Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

MA20116194 |

Pages: 240 |

May 2022 |

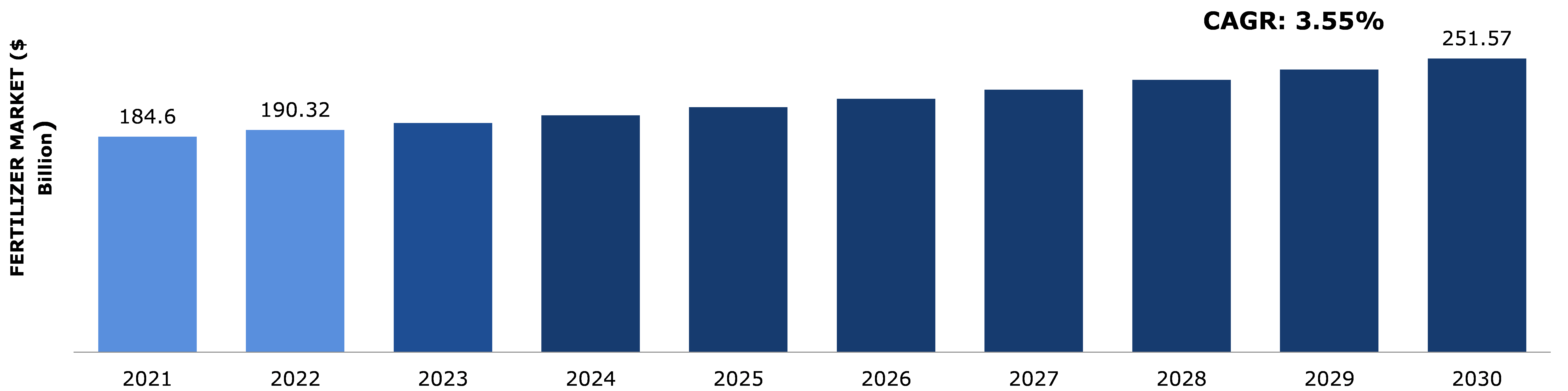

Fertilizer market is gaining huge popularity as it plays a crucial role in improving the crop yield by providing essential nutrients to the crops such as nitrogen, phosphate, potassium, and others that improves the soil fertility. The demand for fertilizers, especially in agriculture sector has increased rapidly as growing population has led to an increase in the demand for food. In addition, lack of nutrients in soil due to use of pesticides and other harmful chemicals has led to decline in agricultural productivity. This is expected to increase the demand for fertilizers. Moreover, fertilizer sector is fragmented with various fertilizer companies operating around the world. Because fertilizers are such a crucial instrument for increasing agricultural output, industry participants are forming strategic alliances and joint ventures to expand their geographic footprint and product portfolio. For example, in 2019, the Haifa Group announced that they have expanded their Controlled Release Fertilizer (CRF) factory in France for producing 8,000 MTPA. Using this technology, the company was able to increase its manufacturing capacity by up to 24,000 MTPA. In 2018, Yara International ASA paid USD 255 billion for Brazil's Vale Cubatao Fertilizantes Complex. As a result of this strategy, the company was able to strengthen its nitrogen production assets and market position in the Brazilian fertilizer industry.

However, the lack of awareness regarding optimum use of fertilizers is anticipated to restrain the market growth. For instance, optimum use of chemical fertilizers is a cost-effective way to boost the crop yield. However, overuse of chemical fertilizers degrades the soil as it disrupts the acidity of soil which is detrimental to the crop and surrounding.

According to regional analysis, the Asia-Pacific fertilizer market accounted for $99.13 billion in 2021 and is predicted to grow with a CAGR of 3.76%, in the projected timeframe owing to rising fertilizer demand across the region. Several countries in the region are looking to export agricultural products around the world in order to grow their economies.

Fertilizers derived from organic or inorganic origin and are applied to the soil or plant tissue to increase the crop productivity, by supplying nutrients essential for the plant growth. For instance, nitrogen-based fertilizers contain nitrogen which is the main constituent of chlorophyll that facilitates photosynthesis process in plants. Phosphorous fertilizers are beneficial for the roots of plants as phosphorous is present in protoplasm of cell that promotes cell growth and proliferation. In addition, organic fertilizers are natural fertilizers obtained from agricultural waste, industrial waste, municipal sludge, or livestock manure. These fertilizers promote reproduction of microorganisms, enhance the physical & chemical properties of soil, and enhance the water retention capacity of the soil.

Moreover. fertilizers are chemical compounds that are applied to plant tissues or soil to provide one or more nutrients required for plant growth. Higher crop yields are encouraged while soil nutrient availability is maintained and increased. The usage of organic fertilizers has risen, allowing farmers to utilize fertilizers more safely and efficiently while reducing the risk of toxic fertilizer exposure.

The global crisis caused by COVID-19 pandemic has negatively affected most of the industries across various countries. The global fertilizer industry also experienced a negative impact due to import-export restrictions which resulted in delays and disruptions at country borders. Restrictions on movement of people and goods brought many challenges for agri-food supply chain. For instance, as stated on June 26, 2020, in Farm Progress, the trusted agriculture news source, China is the largest fertilizer consumer in the world and lockdown in China has greatly impacted the fertilizer production due to shortage of labor. Travel restrictions led to piling up of fertilizers. Similarly, in Germany, the closure of restaurants, cafes, and bars which consume large quantity of French fries witnessed decline in the demand for potatoes by 60%. Hubei, the province of China, is the leading phosphoric acid and phosphate. Due to nation-wide lockdown imposed in China, being the epicenter of disease, the transport of phosphoric acid and phosphate to other provinces and countries was disrupted. Furthermore, as stated by the World Bank Group, the international financial institution, on June 25, 2020, the fertilizer prices declined by 8.5% in May 2020. For instance, the prices of urea fell drastically due to low seasonal demand, lower feedstock costs, closed borders, quarantines, and lockdowns.

Various government initiatives and subsidies to support fertilizer demand & supply and to ensure seamless availability of raw materials are helping the society to recover from the chaotic situation. For instance, as stated by Fertilizers Europe, which represents majority of fertilizer producers in Europe, on March 16, 2020, Jacob Hansen, Director General, Fertilizers Europe, sent letter to European Union commissioner for health, Mrs. Stella Kyriakides, to support the fact that fertilizers play an important role in the food chain and it should be regarded as essential commodity, which will ensure continuation in transportation and distribution of fertilizers. In addition, as stated on April 16, 2020, in the Economic Times, popular news platform, the Indian government is closely monitoring the production and distribution of fertilizers amid the COVID-19 pandemic to meet the fertilizer demand of the farmers, and to achieve growth in fertilizer sector in the long run. The real-time monitoring is done by the respective departments of fertilizers to ensure seamless production and supply chain.

The rising population especially in developing countries such as India is anticipated to increase the demand for fertilizers. As fertilizers play an important role in enhancing the crop productivity by improving the soil fertility, they support the growth of crops. The growing population has led to an increase in the demand for food. Although, rise in awareness campaigns to educate the farmers regarding benefits of fertilizers such as promoting the uses of fertilizers via television advertisements and workshops is estimated to drive the fertilizer demand during 2022-2030. Moreover, now-a-days, liquid fertilizer administration that is more effective and efficient guarantees that plants and crops get the nutrients they need at the correct time and in the right place, with minimal waste. As a result of the development of novel urease inhibitors and low-cost polymer coating technologies, highly efficient fertilizers are rapidly developing in the agriculture business in numerous fields such as cereals and industrial crops.

Furthermore, as stated on September 24, 2020, in the World Fertilizer, international magazine, agriculture plays an important role in economic development of India, and more than 50% of its population is dependent on agriculture. Also, India ranks third in the world for food grain production after China and the U.S. Hence, increase in the demand for food production across the world is estimated to drive the demand for fertilizers market. As fertilizers are food for plants, without the use of fertilizers the crop yield and production would decrease significantly. All these aspects are estimated to drive the demand for fertilizer market during 2022-2030.

To know more about global fertilizer market trends, get in touch with our analysts here.

The use of fertilizers should be optimum and must be regulated as excessive use of fertilizers leads to pollution. For instance, nitrogen-based fertilizers promote the growth of plants. However, excess use of nitrogen-based fertilizers is dangerous as it has toxic effects on animals, humans, plants, and water bodies. Endogenous nitrozation has been linked to high-nitrate diets, which could lead to thyroid disease, several types of human malignancies, neural tube abnormalities, and diabetes. In addition, it contributes to the climate change and emits harmful greenhouse gases such as nitrous oxide along with increasing unpredictability and a strong policy focus on the environment by government, which is estimated to hamper the fertilizer market growth during the forecast period.

Organic fertilizers are gaining huge popularity as it improves soil nutrients, water retention capability, and soil structure. To improve agricultural productivity, organic fertilizers are made from natural plant leftovers & trash, animal manures & excreta, microorganisms, and botanical extracts. Organic fertilizers disintegrate quickly and have no detrimental impact on surface or groundwater, making them safer for humans, animals, birds, and anything else that comes into contact with them. These fertilizers have a long shelf life and improve soil structure while enhancing water and nutrient retention capacity. They are chosen for producing residue-free agricultural yields since they are slow-releasing non-toxic fertilizers that do not leave any residues in the food. Moreover, synthetic or inorganic chemicals contain chemical molecules such as ammonium nitrate, potassium sulphate, and others that are disruptive to the soil. However, organic fertilizers are rich in organic matters such as manure, crushed shells, pulverize fish, and others that helps microbes to thrive via natural biological process. As organic fertilizers nurture the soil with organic matter, they reduce the need for pesticides. Organic fertilizers also improve the crop resistance to erosion.

Furthermore, various government schemes such as financial aids to promote the use of organic fertilizers is estimated to generate huge growth opportunities. For instance, in 2015, Indian government had launched Paramparagat Krishi Vikas Yojana (PKVY) to promote the use of organic fertilizers and organic farming. Under this scheme, a financial assistance of Rs. 50,000 per hectare for 3 years is given to the farmers out of which, Rs. 31,000 is given as incentives. These factors are estimated to generate huge opportunities in the global fertilizers market during 2022-2030.

To know more about global fertilizer market opportunities, get in touch with our analysts here.

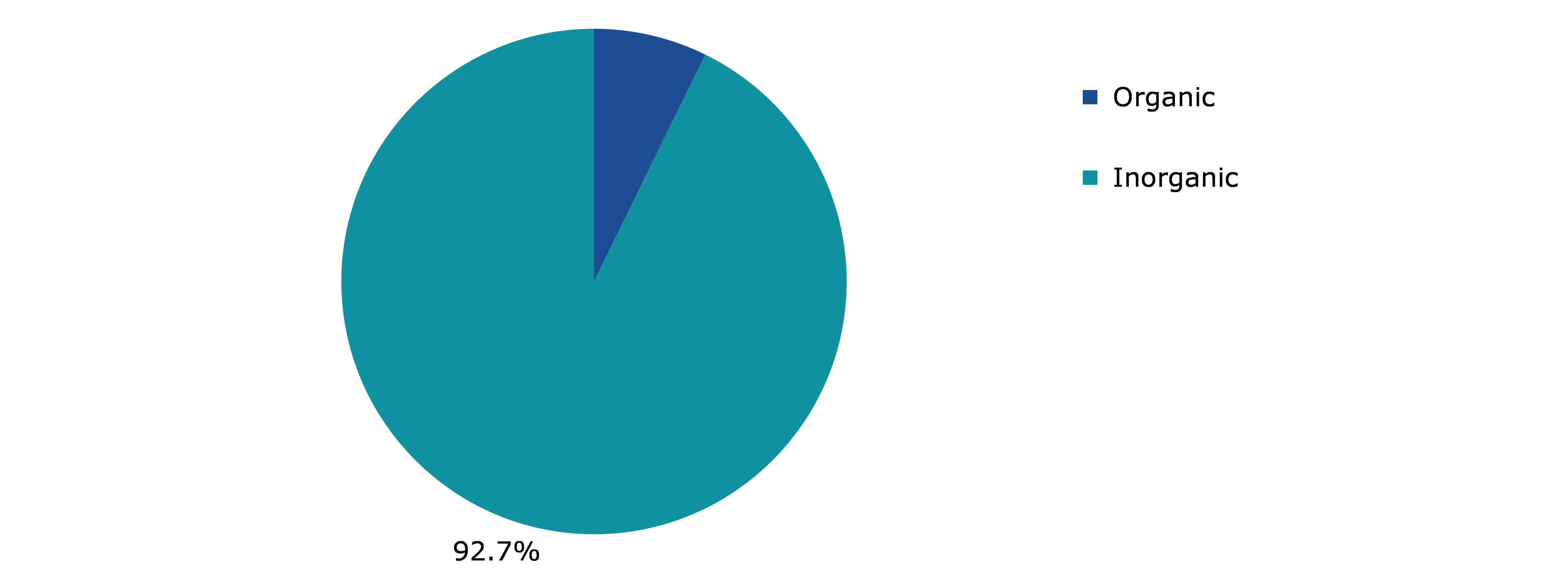

Based on type, the market has been divided into organic and inorganic. Among these, the inorganic sub-segment accounted for the highest revenue share in 2021 and organic sub-segment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

In 2021, the global inorganic fertilizer market had dominant market share and is expected to generate a revenue of $229.92 billion by 2030, growing from $171.19 billion in 2021. Inorganic fertilizers provide quick infusion of nutrients, allowing to feed plants according to convenience. They are completely synthetic and dosed precisely. Their nutrient ratios are clearly indicated on the bag, and one of the key advantages of inorganic fertilizers is fast acting. For instance, inorganic fertilizers include nutrient-rich in salts that dissolve quickly and are immediately made available to the plants for their nourishment. In addition, the inorganic fertilizers have precise content of essential nutrients such as nitrogen, potassium, and phosphorus to meet specific plant needs. Also, these fertilizers are easy to use as they are available in different formulations such as dry granules, liquid concentrates, and water-soluble powders. These fertilizers are produced in bulk due to which they are less costly and balance the soil nutrients for higher yield and better quality of crops. All these factors are estimated to drive the demand for inorganic fertilizers during the forecast period

Based on form, the market has been divided into dry and liquid. Among these, the dry sub-segment accounted for the highest revenue share in 2021, and liquid sub-segment is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The dry fertilizer sub-segment is anticipated to dominate the market during the forecast period and generate a revenue of $202.42 billion by 2030, growing from $151.86 billion in 2021, with a CAGR of 3.29%. Dry fertilizers are widely applied fertilizers. These fertilizers are most suitable for slow-release formulations as they are absorbed at slower rate by the plants, and they must be broken down first. These fertilizers are cheaper and easier to store as they do not “settle out” over time or in cold weather. Moreover, dry fertilizers, often known as granular fertilizers, are nutrients that are dried. Granular fertilizers vary in size and consistency based on the brand and the source of the product. These fertilizers’ physical consistency ranges from huge grains the size of an orange seed to a fine powdered form.

Moreover, dry fertilizers have a longer shelf life. Most dry fertilizers will last an eternity if stored away from moisture and direct sunlight. The rise in demand for dry fertilizers by consumers has generated significant demand for fertilizers.

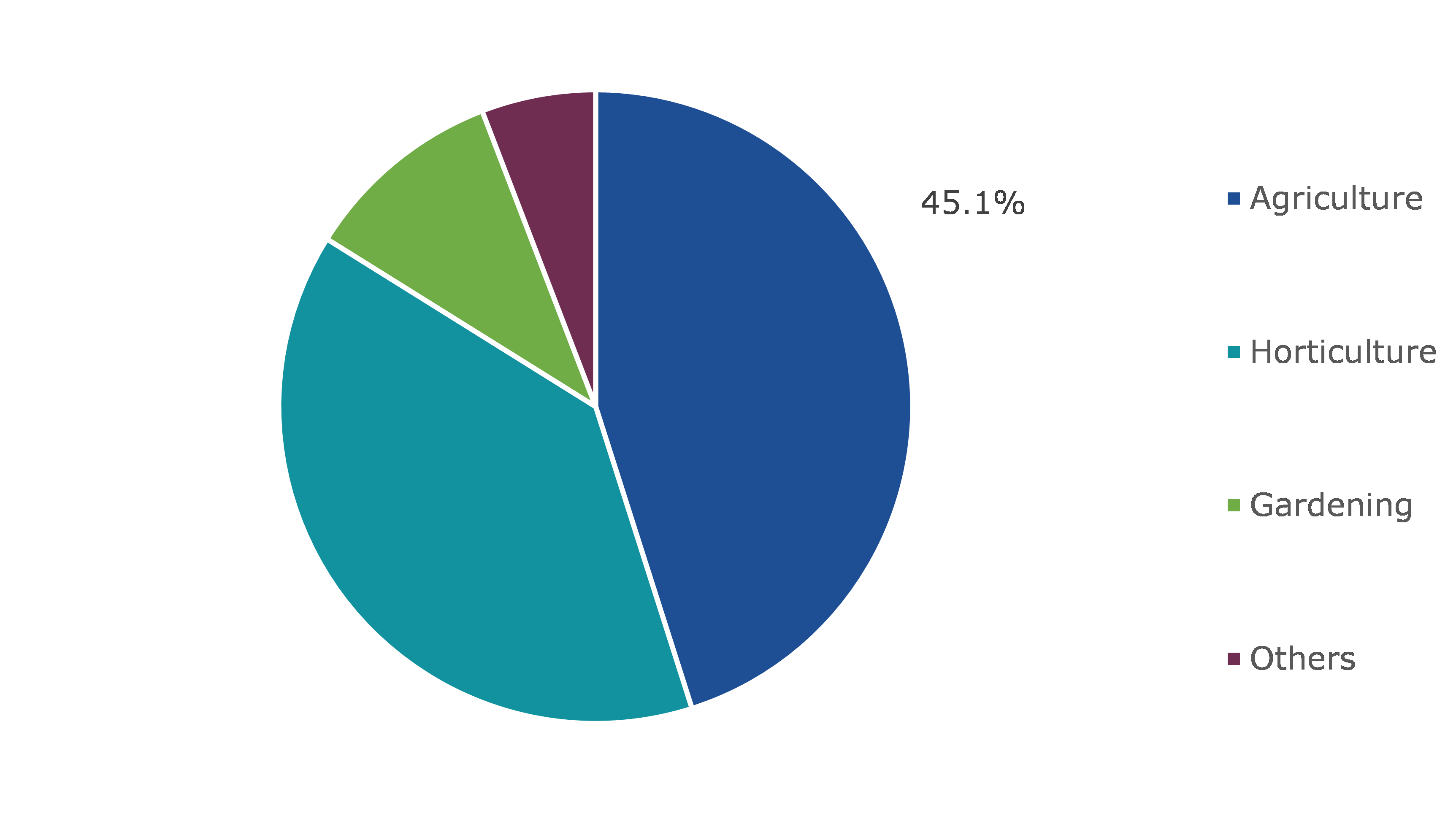

Based on application, the market has been divided into agriculture, horticulture, gardening, and others. Among these, agriculture sub-segment accounted for the highest market share in 2021.

Source: Research Dive Analysis

The agriculture sub-segment is anticipated to have a dominant market share and generate a revenue of $110.02 billion by 2030, growing from $83.23 billion in 2021. The demand for fertilizers in the agriculture sector has gained huge popularity owing to rising global population, globalization, and development of smart cities, which has led to decline in the availability of arable land and increase in the demand for food. To maintain the level of nutrients in the soil, fulfill the nutritional requirements of crops, and boost agricultural productivity, fertilizers are important. As stated on October 30, 2019, by Future Farming, the brand focusing on smart farming, the world’s population is estimated to reach 10 billion mark by 2050. Hence, it is crucial to boost the agricultural productivity to meet the food requirements of the growing population. Hence, the use of fertilizers in agricultural sector is vital to balance nutrients present in the soil and to produce quality yield with high productivity rate.

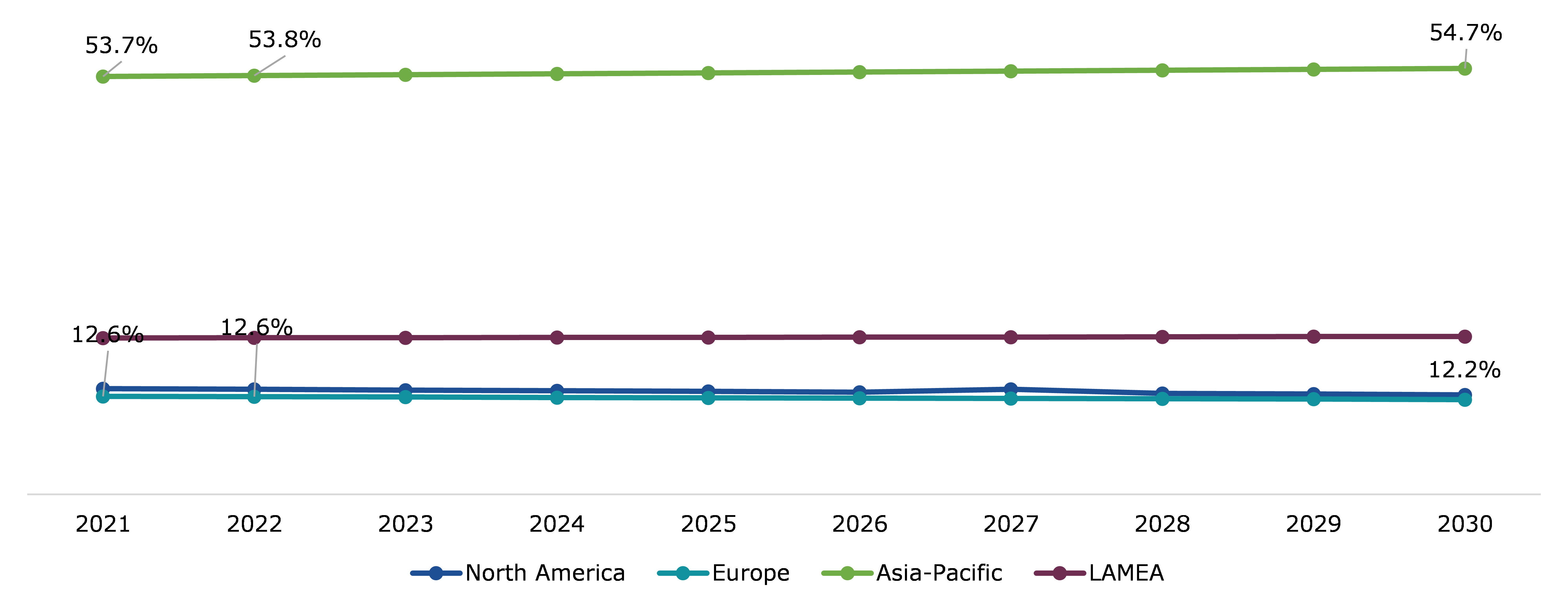

The fertilizer market was inspected across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The Asia-Pacific fertilizer market accounted $99.13 billion in 2021 and is projected to grow with a CAGR of 3.76%. This growth is majorly attributed to the presence of largest fertilizer consumers in this region. For instance, as stated on December 12, 2018, in the World Fertilizer, the popular platform for fertilizer news, China is the largest consumer of urea, and it accounts for one-third of total urea consumption in the world. More than 60% of urea is consumed in China which is applied as a fertilizer for the growth of cereals and oilseeds such as rapeseed, corn, soybean, and others. In addition, India ranks third in the consumption of ammonia after China and the U.S. 99% of urea in India is used as a fertilizer for growing crops. Indian farmers largely prefer urea fertilizer for growing crops as it is cheaper and subsidized compared to potassium and phosphorous fertilizers. In addition, Indonesia ranks third in the consumption of nitrogen fertilizer after China and India, in the Asia-Pacific region. Some other top fertilizer consuming countries in this region are Hong Kong SAR, Singapore, Malaysia, New Zealand, Vietnam, South Korea, and others. All these aspects are anticipated to drive the fertilizer demand in the Asia-Pacific region during the forecast period.

Source: Research Dive Analysis

Some of the leading fertilizer market players are Yara International, Nutrien Ltd., The Mosaic Company, Haifa Group, Syngenta AG, ICL Group Ltd., EuroChem Group, OCP Group S.A., K+S Aktiengesellschaft, and Uralkali.

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2030 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Form |

|

| Segmentation by Application |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Fertilizer market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Fertilizer market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Fertilizer Market Analysis, by Type

5.1.Organic

5.1.1.Market size and forecast, by region, 2022-2030

5.1.2.Comparative market share analysis, 2022 & 2030

5.2.Inorganic

5.2.1.Market size and forecast, by region, 2022-2030

5.2.2.Comparative market share analysis, 2022 & 2030

5.3.Research Dive Exclusive Insights

5.3.1.Market attractiveness

5.3.2.Competition heatmap

6.5.Fertilizer Market, by Form

6.1.Solid

6.1.1.Market size and forecast, by region, 2022-2030

6.1.2.Comparative market share analysis, 2022 & 2030

6.2.Liquid

6.2.1.Market size and forecast, by region, 2022-2030

6.2.2.Comparative market share analysis, 2022 & 2030

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.5.Fertilizer Market, by Application

7.1.Agriculture

7.1.1.Market size and forecast, by region, 2022-2030

7.1.2.Comparative market share analysis, 2022 & 2030

7.2.Horticulture

7.2.1.Market size and forecast, by region, 2022-2030

7.2.2.Comparative market share analysis, 2022 & 2030

7.3.Gardening

7.3.1.Market size and forecast, by region, 2022-2030

7.3.2.Comparative market share analysis, 2022 & 2030

7.4.Others

7.4.1.Market size and forecast, by region, 2022-2030

7.4.2.Comparative market share analysis, 2022 & 2030

7.5.Research Dive Exclusive Insights

7.5.1.Market attractiveness

7.5.2.Competition heatmap

8.5.Fertilizer Market, by Region

8.1.North America

8.1.1.U.S.

8.1.2.Market size and forecast, by Type, 2022-2030

8.1.3.Market size and forecast, by Sensor type, 2022-2030

8.1.4.Market size and forecast, by Distribution Channel, 2022-2030

8.1.5.Canada

8.1.6.Market size and forecast, by Type , 2022-2030

8.1.7.Market size and forecast, by Form , 2022-2030

8.1.8.Market size and forecast, by Application , 2022-2030

8.1.9.Mexico

8.1.10.Market size and forecast, by Type , 2022-2030

8.1.11.Market size and forecast, by Form , 2022-2030

8.1.12.Market size and forecast, by Application , 2022-2030

8.1.13.Research Dive Exclusive Insights

8.1.13.1.Market attractiveness

8.1.13.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.2.Market size and forecast, by Type , 2022-2030

8.2.3.Market size and forecast, by Form , 2022-2030

8.2.4.Market size and forecast, by Application , 2022-2030

8.2.5.UK

8.2.6.Market size and forecast, by Type , 2022-2030

8.2.7.Market size and forecast, by Form , 2022-2030

8.2.8.Market size and forecast, by Application , 2022-2030

8.2.9.France

8.2.10.Market size and forecast, by Type , 2022-2030

8.2.11.Market size and forecast, by Form , 2022-2030

8.2.12.Market size and forecast, by Application , 2022-2030

8.2.13.Spain

8.2.14.Market size and forecast, by Type , 2022-2030

8.2.15.Market size and forecast, by Form , 2022-2030

8.2.16.Market size and forecast, by Application , 2022-2030

8.2.17.Italy

8.2.18.Market size and forecast, by Type , 2022-2030

8.2.19.Market size and forecast, by Form , 2022-2030

8.2.20.Market size and forecast, by Application , 2022-2030

8.2.21.Rest of Europe

8.2.22.Market size and forecast, by Type , 2022-2030

8.2.23.Market size and forecast, by Form , 2022-2030

8.2.24.Market size and forecast, by Application , 2022-2030

8.2.25.Research Dive Exclusive Insights

8.2.25.1.Market attractiveness

8.2.25.2.Competition heatmap

8.3.Asia Pacific

8.3.1.China

8.3.2.Market size and forecast, by Type , 2022-2030

8.3.3.Market size and forecast, by Form , 2022-2030

8.3.4.Market size and forecast, by Application , 2022-2030

8.3.5.Japan

8.3.6.Market size and forecast, by Type , 2022-2030

8.3.7.Market size and forecast, by Form , 2022-2030

8.3.8.Market size and forecast, by Application , 2022-2030

8.3.9.India

8.3.10.Market size and forecast, by Type , 2022-2030

8.3.11.Market size and forecast, by Form , 2022-2030

8.3.12.Market size and forecast, by Application , 2022-2030

8.3.13.Australia

8.3.14.Market size and forecast, by Type , 2022-2030

8.3.15.Market size and forecast, by Form , 2022-2030

8.3.16.Market size and forecast, by Application , 2022-2030

8.3.17.South Korea

8.3.18.Market size and forecast, by Type , 2022-2030

8.3.19.Market size and forecast, by Form , 2022-2030

8.3.20.Market size and forecast, by Application , 2022-2030

8.3.21.Rest of Asia Pacific

8.3.22.Market size and forecast, by Type , 2022-2030

8.3.23.Market size and forecast, by Form , 2022-2030

8.3.24.Market size and forecast, by Application , 2022-2030

8.3.25.Research Dive Exclusive Insights

8.3.25.1.Market attractiveness

8.3.25.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.2.Market size and forecast, by Type , 2022-2030

8.4.3.Market size and forecast, by Form , 2022-2030

8.4.4.Market size and forecast, by Application , 2022-2030

8.4.5.Saudi Arabia

8.4.6.Market size and forecast, by Type , 2022-2030

8.4.7.Market size and forecast, by Form , 2022-2030

8.4.8.Market size and forecast, by Application , 2022-2030

8.4.9.UAE

8.4.10.Market size and forecast, by Type , 2022-2030

8.4.11.Market size and forecast, by Form , 2022-2030

8.4.12.Market size and forecast, by Application , 2022-2030

8.4.13.South Africa

8.4.14.Market size and forecast, by Type , 2022-2030

8.4.15.Market size and forecast, by Form , 2022-2030

8.4.16.Market size and forecast, by Application , 2022-2030

8.4.17.Rest of LAMEA

8.4.18.Market size and forecast, by Type , 2022-2030

8.4.19.Market size and forecast, by Form , 2022-2030

8.4.20.Market size and forecast, by Application , 2022-2030

8.4.21.Research Dive Exclusive Insights

8.4.21.1.Market attractiveness

8.4.21.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Yara International

10.1.1.Business overview

10.1.2.Financial performance

10.1.3.Product portfolio

10.1.4.Recent strategic moves & developments

10.1.5.SWOT analysis

10.2.Nutrien Ltd.

10.2.1.Business overview

10.2.2.Financial performance

10.2.3.Product portfolio

10.2.4.Recent strategic moves & developments

10.2.5.SWOT analysis

10.3.The Mosaic Company

10.3.1.Business overview

10.3.2.Financial performance

10.3.3.Product portfolio

10.3.4.Recent strategic moves & developments

10.3.5.SWOT analysis

10.4.Haifa Group

10.4.1.Business overview

10.4.2.Financial performance

10.4.3.Product portfolio

10.4.4.Recent strategic moves & developments

10.4.5.SWOT analysis

10.5.ICL Group Ltd.

10.5.1.Business overview

10.5.2.Financial performance

10.5.3.Product portfolio

10.5.4.Recent strategic moves & developments

10.5.5.SWOT analysis

10.6.EuroChem Group

10.6.1.Business overview

10.6.2.Financial performance

10.6.3.Product portfolio

10.6.4.Recent strategic moves & developments

10.6.5.SWOT analysis

10.7.OCP Group S.A.

10.7.1.Business overview

10.7.2.Financial performance

10.7.3.Product portfolio

10.7.4.Recent strategic moves & developments

10.7.5.SWOT analysis

10.8.K+S Aktiengesellschaft

10.8.1.Business overview

10.8.2.Financial performance

10.8.3.Product portfolio

10.8.4.Recent strategic moves & developments

10.8.5.SWOT analysis

10.9.Uralkali

10.9.1.Business overview

10.9.2.Financial performance

10.9.3.Product portfolio

10.9.4.Recent strategic moves & developments

10.9.5.SWOT analysis

10.10.Syngenta AG

10.10.1.Business overview

10.10.2.Financial performance

10.10.3.Product portfolio

10.10.4.Recent strategic moves & developments

10.10.5.SWOT analysis

11.Appendix

11.1.Parent & peer market analysis

11.2.Premium insights from industry experts

11.3.Related reports

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}