Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

FO2007306 |

Pages: 552 |

Dec 2020 |

The global plant based meat market forecast shall be $68,448.9 million by 2027, rising from $17,076.9 million in 2019 at a healthy rate of 19.1%. The North America plant based meat market is expected to surge at a CAGR of 24.3% by registering a revenue of $10,445.3 million, during the projected period. Growing importance of vegan diet products, along with increasing awareness about threat of consumption of tainted meat foods is projected to accelerate the market growth in the region.

Numerous health benefits provided by the plant based meat products including no cholesterol, no antibiotics, and less saturated fats, coupled with the increasing adoption of veganism amongst people, are expected to boost the growth of the plant based meat market.

On the other hand, there is a low product penetration in the underdeveloped countries, which is a growth-restricting factor for the market.

According to the regional analysis, the North America market for plant based meat is expected to garner a revenue of $10,445.3 million, holding the majority of market share during the review period.

Plant-based meat are food products produced from plant materials that are designed to mimic meat in every way, including appearance, smell, texture, and taste. These meat products include common ingredients such as legumes and grains, which are used as fiber, protein, and starch sources.

The outbreak of the Coronavirus disease (COVID-19) has positively impacted the global plant based meat market in the recent months. Increasing vegan population and growth in awareness regarding health benefits provided by vegan food are some of the major factors expected to accelerate the growth of the market in the forecast time.

In addition to this, certain innovative market leaders such as Impossible foods, Conagra, and others are entering into strategic collaboration in order to sustain in the COVID-19 situation. For instance, in April 2020, Impossible Foods, a significant US-based company that develops plant-based substitutes for meat products, teamed up with several organizations including Cheetah, a notable player in restaurants, small business food and grocery supplier, in order to adapt to the COVID-19 crisis. Furthermore, in July 2020, Imagine Meats collaborated with Archer Daniels Midland Company (ADM) in order to enhance plant-based innovations in India.

Such effective collaborations are providing lucrative market opportunities to the global plant based meat market during the COVID-19 situation.

The enormous growth in plant based meat market is mainly attributed to the growing prevalence of chronic conditions such as obesity, cardiovascular diseases (CVDs) among the people, increasing adoption of vegan trend, and entry of innovative market leaders like Unilever in this industry. In recent years, companies dealing with food businesses have witnessed a notable growth in the sales of plant-derived meat products owing to health benefits provided by these products including no cholesterol, less saturated fats, and no antibiotics. For instance, according to records, in July 2020, the PLANT BASED FOODS ASSOCIATION. witnessed 23% growth in the sales of plant-based meat products, when these items were showcased in the meat stores.. Moving ahead, market leaders operating in the global industry are officially entering into the plant derived meat business, which may further create positive impact on the global market. For instance, in December 2018, Unilever, a British-Dutch multinational consumer goods company, acquired Vegetarian Butcher, a notable player in meat substitutes, in order to expand the plant-derived food offerings. Moreover, Unilever has expected to register $1.2 billion sales from plant-based meat and dairy alternatives in the coming 5 to 7 years.

To know more about global plant based meat market drivers, get in touch with our analysts here.

Lower product penetration in under-developed countries is also hampering the global plant based meat market. In addition to this, population allergic to plant-derived meat sources like wheat and soy may restrain the market growth, throughout the projected period.

Increasing government initiatives to generate awareness about the importance of plant-based meats is estimated to boost the market growth and create significant growth opportunities for the global market in the upcoming years. For instance, in 2018, the Indian Ministry of Health and Family Welfare conducted a campaign called “Eat Right India” to promote a sustainable diet featuring plant-based foods to support the fight against climate change. This was a major step because animal agriculture is a leading cause of climate change; every year, agriculture produces about 32,000 million tons of carbon dioxide gas and accounts to nearly 18% of greenhouse gas emissions globally. In 2019, about 107 scientists and researchers prepared a report on global climate change for the United Nation’s Intergovernmental Panel on Climate Change (IPCC) and found the consumption of dairy, meat, and several other animals products to be significant contributors to global warming. These aspects are anticipated to fuel the plant-based meat products' industry growth and are predicted to surge the market growth in the coming years.

To know more about global plant based meat market opportunities, get in touch with our analysts here.

Source: Research Dive Analysis

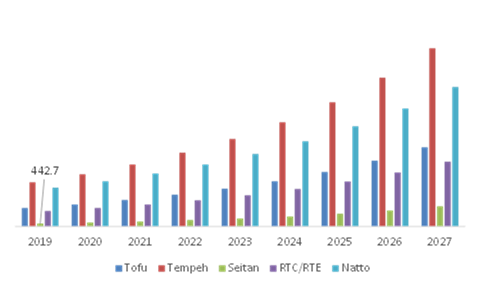

The seitan sub-segment will have a massive market growth and it is expected to generate a revenue of $2850.9 million by 2027, growing from $442.7 million in 2019. The increase in the demand for natural and fresh food products without compromising on meat-like food items is projected to boost the market in the near future. Moreover, some of the key factors boosting seitan’s market are that these food products can be stockpiled for months without losing texture or taste which gives it the upper hand compared to other meat alternatives such as tofu and tempeh.

The tempeh sub-segment will have a magnificent market share and is anticipated to register a revenue of $25,310.8 million by 2027, increasing from $6,283.2 million in 2019. Tempeh also contains probiotics, which help in improving the digestive health and reduces inflammation in the body. The rapid growth in consumer preferences is anticipated to boost the tempeh sub-segment in the upcoming years.

Source: Research Dive Analysis

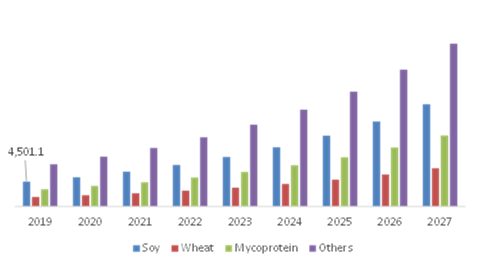

The soy source sub-segment for the global plant based meat industry will have the fastest market growth and is expected to surpass $18,697.6 million by 2027, with a notable surge from $4,501.1 million in 2019 at a remarkable 19.6% CAGR. In modern world, consumers across the globe are adopting more flexible attitudes and behavior regarding food. Hence, established as well as startup companies are serving various food products like mock meat tikkas and plant derived burgers for vegan consumers coupled with non-vegetarian people who are looking to switch for alternatives. For instance, Veggie Champ, an Indian startup dealing with a plant-based meat product, provides mock fish fillet, mock duck, vegan burger, and pepper salami produced with combinations of soy and exotic spices. Moreover, in September 2019, Hormel Foods Corporation., a global branded food establishment with presence in 75 countries worldwide, announced the official launch of its plant-based food range ‘Happy Little Plants’, to fulfill the changing consumer preferences toward veganism and vegetarianism. Under the brand, the company announced to promote and deliver plant-derived soy protein across multiple retail outlets. Such company initiatives and changing consumers preferences are further projected to accelerate the sub-segment growth, during the forecast period.

Source: Research Dive Analysis

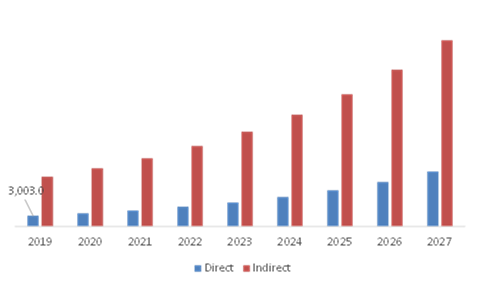

The direct distribution channel for the global plant based meat market will have lucrative growth and is predicted to cross $15,587.4 million by 2027, with an increase from $3,003.0 million in 2019 at a healthy growth rate of 22.9%. Direct distribution channel helps in eliminating intermediary expenses, increasing direct customer contact, and reducing distribution channel options. Furthermore, rise of direct-to-customer trend as well as growing consumer preference are some of the factors are expected to create significant impact on the direct distribution channel sub-segment.

Source: Research Dive Analysis

The North America market for plant based meat products accounted for $1,834.1 million in 2019 and it is expected to register a revenue of $10,445.3 million by the end 2027. Rising importance of vegan diet products over traditional meat foods along with increasing consumer interest and awareness related to threat of consumption of tainted meat foods and their derivates is estimated to fuel the growth of the market in the forecast years. In addition to this, increasing prevalence of chronic diseases such as CVDs is resulting rapid shift of Americans towards veganism. As per study conducted by CDC (Centers for Disease Control and Prevention) 1 person dies in every 36 seconds in the US due to CVDs. Furthermore, according to the online newsletter, around 58% of people in Canada want to decrease their consumption of meat in order to be healthier. Above-stated factors showcases that the need for veganism is expected to dramatically increase in the region, which may further eventually bolster the North America plant based meat market, throughout the forecast period.

Asia-Pacific plant based meat market share is expected to rise at a CAGR of 18.9% by registering a revenue of $30,938.9 million by 2027. This growth is mainly attributed to the supportive government policies, growing disposable income across the Asian countries, and technological innovation in food & beverages industry particularly in China, India, and Japan.

Source: Research Dive Analysis

Some of the leading plant based meat market players include Pinnacle Foods Inc. (Conagra Brands, Inc.), Amy’s Kitchen, Inc., Atlantic Natural Foods, Inc., Lightlife Foods, Inc., Schouten Europe B.V., Sweet Earth, Inc., Impossible Foods Inc., The Kraft Heinz Company, Hain Celestial, Beyond Meat., Pacific Foods of Oregon, LLC, Monde Nissin, Kellogg’s Company, Fry Family Food, Nutrisoy Pty Ltd, Hügli Holding AG, Nasoya Foods, VBites Foods Ltd., Turtle Island Foods, Inc., and Taifun-Tofu GmbH.

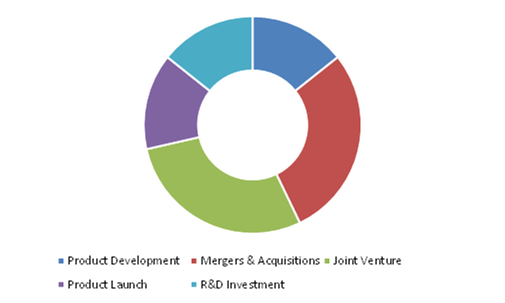

Plant based meat market players are emphasizing on capacity expansion, advanced technical developments, product promotion, and strategic tie-ups in order to strengthen their position in the global market.

| Aspect | Particulars |

| Historical Market Estimations | 2018-2019 |

| Base Year for Market Estimation | 2019 |

| Forecast timeline for Market Projection | 2020-2027 |

| Geographical Scope | North America, Europe, Asia-Pacific, MEA, and Latin America |

| Segmentation by Product Type

|

|

| Segmentation by Source |

|

| Segmentation by Distribution Channel |

|

| Key Countries Covered | The U.S., Canada, Germany, France, Spain, Italy, Russia, Poland, Rest of Europe, China, Australia, Japan, India, ASEAN, New-Zealand, Rest of Asia-Pacific, Mexico, Latin America, Middle East, and South Africa, GCC, Rest of Latin America, Brazil, North Africa |

| Key Companies Profiled |

|

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.4.1. Assumptions

1.4.2. Forecast parameters

1.5. Data sources

1.5.1. Primary

1.5.2. Secondary

2. Executive Summary

2.1. 360° summary

2.2. Product type trends

2.3. Source trends

2.4. Distribution channel trends

3. Market overview

3.1. Market segmentation & definitions

3.2. Key takeaways

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.3. Porter’s five forces analysis

3.3.1. Bargaining power of consumers

3.3.2. Bargaining power of suppliers

3.3.3. Threat of new entrants

3.3.4. Threat of substitutes

3.3.5. Competitive rivalry in the market

3.4. Market dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Technology landscape

3.6. Regulatory landscape

3.7. Patent landscape

3.8. Market value chain analysis

3.9. Strategic overview

4. Plant based meat market, by Product type

4.1. Tofu

4.1.1. Market size and forecast, by region, 2019-2027

4.1.2. Comparative market share analysis, 2019&2027

4.2. Tempeh

4.2.1. Market size and forecast, by region, 2019-2027

4.2.2. Comparative market share analysis, 2019&2027

4.3. Seitan

4.3.1. Market size and forecast, by region, 2019-2027

4.3.2. Comparative market share analysis, 2019&2027

4.4. RTC/RTE

4.4.1. Market size and forecast, by region, 2019-2027

4.4.2. Comparative market share analysis, 2019&2027

4.5. Natto

4.5.1. Market size and forecast, by region, 2019-2027

4.5.2. Comparative market share analysis, 2019&2027

5. Plant based meat market, by Source

5.1. Soy based meat alternatives

5.1.1. Market size and forecast, by region, 2019-2027

5.1.2. Comparative market share analysis, 2019&2027

5.2. Wheat based meat alternatives

5.2.1. Market size and forecast, by region, 2019-2027

5.2.2. Comparative market share analysis, 2019&2027

5.3. Mycoportein meat alternatives

5.3.1. Market size and forecast, by region, 2019-2027

5.3.2. Comparative market share analysis, 2019&2027

5.4. Other source of meat alternatives

5.4.1. Market size and forecast, by region, 2019-2027

5.4.2. Comparative market share analysis, 2019&2027

6. Plant based meat market, by Distribution channel

6.1. Direct

6.1.1. Market size and forecast, by region, 2019-2027

6.1.2. Comparative market share analysis, 2019&2027

6.2. Indirect

6.2.1. Market size and forecast, by region, 2019-2027

6.2.2. Comparative market share analysis, 2019&2027

7. Plant based meat market, by Region

7.1. North America

7.1.1. Market size and forecast, by product type, 2019-2027

7.1.2. Market size and forecast, by source, 2019-2027

7.1.3. Market size and forecast, by distribution channel, 2019-2027

7.1.4. Market size and forecast, by country, 2019-2027

7.1.5. Comparative market share analysis, 2019&2027

7.1.6. U.S.

7.1.6.1. Market size and forecast, by product type, 2019-2027

7.1.6.2. Market size and forecast, by source, 2019-2027

7.1.6.3. Market size and forecast, by distribution channel, 2019-2027

7.1.6.4. Comparative market share analysis, 2019&2027

7.1.7. Canada

7.1.7.1. Market size and forecast, by product type, 2019-2027

7.1.7.2. Market size and forecast, by source, 2019-2027

7.1.7.3. Market size and forecast, by distribution channel, 2019-2027

7.1.7.4. Comparative market share analysis, 2019&2027

7.2. Europe

7.2.1. Market size and forecast, by product type, 2019-2027

7.2.2. Market size and forecast, by source, 2019-2027

7.2.3. Market size and forecast, by distribution channel, 2019-2027

7.2.4. Market size and forecast, by country, 2019-2027

7.2.5. Comparative market share analysis, 2019&2027

7.2.6. Germany

7.2.6.1. Market size and forecast, by product type, 2019-2027

7.2.6.2. Market size and forecast, by source, 2019-2027

7.2.6.3. Market size and forecast, by distribution channel, 2019-2027

7.2.6.4. Comparative market share analysis, 2019&2027

7.2.7. Russia

7.2.7.1. Market size and forecast, by product type, 2019-2027

7.2.7.2. Market size and forecast, by source, 2019-2027

7.2.7.3. Market size and forecast, by distribution channel, 2019-2027

7.2.7.4. Comparative market share analysis, 2019&2027

7.2.8. France

7.2.8.1. Market size and forecast, by product type, 2019-2027

7.2.8.2. Market size and forecast, by source, 2019-2027

7.2.8.3. Market size and forecast, by distribution channel, 2019-2027

7.2.8.4. Comparative market share analysis, 2019&2027

7.2.9. Spain

7.2.9.1. Market size and forecast, by product type, 2019-2027

7.2.9.2. Market size and forecast, by source, 2019-2027

7.2.9.3. Market size and forecast, by distribution channel, 2019-2027

7.2.9.4. Comparative market share analysis, 2019&2027

7.2.10. Italy

7.2.10.1. Market size and forecast, by product type, 2019-2027

7.2.10.2. Market size and forecast, by source, 2019-2027

7.2.10.3. Market size and forecast, by distribution channel, 2019-2027

7.2.10.4. Comparative market share analysis, 2019&2027

7.2.11. Poland

7.2.11.1. Market size and forecast, by product type, 2019-2027

7.2.11.2. Market size and forecast, by source, 2019-2027

7.2.11.3. Market size and forecast, by distribution channel, 2019-2027

7.2.11.4. Comparative market share analysis, 2019&2027

7.2.12. Rest of Europe

7.2.12.1. Market size and forecast, by product type, 2019-2027

7.2.12.2. Market size and forecast, by source, 2019-2027

7.2.12.3. Market size and forecast, by distribution channel, 2019-2027

7.2.12.4. Comparative market share analysis, 2019&2027

7.3. Asia Pacific

7.3.1. Market size and forecast, by product type, 2019-2027

7.3.2. Market size and forecast, by source, 2019-2027

7.3.3. Market size and forecast, by distribution channel, 2019-2027

7.3.4. Market size and forecast, by country, 2019-2027

7.3.5. Comparative market share analysis, 2019&2027

7.3.6. China

7.3.6.1. Market size and forecast, by product type, 2019-2027

7.3.6.2. Market size and forecast, by source, 2019-2027

7.3.6.3. Market size and forecast, by distribution channel, 2019-2027

7.3.6.4. Comparative market share analysis, 2019&2027

7.3.7. India

7.3.7.1. Market size and forecast, by product type, 2019-2027

7.3.7.2. Market size and forecast, by source, 2019-2027

7.3.7.3. Market size and forecast, by distribution channel, 2019-2027

7.3.7.4. Comparative market share analysis, 2019&2027

7.3.8. Japan

7.3.8.1. Market size and forecast, by product type, 2019-2027

7.3.8.2. Market size and forecast, by source, 2019-2027

7.3.8.3. Market size and forecast, by distribution channel, 2019-2027

7.3.8.4. Comparative market share analysis, 2019&2027

7.3.9. Australia

7.3.9.1. Market size and forecast, by product type, 2019-2027

7.3.9.2. Market size and forecast, by source, 2019-2027

7.3.9.3. Market size and forecast, by distribution channel, 2019-2027

7.3.9.4. Comparative market share analysis, 2019&2027

7.3.10. New Zealand

7.3.10.1. Market size and forecast, by product type, 2019-2027

7.3.10.2. Market size and forecast, by source, 2019-2027

7.3.10.3. Market size and forecast, by distribution channel, 2019-2027

7.3.10.4. Comparative market share analysis, 2019&2027

7.3.11. ASEAN

7.3.11.1. Market size and forecast, by product type, 2019-2027

7.3.11.2. Market size and forecast, by source, 2019-2027

7.3.11.3. Market size and forecast, by distribution channel, 2019-2027

7.3.11.4. Comparative market share analysis, 2019&2027

7.3.12. Rest of Asia Pacific

7.3.12.1. Market size and forecast, by product type, 2019-2027

7.3.12.2. Market size and forecast, by source, 2019-2027

7.3.12.3. Market size and forecast, by distribution channel, 2019-2027

7.3.12.4. Comparative market share analysis, 2019&2027

7.4. MEA

7.4.1. Market size and forecast, by product type, 2019-2027

7.4.2. Market size and forecast, by source, 2019-2027

7.4.3. Market size and forecast, by distribution channel, 2019-2027

7.4.4. Market size and forecast, by country, 2019-2027

7.4.5. Comparative market share analysis, 2019&2027

7.4.6. GCC

7.4.6.1. Market size and forecast, by product type, 2019-2027

7.4.6.2. Market size and forecast, by source, 2019-2027

7.4.6.3. Market size and forecast, by distribution channel, 2019-2027

7.4.6.4. Comparative market share analysis, 2019&2027

7.4.7. South Africa

7.4.7.1. Market size and forecast, by product type, 2019-2027

7.4.7.2. Market size and forecast, by source, 2019-2027

7.4.7.3. Market size and forecast, by distribution channel, 2019-2027

7.4.7.4. Comparative market share analysis, 2019&2027

7.4.8. North Africa

7.4.8.1. Market size and forecast, by product type, 2019-2027

7.4.8.2. Market size and forecast, by source, 2019-2027

7.4.8.3. Market size and forecast, by distribution channel, 2019-2027

7.4.8.4. Comparative market share analysis, 2019&2027

7.5. Latin America

7.5.1. Market size and forecast, by product type, 2019-2027

7.5.2. Market size and forecast, by source, 2019-2027

7.5.3. Market size and forecast, by distribution channel, 2019-2027

7.5.4. Market size and forecast, by country, 2019-2027

7.5.5. Comparative market share analysis, 2019&2027

7.5.6. Brazil

7.5.6.1. Market size and forecast, by product type, 2019-2027

7.5.6.2. Market size and forecast, by source, 2019-2027

7.5.6.3. Market size and forecast, by distribution channel, 2019-2027

7.5.6.4. Comparative market share analysis, 2019&2027

7.5.7. Mexico

7.5.7.1. Market size and forecast, by product type, 2019-2027

7.5.7.2. Market size and forecast, by source, 2019-2027

7.5.7.3. Market size and forecast, by distribution channel, 2019-2027

7.5.7.4. Comparative market share analysis, 2019&2027

7.5.8. Rest of Latin America

7.5.8.1. Market size and forecast, by product type, 2019-2027

7.5.8.2. Market size and forecast, by source, 2019-2027

7.5.8.3. Market size and forecast, by distribution channel, 2019-2027

7.5.8.4. Comparative market share analysis, 2019&2027

8. Company profiles

8.1. Pinnacle Foods Inc. (Conagra Brands, Inc.)

8.1.1. Business overview

8.1.2. Financial performance

8.1.3. Product type portfolio

8.1.4. Recent strategic moves & developments

8.1.5. SWOT analysis

8.2. Amy’s Kitchen, Inc.

8.2.1. Business overview

8.2.2. Financial performance

8.2.3. Product type portfolio

8.2.4. Recent strategic moves & developments

8.2.5. SWOT analysis

8.3. Atlantic Natural Foods, Inc.

8.3.1. Business overview

8.3.2. Financial performance

8.3.3. Product type portfolio

8.3.4. Recent strategic moves & developments

8.3.5. SWOT analysis

8.4. Impossible Foods Inc.

8.4.1. Business overview

8.4.2. Financial performance

8.4.3. Product type portfolio

8.4.4. Recent strategic moves & developments

8.4.5. SWOT analysis

8.5. Hain Celestial

8.5.1. Business overview

8.5.2. Financial performance

8.5.3. Product type portfolio

8.5.4. Recent strategic moves & developments

8.5.5. SWOT analysis

8.6. Beyond Meat

8.6.1. Business overview

8.6.2. Financial performance

8.6.3. Product type portfolio

8.6.4. Recent strategic moves & developments

8.6.5. SWOT analysis

8.7. Pacific Foods of Oregon, LLC

8.7.1. Business overview

8.7.2. Financial performance

8.7.3. Product type portfolio

8.7.4. Recent strategic moves & developments

8.7.5. SWOT analysis

8.8. Monde Nissin

8.8.1. Business overview

8.8.2. Financial performance

8.8.3. Product type portfolio

8.8.4. Recent strategic moves & developments

8.8.5. SWOT analysis

8.9. Kellogg’s Company

8.9.1. Business overview

8.9.2. Financial performance

8.9.3. Product type portfolio

8.9.4. Recent strategic moves & developments

8.9.5. SWOT analysis

8.10. Fry Family Food

8.10.1. Business overview

8.10.2. Financial performance

8.10.3. Product type portfolio

8.10.4. Recent strategic moves & developments

8.10.5. SWOT analysis

8.11. Nutrisoy Pty Ltd

8.11.1. Business overview

8.11.2. Financial performance

8.11.3. Product type portfolio

8.11.4. Recent strategic moves & developments

8.11.5. SWOT analysis

8.12. Nasoya Foods

8.12.1. Business overview

8.12.2. Financial performance

8.12.3. Product type portfolio

8.12.4. Recent strategic moves & developments

8.12.5. SWOT analysis

8.13. Hügli Holding AG

8.13.1. Business overview

8.13.2. Financial performance

8.13.3. Product type portfolio

8.13.4. Recent strategic moves & developments

8.13.5. SWOT analysis

8.14. Sweet Earth, Inc.

8.14.1. Business overview

8.14.2. Financial performance

8.14.3. Product type portfolio

8.14.4. Recent strategic moves & developments

8.14.5. SWOT analysis

8.15. VBites Foods Ltd

8.15.1. Business overview

8.15.2. Financial performance

8.15.3. Product type portfolio

8.15.4. Recent strategic moves & developments

8.15.5. SWOT analysis

8.16. The Kraft Heinz Company (KHC)

8.16.1. Business overview

8.16.2. Financial performance

8.16.3. Product type portfolio

8.16.4. Recent strategic moves & developments

8.16.5. SWOT analysis

8.17. Schouten Europe B.V.

8.17.1. Business overview

8.17.2. Financial performance

8.17.3. Product type portfolio

8.17.4. Recent strategic moves & developments

8.17.5. SWOT analysis

8.18. Turtle Island Foods, Inc.

8.18.1. Business overview

8.18.2. Financial performance

8.18.3. Product type portfolio

8.18.4. Recent strategic moves & developments

8.18.5. SWOT analysis

8.19. Lightlife Foods, Inc.

8.19.1. Business overview

8.19.2. Financial performance

8.19.3. Product type portfolio

8.19.4. Recent strategic moves & developments

8.19.5. SWOT analysis

8.20. Taifun-Tofu GmbH

8.20.1. Business overview

8.20.2. Financial performance

8.20.3. Product type portfolio

8.20.4. Recent strategic moves & developments

8.20.5. SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}