Zero Trust Security Market Report

RA05368

Zero Trust Security Market by Solution Type (Network Security, Data Security, Endpoint Security, Security Orchestration Automation and Response, API Security, Security Analytics, Security Policy Management, and Others), Deployment Type (On Premises and Cloud), Authentication Type (Single-Factor Authentication and Multi-Factor Authentication), Organization Size (Small & Medium Enterprises and Large Enterprises), End-user (BFSI, IT & Telecommunications, Government and Defense, Healthcare, Retail, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2021–2030

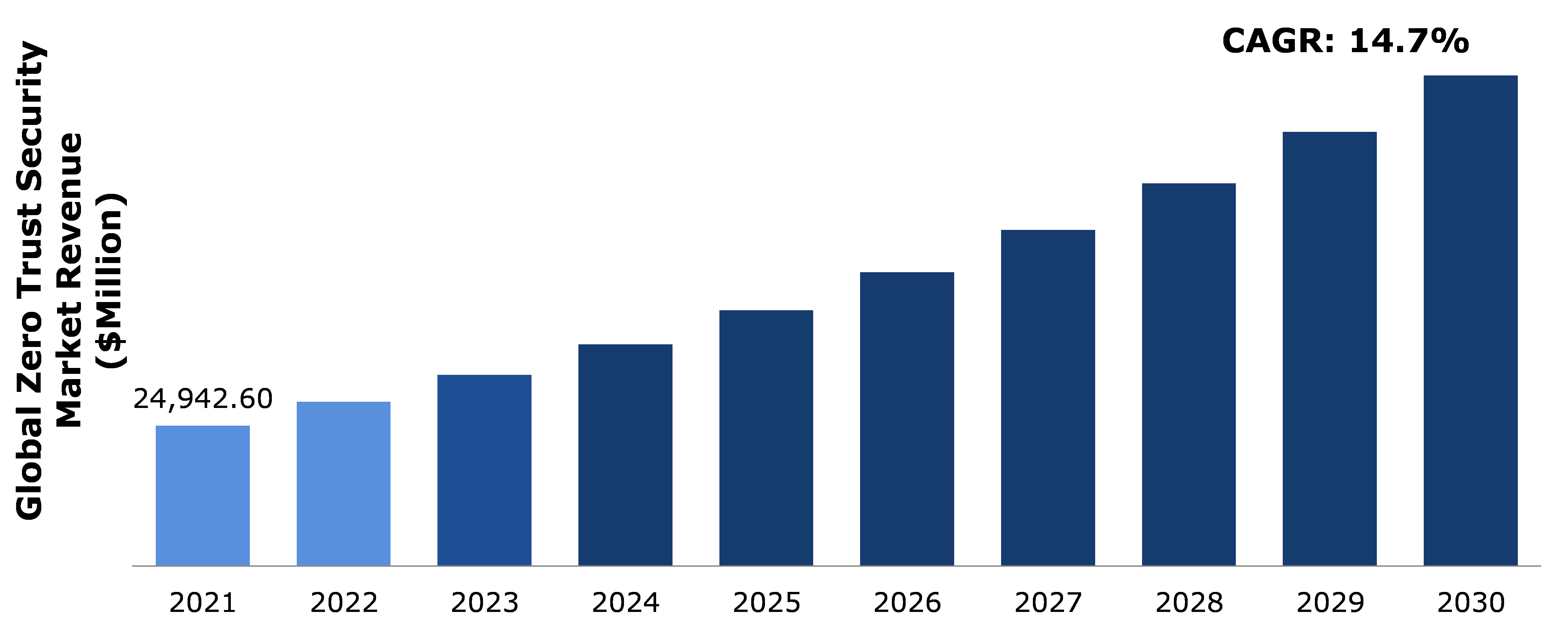

Global Zero Trust Security Market Analysis

The global zero trust security market size was $24,942.6 million in 2021 and is predicted to grow with a CAGR of 14.7%, by generating a revenue of $87,162.8 million by 2030.

Global Zero Trust Security Market Synopsis

Zero trust market is gaining significant popularity as the concept of zero trust security states that devices should never be trusted by default, even if they are connected to a permissioned network such as a corporate LAN and even if they have already been confirmed. Several interconnected zones, cloud services, mobile connectivity, connections to remote and mobile settings, and links to non-conventional IT, including IoT devices, make up the majority of modern business networks. On the other hand, a zero-trust architecture offers significant defense against the kinds of attacks that currently affect businesses, such as the heist of corporate assets and identities. Employing zero trust enables businesses to safeguard corporate data, improve compliance auditing capabilities, reduce breach risk and discovery time, increase network traffic visibility, and exert more control over cloud environments.

However, the high implementation costs associated with zero trust security is expected to hinder the zero trust security market growth. In order to protect the organization’s network and IT infrastructure from various cyber-attacks, the majority of small businesses lack the financial resources and IT security experience to implement better cyber-security solutions. Some small and medium-sized businesses may find it difficult to adopt a zero-trust security architecture due to lack of financial finance and knowledge.

The use of zero trust security is anticipated to gain significant market share. This is due to the fact that the global demand for zero trust security solutions is expanding along with the demand for better data connectivity and the number of companies offering advanced data security solutions. During the projection period, it is anticipated that ongoing digital transformation and an increase in cloud-based infrastructure usage by businesses would drive the global zero trust security market.

According to regional analysis, the Europe zero trust security market accounted for 7,033.8 million in 2021 and is predicted to grow with a CAGR of 15.1% in the projected timeframe. This surge is the result of the region's rising use of mobile devices and cloud-based networking. The market for zero trust security will expand more quickly as there are more people using Internet, more IoT devices are being adopted, and stricter government & industry rules for the security of corporate processes.

Zero Trust Security Overview

Zero trust security is a strategic cyber security technique that safeguards a company by getting rid of implicit trust and constantly confirming each stage of digital contact. Zero trust security, which is based on the maxim ‘never trust, always verify’, uses strong authentication techniques, network segmentation, lateral movement prevention, Layer 7 threat prevention, and simplified granular, ‘least access’ policies to protect modern environments and facilitate digital transformation. The understanding that existing security solutions rely on the antiquated presumption that everything on a company's network should be trusted led to the creation of zero trust security. Due to a lack of granular security restrictions, users, especially threat actors and malicious insiders, are free to move about the network and access or exfiltrate sensitive data once they are connected.

COVID-19 Impact on Zero Trust Security Market

The COVID-19 pandemic has helped the market for zero-trust security to expand significantly over the past few years and is anticipated to do so at an impressive rate in the forecast period. People are more attracted to embrace digital technologies such as cloud solutions as a result of the widespread usage of Bring your own device (BYOD), the work-from-home trend, and Internet penetration in every corner of the world. Enterprises now understand how important a zero-trust environment is for protecting their critical data as a result of the COVID-19 outbreak. With employees using vulnerable networking infrastructure while working remotely, the IT security landscape has radically changed. Due to the difficulty in maintaining a network perimeter-centric view of security across companies, tech-savvy hackers are now able to conduct phishing attacks against unprotected systems. The usage of a zero-trust security method ensures that only authorized individuals have a certain level of access, which is regularly evaluated without increasing user friction. The investment has been comparatively smaller than anticipated by solution providers because the pandemic has deprived firms of their intended income for the years 2020–2021. However, after the pandemic, businesses want to continue operating remotely and will make significant investments in putting the zero-trust infrastructure into place.

Zero Trust Security Helps to Create Well Organized and Time-Saving Security Policies, these Factors are Expected to Drive the Market Growth

Zero trust security helps to create well organized and time-saving security policies. Threat prevention was done using a compartmentalized approach in traditional security frameworks. This implied that every security tool had its own configuration and ran independently of the others. When security tools were lost on the network or were configured incorrectly, this frequently made certain elements of the infrastructure more vulnerable. Zero trust is helpful in this aspect since it allows for the creation of a universal policy that can then be applied throughout the entire organization. Again, Single sign-on (SSO) is an excellent illustration of this as it controls authentication for all network resources. The potential for security vulnerabilities or gaps in some sections of the infrastructure also becomes much less likely, making the deployment and management of security policies from the administrator's perspective much more straightforward.

Financial Limitations in New and Small Businesses in Developing Nations are Anticipated to Restrain Market Growth

The high cost of the implementation of zero trust security is expected to restrain revenue growth of the zero-trust security market. Most small and medium sized businesses lack the financial resources and IT security skills necessary to implement improved cyber-security measures that will protect their network, data and IT infrastructure from a variety of cyber-attacks. A zero-trust security architecture may be difficult for certain small and medium-sized businesses to adopt due to a lack of financial resources and knowledge about the zero trust security networks. These factors are expected to hinder the zero trust security industry growth during forecast period.

Rising Need for Enhanced Data Security Solutions Projected to Create Growth Opportunities for Zero Trust Security Market

The demand for better data communication is expanding, and there are more companies providing advanced data security solutions, which is fueling the expansion of zero trust security market globally. During the projection period, it is anticipated that ongoing digital transformation and an increase in cloud-based infrastructure usage by businesses would drive the global zero trust security market. The introduction of cloud-based solutions and cloud infrastructure has provided numerous benefits to businesses across all industry sectors. Cloud computing has transformed the way businesses operate due to improvements in efficiency, profitability, scalability, and accessibility. These factors are expected to create the zero trust security market opportunity in the forecast period.

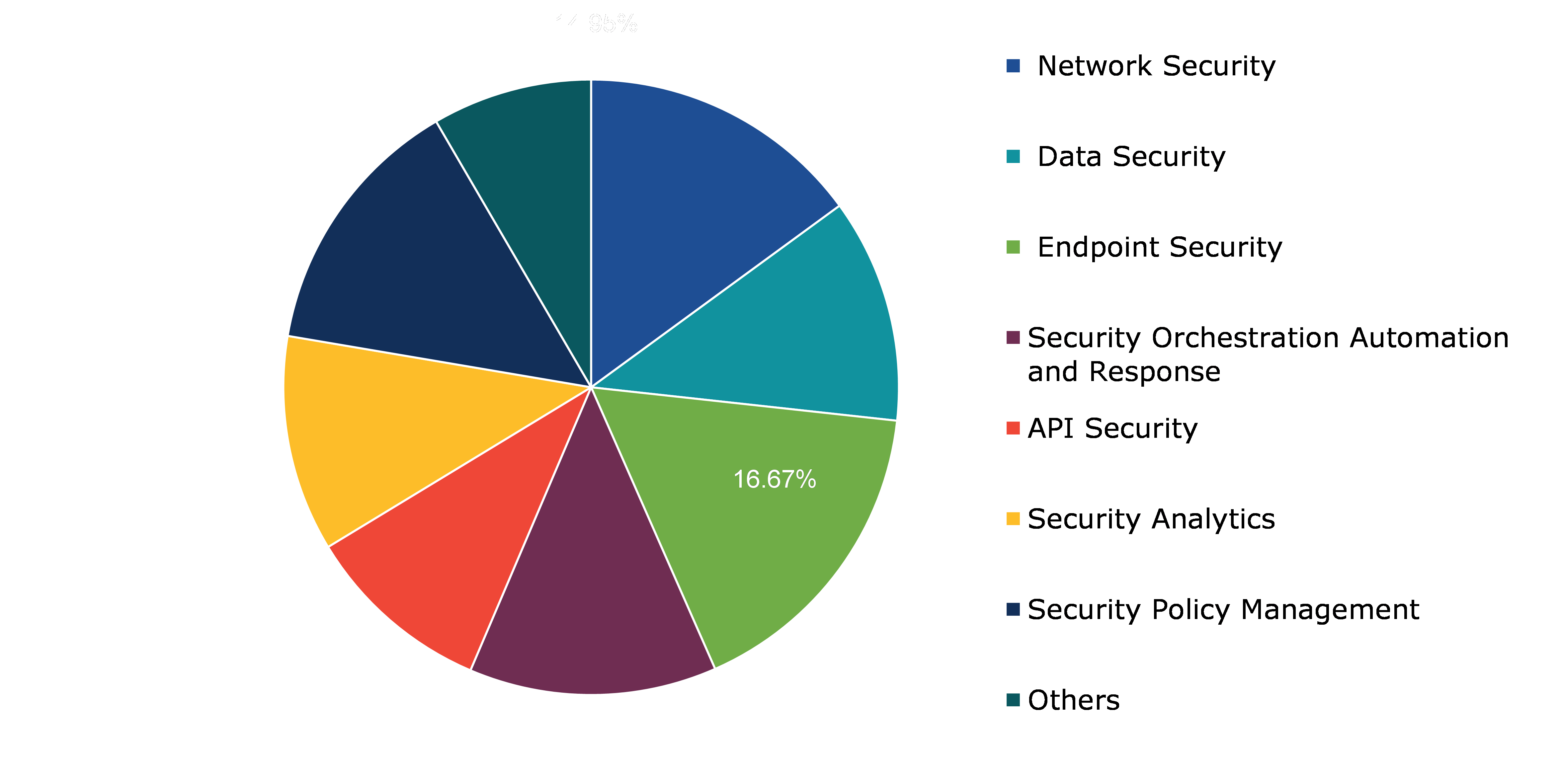

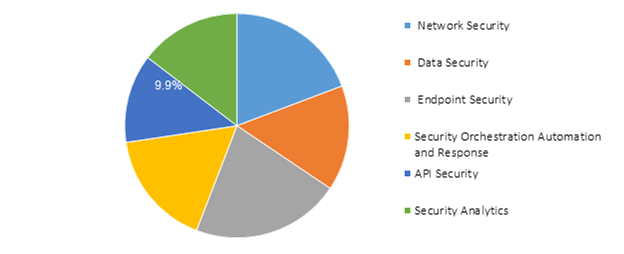

Global Zero Trust Security Market, by Solution Type

Based on solution type, the market is further divided into network security, data security, endpoint security, security orchestration automation and response, API security, security analytics, security policy management, and others. Among these, the endpoint security sub-segment accounted for highest market share in 2021, whereas the data security sub–segment is estimated to show the fastest growth during the forecast period.

Global Zero Trust Security Market Share, by Solution Type, 2021

Source: Research Dive Analysis

The endpoint security sub-segment is forecasted to have dominant market share during the forecast period. The endpoint security sub-segment for solution type of zero trust security market is expected to generate revenue of $13,556.9 million by 2030, increasing from $4,156.9 million in 2021. The development of endpoint solutions was significantly assisted by cutting-edge technologies such as cloud, Artificial Intelligence (AI), Internet of Things (IOT), linked devices, and others.

The data security sub-segment is expected to show the fastest growth during the forecast period. The data security sub-segment for solution type of zero trust security market is expected to generate revenue of $10,966.6 million by 2030, increasing from $2,938.6 million in 2021. The large risk of data theft is driving up product demand across a range of industries. This is the major factor expected to drive the market growth.

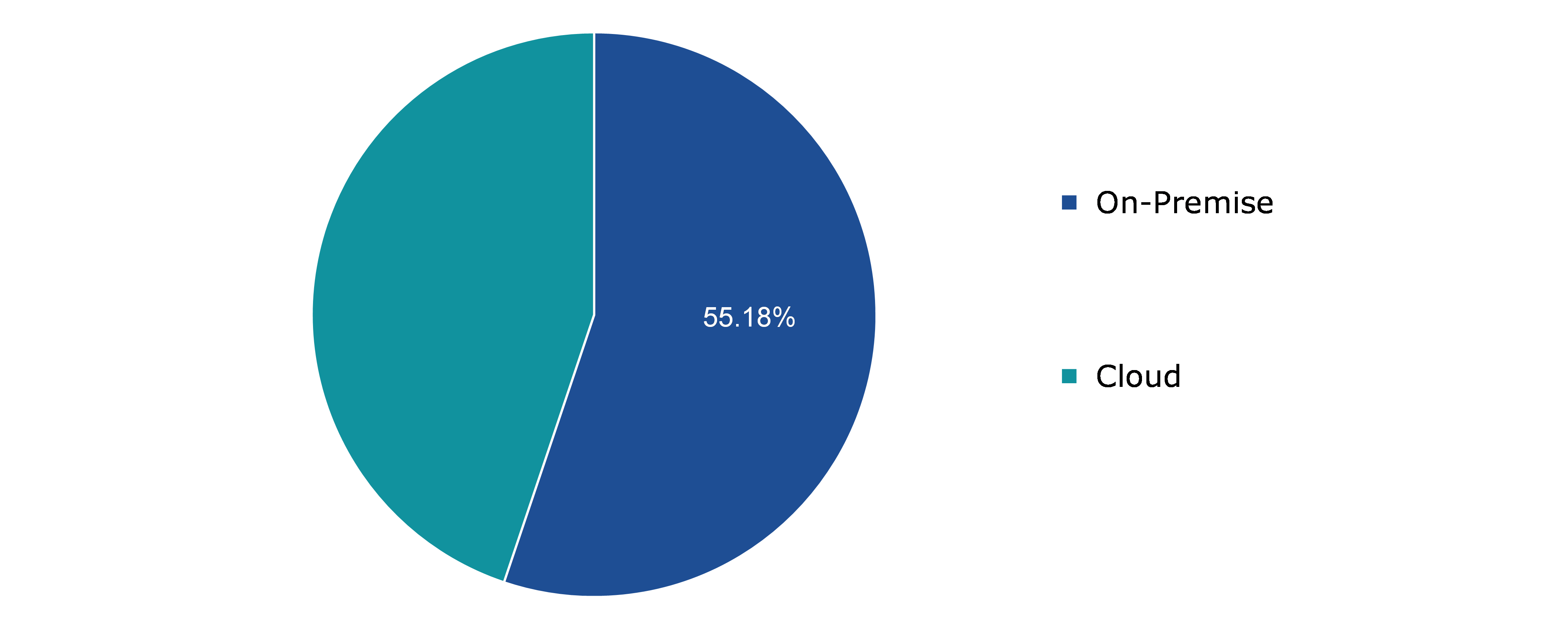

Global Zero Trust Security Market, by Deployment Type

Based on deployment type, the global zero trust security market has been divided into on premises and cloud. Among these, the cloud sub-segment accounted for highest revenue share in 2021, where the on premises sub-segment is anticipated to have the fastest growth during the forecast period.

Global Zero Trust Security Market Share, by Deployment Type, 2021

Source: Research Dive Analysis

The cloud sub-segment is expected to have highest market share during the forecast period. The cloud sub-segment for deployment type of zero trust security market is expected to generate the revenue of $50,837.2 million by 2030, increasing from $11,180.5 million in 2021. The need for technological advancements and security concerns are both increasing. Cloud based applications features data privacy and security, and these factors are expected to drive the market growth in the analysis period.

The on premises sub-segment of the global zero trust security market price is expected to have the fastest growth and exceed $36,325.6 million by 2030, with an increase from $13,762.1 million in 2021. The demand for on-premise enterprise application software is being driven by rising concerns about improving internal systems and procedures, security concerns with cloud deployment, and increased demand for enterprise application software across a variety of industrial verticals.

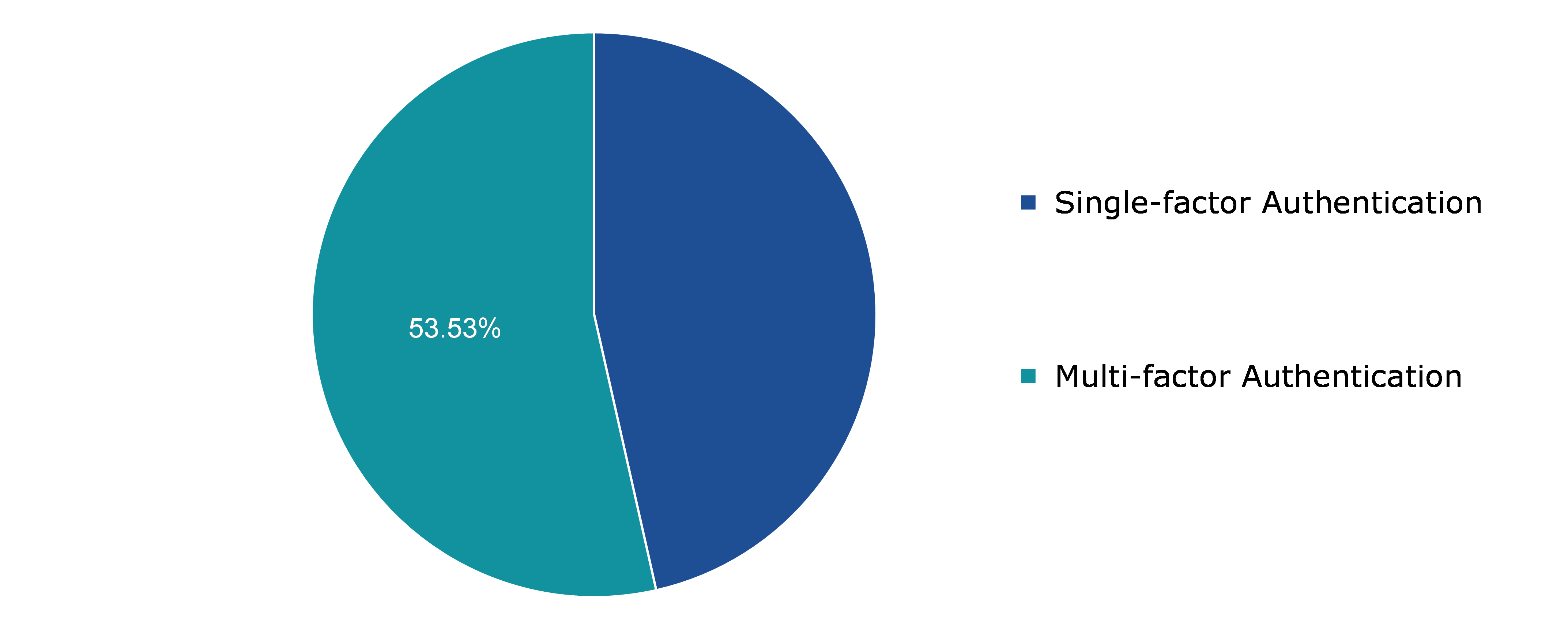

Global Zero Trust Security Market, by Authentication Type

Based on authentication type, the global zero trust security market has been divided into single-factor authentication and multi-factor authentication. Among these, the single-factor authentication sub-segment accounted for highest revenue share in 2021, where the multi-factor authentication sub-segment is anticipated to have the fastest growth during the forecast period.

Global Zero Trust Security Market Share, by Authentication Type, 2021

Source: Research Dive Analysis

The multi-factor authentication sub-segment of the global zero trust security market trends is expected to have the fastest growth and exceed $51,553.7 million by 2030, with an increase from $13,350.9 million in 2021. The growth of the multi-factor authentication sub-segment is primarily being driven by a rise in the number of online transactions, while other factors, such as an increase in the price of OTP tokens, may restrain industry expansion. As a result, multi-factor authentication has been progressively becoming more popular.

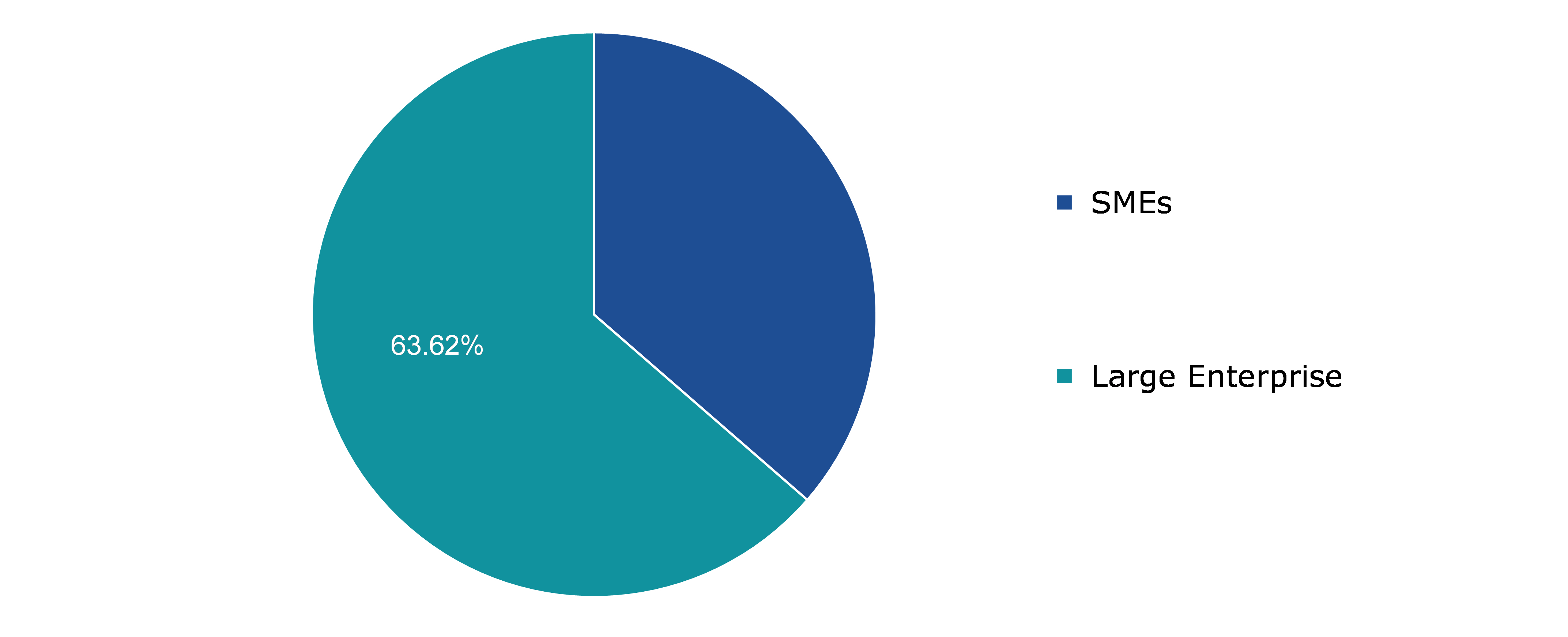

Global Zero Trust Security Market, by Organization Size

Based on organization size, the global zero trust security market has been divided into small & medium enterprises and large enterprises. Among these, the large enterprises sub-segment is anticipated to have the fastest growth and dominant market share during the forecast period.

Global Zero Trust Security Market Share, by Organization Size, 2021

Source: Research Dive Analysis

The large enterprises sub-segment is expected to have highest market share and fastest growth during the forecast period. Large enterprises sub-segment in the organization size segment of the zero trust security market price is expected to generate revenue of $ 41,714.3 million by 2030, increasing from $15,867.4 million in 2021. Due to sophisticated networking, programs, and endpoints of large-scale businesses that require reliable solutions to preserve data by continuously validating and documenting authentication in real-time, the segment will maintain its leadership position during the projection period. Companies rely on entrusting only authorized users, who run a higher risk of an internal breach, and strictly adhering to compliance.

Global Zero Trust Security Market, by End-user

Based on end-user, the global zero trust security market has been divided into BFSI, IT & telecommunications, government and defense, healthcare, retail, and others. Among these, the retail sub-segment accounted for highest revenue and expected to be fastest growing during the forecast period.

Global Zero Trust Security Market Share, by End-user, 2021

Source: Research Dive Analysis

The retail type sub-segment is expected to have highest market share as well as predicted to be fastest growing during the forecast period. The retail type sub-segment in the end-user segment of the zero-trust security market is expected to generate the revenue of $20,010.2 million by 2030, increasing from $ 6,002.7 million in 2021. The retail industries are growing rapidly as a result of the expansion of sales and marketing platforms such as social media and e-commerce. The rise of the retail sub-segment is being driven by an increase in middle-class consumers and an increase in the number of working population worldwide. These factors are estimated to fuel the zero trust security market value.

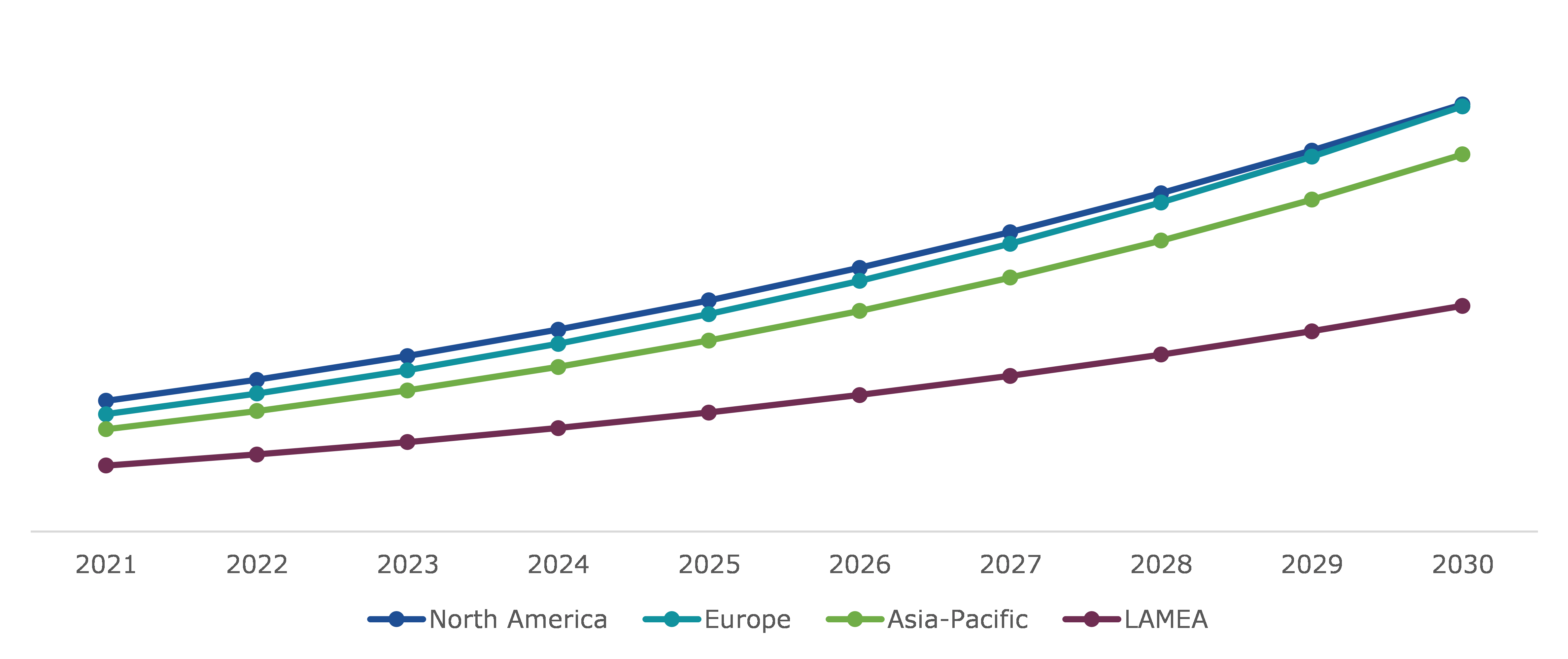

Global Zero Trust Security Market, Regional Insights

The zero trust security market was investigated across Europe, North America, Asia-Pacific, and LAMEA.

Global Zero Trust Security Market Size & Forecast, by Region, 2021-2030 (USD Million)

Source: Research Dive Analysis

The Zero Trust Security Market in Europe to be the Most Dominant

The zero-trust security market in Europe accounted $7,033.8 million in 2021 and is projected to grow with a CAGR of 15.1%. The widespread adoption of mobile devices and cloud-based networking in the region is primarily responsible for the market rapid expansion in Europe. The market for zero trust security will expand more quickly as there are more people using Internet, more IoT devices being adopted, and stricter government & industry rules for the security of corporate processes. These factors are anticipated to boost the zero trust security market value over forecasted time period.

The Zero Trust Security Market in Asia-Pacific is Expected to be the Fastest Growing

The zero-trust security market in Asia-Pacific region accounted $6,128.4 in million in 2021 and is projected to grow with a CAGR of 15.3%. Asia-Pacific is one of the region’s most vulnerable to cyber-attacks due to the rapid increase in the transmission of sensitive data. The region is very concerned about sophisticated cyber-attacks as digitization increases. The Asia-Pacific region has seen a significant growth in demand for zero trust security solutions as people's knowledge of security breaches and their effects on consumer confidence and brand reputation has grown.

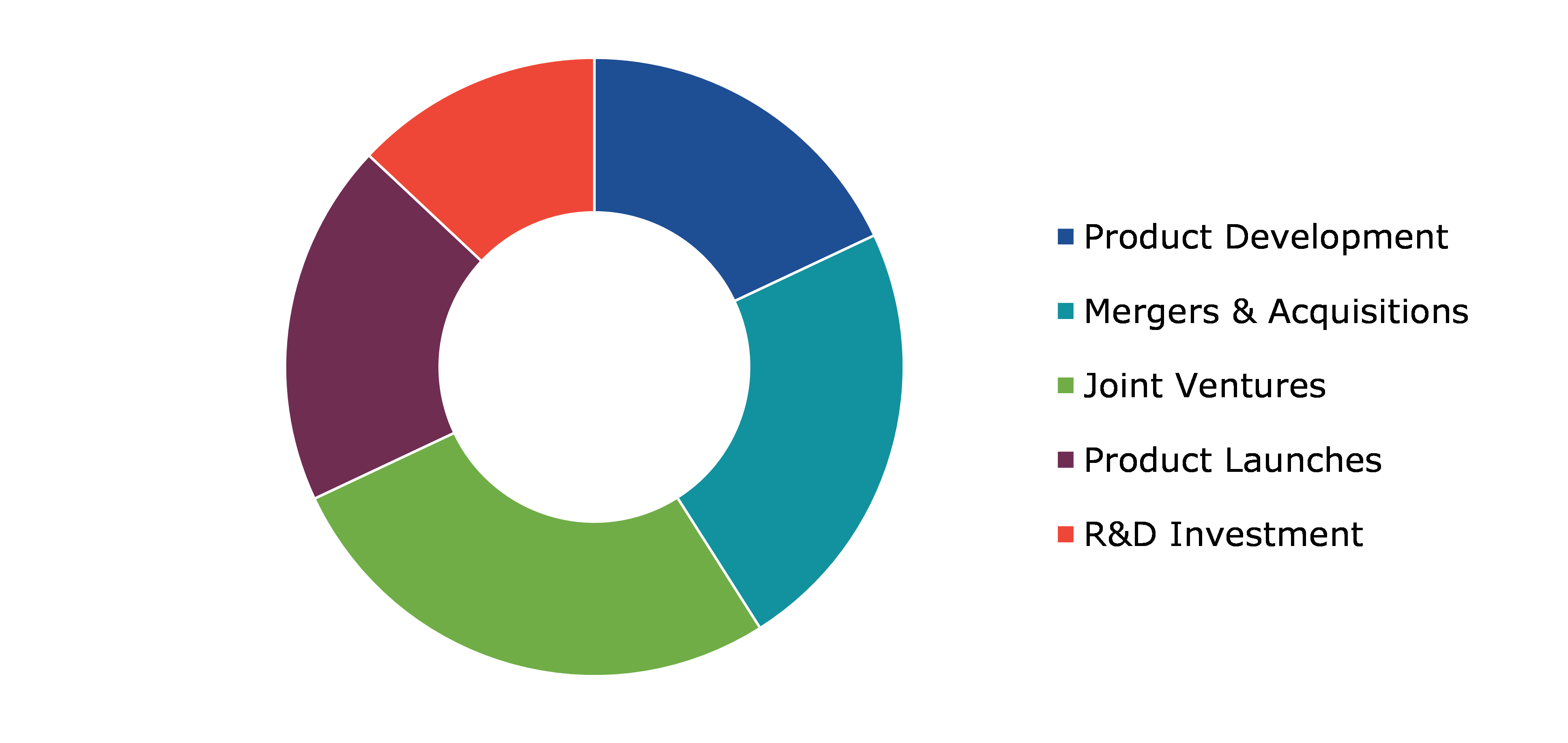

Global Zero Trust Security Market Competitive Scenario

Strategic partnerships, acquisition, and technological development are the common strategies followed by major zero trust security market players.

For instance, in February 2022, The American multinational technology company IBM (International Business Machines) acquired Neudesic, a leading U.S. cloud services consultant with expertise in multicloud and a focus on the Microsoft Azure platform. This acquisition will aid IBM in developing its hybrid multicloud services portfolio and advancing its hybrid cloud and AI strategy.

Source: Research Dive Analysis

Some of the leading players in zero trust security market are Fortinet Inc., Broadcom Inc., Check Point Software Technologies Ltd., Fireeye, Cisco Systems Inc., Akamai Technologies, Palo Alto Networks, Mcafee LLC, IBM Corporation, and Okta.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast timeline for Market Projection | 2022-2030 |

| Geographical Scope | Europe, North America, Asia-Pacific, and LAMEA |

| Segmentation by Solution Type

|

|

| Segmentation by Deployment Type |

|

| Segmentation by Authentication Type |

|

| Segmentation by Organization Size |

|

| Segmentation by End-user |

|

| Key Companies Profiled |

|

Q1. What is the size of the zero-trust security market?

A. The global zero trust security market size was over $24,942.6 million in ¬¬¬2021 and is further anticipated to reach $87,162.8 million by 2030.

Q2. Which are the leading companies in the zero-trust security market?

A. Fortinet, Symantec Corporation, Check Point Software Technologies, and Fireeye Inc. are some of the key players in the global zero trust security market.

Q3. Which region possesses greater investment opportunities in the coming future?

A. Asia-Pacific possesses great investment opportunities for the investors to witness the most promising growth in the coming years.

Q4. What is the growth rate of the Asia-Pacific market?

A. The Asia-Pacific zero trust security market is anticipated to grow at 15.3% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Strategic partnership and technological development are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Cisco Systems Inc., Fireeye Inc., and Broadcom are investing more on R&D activities for developing new products and technologies.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global Zero Trust Security market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on Zero Trust Security market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Zero Trust Security Market Analysis, by Solution Type

5.1.Overview

5.2.Network Security

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region,2021-2030

5.2.3.Market share analysis, by country,2021-2030

5.3.Data Security

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region,2021-2030

5.3.3.Market share analysis, by country,2021-2030

5.4.Endpoint Security

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region,2021-2030

5.4.3.Market share analysis, by country,2021-2030

5.5.Security Orchestration Automation and Response

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region,2021-2030

5.5.3.Market share analysis, by country,2021-2030

5.6.API Security

5.6.1.Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region,2021-2030

5.6.3.Market share analysis, by country,2021-2030

5.7.Security Analytics

5.7.1.Definition, key trends, growth factors, and opportunities

5.7.2.Market size analysis, by region,2021-2030

5.7.3.Market share analysis, by country,2021-2030

5.8.Security Policy Management

5.8.1.Definition, key trends, growth factors, and opportunities

5.8.2.Market size analysis, by region,2021-2030

5.8.3.Market share analysis, by country,2021-2030

5.9.Others

5.9.1.Definition, key trends, growth factors, and opportunities

5.9.2.Market size analysis, by region,2021-2030

5.9.3.Market share analysis, by country,2021-2030

5.10.Research Dive Exclusive Insights

5.10.1.Market attractiveness

5.10.2.Competition heatmap

6.Zero Trust Security Market Analysis, by Deployment Type

6.1.Overview

6.2.On Premises

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region,2021-2030

6.2.3.Market share analysis, by country,2021-2030

6.3.Cloud

6.3.1.Definition, key trends, growth factors, and opportunities

6.3.2.Market size analysis, by region,2021-2030

6.3.3.Market share analysis, by country,2021-2030

6.4.Others

6.4.1.Definition, key trends, growth factors, and opportunities

6.4.2.Market size analysis, by region,2021-2030

6.4.3.Market share analysis, by country,2021-2030

6.5.Research Dive Exclusive Insights

6.5.1.Market attractiveness

6.5.2.Competition heatmap

7.Zero Trust Security Market Analysis, by Authentication Type

7.1.Overview

7.2.Single-factor Authentication

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region,2021-2030

7.2.3.Market share analysis, by country,2021-2030

7.3.Multi-factor Authentication

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region,2021-2030

7.3.3.Market share analysis, by country,2021-2030

7.4.Research Dive Exclusive Insights

7.4.1.Market attractiveness

7.4.2.Competition heatmap

8.Zero Trust Security Market Analysis, by Organization Size

8.1.Overview

8.2.Small & Medium Enterprises

8.2.1.Definition, key trends, growth factors, and opportunities

8.2.2.Market size analysis, by region,2021-2030

8.2.3.Market share analysis, by country,2021-2030

8.3.Large Enterprises

8.3.1.Definition, key trends, growth factors, and opportunities

8.3.2.Market size analysis, by region,2021-2030

8.3.3.Market share analysis, by country,2021-2030

8.4.Research Dive Exclusive Insights

8.4.1.Market attractiveness

8.4.2.Competition heatmap

9.Zero Trust Security Market Analysis, by Vertical Type

9.1.Overview

9.2.BFSI

9.2.1.Definition, key trends, growth factors, and opportunities

9.2.2.Market size analysis, by region,2021-2030

9.2.3.Market share analysis, by country,2021-2030

9.3.IT & Telecommunications

9.3.1.Definition, key trends, growth factors, and opportunities

9.3.2.Market size analysis, by region,2021-2030

9.3.3.Market share analysis, by country,2021-2030

9.4.Government and Defense

9.4.1.Definition, key trends, growth factors, and opportunities

9.4.2.Market size analysis, by region,2021-2030

9.4.3.Market share analysis, by country,2021-2030

9.5.Healthcare

9.5.1.Definition, key trends, growth factors, and opportunities

9.5.2.Market size analysis, by region,2021-2030

9.5.3.Market share analysis, by country,2021-2030

9.6.Retail

9.6.1.Definition, key trends, growth factors, and opportunities

9.6.2.Market size analysis, by region,2021-2030

9.6.3.Market share analysis, by country,2021-2030

9.7.Others

9.7.1.Definition, key trends, growth factors, and opportunities

9.7.2.Market size analysis, by region,2021-2030

9.7.3.Market share analysis, by country,2021-2030

9.8.Research Dive Exclusive Insights

9.8.1.Market attractiveness

9.8.2.Competition heatmap

10.Zero Trust Security Market, by Region

10.1.North America

10.1.1.U.S.

10.1.1.1.Market size analysis, by Solution Type, 2021-2030

10.1.1.2.Market size analysis, by Deployment Type, 2021-2030

10.1.1.3.Market size analysis, Authentication Type, 2021-2030

10.1.1.4.Market size analysis, Organization Size, 2021-2030

10.1.1.5.Market size analysis, Vertical Type, 2021-2030

10.1.2.Canada

10.1.2.1.Market size analysis, by Solution Type, 2021-2030

10.1.2.2.Market size analysis, by Deployment Type, 2021-2030

10.1.2.3.Market size analysis, Authentication Type, 2021-2030

10.1.2.4.Market size analysis, Organization Size, 2021-2030

10.1.2.5.Market size analysis, Vertical Type, 2021-2030

10.1.3.Mexico

10.1.3.1.Market size analysis, by Solution Type, 2021-2030

10.1.3.2.Market size analysis, by Deployment Type, 2021-2030

10.1.3.3.Market size analysis, Authentication Type, 2021-2030

10.1.3.4.Market size analysis, Organization Size, 2021-2030

10.1.3.5.Market size analysis, Vertical Type, 2021-2030

10.1.4.Research Dive Exclusive Insights

10.1.4.1.Market attractiveness

10.1.4.2.Competition heatmap

10.2.Europe

10.2.1.Germany

10.2.1.1.Market size analysis, by Solution Type, 2021-2030

10.2.1.2.Market size analysis, by Deployment Type, 2021-2030

10.2.1.3.Market size analysis, Authentication Type, 2021-2030

10.2.1.4.Market size analysis, Organization Size, 2021-2030

10.2.1.5.Market size analysis, Vertical Type, 2021-2030

10.2.2.UK

10.2.2.1.Market size analysis, by Solution Type, 2021-2030

10.2.2.2.Market size analysis, by Deployment Type, 2021-2030

10.2.2.3.Market size analysis, Authentication Type, 2021-2030

10.2.2.4.Market size analysis, Organization Size, 2021-2030

10.2.2.5.Market size analysis, Vertical Type, 2021-2030

10.2.3.France

10.2.3.1.Market size analysis, by Solution Type, 2021-2030

10.2.3.2.Market size analysis, by Deployment Type, 2021-2030

10.2.3.3.Market size analysis, Authentication Type, 2021-2030

10.2.3.4.Market size analysis, Organization Size, 2021-2030

10.2.3.5.Market size analysis, Vertical Type, 2021-2030

10.2.4.Spain

10.2.4.1.Market size analysis, by Solution Type, 2021-2030

10.2.4.2.Market size analysis, by Deployment Type, 2021-2030

10.2.4.3.Market size analysis, Authentication Type, 2021-2030

10.2.4.4.Market size analysis, Organization Size, 2021-2030

10.2.4.5.Market size analysis, Vertical Type, 2021-2030

10.2.5.Italy

10.2.5.1.Market size analysis, by Solution Type, 2021-2030

10.2.5.2.Market size analysis, by Deployment Type, 2021-2030

10.2.5.3.Market size analysis, Authentication Type, 2021-2030

10.2.5.4.Market size analysis, Organization Size, 2021-2030

10.2.5.5.Market size analysis, Vertical Type, 2021-2030

10.2.6.Rest of Europe

10.2.6.1.Market size analysis, by Solution Type, 2021-2030

10.2.6.2.Market size analysis, by Deployment Type, 2021-2030

10.2.6.3.Market size analysis, Authentication Type, 2021-2030

10.2.6.4.Market size analysis, Organization Size, 2021-2030

10.2.6.5.Market size analysis, Vertical Type, 2021-2030

10.2.7.Research Dive Exclusive Insights

10.2.7.1.Market attractiveness

10.2.7.2.Competition heatmap

10.3.Asia-Pacific

10.3.1.China

10.3.1.1.Market size analysis, by Solution Type, 2021-2030

10.3.1.2.Market size analysis, by Deployment Type, 2021-2030

10.3.1.3.Market size analysis, Authentication Type, 2021-2030

10.3.1.4.Market size analysis, Organization Size, 2021-2030

10.3.1.5.Market size analysis, Vertical Type, 2021-2030

10.3.2.Japan

10.3.2.1.Market size analysis, by Solution Type, 2021-2030

10.3.2.2.Market size analysis, by Deployment Type, 2021-2030

10.3.2.3.Market size analysis, Authentication Type, 2021-2030

10.3.2.4.Market size analysis, Organization Size, 2021-2030

10.3.2.5.Market size analysis, Vertical Type, 2021-2030

10.3.3.India

10.3.3.1.Market size analysis, by Solution Type, 2021-2030

10.3.3.2.Market size analysis, by Deployment Type, 2021-2030

10.3.3.3.Market size analysis, Authentication Type, 2021-2030

10.3.3.4.Market size analysis, Organization Size, 2021-2030

10.3.3.5.Market size analysis, Vertical Type, 2021-2030

10.3.4.Australia

10.3.4.1.Market size analysis, by Solution Type, 2021-2030

10.3.4.2.Market size analysis, by Deployment Type, 2021-2030

10.3.4.3.Market size analysis, Authentication Type, 2021-2030

10.3.4.4.Market size analysis, Organization Size, 2021-2030

10.3.4.5.Market size analysis, Vertical Type, 2021-2030

10.3.5.South Korea

10.3.5.1.Market size analysis, by Solution Type, 2021-2030

10.3.5.2.Market size analysis, by Deployment Type, 2021-2030

10.3.5.3.Market size analysis, Authentication Type, 2021-2030

10.3.5.4.Market size analysis, Organization Size, 2021-2030

10.3.5.5.Market size analysis, Vertical Type, 2021-2030

10.3.6.Rest of Asia-Pacific

10.3.6.1.Market size analysis, by Solution Type, 2021-2030

10.3.6.2.Market size analysis, by Deployment Type, 2021-2030

10.3.6.3.Market size analysis, Authentication Type, 2021-2030

10.3.6.4.Market size analysis, Organization Size, 2021-2030

10.3.6.5.Market size analysis, Vertical Type, 2021-2030

10.3.7.Research Dive Exclusive Insights

10.3.7.1.Market attractiveness

10.3.7.2.Competition heatmap

10.4.LAMEA

10.4.1.Brazil

10.4.1.1.Market size analysis, by Solution Type, 2021-2030

10.4.1.2.Market size analysis, by Deployment Type, 2021-2030

10.4.1.3.Market size analysis, Authentication Type, 2021-2030

10.4.1.4.Market size analysis, Organization Size, 2021-2030

10.4.1.5.Market size analysis, Vertical Type, 2021-2030

10.4.2.Saudi Arabia

10.4.2.1.Market size analysis, by Solution Type, 2021-2030

10.4.2.2.Market size analysis, by Deployment Type, 2021-2030

10.4.2.3.Market size analysis, Authentication Type, 2021-2030

10.4.2.4.Market size analysis, Organization Size, 2021-2030

10.4.2.5.Market size analysis, Vertical Type, 2021-2030

10.4.3.UAE

10.4.3.1.Market size analysis, by Solution Type, 2021-2030

10.4.3.2.Market size analysis, by Deployment Type, 2021-2030

10.4.3.3.Market size analysis, Authentication Type, 2021-2030

10.4.3.4.Market size analysis, Organization Size, 2021-2030

10.4.3.5.Market size analysis, Vertical Type, 2021-2030

10.4.4.South Africa

10.4.4.1.Market size analysis, by Solution Type, 2021-2030

10.4.4.2.Market size analysis, by Deployment Type, 2021-2030

10.4.4.3.Market size analysis, Authentication Type, 2021-2030

10.4.4.4.Market size analysis, Organization Size, 2021-2030

10.4.4.5.Market size analysis, Vertical Type, 2021-2030

10.4.5.Rest of LAMEA

10.4.5.1.Market size analysis, by Solution Type, 2021-2030

10.4.5.2.Market size analysis, by Deployment Type, 2021-2030

10.4.5.3.Market size analysis, Authentication Type, 2021-2030

10.4.5.4.Market size analysis, Organization Size, 2021-2030

10.4.5.5.Market size analysis, Vertical Type, 2021-2030

10.4.6.Research Dive Exclusive Insights

10.4.6.1.Market attractiveness

10.4.6.2.Competition heatmap

11.Competitive Landscape

11.1.Top winning strategies, 2021

11.1.1.By strategy

11.1.2.By year

11.2.Strategic overview

11.3.Market share analysis, 2021

12.Company Profiles

12.1.Fortinet, Inc.

12.1.1.Overview

12.1.2.Business segments

12.1.3.Product portfolio

12.1.4.Financial performance

12.1.5.Recent developments

12.1.6.SWOT analysis

12.2.Broadcom Inc.

12.2.1.Overview

12.2.2.Business segments

12.2.3.Product portfolio

12.2.4.Financial performance

12.2.5.Recent developments

12.2.6.SWOT analysis

12.3.Check Point Software Technologies Ltd.

12.3.1.Overview

12.3.2.Business segments

12.3.3.Product portfolio

12.3.4.Financial performance

12.3.5.Recent developments

12.3.6.SWOT analysis

12.4.FireEye

12.4.1.Overview

12.4.2.Business segments

12.4.3.Product portfolio

12.4.4.Financial performance

12.4.5.Recent developments

12.4.6.SWOT analysis

12.5.Cisco Systems, Inc.

12.5.1.Overview

12.5.2.Business segments

12.5.3.Product portfolio

12.5.4.Financial performance

12.5.5.Recent developments

12.5.6.SWOT analysis

12.6.Akamai Technologies

12.6.1.Overview

12.6.2.Business segments

12.6.3.Product portfolio

12.6.4.Financial performance

12.6.5.Recent developments

12.6.6.SWOT analysis

12.7.Palo Alto Networks

12.7.1.Overview

12.7.2.Business segments

12.7.3.Product portfolio

12.7.4.Financial performance

12.7.5.Recent developments

12.7.6.SWOT analysis

12.8.McAfee, LLC.

12.8.1.Overview

12.8.2.Business segments

12.8.3.Product portfolio

12.8.4.Financial performance

12.8.5.Recent developments

12.8.6.SWOT analysis

12.9.IBM Corporation

12.9.1.Overview

12.9.2.Business segments

12.9.3.Product portfolio

12.9.4.Financial performance

12.9.5.Recent developments

12.9.6.SWOT analysis

12.10.Okta

12.10.1.Overview

12.10.2.Business segments

12.10.3.Product portfolio

12.10.4.Financial performance

12.10.5.Recent developments

12.10.6.SWOT analysis

13.Appendix

13.1.Parent & peer market analysis

13.2.Premium insights from industry experts

13.3.Related reports

Zero trust security is a strategic cybersecurity technique that protects an organization from getting rid of implicit trust and regularly confirming every digital contact. The policy is based on ‘never trust, always verify’ and uses strong network segmentation, threat prevention, reliable authentication techniques, etc. The lack of zero trust security and other granular security restrictions allows tech-savvy attackers to conduct malicious activities and access sensitive corporate information. The policy also emphasizes on never trusting devices by default, even if they’re connected to a corporate LAN or any other permissioned network.

Forecast Analysis of the Zero Trust Security Market

Organizations’ growing demand for better data security solutions, availability of high-speed internet connectivity, and the rising adoption of cloud-based models for better scalability, profitability, accessibility, and efficiency are some factors to drive the growth of the global zero trust security market during the analysis years. Moreover, the potential for security vulnerabilities in some sections of the infrastructure and the increasing demand for better data communication are some more factors predicted to offer ample growth opportunities for the global zero trust security market by 2030. In addition, the implementation of well-organized and time-saving data security policies by businesses is also estimated to augment the market development during the analysis years. However, high implementation cost of zero trust security is the major hampering factor for the market growth.

Regionally, the zero trust security market in the Europe region is projected to be the most dominant and grow at 15.1% CAGR by 2030 due to widespread adoption of mobile devices and cloud-based technologies in the region. Moreover, government’s strict regulations regarding data protection in corporates is also estimated to augment the market growth in the Europe region during the forecast period.

According to the report published by Research Dive, the global zero trust security market is expected to garner a revenue of $87,162.8 million and grow at 14.7% CAGR during the 2021-2030 analysis timeframe. Some significant zero trust security market players are Fireeye, Akamai Technologies, Okta, Broadcom Inc., Fortinet Inc., Cisco Systems Inc., Palo Alto Networks, IBM Corporation, Check Point Software Technologies Ltd., Mcafee LLC, among others.

Covid-19 Impact on the Market

The onset of the covid-19 pandemic has positively impacted the global zero trust security market mainly due to increased adoption of digital technologies like cloud computing during the catastrophic chaos. Governments worldwide have imposed strict travel restrictions and social distancing norms that has forced employees to work from home. This has led to the growing demand for high-speed internet connectivity and well-established data security solutions especially in the corporate industry. And due to vulnerable networking infrastructure, tech-savvy hackers can easily conduct phishing attacks against unprotected systems. These factors are anticipated to augment the market growth during the pandemic chaos.

Prominent Zero Trust Security Market Trends & Developments

Some prominent organizations operating in the industry are adopting numerous growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, thus helping the market to flourish during the 2021-2030 analysis period. For instance:

In October 2021, Vectra AI, an AI-driven threat detection solutions provider, announced its collaboration with Microsoft at GITEX Technology Week 2021, to actively mitigate threats emerging from distributed and hybrid-remote workforces. The strategic collaboration brought its Threat Detection and Response platform’s zero trust capabilities to Microsoft platforms for Office 365 and Azure AD.

In December 2021, Tech Data India, a world-class software company, announced its partnership with Zscaler, a cloud services provider, to boost and purchase security solutions as part of the latter’s zero trust security platform directly from Tech Data India.

In February 2022, IBM (International Business Machines), an American multinational technology company, announced its acquisition of Neudesic, a renowned U.S. cloud services consultant, to develop its hybrid multi-cloud services portfolio and enhance its hybrid cloud and AI strategy with the help of the latter’s expertise in the cloud domain.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com