Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

LI21098496 |

Pages: 240 |

Sep 2021 |

The global liver disease treatment market is anticipated to garner $32,028.5 million in the 2021–2028 period, rising from $13,348.3 million in 2020, at a noteworthy CAGR of 11.7%.

Growing government awareness programs to create enormous impact on the global liver disease treatment market.

However, less availability along with high investment cost of drugs particularly across the developing nations may obstruct the global liver disease treatment market growth.

According to the regional analysis of the liver disease treatment market, Asia-Pacific region is anticipated to surge at a CAGR of 14.0%, by registering a revenue of $4,099.7 million, during the forecast period.

Liver is the largest solid internal organ in the body which helps in removing toxins from the blood supply. It also regulates blood clotting, performs hundreds of other vital functions, and maintains healthy blood sugar levels. However, any disturbance in the functioning of liver that causes illness is a liver disease (hepatic disease). The signs and symptoms associated with liver disease includes abdominal pain and swelling, jaundice, dark urine color, itchy skin, and nausea.

In response to the Covid-19 pandemic, business sectors namely transportation, petroleum, retail, and tourism industry have been forced to reconsider their business models and policies. Global liver disease treatment market has also witnessed declined growth, throughout the pandemic period mainly because of disruption in supply chain along with halt in the novel drug development projects.

On the other hand, alcohol-associated liver disease (ALD) surged as significant number of people drank more throughout the COVID-19 crisis. For example, in 2020, according to the UK's Office for National Statistics, country’s largest independent producer of official statistics, approximately 80% of the alcohol-associated deaths were due to ALD. Furthermore, key players operating in the liver disease treatment market are coming up with effective collaborations. For instance, in December 2020 Gilead Sciences, Inc., an American research-based biopharmaceutical company, announced the acquisition of MYR GmbH, a German based healthcare company emphasized on the development and commercialization of therapeutics for the chronic liver disease treatment. Gilead announced to acquire MYR for around $1.36 billion in cash. Such huge investments may further create significant opportunities for the investors, post COVID-19 outbreak.

Liver disease specifically non-alcoholic fatty liver disease (NAFLD) is the abnormal accumulation of excess fat in the liver. NAFLD is emerging as the main cause of chronic liver disorder in the developing countries such as India and China. Hence, government bodies are coming up with novel and attractive programs to fight with liver diseases. For instance, in February 2021, Indian government announced the integration of NAFLD in the National Program for prevention & Control of Cancer, Diabetes, Cardiovascular Diseases & stroke (NPCDCS). This program is mainly focused on multiple factors including early diagnosis and management of NAFLD, along with building healthcare infrastructure for prevention, diagnosis, and treatment of NAFLD. Such government initiatives may further flourish the market for liver disease treatment market, in the forecast period.

To know more about global liver disease treatment market drivers, get in touch with our analysts here.

Requirement of high investment in the development of liver disease treatment drugs may restrict the global liver disease treatment market growth, in the analysis period. Moreover, stringent government policies by Medicines and Healthcare products Regulatory Agency (MHRA) and U.S. Food and Drug Administration (FDA) combined with side effect associated with medicines are some the factors hampering the global market growth.

The prevalence of liver diseases remains high worldwide particularly in the Latin American and Middle East countries. The death rate caused by liver disease in Egypt is by far the highest across the globe, followed by other African countries. For example, as per data published in 2018 by World life expectancy, the largest global health and life expectancy database, liver disease death rate per 100,000 patients in Egypt, Nigeria, Ivory Coast, and São Tomé is 116.0, 64.4, 62.1, and, 60.7 respectively. Further, according to the, Translational Gastroenterology and Hepatology, an open-access, peer-reviewed, international, PubMed-indexed online journal, prevalence of NAFLD in the Middle East region was around 32% in 2019. Hence, the demand for liver disease medications is expected to grow exponentially.

Therefore, government bodies of the Middle East countries are coming up to fight against liver diseases. For example, in June 2019, Egypt government announced that it would be supplying hepatitis C testing and treatment facilities for 1 million people in an around 14 African countries. The initiative would be undertaken in the economies including Chad, Burundi, Djibouti, the Democratic Republic of Congo, Eritrea, Equatorial Guinea, Kenya, Ethiopia, Mali, South Sudan, Somalia, Sudan, Uganda, and Tanzania. Such government developments are expected to create market opportunities in the coming years.

To know more about global liver disease treatment market opportunities, get in touch with our analysts here.

[TREATMENTTYPEGRAPH]

Source: Research Dive Analysis

The antiviral drugs sub-segment is projected to have the dominating share of the liver disease treatment market size in 2020, and it is expected to register a revenue of $13,503.3 million by 2028. Significantly growing investments in the field of antiviral drugs, mainly owing to its enormous benefits is creating positive impact on the antiviral drug’s sub-segment. In addition, increase in healthcare expenditure, surge in the public awareness, and growing incidence of hepatitis B and C are some important factors projected to continue to augment market growth.

Moreover, prominent players of the market are coming up with novel innovations in order to strengthen their presence worldwide. For example, In June 2021, Gilead Sciences, an American biopharmaceutical company, proposed a plan to file for approval of ‘Hepcludex’, the antiviral drug for hepatitis D virus (HDV) in the US. Hepcludex is an excellent entry inhibitor registered in Russia as ‘Myrcludex B’ and also granted by the European Commission. Such company inventions are further expected to create enormous opportunities, across the globe.

[DISEASETYPEGRAPH]

Source: Research Dive Analysis

The non-alcoholic fatty liver disease sub-segment of the global liver disease treatment market is estimated to grow at the most notable CAGR and surpass $3,667.2 million by 2028, with a rise from $1,380.6 million in 2020.Massive increase in the prevalence of obesity worldwide, increase in awareness about liver conditions in developing region, upsurge in diabetes, and notable R&D funding are some of the crucial factors propelling the sub-segments growth. Further, according to the National Diabetes Statistics Report, 2020 published by CDC, almost 34.2 million people have diabetes in the US (10.5% of US population) and it is a 7th leading cause of death in the country. These key elements are further anticipated to drive the demand for NAFLD medications market.

Along with this, improvisation of healthcare infrastructure and availability of proper diagnostic facilities for treatment of the disease is likely to boost the sub-segment’s growth, in the forecast period.

The hepatitis sub-segment of the global liver disease treatment market will have largest share and it is projected surpass $21,729.3 million by 2028, with a rise from $9.124.4 million in 2020. In recent several years, the inflammation condition of liver tissue has massively increased owing to the medication errors, excessive alcohol consumption, autoimmune diseases, viral infection, and nonalcoholic steatohepatitis. According to the WHO, in 2019, almost 290,000 patients died from hepatitis C along with 820, 000 patients died from hepatitis B across the globe. Such facts & figures showcase that the demand for hepatitis medications are expected increase notably, which will accelerate the sub-segment’s growth, in the analysis period.

Also, increasing awareness regarding hepatitis treatment medicines including tenofovir (Viread), entecavir (Baraclude), adefovir (Hepsera) lamivudine (Epivir), and telbivudine (Tyzeka) across the developing regions is also creating positive impact on the sub-segment’s growth.

[ENDUSERGRAPH]

Source: Research Dive Analysis

The hospitals sub-segment of the global liver disease treatment market is expected to have dominating share and grow at the most notable CAGR. The hospital sub-segment will surpass $22,276.3 million by 2028, with a rise from $9,325.8 million in 2020.Availability of the integrated liver treatment hospitals across the European and American countries with a dedicated team comprising some of the best liver surgeons and hepatologists is one of the major factors driving the sub-segment’s growth. Also, modernization of healthcare facilities along with government’s favorable schemes are accelerating the growth of hospitals sub-segment. In addition to this, increasing occurrence of chronic liver diseases such as live tumor and cirrhosis is also making positive impact on the hospital sub-segment.

Source: Research Dive Analysis

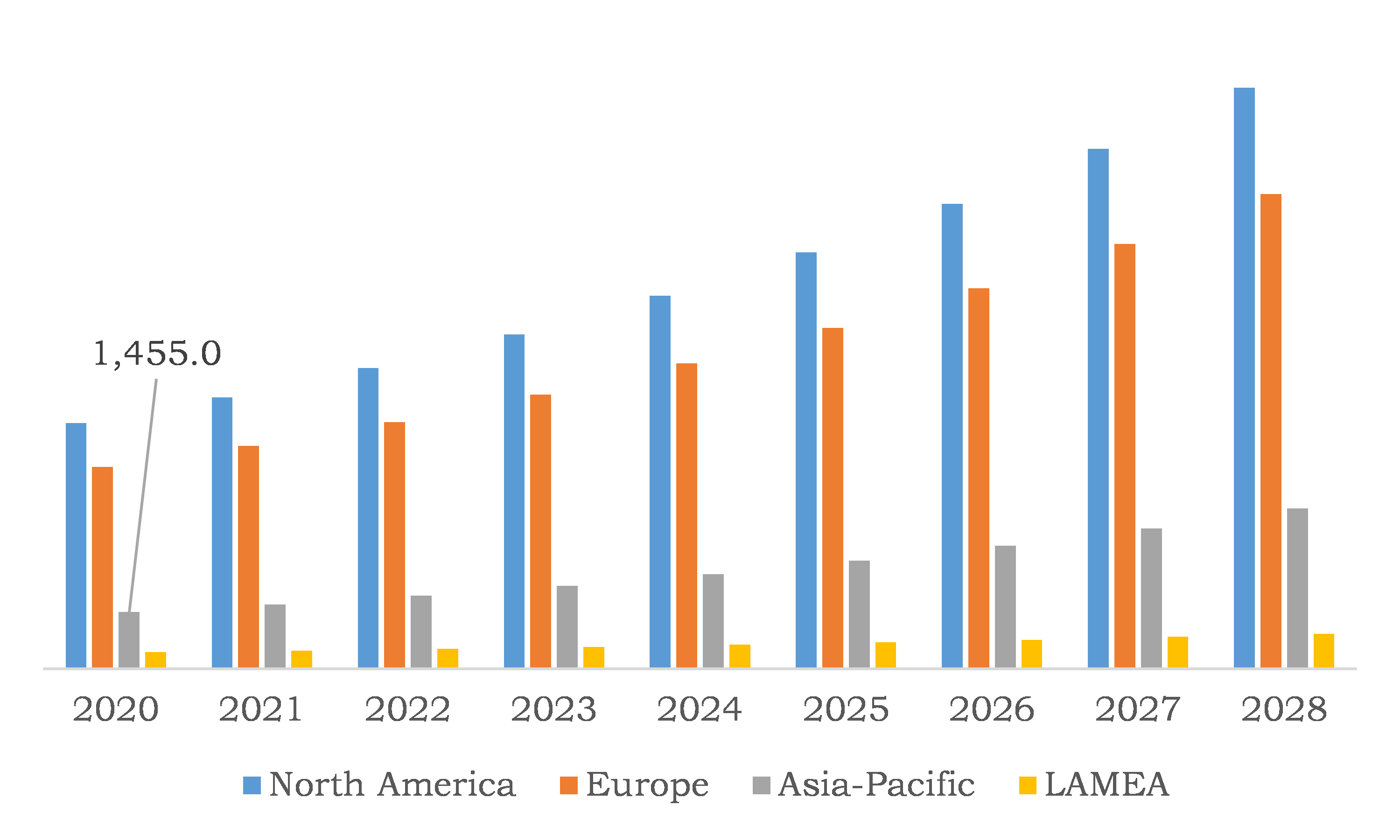

Asia-Pacific liver disease treatment market accounted $1,455.0 million in 2020 and is expected to register a revenue of $4,099.7 million by 2028.

The extensively increasing need for advanced and innovative liver disease therapeutics particularly in China, India, and South Korea is one of the key elements boosting the development of the industry. Also, one of the major factors behind this growth can be the increasing prevalence of NAFLD and hepatitis, lack of expertise, and the poor healthcare infrastructure in the region. Further, aging population combined with dramatic growth in the overweight and obesity rates in China and Australia is raising the chances of liver disease, which is further expected to boost the demand for liver disease treatment market, in the region.

Liver disease treatment market for North America region is highly competitive and leading companies in the market are adopting multiple strategies to garner highest North America liver disease treatment market share. North America liver disease treatment market accounted $6,287.1 million in 2020 and is expected to register a revenue of $14,861.2 million by 2028.

Massive Increase in the alcohol consumption along with use of illegal drugs are some of the crucial factors that contributes toward the liver disease market growth in the North America region. For example, according to the 2019 national survey on drug use and health (NSDUH), US based survey that gives up-to date information on alcohol and tobacco, almost 85.6 % of people aging 18 and older found that they drank alcoholic beverages at some point in their life-span, in the US. Moreover, around 54.9% Americans reported that they consumed alcohol in the past months. These facts & figures showcase that the demand for treatment of alcohol- related cirrhosis and hepatitis is expected to increase, which may accelerate the North America liver disease treatment market, in the forecast period.

Also, companies operating in the region are following strategic tie-ups to deal with liver diseases. For example, in April 2019, Gilead Sciences Inc., an American biopharmaceutical firm headquartered in California, announced to collaborate with Novo Nordisk, Denmark-based leading healthcare company for the development of a liver disease drug molecule. As per this agreement, Gilead may combine firsocostat and cilofexor, its investigational drugs with Novo Nordisk's semaglutide in order to treat NASH. Such company initiatives are also further expected to create novel opportunities in the global market.

Source: Research Dive Analysis

Some of the leading Liver disease treatment market players are Pfizer Inc., Johnson & Johnson Services, Inc., F. Hoffmann-La Roche Ltd, GlaxoSmithKline plc., Sanofi, Novartis AG, Bayer AG, Bristol Myers Squibb (BMS), Gilead Sciences, Inc., and AbbVie.

Porter’s Five Forces Analysis for the Global Liver Disease Treatment Market:

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2020 |

| Forecast timeline for Market Projection | 2021-2028 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Treatment type |

|

| Segmentation by Disease Type |

|

| Segmentation by End-user |

|

| Key Countries Covered | U.S., Canada, Mexico, Germany, France, UK, Italy, Spain, Russia, Rest of Europe, China, Japan, India, Australia, South Korea, Rest of Asia-Pacific, Brazil, Saudi Arabia, United Arab Emirates, Rest of LAMEA |

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.By treatment trends

2.3.By disease type trends

2.4.By end user trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Pricing overview

3.8.1.by treatment

3.8.2.by disease type

3.8.3.by end user

3.9.Market value chain analysis

3.9.1.Stress point analysis

3.9.2.Raw material analysis

3.9.3.Manufacturing process

3.9.4.Distribution channel analysis

3.9.5.Operating vendors

3.9.5.1.Raw material suppliers

3.9.5.2.Product manufacturers

3.9.5.3.Product distributors

3.10.Strategic overview

4.Liver Disease Treatment Market, by Treatment

4.1.Anti-Rejection Drugs/Immunosupressants

4.1.1.Market size and forecast, by region, 2020-2028

4.1.2.Comparative market share analysis, 2020 & 2028

4.2.Chemotherapy Drugs

4.2.1.Market size and forecast, by region, 2020-2028

4.2.2.Comparative market share analysis, 2020 & 2028

4.3.Targeted Therapy

4.3.1.Market size and forecast, by region, 2020-2028

4.3.2.Comparative market share analysis, 2020 & 2028

4.4.Vaccines

4.4.1.Market size and forecast, by region, 2020-2028

4.4.2.Comparative market share analysis, 2020 & 2028

4.5.Anti-Viral Drugs

4.5.1.Market size and forecast, by region, 2020-2028

4.5.2.Comparative market share analysis, 2020 & 2028

5.Liver Disease Treatment Market, by Disease type

5.1.Hepatitis

5.1.1.Market size and forecast, by region, 2020-2028

5.1.2.Comparative market share analysis, 2020 & 2028

5.2.Liver Cancer

5.2.1.Market size and forecast, by region, 2020-2028

5.2.2.Comparative market share analysis, 2020 & 2028

5.3.Non-Alcoholic Fatty Liver Disease

5.3.1.Market size and forecast, by region, 2020-2028

5.3.2.Comparative market share analysis, 2020 & 2028

5.4.Others

5.4.1.Market size and forecast, by region, 2020-2028

5.4.2.Comparative market share analysis, 2020 & 2028

6.Liver Disease Treatment Market, by End User

6.1.Hospitals

6.1.1.Market size and forecast, by region, 2020-2028

6.1.2.Comparative market share analysis, 2020 & 2028

6.2.Ambulatory Surgery Centers

6.2.1.Market size and forecast, by region, 2020-2028

6.2.2.Comparative market share analysis, 2020 & 2028

6.3.Other End Users

6.3.1.Market size and forecast, by region, 2020-2028

6.3.2.Comparative market share analysis, 2020 & 2028

7.Liver Disease Treatment Market, by Region

7.1.North America

7.1.1.Market size and forecast, by treatment, 2020-2028

7.1.2.Market size and forecast, by disease type, 2020-2028

7.1.3.Market size and forecast, by end user, 2020-2028

7.1.4.Market size and forecast, by country, 2020-2028

7.1.5.Comparative market share analysis, 2020 & 2028

7.1.6.U.S.

7.1.6.1.Market size and forecast, by treatment, 2020-2028

7.1.6.2.Market size and forecast, by disease type, 2020-2028

7.1.6.3.Market size and forecast, by end user, 2020-2028

7.1.6.4.Comparative market share analysis, 2020 & 2028

7.1.7.Canada

7.1.7.1.Market size and forecast, by treatment, 2020-2028

7.1.7.2.Market size and forecast, by disease type, 2020-2028

7.1.7.3.Market size and forecast, by end user, 2020-2028

7.1.7.4.Comparative market share analysis, 2020 & 2028

7.1.8.Mexico

7.1.8.1.Market size and forecast, by treatment, 2020-2028

7.1.8.2.Market size and forecast, by disease type, 2020-2028

7.1.8.3.Market size and forecast, by end user, 2020-2028

7.1.8.4.Comparative market share analysis, 2020 & 2028

7.2.Europe

7.2.1.Market size and forecast, by treatment, 2020-2028

7.2.2.Market size and forecast, by disease type, 2020-2028

7.2.3.Market size and forecast, by end user, 2020-2028

7.2.4.Market size and forecast, by country, 2020-2028

7.2.5.Comparative market share analysis, 2020 & 2028

7.2.6.Germany

7.2.6.1.Market size and forecast, by treatment, 2020-2028

7.2.6.2.Market size and forecast, by disease type, 2020-2028

7.2.6.3.Market size and forecast, by end user, 2020-2028

7.2.6.4.Comparative market share analysis, 2020 & 2028

7.2.7.UK

7.2.7.1.Market size and forecast, by treatment, 2020-2028

7.2.7.2.Market size and forecast, by disease type, 2020-2028

7.2.7.3.Market size and forecast, by end user, 2020-2028

7.2.7.4.Comparative market share analysis, 2020 & 2028

7.2.8.France

7.2.8.1.Market size and forecast, by treatment, 2020-2028

7.2.8.2.Market size and forecast, by disease type, 2020-2028

7.2.8.3.Market size and forecast, by end user, 2020-2028

7.2.8.4.Comparative market share analysis, 2020 & 2028

7.2.9.Spain

7.2.9.1.Market size and forecast, by treatment, 2020-2028

7.2.9.2.Market size and forecast, by disease type, 2020-2028

7.2.9.3.Market size and forecast, by end user, 2020-2028

7.2.9.4.Comparative market share analysis, 2020 & 2028

7.2.10.Italy

7.2.10.1.Market size and forecast, by treatment, 2020-2028

7.2.10.2.Market size and forecast, by disease type, 2020-2028

7.2.10.3.Market size and forecast, by end user, 2020-2028

7.2.10.4.Comparative market share analysis, 2020 & 2028

7.2.11.Rest of Europe

7.2.11.1.Market size and forecast, by treatment, 2020-2028

7.2.11.2.Market size and forecast, by disease type, 2020-2028

7.2.11.3.Market size and forecast, by end user, 2020-2028

7.2.11.4.Comparative market share analysis, 2020 & 2028

7.3.Asia Pacific

7.3.1.Market size and forecast, by treatment, 2020-2028

7.3.2.Market size and forecast, by disease type, 2020-2028

7.3.3.Market size and forecast, by end user, 2020-2028

7.3.4.Market size and forecast, by country, 2020-2028

7.3.5.Comparative market share analysis, 2020 & 2028

7.3.6.China

7.3.6.1.Market size and forecast, by treatment, 2020-2028

7.3.6.2.Market size and forecast, by disease type, 2020-2028

7.3.6.3.Market size and forecast, by end user, 2020-2028

7.3.6.4.Comparative market share analysis, 2020 & 2028

7.3.7.India

7.3.7.1.Market size and forecast, by treatment, 2020-2028

7.3.7.2.Market size and forecast, by disease type, 2020-2028

7.3.7.3.Market size and forecast, by end user, 2020-2028

7.3.7.4.Comparative market share analysis, 2020 & 2028

7.3.8.Japan

7.3.8.1.Market size and forecast, by treatment, 2020-2028

7.3.8.2.Market size and forecast, by disease type, 2020-2028

7.3.8.3.Market size and forecast, by end user, 2020-2028

7.3.8.4.Comparative market share analysis, 2020 & 2028

7.3.9.South Korea

7.3.9.1.Market size and forecast, by treatment, 2020-2028

7.3.9.2.Market size and forecast, by disease type, 2020-2028

7.3.9.3.Market size and forecast, by end user, 2020-2028

7.3.9.4.Comparative market share analysis, 2020 & 2028

7.3.10.Australia

7.3.10.1.Market size and forecast, by treatment, 2020-2028

7.3.10.2.Market size and forecast, by disease type, 2020-2028

7.3.10.3.Market size and forecast, by end user, 2020-2028

7.3.10.4.Comparative market share analysis, 2020 & 2028

7.3.11.Rest of Asia Pacific

7.3.11.1.Market size and forecast, by treatment, 2020-2028

7.3.11.2.Market size and forecast, by disease type, 2020-2028

7.3.11.3.Market size and forecast, by end user, 2020-2028

7.3.11.4.Comparative market share analysis, 2020 & 2028

7.4.LAMEA

7.4.1.Market size and forecast, by treatment, 2020-2028

7.4.2.Market size and forecast, by disease type, 2020-2028

7.4.3.Market size and forecast, by end user, 2020-2028

7.4.4.Market size and forecast, by country, 2020-2028

7.4.5.Comparative market share analysis, 2020 & 2028

7.4.6.Latin America

7.4.6.1.Market size and forecast, by treatment, 2020-2028

7.4.6.2.Market size and forecast, by disease type, 2020-2028

7.4.6.3.Market size and forecast, by end user, 2020-2028

7.4.6.4.Comparative market share analysis, 2020 & 2028

7.4.7.Middle East

7.4.7.1.Market size and forecast, by treatment, 2020-2028

7.4.7.2.Market size and forecast, by disease type, 2020-2028

7.4.7.3.Market size and forecast, by end user, 2020-2028

7.4.7.4.Comparative market share analysis, 2020 & 2028

7.4.8.Africa

7.4.8.1.Market size and forecast, by treatment, 2020-2028

7.4.8.2.Market size and forecast, by disease type, 2020-2028

7.4.8.3.Market size and forecast, by end user, 2020-2028

7.4.8.4.Comparative market share analysis, 2020 & 2028

8.Company profiles

8.1.Pfizer Inc.

8.1.1.Business overview

8.1.2.Financial performance

8.1.3.Product portfolio

8.1.4.Recent strategic moves & developments

8.1.5.SWOT analysis

8.2.Johnson & Johnson Services, Inc.

8.2.1.Business overview

8.2.2.Financial performance

8.2.3.Product portfolio

8.2.4.Recent strategic moves & developments

8.2.5.SWOT analysis

8.3.F. Hoffmann-La Roche Ltd

8.3.1.Business overview

8.3.2.Financial performance

8.3.3.Product portfolio

8.3.4.Recent strategic moves & developments

8.3.5.SWOT analysis

8.4.GlaxoSmithKline plc.

8.4.1.Business overview

8.4.2.Financial performance

8.4.3.Product portfolio

8.4.4.Recent strategic moves & developments

8.4.5.SWOT analysis

8.5.Sanofi

8.5.1.Business overview

8.5.2.Financial performance

8.5.3.Product portfolio

8.5.4.Recent strategic moves & developments

8.5.5.SWOT analysis

8.6.Novartis AG

8.6.1.Business overview

8.6.2.Financial performance

8.6.3.Product portfolio

8.6.4.Recent strategic moves & developments

8.6.5.SWOT analysis

8.7.Bayer AG

8.7.1.Business overview

8.7.2.Financial performance

8.7.3.Product portfolio

8.7.4.Recent strategic moves & developments

8.7.5.SWOT analysis

8.8.Bristol Myers Squibb (BMS)

8.8.1.Business overview

8.8.2.Financial performance

8.8.3.Product portfolio

8.8.4.Recent strategic moves & developments

8.8.5.SWOT analysis

8.9.Gilead Sciences, Inc.

8.9.1.Business overview

8.9.2.Financial performance

8.9.3.Product portfolio

8.9.4.Recent strategic moves & developments

8.9.5.SWOT analysis

8.10.AbbVie

8.10.1.Business overview

8.10.2.Financial performance

8.10.3.Product portfolio

8.10.4.Recent strategic moves & developments

8.10.5.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}