Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

LI23058676 |

Pages: 350 |

May 2023 |

Polysomnography (PSG) systems are used to record and analyze sleep studies set up and supervised by sleep medicine professionals in a sleep laboratory. They monitor and record a patient's sleep patterns and physiological features. PSG is a diagnostic method used to assess sleep problems by capturing numerous physiological factors such as brain activity, eye movements, and muscle tone during sleep. There is a rising demand for precise and effective diagnostic tools to assist healthcare professionals in diagnosing and treating sleep disorders as their incidence rises globally. In this aspect, outpatient PSG systems are especially helpful since they let patients perform sleep testing from the convenience of their own homes rather than requiring them to spend the night in a sleep lab. These factors are anticipated to boost the ambulatory polysomnography (PSG) systems market growth in the upcoming years.

However, ambulatory polysomnography (PSG) technologies may not be widely adopted in healthcare institutions because of technological constraints. Due to limitations in the technology used to collect and analyze data, the accuracy and reliability of ambulatory PSG systems may not be as good as those of laboratory PSG systems. For example, the sensors used in ambulatory PSG systems could be less precise or sensitive than the sensors used in laboratory PSG systems, which could lead to data that is unreliable or erroneous. Furthermore, it is possible that the algorithms used to analyze the data gathered by ambulatory PSG systems are less advanced or precise than those employed in laboratory PSG systems.

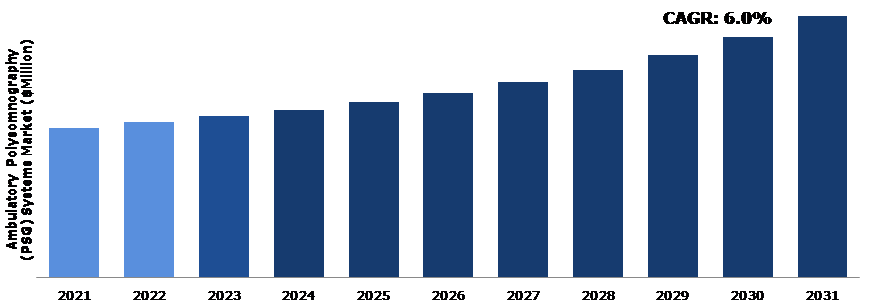

The ambulatory polysomnography (PSG) systems market has a great potential because of the increased demand for portable and home PSG devices. There is an increasing need for portable PSG systems that may be utilized outside of clinical institutions as more people want diagnostic procedures in the convenience of their own homes. Other advantages of portable PSG systems over conventional PSG systems include lower prices and the ability to monitor patients while they are sleeping in their own beds. As a consequence, the findings could be more precise, and the patient's anomalies and sleep patterns might be better understood.

According to regional analysis, the North America ambulatory polysomnography (PSG) systems market size accounted for the highest market share in 2021. The market for ambulatory polysomnography (PSG) systems is in North America because of the high frequency of sleep disorders and the developing understanding of how they affect general health. The area also has a strong acceptance rate for cutting-edge medical technology and a well-developed healthcare infrastructure, all of which contribute to the increase in demand for PSG systems.

Polysomnography, known as a sleep study, is a test used to diagnose sleep disorders. Polysomnography records your brain waves, the oxygen level in your blood, and your heart rate and breathing during sleep. It also measures eye and leg movements. Ambulatory PSG systems are transportable tools that let people carry out sleep studies in their homes as opposed to at a sleep center. These systems generally include a tiny, lightweight recorder worn by patients while they sleep and sensors connected to the patient's legs, chest, face, and scalp.

The market for ambulatory polysomnography (PSG) systems has been significantly impacted by the COVID-19 pandemic. A diagnostic method for evaluating sleep disturbances is polysomnography. With the use of ambulatory polysomnography technology, patients may complete sleep tests in the convenience of their own homes. Many people were hesitant to go to hospitals and clinics for non-urgent treatments, such as sleep testing, during the pandemic. A drop in demand for ambulatory polysomnography systems thus resulted during the pandemic.

The pandemic also affected the supply chain, which slowed down the creation and distribution of polysomnography machinery. Because fewer of these systems were available, this had a bigger effect on the market. However, people want to enhance their sleep quality and general health, and this might result in a rise in the demand for sleep studies and ambulatory polysomnography equipment in the future.

The COVID-19 pandemic has had a mixed impact on the ambulatory polysomnography (PSG) systems market, with a decrease in demand due to patient hesitancy and disruptions in the supply chain, but a potential increase in demand due to increased awareness of the importance of sleep hygiene.

The demand for ambulatory PSG systems is due to an increase in awareness of sleep disorders among healthcare professionals and the general population. The need for diagnostic tools that can reliably identify these diseases is increasing as more individuals become aware of the value of getting good sleep and the potential risks linked to sleep disorders. Because they enable patients to do sleep tests in the comfort of their own homes rather than needing to spend the night in a sleep lab, outpatient PSG systems are growing in popularity. This may make the patient feel more at ease and cause less disruption to regular sleeping habits, producing more precise and trustworthy findings. Furthermore, early detection and treatment of sleep disturbances might lessen the risk of developing significant health issues including heart disease, diabetes, and stroke. As a result, many medical professionals understand the significance of sleep health and are more inclined to advise patients to get PSG testing. The increasing awareness about sleep disorders is driving ambulatory polysomnography (PSG) systems market demand for ambulatory PSG systems, as more people seek to diagnose and treat these conditions early on to prevent serious health complications.

To know more about global ambulatory polysomnography (PSG) systems market drivers, get in touch with our analysts here.

Ambulatory polysomnography's high-cost systems are sophisticated and complicated technologies that require special expertise to maintain and operate. For some healthcare practitioners, the expense of purchasing and maintaining these devices might be a significant hurdle. Additionally, individuals who require these tests could be concerned about the price of PSG equipment. Some individuals can struggle to get access to these tests because they lack health insurance or have substantial out-of-pocket expenses. For underprivileged populations, who may have restricted access to healthcare services generally, this might be a specific issue, which is anticipated to hamper the ambulatory polysomnography (PSG) systems market growth.

The market for ambulatory polysomnography (PSG) systems is experiencing technological developments, which gives businesses a chance to create more complex and cutting-edge PSG systems. PSG systems' precision, dependability, and usability may be significantly increased by using wireless technologies, downsizing hardware, and incorporating AI and ML algorithms. For instance, wireless technology can reduce the need for bulky wires and sensors, making PSG systems more comfortable for patients. While AI and ML algorithms may make it possible to analyze sleep patterns and identify sleep disorders more effectively, the miniaturization of equipment may also make PSG systems more practical and unobtrusive. The need for PSG systems will also increase in the upcoming years due to the rising prevalence of sleep disorders such as sleep apnea, narcolepsy, and insomnia as well as increased awareness of the value of good sleep. This creates a sizable potential for businesses to create and market more sophisticated and approachable PSG devices that can satisfy the expanding demand for sleep diagnoses and monitoring.

To know more about global ambulatory polysomnography (PSG) systems market opportunities, get in touch with our analysts here.

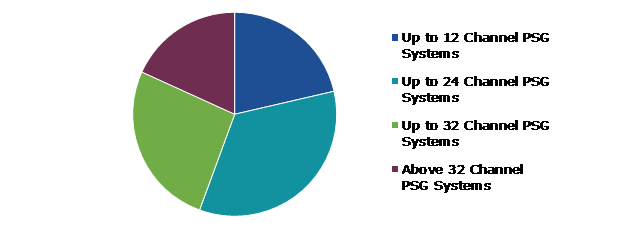

Based on product, the market has been divided into up to 12 channel PSG systems, up to 24 channel PSG systems, up to 32 channel PSG systems and above 32 channel PSG systems. among these, the up to 24 channel PSG systems sub-segment accounted for the highest market share in 2021.

Source: Research Dive Analysis

The up to 24 channel PSG systems sub-type accounted for the highest market share in 2021 and is estimated to show the fastest growth during the forecast period. There is rising demand for more sophisticated PSG systems that offer a more thorough and precise diagnosis of sleep disorders. The detection and monitoring of a variety of physiological signals during sleep, including as brain waves, eye movements, muscle activity, heart rate, and breathing patterns, may be done with high degrees of sensitivity and specificity using PSG systems with up to 24 channels. For the diagnosis and monitoring of sleep disorders such sleep apnea, narcolepsy, restless legs syndrome, and insomnia, these devices are commonly utilized at sleep clinics and research institutes. There is a growing need for better PSG systems that can offer more precise and trustworthy diagnostic information because of the rising prevalence of sleep disorders globally.

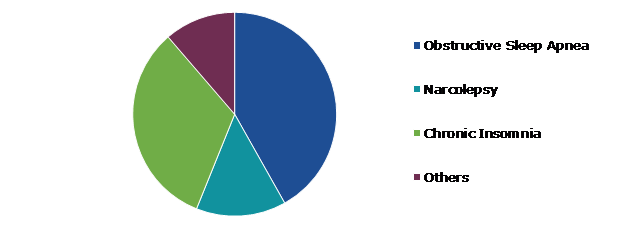

Based on application, the market has been divided into obstructive sleep apnea, narcolepsy, chronic insomnia, and others. Among these, the obstructive sleep apnea sub-segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The obstructive sleep apnea sub-segment accounted for the highest ambulatory polysomnography (PSG) systems market share in 2021. The market for ambulatory polysomnography (PSG) systems has an obstructive sleep sector, which is driven by the rising incidence of sleep apnea and other sleep disorders. Obstructive sleep apnea (OSA) results in breathing difficulties while an individual is asleep and the muscles at the back of the neck fail to facilitate breathing. Demand for diagnostic tools such as ambulatory PSG equipment rises as knowledge of the health dangers linked to untreated sleep apnea grows. These tools let people monitor their sleep apnea and other sleep problems without having to travel to a sleep clinic. Ambulatory PSG systems have also become more precise and user-friendly because of technological advancements, which has further contributed to their rising popularity. These devices may be used to track other aspects including heart rate, brain activity, and oxygen levels. These factors are anticipated to boost the growth of obstructive sleep apnea sub-segment during the analysis timeframe.

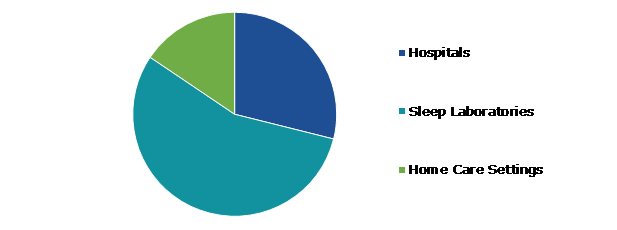

Based on End-user, the market has been divided into hospitals, sleep laboratories, and home care settings. Among these, the sleep laboratories sub-segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The sleep laboratories sub-segment accounted for the highest ambulatory polysomnography (PSG) systems market share in 2021. There are various reasons for ambulatory PSG systems in sleep labs becoming popular. There is an increasing need for diagnosis and treatment services due to the rising incidence of sleep disorders in the world's population. The American Sleep Apnea Association estimates that 22 million Americans had sleep apnea in 2019, which is a major contributor to daytime sleepiness and other health issues. The need for PSG systems in sleep labs is rising as a result of the expanding patient population. The technological advancements in ambulatory PSG systems are also contributing to the growth of the market. The latest PSG systems offer advanced features such as wireless connectivity, cloud-based data management, and improved accuracy and reliability. These features are making PSG systems more user-friendly and efficient, thereby driving their adoption in sleep laboratories. These factors are anticipated to boost the growth of sleep laboratories sub-segment during the analysis timeframe.

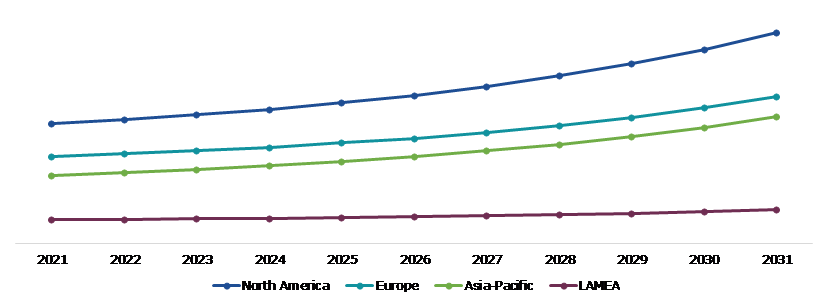

The ambulatory polysomnography (PSG) systems market analysis was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The North America ambulatory polysomnography (PSG) systems market accounted for the highest market share in 2021. In North America, sleep-related problems are quite common, which has increased demand for PSG devices. The need for PSG systems in the area has been further spurred by a rise in patient and healthcare provider awareness of the value of early identification and treatment of sleep disorders. The ambulatory polysomnography (PSG) system market. The market expansion in North America has also been helped by the existence of significant market players such Natus Medical Incorporated, Nihon Kohden Corporation, and Philips Healthcare, which provide sophisticated PSG systems with improved features and capabilities.

Investment and agreement are common strategies followed by major market players. For instance, in August 2020, The FDA has given SOMNOmedics GmbH permission to use SOMNOscreen HD, SOMNOscreen plus, and SOMNOscreen Eco on children as young as two years old.

Source: Research Dive Analysis

Some of the leading ambulatory polysomnography (PSG) systems market players are Koninklijke Philips N.V., Natus Medical Incorporated, Nihon Kohden Corporation, Nox Medical, Löwenstein Medical Technology GmbH + Co. KG., neurosoft, Cadwell Industries Inc., SOMNOmedics GmbH, Compumedics Limited, and Neurovirtual / Sleepvirtual.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product |

|

| Segmentation by Application

|

|

| Segmentation by End-user |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global ambulatory polysomnography (PSG) systems market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on ambulatory polysomnography (PSG) systems market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Ambulatory Polysomnography (PSG) Systems Market Analysis, by Product

5.1.Overview

5.2.Up to 12 Channel PSG Systems

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2031

5.2.3.Market share analysis, by country,2021-2031

5.3.Up to 24 Channel PSG Systems

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2031

5.3.3.Market share analysis, by country,2021-2031

5.4.Up to 32 Channel PSG Systems

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region,2021-2031

5.4.3.Market share analysis, by country,2021-2031

5.5.Above 32 Channel PSG Systems

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region,2021-2031

5.5.3.Market share analysis, by country,2021-2031

5.6.Research Dive Exclusive Insights

5.6.1.Market attractiveness

5.6.2.Competition heatmap

6.Ambulatory Polysomnography (PSG) Systems Market Analysis, by Application

6.1.Obstructive Sleep

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region,2021-2031

6.1.3.Market share analysis, by country,2021-2031

6.2.Apnea Narcolepsy

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2031

6.2.3.Market share analysis, by country,2021-2031

6.3.Chronic Insomnia

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2021-2031

6.3.3.Market share analysis, by country,2021-2031

6.4.Others

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region,2021-2031

6.4.3.Market share analysis, by country,2021-2031

6.5.Research Dive Exclusive Insights

6.5.1.Market attractiveness

6.5.2.Competition heatmap

7.Ambulatory Polysomnography (PSG) Systems Market Analysis, by End-user

7.1.Hospitals

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region,2021-2031

7.1.3.Market share analysis, by country,2021-2031

7.2.Sleep Laboratories

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2031

7.2.3.Market share analysis, by country,2021-2031

7.3.Home Care Settings

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2031

7.3.3.Market share analysis, by country,2021-2031

7.4.Research Dive Exclusive Insights

7.4.1.Market attractiveness

7.4.2.Competition heatmap

8.Ambulatory Polysomnography (PSG) Systems Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Product, 2021-2031

8.1.1.2.Market size analysis, by Application, 2021-2031

8.1.1.3.Market size analysis, by End-user, 2021-2031

8.1.2.Canada

8.1.2.1.Market size analysis, by Product, 2021-2031

8.1.2.2.Market size analysis, by Application, 2021-2031

8.1.2.3.Market size analysis, by End-user, 2021-2031

8.1.3.Mexico

8.1.3.1.Market size analysis, by Product, 2021-2031

8.1.3.2.Market size analysis, by Application, 2021-2031

8.1.3.3.Market size analysis, by End-user, 2021-2031

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Product, 2021-2031

8.2.1.2.Market size analysis, by Application, 2021-2031

8.2.1.3.Market size analysis, by End-user, 2021-2031

8.2.2.UK

8.2.2.1.Market size analysis, by Product, 2021-2031

8.2.2.2.Market size analysis, by Application, 2021-2031

8.2.2.3.Market size analysis, by End-user, 2021-2031

8.2.3.France

8.2.3.1.Market size analysis, by Product, 2021-2031

8.2.3.2.Market size analysis, by Application, 2021-2031

8.2.3.3.Market size analysis, by End-user, 2021-2031

8.2.4.Spain

8.2.4.1.Market size analysis, by Product, 2021-2031

8.2.4.2.Market size analysis, by Application, 2021-2031

8.2.4.3.Market size analysis, by End-user, 2021-2031

8.2.5.Italy

8.2.5.1.Market size analysis, by Product, 2021-2031

8.2.5.2.Market size analysis, by Application, 2021-2031

8.2.5.3.Market size analysis, by End-user, 2021-2031

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Product, 2021-2031

8.2.6.2.Market size analysis, by Application, 2021-2031

8.2.6.3.Market size analysis, by End-user, 2021-2031

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Product, 2021-2031

8.3.1.2.Market size analysis, by Application, 2021-2031

8.3.1.3.Market size analysis, by End-user, 2021-2031

8.3.2.Japan

8.3.2.1.Market size analysis, by Product, 2021-2031

8.3.2.2.Market size analysis, by Application, 2021-2031

8.3.2.3.Market size analysis, by End-user, 2021-2031

8.3.3.India

8.3.3.1.Market size analysis, by Product, 2021-2031

8.3.3.2.Market size analysis, by Application, 2021-2031

8.3.3.3.Market size analysis, by End-user, 2021-2031

8.3.4.Australia

8.3.4.1.Market size analysis, by Product, 2021-2031

8.3.4.2.Market size analysis, by Application, 2021-2031

8.3.4.3.Market size analysis, by End-user, 2021-2031

8.3.5.South Korea

8.3.5.1.Market size analysis, by Product, 2021-2031

8.3.5.2.Market size analysis, by Application, 2021-2031

8.3.5.3.Market size analysis, by End-user, 2021-2031

8.3.6.Rest of Asia Pacific

8.3.6.1.Market size analysis, by Product, 2021-2031

8.3.6.2.Market size analysis, by Application, 2021-2031

8.3.6.3.Market size analysis, by End-user, 2021-2031

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Product, 2021-2031

8.4.1.2.Market size analysis, by Application, 2021-2031

8.4.1.3.Market size analysis, by End-user, 2021-2031

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Product, 2021-2031

8.4.2.2.Market size analysis, by Application, 2021-2031

8.4.2.3.Market size analysis, by End-user, 2021-2031

8.4.3.UAE

8.4.3.1.Market size analysis, by Product, 2021-2031

8.4.3.2.Market size analysis, by Application, 2021-2031

8.4.3.3.Market size analysis, by End-user, 2021-2031

8.4.4.South Africa

8.4.4.1.Market size analysis, by Product, 2021-2031

8.4.4.2.Market size analysis, by Application, 2021-2031

8.4.4.3.Market size analysis, by End-user, 2021-2031

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Product, 2021-2031

8.4.5.2.Market size analysis, by Application, 2021-2031

8.4.5.3.Market size analysis, by End-user, 2021-2031

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Koninklijke Philips N.V.

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Natus Medical Incorporated

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.Nihon Kohden Corporation

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Nox Medical

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Löwenstein Medical Technology GmbH + Co. KG.

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Neurosoft

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.Cadwell Industries Inc.

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.SOMNOmedics GmbH

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.Compumedics Limited

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.Neurovirtual / Sleepvirtual

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}