the analysis timeframe owing to availability of diverse range of confectioneries in the supermarket, freedom of selection, and other facilities are expected to increase the sales of confectioneries in supermarkets. Furthermore, shopping in supermarkets offers customers to buy quality goods at affordable and lower prices. Such factors may create huge opportunities for the sub-segment throughout the forecast period.

Source: Research Dive Analysis

The Market for Confectionery in Europe to be the Most Dominant

The Europe confectionery market accounted $77.1 billion in 2019 and is projected to register a revenue of $86.9 billion by 2027. The extensive growth of the European confectionery market is mainly driven by the presence of largest manufacturer of cocoa beans across the region. In addition to this, confectionery platform providers operating in Europe are following strategic collaborations to achieve novel technological innovation and acquire a prominent position in the marketplace. For instance, Ferrero International, manufacturer of branded chocolate and confectionery in Italy, announced that they have acquired Nestle’s U.S confectionery business and it will include more than 20 brans of confectioneries including SweetTarts, BabyRuth, Butterfinger, Crunch, and others. The main aim of the acquisition is to expand Ferrero’s premium confectioneries internationally. These factors will ultimately drive the demand in the European confectionery market across the globe.

The Market for Confectionery in Asia-Pacific to be the Fastest Growing

The share of Asia-Pacific confectionery market is anticipated to grow at a CAGR of 4.8% by registering a revenue of $60 billion by 2027. The growth shall be a result of increasing disposable incomes and growing retail market in Asian countries such as India and China. Also, innovation in products, joint ventures, and private-public strategic alliances will spur the confectionery market size in the foreseeable future. For instance, in June 2019, Cadbury, multinational confectionery company in UK and Mondelez, a multinational confectionery and food company in US, announced that they have launched a new milky bar that has 30% less sugar than normal milky bar in India. Such initiatives and company development may further surge the growth of market, during the analysis timeframe.

Source: Research Dive Analysis

Some of the leading confectionery market players are Mars, Incorporated, The Hershey Company, Nestlé S.A., Mondelez International, Inc., Ferrero Group, Meiji Co., Ltd., , Chocoladefabriken Lindt & Sprüngli AG, pladis Global, Ezaki Glico Co., Ltd. and Haribo GmbH & Co. K.G.

Porter’s Five Forces Analysis for the Global Confectionery Market:

| Aspect | Particulars |

| Historical Market Estimations | 2018-2019 |

| Base Year for Market Estimation | 2019 |

| Forecast Timeline for Market Projection | 2020-2027 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Distribution Channel |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.By type trends

2.3.By distribution channel trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Pricing overview

3.8.1.by Type

3.8.2.by distribution channel type

3.9.Market value chain analysis

3.9.1.Stress point analysis

3.9.2.Raw material analysis

3.9.3.Manufacturing process

3.9.4.Distribution channel analysis

3.9.5.Operating vendors

3.9.5.1.Raw material suppliers

3.9.5.2.Product manufacturers

3.9.5.3.Product distributors

3.10.Strategic overview

4.Confectionery Market, by Type

4.1.Chocolate Confectionery

4.1.1.Market size and forecast, by region, 2019-2027

4.1.2.Comparative market share analysis, 2019 & 2027

4.2.Sugar Confectionery

4.2.1.Market size and forecast, by region, 2019-2027

4.2.2.Comparative market share analysis, 2019 & 2027

4.3.Gum & Candies

4.3.1.Market size and forecast, by region, 2019-2027

4.3.2.Comparative market share analysis, 2019 & 2027

5.Confectionery Market, by distribution channel

5.1.Supermarkets/ Hypermarkets

5.1.1.Market size and forecast, by region, 2019-2027

5.1.2.Comparative market share analysis, 2019 & 2027

5.2.Bakeries

5.2.1.Market size and forecast, by region, 2019-2027

5.2.2.Comparative market share analysis, 2019 & 2027

5.3.Convenience stores

5.3.1.Market size and forecast, by region, 2019-2027

5.3.2.Comparative market share analysis, 2019 & 2027

5.4.Online

5.4.1.Market size and forecast, by region, 2019-2027

5.4.2.Comparative market share analysis, 2019 & 2027

5.5.Others

5.5.1.Market size and forecast, by region, 2019-2027

5.5.2.Comparative market share analysis, 2019 & 2027

6.Confectionery Market, by Region

6.1.North America

6.1.1.Market size and forecast, by type, 2019-2027

6.1.2.Market size and forecast, by Distribution Channel , 2019-2027

6.1.3.Market size and forecast, by country, 2019-2027

6.1.4.Comparative market share analysis, 2019 & 2027

6.1.5.U.S.

6.1.5.1.Market size and forecast, by Type, 2019-2027

6.1.5.2.Market size and forecast, by Distribution Channel , 2019-2027

6.1.5.3.Comparative market share analysis, 2019 & 2027

6.1.6.Canada

6.1.6.1.Market size and forecast, by Type, 2019-2027

6.1.6.2.Market size and forecast, by Distribution Channel , 2019-2027

6.1.6.3.Comparative market share analysis, 2019 & 2027

6.1.7.Mexico

6.1.7.1.Market size and forecast, by Type, 2019-2027

6.1.7.2.Market size and forecast, by Distribution Channel , 2019-2027

6.1.7.3.Comparative market share analysis, 2019 & 2027

6.2.Europe

6.2.1.Market size and forecast, by Type, 2019-2027

6.2.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.3.Market size and forecast, by country, 2019-2027

6.2.4.Comparative market share analysis, 2019 & 2027

6.2.5.Germany

6.2.5.1.Market size and forecast, by Type, 2019-2027

6.2.5.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.5.3.Comparative market share analysis, 2019 & 2027

6.2.6.UK

6.2.6.1.Market size and forecast, by Type, 2019-2027

6.2.6.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.6.3.Comparative market share analysis, 2019 & 2027

6.2.7.France

6.2.7.1.Market size and forecast, by Type, 2019-2027

6.2.7.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.7.3.Comparative market share analysis, 2019 & 2027

6.2.8.Spain

6.2.8.1.Market size and forecast, by Type, 2019-2027

6.2.8.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.8.3.Comparative market share analysis, 2019 & 2027

6.2.9.Italy

6.2.9.1.Market size and forecast, by Type, 2019-2027

6.2.9.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.9.3.Comparative market share analysis, 2019 & 2027

6.2.10.Rest of Europe

6.2.10.1.Market size and forecast, by Type, 2019-2027

6.2.10.2.Market size and forecast, by Distribution Channel , 2019-2027

6.2.10.3.Comparative market share analysis, 2019 & 2027

6.3.Asia Pacific

6.3.1.Market size and forecast, by Type, 2019-2027

6.3.2.Market size and forecast, by Distribution Channel , 2019-2027

6.3.3.Market size and forecast, by country, 2019-2027

6.3.4.Comparative market share analysis, 2019 & 2027

6.3.5.China

6.3.5.1.Market size and forecast, by Type, 2019-2027

6.3.5.2.Market size and forecast, by Distribution Channel , 2019-2027

6.3.5.3.Comparative market share analysis, 2019 & 2027

6.3.6.India

6.3.6.1.Market size and forecast, by Type, 2019-2027

6.3.6.2.Market size and forecast, by Distribution Channel , 2019-2027

6.3.6.3.Comparative market share analysis, 2019 & 2027

6.3.7.Australia

6.3.7.1.Market size and forecast, by Type, 2019-2027

6.3.7.2.Market size and forecast, by Distribution Channel , 2019-2027

6.3.7.3.Comparative market share analysis, 2019 & 2027

6.3.8.Rest of Asia Pacific

6.3.8.1.Market size and forecast, by Type, 2019-2027

6.3.8.2.Market size and forecast, by Distribution Channel , 2019-2027

6.3.8.3.Comparative market share analysis, 2019 & 2027

6.4.LAMEA

6.4.1.Market size and forecast, by Type, 2019-2027

6.4.2.Market size and forecast, by Distribution Channel , 2019-2027

6.4.3.Market size and forecast, by country, 2019-2027

6.4.4.Comparative market share analysis, 2019 & 2027

6.4.5.Latin America

6.4.5.1.Market size and forecast, by Type, 2019-2027

6.4.5.2.Market size and forecast, by Distribution Channel , 2019-2027

6.4.5.3.Comparative market share analysis, 2019 & 2027

6.4.6.Middle East

6.4.6.1.Market size and forecast, by Type, 2019-2027

6.4.6.2.Market size and forecast, by Distribution Channel , 2019-2027

6.4.6.3.Comparative market share analysis, 2019 & 2027

6.4.7.Africa

6.4.7.1.Market size and forecast, by Type, 2019-2027

6.4.7.2.Market size and forecast, by Distribution Channel , 2019-2027

6.4.7.3.Comparative market share analysis, 2019 & 2027

7.Company profiles

7.1.Mars, Incorporated

7.1.1.Business overview

7.1.2.Financial performance

7.1.3.Product portfolio

7.1.4.Recent strategic moves & developments

7.1.5.SWOT analysis

7.2.The Hershey Company

7.2.1.Business overview

7.2.2.Financial performance

7.2.3.Product portfolio

7.2.4.Recent strategic moves & developments

7.2.5.SWOT analysis

7.3.Nestle

7.3.1.Business overview

7.3.2.Financial performance

7.3.3.Product portfolio

7.3.4.Recent strategic moves & developments

7.3.5.SWOT analysis

7.4.Mondelez International, Inc.

7.4.1.Business overview

7.4.2.Financial performance

7.4.3.Product portfolio

7.4.4.Recent strategic moves & developments

7.4.5.SWOT analysis

7.5.Ferrero Group

7.5.1.Business overview

7.5.2.Financial performance

7.5.3.Product portfolio

7.5.4.Recent strategic moves & developments

7.5.5.SWOT analysis

7.6.Meiji Co., Ltd.

7.6.1.Business overview

7.6.2.Financial performance

7.6.3.Product portfolio

7.6.4.Recent strategic moves & developments

7.6.5.SWOT analysis

7.7.Chocoladefabriken Lindt & Sprüngli AG

7.7.1.Business overview

7.7.2.Financial performance

7.7.3.Product portfolio

7.7.4.Recent strategic moves & developments

7.7.5.SWOT analysis

7.8.pladis Global

7.8.1.Business overview

7.8.2.Financial performance

7.8.3.Product portfolio

7.8.4.Recent strategic moves & developments

7.8.5.SWOT analysis

7.9.Ezaki Glico Co., Ltd.

7.9.1.Business overview

7.9.2.Financial performance

7.9.3.Product portfolio

7.9.4.Recent strategic moves & developments

7.9.5.SWOT analysis

7.10.Haribo GmbH & Co. K.G.

7.10.1.Business overview

7.10.2.Financial performance

7.10.3.Product portfolio

7.10.4.Recent strategic moves & developments

7.10.5.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}