Military Embedded Systems Market Report

RA08415

Military Embedded Systems Market by Product Type (Motherboard & Computer-On-module (COM), OPEN VPX, VME Bus, Compact-PCI (Board & Serial), and Others), Component Type (Hardware and Software), Platform Type (Airborne, Land, Naval, and Space), Application (Radar, Command & Control, Avionics, Electronic Warfare, Communication & Navigation, Weapon Fire Control System, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2031

Global Military Embedded Systems Market Analysis

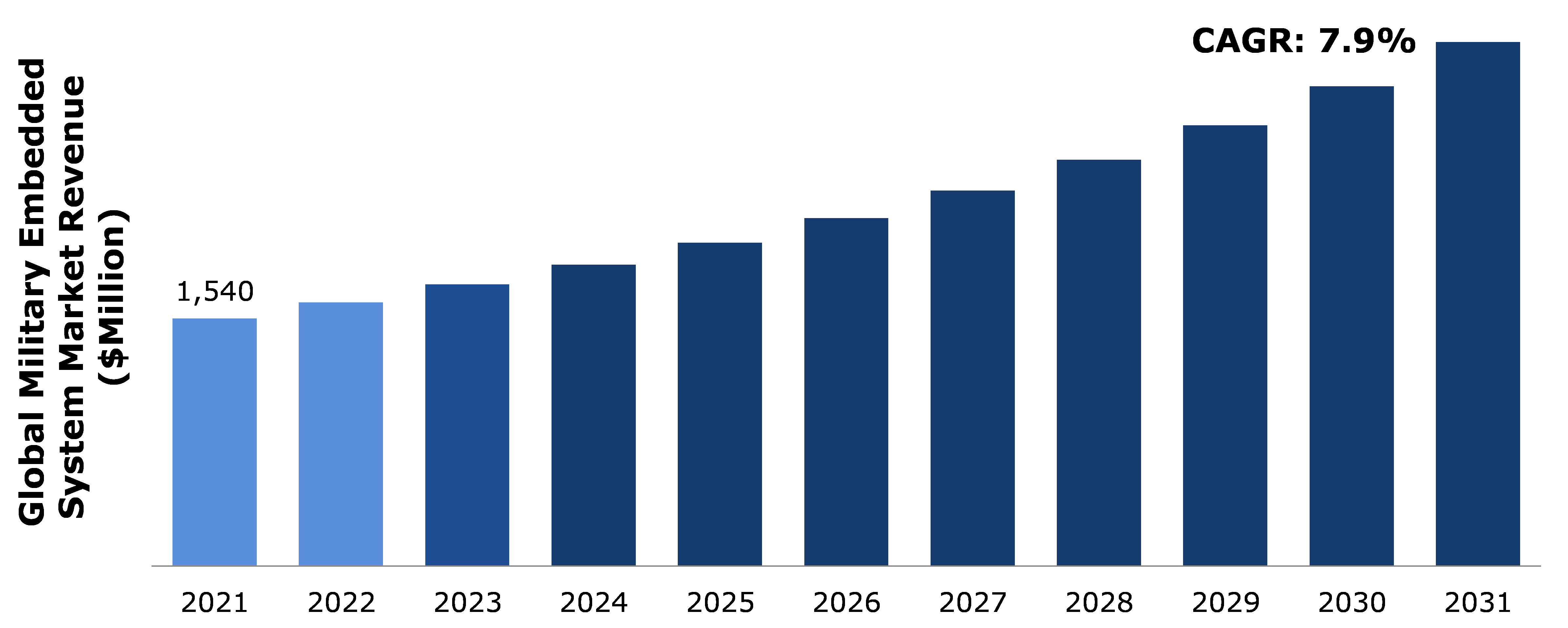

The Global Military Embedded Systems Market Size was $1,540 million in 2021 and is predicted to grow with a CAGR of 7.9%, by generating revenue of $3,259.3 million by 2031.

Global Military Embedded Systems Market Synopsis

Embedded systems are widely employed in industries such as home automation, healthcare, business, the military, and others. An embedded system is a hardware and software combination based on a microprocessor or microcontroller and intended to carry out specific tasks within a broader mechanical or electrical system. An integrated circuit built to perform computing for real-time processes is at the heart of the system. Military eEmbedded sSystems focuses on embedded electronics software and hardware for military applications by providing technical coverage of every stage of the design process. Access to the most recent technology is essential in the military and defense industries.

The majority of today's cutting-edge technologies rely on computing and embedded systems to support the unique requirements of the military. The general-purpose embedded systems utilized in civilian applications are not the same as the embedded systems used in military applications. Compared to general-purpose embedded systems, military embedded systems must be more efficient, dependable, secure, and tough. These systems provide the highest level of security to prevent reverse engineering or data interception in situations like rising terrorism or hacking.

Major factors limiting military embedded systems market share growth include an increase in the complexity of developing embedded products and the necessity for system design certification for system upgrades. In addition, the military embedded software market will face additional challenges during the forecast period due to rising barriers in designing military embedded systems and crucial security procedures in embedded devices.

In recent years, there has been a significant advancement in military electronics. High durability, effectiveness, and simplicity of structure are some of the most important requirements for electronic equipment and systems employed in military applications. Since most traditional radar systems employ set frequencies, it is simple to recognize, comprehend, and create defenses against them. But on the contrary, modern digitally programmable radars have the capacity of producing waveforms that have not yet been observed, making them harder to counter. As a result, market players can develop quick and flexible electronic warfare systems that can identify and block sophisticated sensors. It is anticipated that these developments will open up a wealth of options.

According to regional analysis, the North American military embedded systems market accounted for highest market growth in 2021 and is predicted to grow with a considerable CAGR in the projected timeframe.

Military Embedded Systems Overview

A system is a configuration where each of its component parts operates in accordance with clearly defined principles. It is a way of setting up, carrying out, or carrying out a task or tasks in accordance with a predetermined plan. An embedded system is a physical computer system with integrated software that uses a semiconductor microprocessor to carry out a particular task as a stand-alone or large-scale system. The central component of embedded systems is an integrated circuit designed to advance computing activities and processes in real-time. From simple linked peripherals to complicated connected microcontrollers, from no UI to realistic graphical UI, embedded systems can be simple to use. They can be constructed at any level of deep collaboration, depending on their tasks. Their use included everything from electric vehicles to military equipment.

COVID-19 Impact on Global Military Embedded Systems Market

The COVID-19 pandemic created several uncertainties, resulting in significant economic losses as various businesses around the world came to a halt. The disruption of supply chain, closure of manufacturing plants, slowdown of economies across several countries have resulted in a reduction in demand for military embedded systems. In addition, due to the lockdown policies and restrictions imposed by the government on migrants and workers working in the manufacturing plants were unable to reach their locations, which affected the production and supply of embedded systems. The supply chain problems have temporarily halted the production of these systems, despite the fact that their manufacturing for military purposes is of the utmost importance. The degree of COVID-19 exposure a nation experiences, the efficiency of its manufacturing processes, and import-export regulations are just a few of the factors that affect when manufacturing and demand pick back up. Orders may still be accepted by businesses, but delivery schedules might not be set in stone. During the pandemic, for instance, to reduce the COVID-19 outbreak, various government and healthcare institutions used various embedded systems, such as deep learning-based embedded surveillance systems, to monitor, detect, and report effected COVID-19 virus patients. All these factors severely affected the growth of military embedded systems market size growth in the pandemic time.

Increase in Government Expenditure in the Military Sector is Anticipated to Drive the Market Growth

Government financing hikes in the military budget are anticipated to fuel market expansion. Modernizing military and defense equipment is a priority for governments around the world. Due to this circumstance, the global supply for unmanned applications and the military embedded systems market opportunity have increased significantly. In addition, the widespread adoption of multi-core processors, wireless technologies, and revolutionary warfare systems is anticipated to support the growth of the military embedded systems market revenue during the next few decades. For instance, on 25 April, 2022, report published by Stockholm International Peace Research Institute (SIPRI), the U.S, China, India, the U.K., and Russia jointly accounted for 62% of expenditure in 2021. In 2021, total worldwide military spending will increase by 0.7% in real terms to $2113 billion.

Legal Concerns and Security Issues Might Restrict the Military Embedded Systems Market Growth

Ensuring security in embedded systems translates into many architectural problems imposed by these systems' specific properties. Due to these characteristics, it is impractical to integrate traditional security measures, necessitating a deeper comprehension of the overall security issue. Because embedded systems lack additional processing power, these devices frequently aim to use as few processor cycles and programmed memory as possible. Therefore, the security issues faced by embedded devices cannot be solved by security solutions made for PCs. In actuality, the security measures of the PC will not be used by the majority of embedded devices. This presents several security difficulties for embedded systems.

Development of Electronic Warfare Systems with Increased Capabilities is Expected to Increase the Opportunities

The world is moving toward a more complete integration of digital technology into modern life, to digitally empower people and boost the transfer of technology. The electronics and communication industries have experienced broad growth as a result, and there has been a noticeable rise in the convergence of cyber, electronic, and optical technologies. In recent times, nations' focus has switched to the newest electronic warfare technology. Electronic warfare (EW) refers to any military activity that uses the electromagnetic spectrum or focused energy, such as laser, to prevent or limit the use of the electromagnetic spectrum by the enemy while preserving the spectrum for ally forces. For instance, to oppose U.S. forces in the Indo-Pacific region, China is constructing its anti-access (A2/AD) defensive system. Furthermore, the U.S. intends to create the idea of a multi-domain (or cross-domain) battle, which is centered on creating military electronic warfare tools that concentrate on eliminating adversaries across all domains, including the electromagnetic spectrum, cyberspace, land, and water.

To know more about global Military Embedded Systems market opportunities, get in touch with our analysts here.

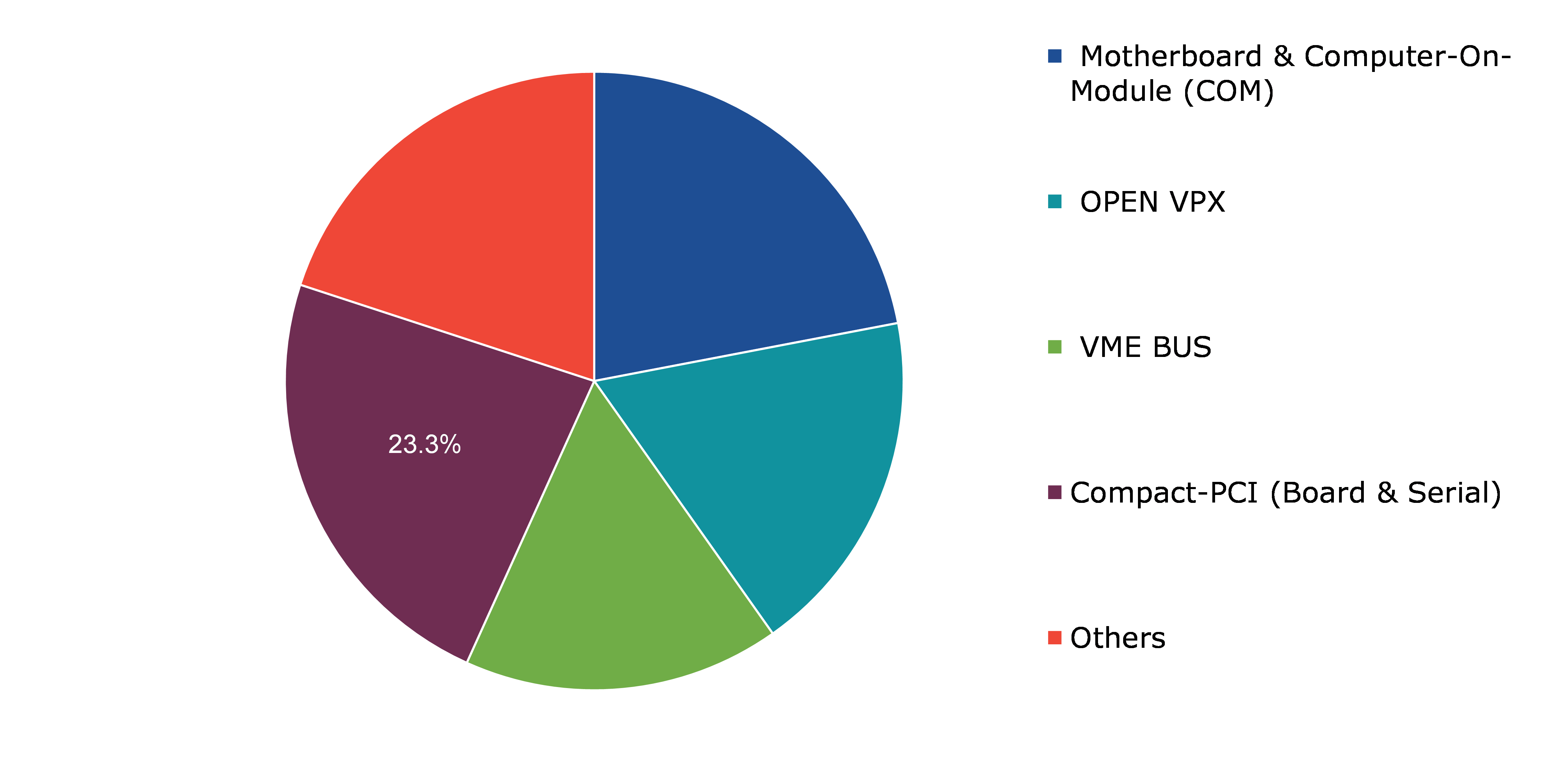

Global Military Embedded Systems Market, by Product Type

Based on product type, the market has been divided into motherboard & computer-on-module (COM), OPEN VPX, VME Bus, compact-PCI (Board & Serial), and others. Among these, the motherboard & computer-on-module sub-segment accounted for the highest market share in 2021.

Global Military Embedded Systems Market Size, by Feedstock, 2021

Source: Research Dive Analysis

The motherboard & computer-on-module sub-type is anticipated to have a dominant market share in 2021. An extremely small and tightly integrated embedded computer module called a “motherboard & computer-on-module” can be used with carrier boards that are compatible with it. Design concepts become more modular, economical, and time-to-market efficient when the carrier board and computer-on-module module designs are separated. For applications that need to increase CPU performance while maintaining the carrier board's input/output ports to reduce additional development time and expense, computer-on-module is the perfect answer. Because of their unique feature of secure knowledge, computer on modules are most effective for military use. For ruggedized military mobile systems, customers can construct their own application-specific carrier board using off-the-shelf computer modules, regardless of how critical the information is for the military.

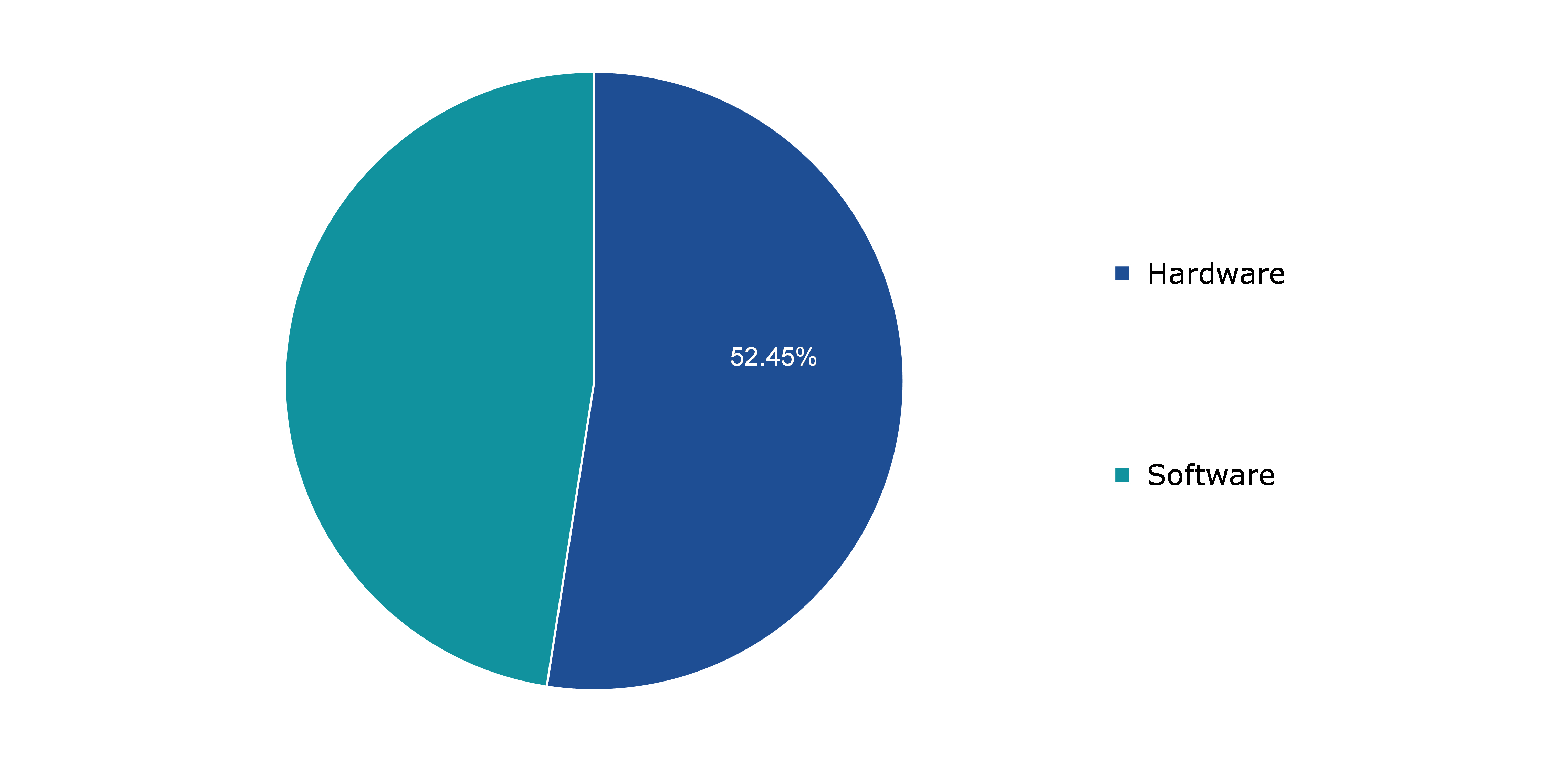

Global Military Embedded Systems Market, by Component

Based on component, the market has been divided into hardware and software. Among these, the hardware sub-segment accounted for the highest revenue share in 2021, and the software sub-segment shows the fastest growth during the forecasted time period.

Global Military Embedded Systems Market Share, by Component, 2021

Source: Research Dive Analysis

The hardware sub-segment is anticipated to have a dominant market share in 2021. Computer hardware" refers to any physical component of an analogue or digital computer. The term "hardware" separates the physical components of a computing system from "software," which is made up of written, machine-readable instructions or programs that specify what to do and when to execute physical components. The term “military hardware” describes devices created and produced specifically for use in the armed forces. Military computers hardware is designed to function in conditions that are far more difficult than those seen in regular industrial applications. For instance, desert heat and cold, a hostile battleground, and highly shock and vibration tactical combat vehicles. For instance, Crystal Group, a pioneer in the production of rugged, highly reliable computing hardware for military, defense, and industrial scenarios, has demonstrated its expertise in this area. The "Silver" profile highlights the company's secure computing, networking, and data storage solutions as being appropriate for Internet of Things (IoT) applications, drones, autonomous vehicles, and UAVs.

The software sub-type shows fastest market share in 2031. Software embedded systems are far smaller than conventional computers, which makes them more portable and appropriate for mass production. The use of synthetic instruments (SI) in electronic testing of military systems is a significant trend. Embedded systems software refers to specialized programming tools in embedded devices that facilitate the machines' operation. The software oversees systems and hardware. The primary objective of embedded systems software is to control the operation of a collection of hardware parts without compromising their intended purpose or efficiency.

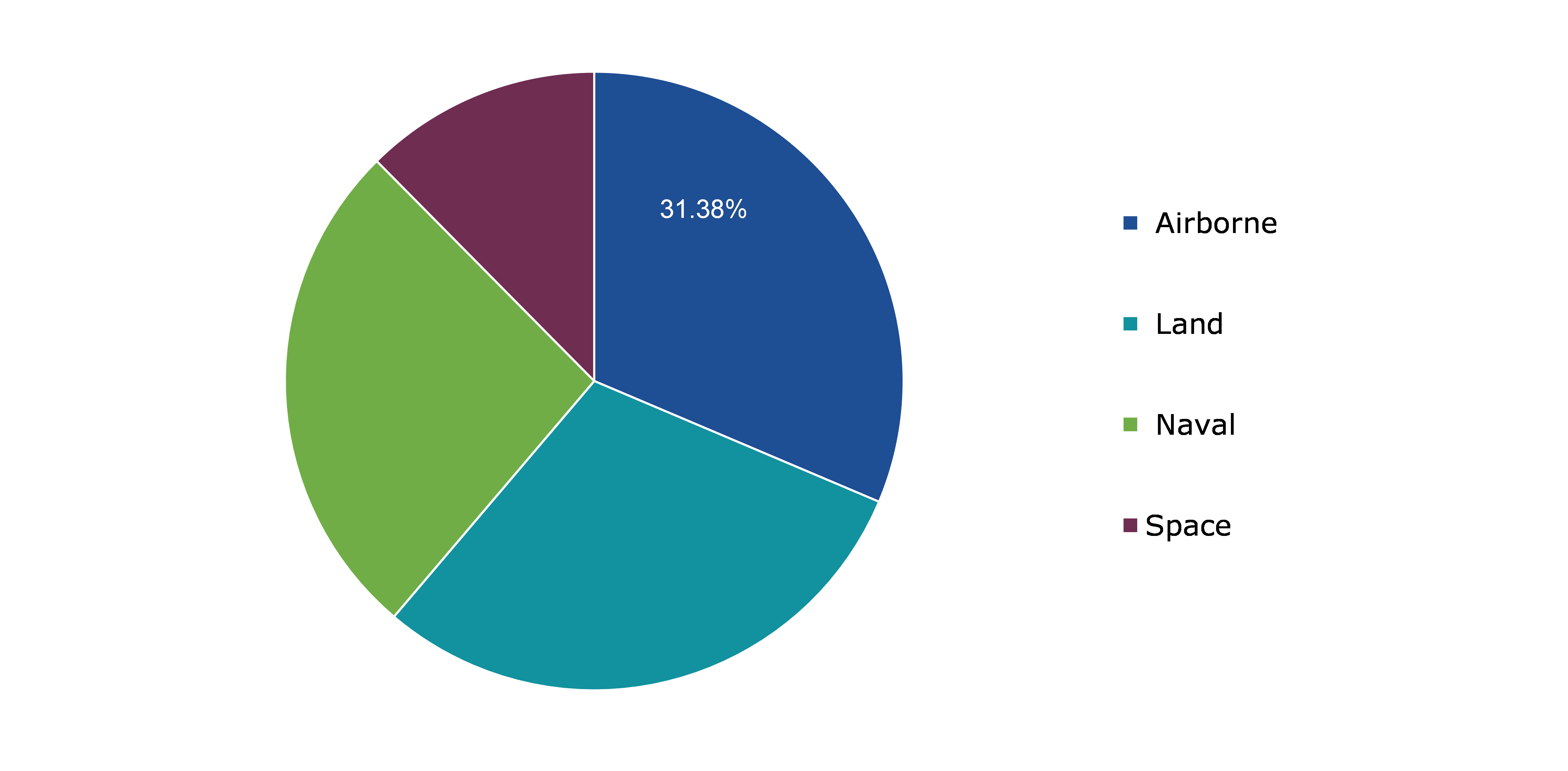

Global Military Embedded Systems Market, by Platform

Based on platform, the market has been divided into airborne, land, naval, and space. Among these, the land sub-segment accounted for the highest revenue share in 2021, and airborne sub-segment shows the fastest growth during the forecasted time period.

Global Military Embedded Systems Market Trends, by Platform, 2021

Source: Research Dive Analysis

The land sub-segment is anticipated to have a dominant market share in 2021. The development of sophisticated electronic systems and mission-critical embedded systems, together with the rising demand for surveillance operations brought on by regional instability, are all factors that have contributed to the expansion of this market. The military intends to increase the use of low-cost, flexible standard electronics in military ground vehicles by utilizing harsh environment embedded computing systems. Land-based platforms are equipped with a variety of instruments, including cameras that are deployed on the platforms, including digital and film cameras, light-detection and ranging (LIDAR) systems, visible and infrared and thermal infrared scanners, and radars systems.

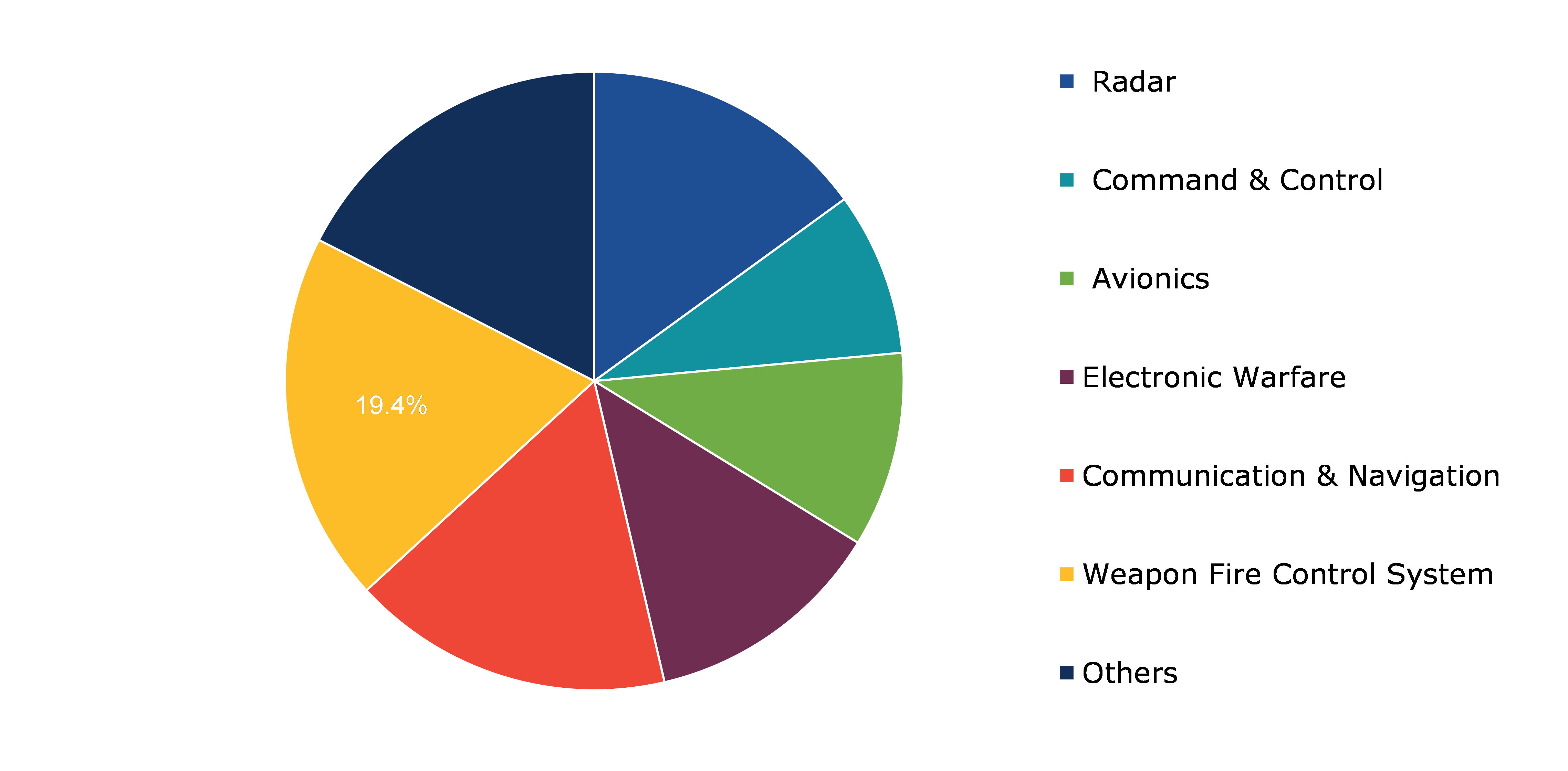

Global Military Embedded Systems Market, by Application

Based on application, the market has been divided into radar, command & control, avionics, electronic warfare, communication & navigation, weapon fire control system, and others. Among these, the land sub-segment accounted for the highest revenue share in 202, and the airborne sub-segment shows the fastest growth during the forecasted time period.

Global Military Embedded Systems Market Growth, by Application, 2021

Source: Research Dive Analysis

The weapon fire control system sub-segment is anticipated to have a dominant market share in 2021. The defense sector is undergoing significant changes as a result of the numerous technological developments made by industry players to meet the changing demands of the armed services. The market for automatic fire systems is expanding. The creation of consolidated fire control systems is one of the main trends that will take off in the military fire control systems industry in the upcoming years. Large firms are also focusing more and more of their efforts on developing weapons that are connected to fire control systems.

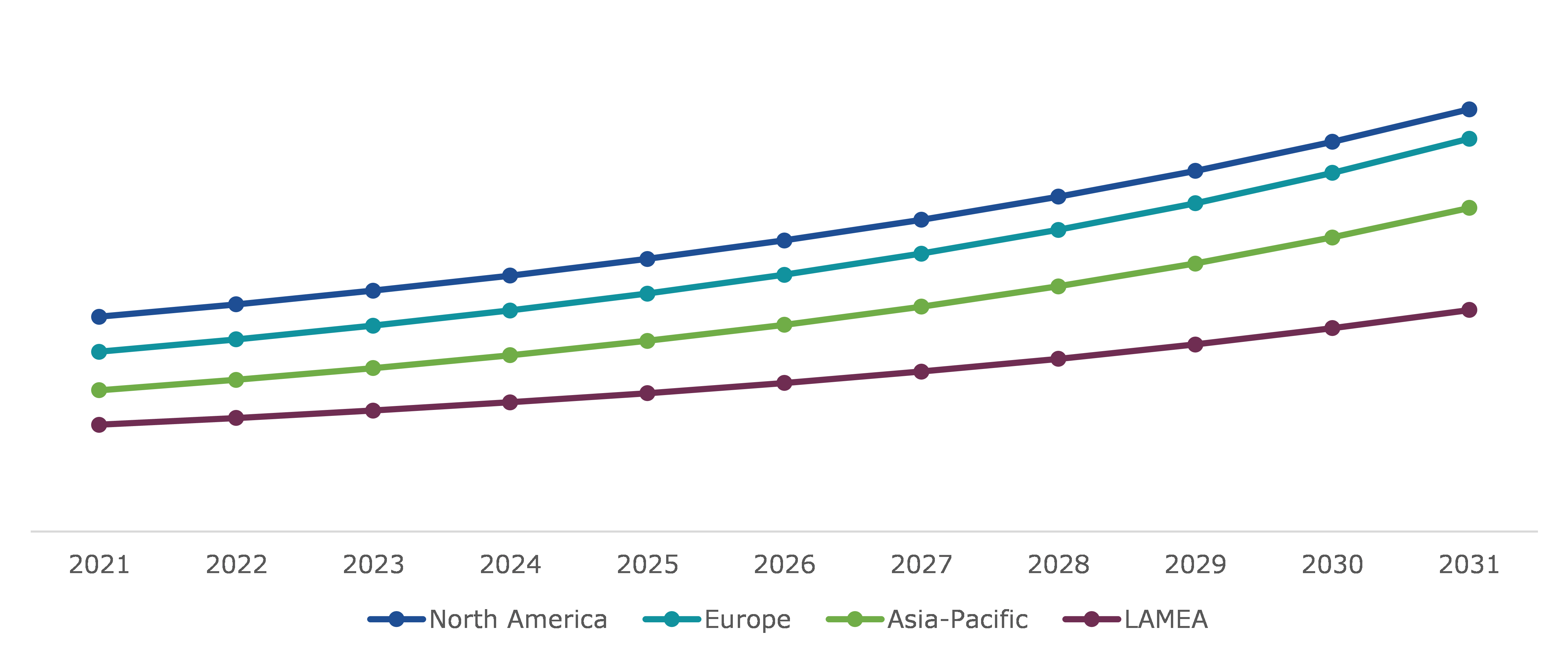

Global Military Embedded Systems Market, Regional Insights

The Military Embedded Systems market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Military Embedded Systems Market Size & Forecast, by Region, 2021-2031 (USD Million)

Source: Research Dive Analysis

The Market for Military Embedded Systems in North America to be the Most Dominant

The North American military embedded systems market had a dominating market share in 2021. Applications of cutting-edge technology are widely used in North America. As a country with advanced technology, the US has enormous investment opportunities in embedded system technology. Due to the region's progress in next-generation communication technologies and the United States' rapid advancement in military and aerospace, the North American military embedded system market is anticipated to dominate the global military embedded system market. In the past few years, modern electronic warfare systems have been widely deployed throughout the region. These factors are anticipated to boost the military embedded system market share in the North America region during the forecasted time period.

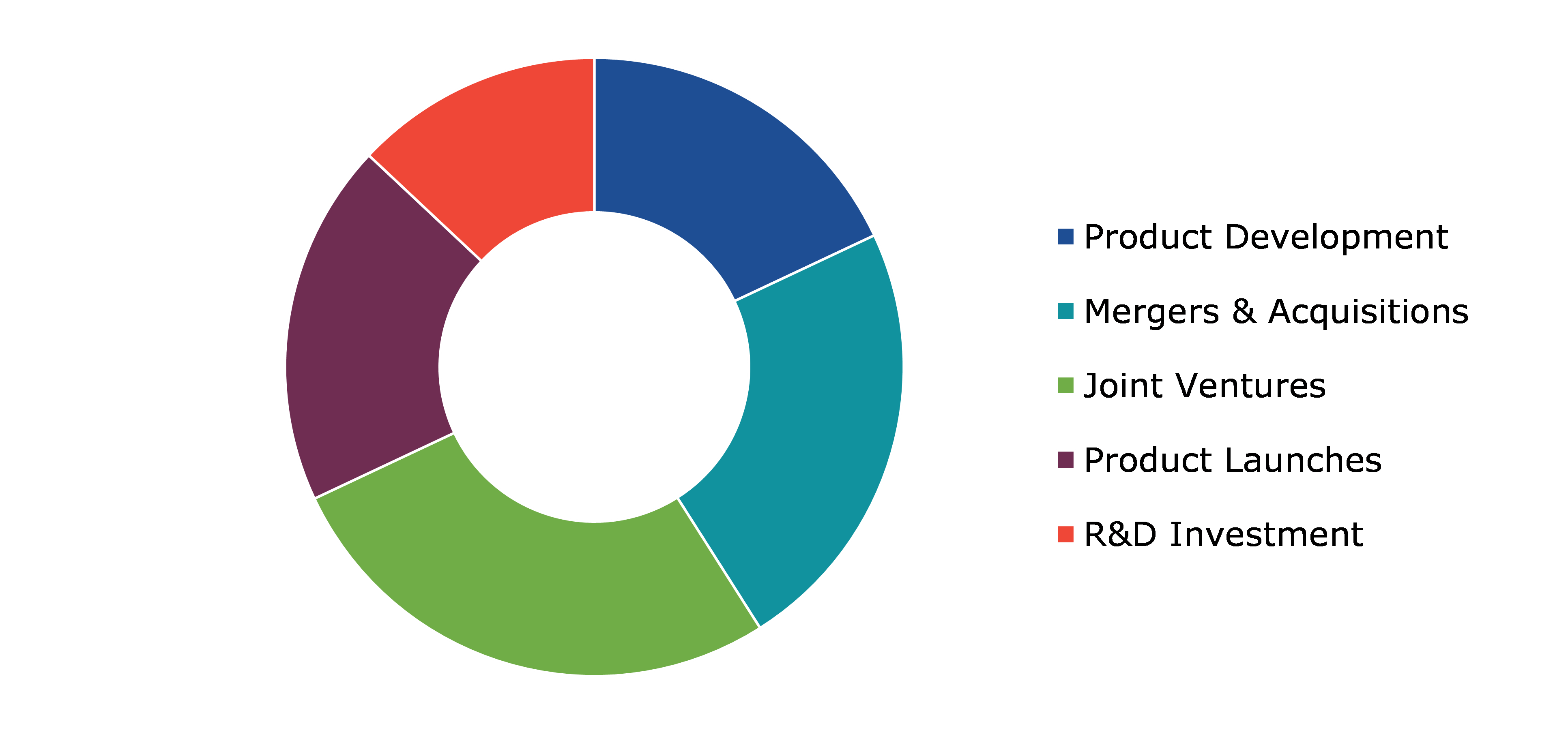

Competitive Scenario in the Global Military Embedded Systems Market

Investment and agreement are common strategies followed by major market players. For instance, in August 2022, the U.S. Navy and BAE Systems have agreed to a $42.6 million contract for the creation of seven Network Tactical Common Data Link systems. These systems will allow the Navy to simultaneously transmit and receive real-time intelligence, surveillance, and reconnaissance data from various sources and allow the exchange of command-and-control information through different data lines.

Source: Research Dive Analysis

Some of the leading Military Embedded Systems market players are Intel Corporation, Mercury Systems, Inc. Curtiss-Wright Corporation, Advantech Co., Ltd., BAE Systems, SMART Embedded Computing, SDK Embedded Systems Ltd., General Dynamics Corporation, Kontron (S&T), and Xilinx Inc.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Product Type |

|

| Segmentation by Component |

|

| Segmentation by Platform Type |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

Q1. What is the size of the global military embedded systems market?

A. The size of the global military embedded systems market was over $1,540 million in 2021 and is projected to reach $3,259.3 million by 2031.

Q2. Which are the major companies in the Military Embedded Systems market?

A. Intel Corporation, Mercury Systems, Inc., and Curtiss-Wright Corporation are some of the key players in the global military embedded systems market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific military embedded systems market?

A. Asia-Pacific military embedded systems market is anticipated to grow at 8.8% CAGR during the forecast period.

Q5. What are the strategies opted for by the leading players in this market?

A. Agreement and investment are the two key strategies opted for by the operating companies in this market.

Q6. Which companies are investing more in R&D practices?

A. Advantech Co., Ltd., BAE Systems, and SMART Embedded Computing are the companies investing more in R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global military embedded systems market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on military embedded systems market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Military embedded systems Market Analysis, by Product Type

5.1.Overview

5.2.Motherboard & Computer-On-Module (COM),

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region, 2022-2031

5.2.3.Market share analysis, by country, 2022-2031

5.3.OPEN VPX

5.3.1. Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region, 2022-2031

5.3.3.Market share analysis, by country, 2022-2031

5.4.VME BUS

5.4.1. Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region, 2022-2031

5.4.3.Market share analysis, by country, 2022-2031

5.5.Compact-PCI (Board & Serial)

5.5.1. Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region, 2022-2031

5.5.3.Market share analysis, by country, 2022-2031

5.6.Others

5.6.1. Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region, 2022-2031

5.6.3.Market share analysis, by country, 2022-2031

5.7.Research Dive Exclusive Insights

5.7.1.Market attractiveness

5.7.2.Competition heatmap

6.Military embedded systems Market Analysis, by Component Type

6.1.Hardware

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region, 2022-2031

6.1.3.Market share analysis, by country, 2022-2031

6.2.Software

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region, 2022-2031

6.2.3.Market share analysis, by country, 2022-2031

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Military embedded systems Market Analysis, by Platform Type

7.1.Overview

7.2.Airborne

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region, 2022-2031

7.2.3.Market share analysis, by country, 2022-2031

7.3.Land

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region, 2022-2031

7.3.3.Market share analysis, by country, 2022-2031

7.4.Naval

7.4.1.Definition, key trends, growth factors, and opportunities

7.4.2.Market size analysis, by region, 2022-2031

7.4.3.Market share analysis, by country, 2022-2031

7.5.Space

7.5.1.Definition, key trends, growth factors, and opportunities

7.5.2.Market size analysis, by region, 2022-2031

7.5.3.Market share analysis, by country, 2022-2031

7.6.Research Dive Exclusive Insights

7.6.1.Market attractiveness

7.6.2.Competition heatmap

8.Military embedded systems Market Analysis, by Application

8.1.Overview

8.2.Radar

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region, 2022-2031

8.2.3.Market share analysis, by country, 2022-2031

8.3.Command & Control

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region, 2022-2031

8.3.3.Market share analysis, by country, 2022-2031

8.4.Avionics

8.4.1.Definition, key trends, growth factors, and opportunities

8.4.2.Market size analysis, by region, 2022-2031

8.4.3.Market share analysis, by country, 2022-2031

8.5.Electronic Warfare

8.5.1.Definition, key trends, growth factors, and opportunities

8.5.2.Market size analysis, by region, 2022-2031

8.5.3.Market share analysis, by country, 2022-2031

8.6.Communication & Navigation

8.6.1.Definition, key trends, growth factors, and opportunities

8.6.2.Market size analysis, by region, 2022-2031

8.6.3.Market share analysis, by country, 2022-2031

8.7.Weapon Fire Control System

8.7.1.Definition, key trends, growth factors, and opportunities

8.7.2.Market size analysis, by region, 2022-2031

8.7.3.Market share analysis, by country, 2022-2031

8.8.Others

8.8.1.Definition, key trends, growth factors, and opportunities

8.8.2.Market size analysis, by region, 2022-2031

8.8.3.Market share analysis, by country, 2022-2031

8.9.Research Dive Exclusive Insights

8.9.1.Market attractiveness

8.9.2.Competition heatmap

9.Military embedded systems Market, by Region

9.1.North America

9.1.1.U.S.

9.1.1.1.Market size analysis, by Product Type, 2022-2031

9.1.1.2.Market size analysis, by Component Type, 2022-2031

9.1.1.3.Market size analysis, by Platform Type, 2022-2031

9.1.1.4.Market size and forecast, by Application Type, 2022-2031

9.1.2.Canada

9.1.2.1.Market size analysis, by Product Type, 2022-2031

9.1.2.2.Market size analysis, by Component Type, 2022-2031

9.1.2.3.Market size analysis, by Platform Type, 2022-2031

9.1.2.4.Market size and forecast, by Application Type, 2022-2031

9.1.3.Mexico

9.1.3.1.Market size analysis, by Product Type, 2022-2031

9.1.3.2.Market size analysis, by Component Type, 2022-2031

9.1.3.3.Market size analysis, by Platform Type, 2022-2031

9.1.3.4.Market size and forecast, by Application Type, 2022-2031

9.1.4.Research Dive Exclusive Insights

9.1.4.1.Market attractiveness

9.1.4.2.Competition heatmap

9.2.Europe

9.2.1.Germany

9.2.1.1.Market size analysis, by Product Type, 2022-2031

9.2.1.2.Market size analysis, by Component Type, 2022-2031

9.2.1.3.Market size analysis, by Platform Type, 2022-2031

9.2.1.4.Market size and forecast, by Application Type, 2022-2031

9.2.2.UK

9.2.2.1.Market size analysis, by Product Type, 2022-2031

9.2.2.2.Market size analysis, by Component Type, 2022-2031

9.2.2.3.Market size analysis, by Platform Type, 2022-2031

9.2.2.4.Market size and forecast, by Application Type, 2022-2031

9.2.3.France

9.2.3.1.Market size analysis, by Product Type, 2022-2031

9.2.3.2.Market size analysis, by Component Type, 2022-2031

9.2.3.3.Market size analysis, by Platform Type, 2022-2031

9.2.3.4.Market size and forecast, by Application Type, 2022-2031

9.2.4.Spain

9.2.4.1.Market size analysis, by Product Type, 2022-2031

9.2.4.2.Market size analysis, by Component Type, 2022-2031

9.2.4.3.Market size analysis, by Platform Type, 2022-2031

9.2.4.4.Market size and forecast, by Application Type, 2022-2031

9.2.5.Italy

9.2.5.1.Market size analysis, by Product Type, 2022-2031

9.2.5.2.Market size analysis, by Component Type, 2022-2031

9.2.5.3.Market size analysis, by Platform Type, 2022-2031

9.2.5.4.Market size and forecast, by Application Type, 2022-2031

9.2.6.Rest of Europe

9.2.6.1.Market size analysis, by Product Type, 2022-2031

9.2.6.2.Market size analysis, by Component Type, 2022-2031

9.2.6.3.Market size analysis, by Platform Type, 2022-2031

9.2.6.4.Market size and forecast, by Application Type, 2022-2031

9.2.7.Research Dive Exclusive Insights

9.2.7.1.Market attractiveness

9.2.7.2.Competition heatmap

9.3.Asia Pacific

9.3.1.China

9.3.1.1.Market size analysis, by Product Type, 2022-2031

9.3.1.2.Market size analysis, by Component Type, 2022-2031

9.3.1.3.Market size analysis, by Platform Type, 2022-2031

9.3.1.4.Market size and forecast, by Application Type, 2022-2031

9.3.2.Japan

9.3.2.1.Market size analysis, by Product Type, 2022-2031

9.3.2.2.Market size analysis, by Component Type, 2022-2031

9.3.2.3.Market size analysis, by Platform Type, 2022-2031

9.3.2.4.Market size and forecast, by Application Type, 2022-2031

9.3.3.India

9.3.3.1.Market size analysis, by Product Type, 2022-2031

9.3.3.2.Market size analysis, by Component Type, 2022-2031

9.3.3.3.Market size analysis, by Platform Type, 2022-2031

9.3.3.4.Market size and forecast, by Application Type, 2022-2031

9.3.4.Australia

9.3.4.1.Market size analysis, by Product Type, 2022-2031

9.3.4.2.Market size analysis, by Component Type, 2022-2031

9.3.4.3.Market size analysis, by Platform Type, 2022-2031

9.3.4.4.Market size and forecast, by Application Type, 2022-2031

9.3.5.South Korea

9.3.5.1.Market size analysis, by Product Type, 2022-2031

9.3.5.2.Market size analysis, by Component Type, 2022-2031

9.3.5.3.Market size analysis, by Platform Type, 2022-2031

9.3.5.4.Market size and forecast, by Application Type, 2022-2031

9.3.6.Rest of Asia Pacific

9.3.6.1.Market size analysis, by Product Type, 2022-2031

9.3.6.2.Market size analysis, by Component Type, 2022-2031

9.3.6.3.Market size analysis, by Platform Type, 2022-2031

9.3.6.4.Market size and forecast, by Application Type, 2022-2031

9.3.7.Research Dive Exclusive Insights

9.3.7.1.Market attractiveness

9.3.7.2.Competition heatmap

9.4.LAMEA

9.4.1.Brazil

9.4.1.1.Market size analysis, by Product Type, 2022-2031

9.4.1.2.Market size analysis, by Component Type, 2022-2031

9.4.1.3.Market size analysis, by Platform Type, 2022-2031

9.4.1.4.Market size and forecast, by Application Type, 2022-2031

9.4.2.Saudi Arabia

9.4.2.1.Market size analysis, by Product Type, 2022-2031

9.4.2.2.Market size analysis, by Component Type, 2022-2031

9.4.2.3.Market size analysis, by Platform Type, 2022-2031

9.4.2.4.Market size and forecast, by Application Type, 2022-2031

9.4.3.UAE

9.4.3.1.Market size analysis, by Product Type, 2022-2031

9.4.3.2.Market size analysis, by Component Type, 2022-2031

9.4.3.3.Market size analysis, by Platform Type, 2022-2031

9.4.3.4.Market size and forecast, by Application Type, 2022-2031

9.4.4.South Africa

9.4.4.1.Market size analysis, by Product Type, 2022-2031

9.4.4.2.Market size analysis, by Component Type, 2022-2031

9.4.4.3.Market size analysis, by Platform Type, 2022-2031

9.4.4.4.Market size and forecast, by Application Type, 2022-2031

9.4.5.Rest of LAMEA

9.4.5.1.Market size analysis, by Product Type, 2022-2031

9.4.5.2.Market size analysis, by Component Type, 2022-2031

9.4.5.3.Market size analysis, by Platform Type, 2022-2031

9.4.5.4.Market size and forecast, by Application Type, 2022-2031

9.4.6.Research Dive Exclusive Insights

9.4.6.1.Market attractiveness

9.4.6.2.Competition heatmap

10.Competitive Landscape

10.1.Top winning strategies, 2021

10.1.1.By strategy

10.1.2.By year

10.2.Strategic overview

10.3.Market share analysis, 2021

11.Company Profiles

11.1.Intel Corporation

11.1.1.Overview

11.1.2.Business segments

11.1.3.Product portfolio

11.1.4.Financial performance

11.1.5.Recent developments

11.1.6.SWOT analysis

11.1.7.RESEARCH DIVE ANALYST VIEW

11.2.Mercury Systems, Inc

11.2.1.Overview

11.2.2.Business segments

11.2.3.Product portfolio

11.2.4.Financial performance

11.2.5.Recent developments

11.2.6.SWOT analysis

11.2.7.RESEARCH DIVE ANALYST VIEW

11.3.Curtiss-Wright Corporation

11.3.1.Overview

11.3.2.Business segments

11.3.3.Product portfolio

11.3.4.Financial performance

11.3.5.Recent developments

11.3.6.SWOT analysis

11.3.7.RESEARCH DIVE ANALYST VIEW

11.4.Advantech Co., Ltd.

11.4.1.Overview

11.4.2.Business segments

11.4.3.Product portfolio

11.4.4.Financial performance

11.4.5.Recent developments

11.4.6.SWOT analysis

11.4.7.RESEARCH DIVE ANALYST VIEW

11.5.BAE Systems

11.5.1.Overview

11.5.2.Business segments

11.5.3.Product portfolio

11.5.4.Financial performance

11.5.5.Recent developments

11.5.6.SWOT analysis

11.5.7.RESEARCH DIVE ANALYST VIEW

11.6.SMART Embedded Computing

11.6.1.Overview

11.6.2.Business segments

11.6.3.Product portfolio

11.6.4.Financial performance

11.6.5.Recent developments

11.6.6.SWOT analysis

11.6.7.RESEARCH DIVE ANALYST VIEW

11.7.BAE Systems

11.7.1.Overview

11.7.2.Business segments

11.7.3.Product portfolio

11.7.4.Financial performance

11.7.5.Recent developments

11.7.6.SWOT analysis

11.7.7.RESEARCH DIVE ANALYST VIEW

11.8.General Dynamics Corporation

11.8.1.Overview

11.8.2.Business segments

11.8.3.Product portfolio

11.8.4.Financial performance

11.8.5.Recent developments

11.8.6.SWOT analysis

11.8.7.RESEARCH DIVE ANALYST VIEW

11.9.Kontron (S&T)

11.9.1.Overview

11.9.2.Business segments

11.9.3.Product portfolio

11.9.4.Financial performance

11.9.5.Recent developments

11.9.6.SWOT analysis

11.9.7.RESEARCH DIVE ANALYST VIEW

11.10.Xilinx Inc

11.10.1.Overview

11.10.2.Business segments

11.10.3.Product portfolio

11.10.4.Financial performance

11.10.5.Recent developments

11.10.6.SWOT analysis

11.10.7.RESEARCH DIVE ANALYST VIEW

12.Appendix

12.1.Parent & peer market analysis

12.2.Premium insights from industry experts

12.3.Related reports

The globe is moving toward a more comprehensive use of digital technology in modern society in order to digitally empower individuals and accelerate technological transfer. Systems used in the military must be extremely secure, dependable, and tough. In the military and defense industries, having access to cutting-edge technology is essential. Most of today's latest technology relies on computing and embedded systems to support the unique requirements of the military. Embedded systems used for military purposes differ from those used for general-purpose purposes in civilian applications.

An embedded system may run separately or in combination with another, larger system. It is referred to as a military embedded system when employed in defense and military applications. An embedded system consists of several components, like rugged systems, single-board computers, multifunction I/O boards, and general-purpose graphics processing units. It is a device that uses a microprocessor or microcontroller to carry out real-time analysis and other specialized functions. Military embedded systems are used in numerous applications like reconnaissance and surveillance, intelligence, communication equipment, computers, control and command systems, data storage devices, and data acquisition equipment. The global military embedded systems market is expanding at a rapid pace due to the popularity of standard electronics like smart wearables and smartphones, as well as lightweight armoured vehicles.

Latest Market Insights in Military Embedded Systems

The military embedded systems market is experiencing growth due to the extensive use of wireless and multicore technology, the growing emphasis on cloud computing, and the development of systems for modern warfare. As per a report by Research Dive, the global military embedded systems market is expected to surpass a revenue of $3,259.3 million in the 2022–2031 timeframe. The North American military embedded systems market is expected to grow at a rapid rate in the coming years. This is because the region has a gigantic demand for military embedded systems owing to advancements in next-generation communication technologies in the region.

How are Market Players Responding to the Rising Demand for Military Embedded Systems?

Market players are greatly investing in pioneering research and inventions to cater for the increasing technological progress in network convergence. Some of the foremost players in the military embedded systems market are Mercury Systems, Inc., Curtiss-Wright Corporation, Intel Corporation, SMART Embedded Computing, BAE Systems, Advantech Co., Ltd., General Dynamics Corporation, Xilinx Inc., SDK Embedded Systems Ltd., Kontron (S&T), and others. These players are focused on planning and devising tactics such as mergers and acquisitions, collaborations, novel advances, and partnerships to reach a notable position in the global market. For instance:

- In March 2018, Chassis Plans, an American military and industrial computer systems manufacturer, launched 7-inch tablet for industrial and military applications.

- In September 2022, Curtiss-Wrights Defence Solutions, a leading provider of successful MOSA (modular open systems approach)-based solutions, announced that a leading defence system integrator has once again chosen it to supply its embedded security IP module technology.

- In January 2023, GET Engineering, a foremost high technology engineering company offering tactical data solutions to government and industrial clients, launched the Compact Embedded System (CES) for military and industrial applications.

COVID-19 Impact on the Global Military Embedded Systems Market

The unpredicted rise of the coronavirus pandemic in 2020 had adversely impacted the global military embedded systems market. During the pandemic period, the closure of manufacturing plants, the disruption of the supply chain, and the slowdown of economies across various countries have resulted in a reduction in demand for military embedded systems. Additionally, because of the government's limitations and lockdown measures, migrants and factory workers were unable to get to their workplaces, which had an impact on the supply and production of embedded systems. Even though these systems' manufacturing is crucial for military objectives, supply chain issues have temporarily halted production. A nation's level of COVID-19 exposure, the effectiveness of its production procedures, and import-export laws are only a few of the variables that impact when manufacturing and demand continue. The market expansion for military embedded systems during the pandemic was significantly impacted by all of these reasons.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com