Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

IC22028561 |

Pages: 260 |

Apr 2023 |

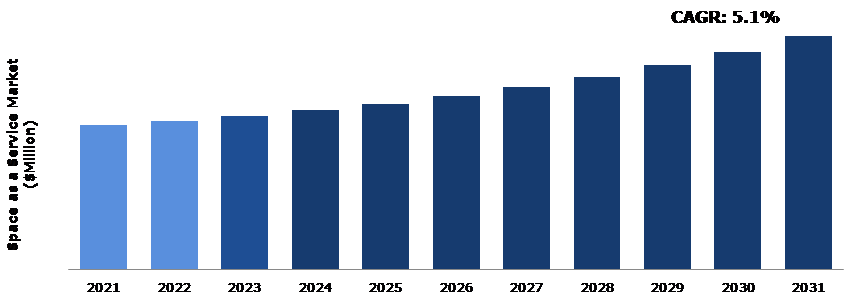

The Space as a Service (SPaaS) market refers to the provision of on-demand access to workspace, meeting rooms, and other office amenities, without the need for long-term leasing or ownership of office space. The factor driving this market is the growing demand for flexible working options and the increasing number of freelancers, entrepreneurs, and small businesses that require affordable, flexible office solutions. Moreover, traditional office leasing can be expensive and inflexible, requiring long-term commitments and large upfront costs. SPaaS provides a cost-effective solution that enables businesses to access the office space they need on a flexible basis. In addition, large corporations are also adopting SPaaS solutions as a way to reduce costs and increase flexibility. SPaaS providers are able to offer a range of options that meet the needs of large companies, including flexible office spaces, meeting rooms, and virtual office solutions. The SPaaS market is being driven by a combination of changing workforce dynamics, technological advancements, and a growing demand for flexible and cost-effective office solutions. These factors are anticipated to boost the space as a Service industry growth in the upcoming years.

However, some of the disadvantages of space as a service include regulatory issues. The SPaaS market is subject to various regulatory issues, including zoning laws, building codes, and health and safety regulations. These regulations can vary depending on location and can impact the ability of providers to offer their services. These regulatory issues can be particularly challenging for space-as-a-service providers who operate in multiple locations, as regulations can vary significantly from one jurisdiction to another. Regulatory issues are an important consideration for anyone looking to enter the space-as-a-service market, and it is important to work closely with legal and regulatory experts to ensure compliance with all relevant laws and regulations.

For business owners and investors hoping to profit from the rising demand for flexible office and workplace solutions, the SPaaS sector offers huge opportunities. SPaaS leading players offer a wide range of services that include meeting rooms, completely furnished workspaces, virtual office solutions, and event spaces that can be rented on a flexible, pay-per-use basis. The SPaaS market is anticipated to grow rapidly in the upcoming years, offering an exciting opportunity for innovative entrepreneurs and investors looking to disrupt the traditional office space rental market.

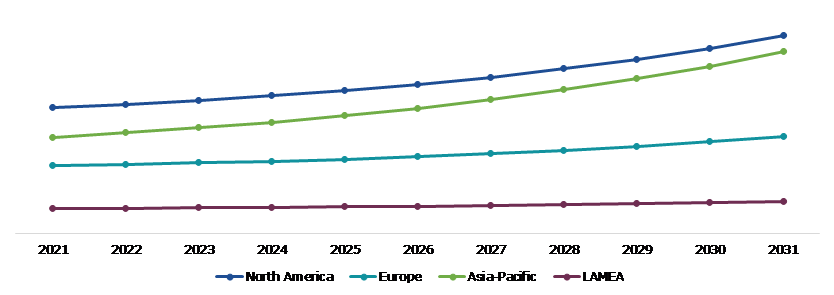

According to regional analysis, the North America space as a service market accounted for the largest market share in 2021 owing to the rising demand for flexible and affordable office solutions. The rise of remote work and the need for hybrid work models further boost the demand for SPaaS in North America.

Space as a Service (SPaaS) is a business model that provides flexible workspace solutions to individuals and organizations on a subscription or pay-per-use basis. This concept is similar to Software as a Service (SaaS), where software applications are offered on a subscription basis instead of being purchased outright. SPaaS providers offer a range of workspace options, including coworking spaces, private offices, meeting rooms, and event spaces. These spaces are fully furnished and equipped with modern amenities such as high-speed internet, printers, and video conferencing equipment.

The COVID-19 pandemic has had a moderate impact on the SPaaS market. During the pandemic, the demand for office and workspace solutions decreased significantly, as many businesses shifted to remote work arrangements to comply with social distancing guidelines and reduce the spread of the virus. This resulted in a decline in occupancy rates and rental revenues for SPaaS providers. However, the pandemic also created new opportunities for SPaaS providers to innovate and adapt to the changing needs of their customers. Many providers introduced new health and safety measures, such as increased cleaning and disinfection, to make their workspaces safer for those who use them. Additionally, some providers shifted their focus towards providing remote work solutions, such as virtual offices and coworking spaces that can be accessed from anywhere. Some SPaaS providers have also adapted to the pandemic by implementing safety measures such as increased sanitation, social distancing protocols, and flexible cancellation policies. They focused on offering more private office spaces, as opposed to shared coworking spaces, to meet the changing demands of the market. Hence, the pandemic caused some disruptions in the SPaaS market. However, it also presented new opportunities for innovation and growth in the long term.

Increasing demand for flexible workspaces is primarily due to the growing trend of the gig economy and remote work. With more people opting for freelance work or working remotely, there is an increasing need for flexible workspaces that can accommodate their changing needs. SPaaS providers offer a range of flexible options such as hot-desking, private offices, and meeting rooms, which can be customized to suit the needs of individual users. These workspaces can be rented on a short-term or long-term basis, allowing users to adjust their space requirements based on their changing needs. Furthermore, SPaaS providers also offer a range of amenities and services such as high-speed internet, printing facilities, and concierge services, which make it easier for users to work efficiently and productively. The increasing demand for flexible workspaces has led to a growth in the SPaaS market, and providers are constantly innovating to provide even more customized solutions to meet the needs of their users.

To know more about global space as a service market driver, get in touch with our analysts here.

The limited availability of suitable properties for conversion into flexible workspaces is a potential restraint for the Space as a Service market. As demand for flexible workspace continues to grow, there may be increased competition for available properties, leading to higher prices and reduced options for providers and customers. A potential restraint of the space-as-a-service market is the lack of customization options available for businesses. While these flexible workspaces offer a range of amenities and services, they may not be able to cater to the unique needs and preferences of individual businesses. This limitation can affect various aspects of the workspace, including layout, design, and functionality, which can ultimately impact the productivity and efficiency of a business, which is anticipated to hamper the space as a service market growth.

The need for SPaaS from SMEs is anticipated to continue to increase during the forecast period. SMEs are increasingly realizing the advantages of flexible office spaces that let them quickly scale their business up or down as required, without incurring high costs and long-term commitments associated with traditional office leases. Moreover, SPaaS providers offer additional services and amenities including IT support and reception services, that can assist SMEs to operate more efficiently and cost-effectively. Many SMEs are looking for alternative solutions to support their distributed workforce because of the COVID-19 pandemic. SPaaS can help SMEs by providing fully equipped office spaces and meeting rooms that are available on a short-term basis and can be booked as needed.

To know more about global space as a service market opportunity, get in touch with our analysts here.

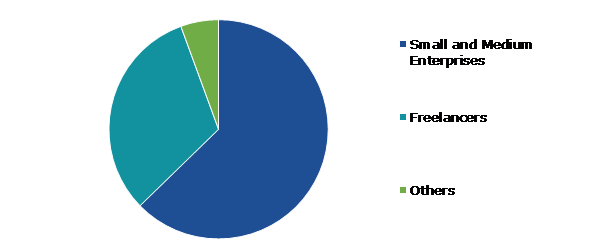

Based on end-user, the market has been divided into small & medium enterprises, freelancers, and others. Among these, the small & medium enterprises sub-segment accounted for the highest market share in 2021 and this sub-segment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The small & medium enterprises sub-segment accounted for the largest market share in 2021. Small and medium enterprises (SMEs) are considered as the backbone of many economies worldwide, and the SPaaS market is not an exception. SMEs require flexible, cost-effective, and scalable workspace solutions to run their businesses. SPaaS providers offer a range of workspace solutions, including co-working spaces, private offices, meeting rooms, and virtual offices, which are specifically designed to meet the needs of SMEs. These solutions provide SMEs with access to high-quality office space without having to invest in expensive real estate, office infrastructure, or long-term lease agreements. These factors are anticipated to boost the growth of small & medium enterprises sub-segment during the analysis timeframe.

The space as a service market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The SPaaS market in North America is being driven by several key factors. The rise of remote work has led to an increased demand for flexible and adaptable workspace solutions. In addition, technological advancements have facilitated SPaaS providers to offer a range of amenities and services, such as high-speed internet, meeting rooms, and reception services, which attracted businesses of all sizes. The growing focus on sustainability and energy efficiency in this region is expected to increase the demand for SPaaS solutions providers that offer environmentally friendly buildings and spaces.

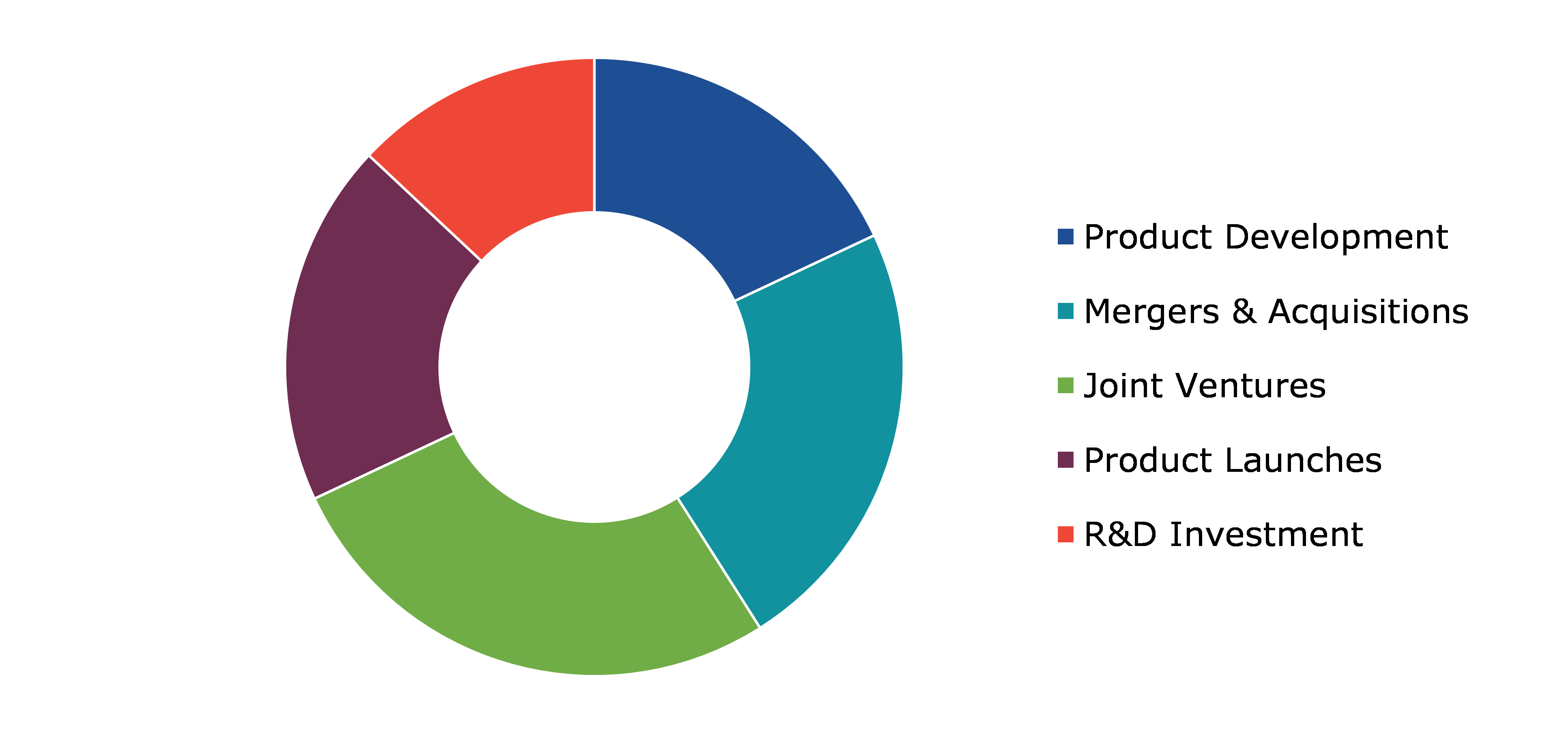

Investment and agreement are common strategies followed by major market players. For instance, in November 2021, Awfis, an Indian company using the space as a service business model, collaborated with the American real estate service company CBRE and the startup agritech company WayCool. For the three parties engaged in the transaction, this cooperation has created a number of new business opportunities because they can each strengthen their position in their respective industries by combining their own skills.

Source: Research Dive Analysis

Some of the leading space as a service market players are WeWork, 91springboard, Awfis, Common Ground, Innov8, Workbar LLC, Regus, Colive, MindSpace, and Industrious.

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by End-use |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global space as a service market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on space as a service market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Space as a Service Market Analysis, by End-user

5.1.Small & Medium Enterprises

5.1.1.Definition, key trends, growth factors, and opportunities

5.1.2.Market size analysis, by region,2021-2031

5.1.3.Market share analysis, by country,2021-2031

5.2.Freelancers

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2031

5.2.3.Market share analysis, by country,2021-2031

5.3.Others

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2031

5.3.3.Market share analysis, by country,2021-2031

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Space as a Service Market, by region

6.1.North America

6.1.1.U.S.

6.1.1.1.Market size analysis, by End-user,2021-2031

6.1.2.Canada

6.1.2.1.Market size analysis, by End-user,2021-2031

6.1.3.Mexico

6.1.3.1.Market size analysis, by End-user,2021-2031

6.1.4.Research Dive Exclusive Insights

6.1.4.1.Market attractiveness

6.1.4.2.Competition heatmap

6.2.Europe

6.2.1.Germany

6.2.1.1.Market size analysis, by End-user,2021-2031

6.2.2.UK

6.2.2.1.Market size analysis, by End-user,2021-2031

6.2.3.France

6.2.3.1.Market size analysis, by End-user,2021-2031

6.2.4.Spain

6.2.4.1.Market size analysis, by End-user,2021-2031

6.2.5.Italy

6.2.5.1.Market size analysis, by End-user,2021-2031

6.2.6.Rest of Europe

6.2.6.1.Market size analysis, by End-user,2021-2031

6.2.7.Research Dive Exclusive Insights

6.2.7.1.Market attractiveness

6.2.7.2.Competition heatmap

6.3.Asia Pacific

6.3.1.China

6.3.1.1.Market size analysis, by End-user,2021-2031

6.3.2.Japan

6.3.2.1.Market size analysis, by End-user,2021-2031

6.3.3.India

6.3.3.1.Market size analysis, by End-user,2021-2031

6.3.4.Australia

6.3.4.1.Market size analysis, by End-user,2021-2031

6.3.5.South Korea

6.3.5.1.Market size analysis, by End-user,2021-2031

6.3.6.Rest of Asia Pacific

6.3.6.1.Market size analysis, by End-user,2021-2031

6.3.7.Research Dive Exclusive Insights

6.3.7.1.Market attractiveness

6.3.7.2.Competition heatmap

6.4.LAMEA

6.4.1.Brazil

6.4.1.1.Market size analysis, by End-user,2021-2031

6.4.2.Saudi Arabia

6.4.2.1.Market size analysis, by End-user,2021-2031

6.4.3.UAE

6.4.3.1.Market size analysis, by End-user,2021-2031

6.4.4.South Africa

6.4.4.1.Market size analysis, by End-user,2021-2031

6.4.5.Rest of LAMEA

6.4.5.1.Market size analysis, by End-user,2021-2031

6.4.6.Research Dive Exclusive Insights

6.4.6.1.Market attractiveness

6.4.6.2.Competition heatmap

7.Competitive Landscape

7.1.Top winning strategies, 2021

7.1.1.By strategy

7.1.2.By year

7.2.Strategic overview

7.3.Market share analysis, 2021

8.Company Profiles

8.1.WeWork

8.1.1.Overview

8.1.2.Business segments

8.1.3.Product portfolio

8.1.4.Financial performance

8.1.5.Recent developments

8.1.6.SWOT analysis

8.2.91springboard

8.2.1.Overview

8.2.2.Business segments

8.2.3.Product portfolio

8.2.4.Financial performance

8.2.5.Recent developments

8.2.6.SWOT analysis

8.3.Awfis

8.3.1.Overview

8.3.2.Business segments

8.3.3.Product portfolio

8.3.4.Financial performance

8.3.5.Recent developments

8.3.6.SWOT analysis

8.4.Common Ground

8.4.1.Overview

8.4.2.Business segments

8.4.3.Product portfolio

8.4.4.Financial performance

8.4.5.Recent developments

8.4.6.SWOT analysis

8.5.Innov8

8.5.1.Overview

8.5.2.Business segments

8.5.3.Product portfolio

8.5.4.Financial performance

8.5.5.Recent developments

8.5.6.SWOT analysis

8.6.Workbar LLC

8.6.1.Overview

8.6.2.Business segments

8.6.3.Product portfolio

8.6.4.Financial performance

8.6.5.Recent developments

8.6.6.SWOT analysis

8.7.Regus

8.7.1.Overview

8.7.2.Business segments

8.7.3.Product portfolio

8.7.4.Financial performance

8.7.5.Recent developments

8.7.6.SWOT analysis

8.8.Colive

8.8.1.Overview

8.8.2.Business segments

8.8.3.Product portfolio

8.8.4.Financial performance

8.8.5.Recent developments

8.8.6.SWOT analysis

8.9.MindSpace

8.9.1.Overview

8.9.2.Business segments

8.9.3.Product portfolio

8.9.4.Financial performance

8.9.5.Recent developments

8.9.6.SWOT analysis

8.10.Industrious

8.10.1.Overview

8.10.2.Business segments

8.10.3.Product portfolio

8.10.4.Financial performance

8.10.5.Recent developments

8.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}