Fluid Sensors Market Report

RA05178

Fluid Sensors Market by Type (Flow Sensor and Level Sensor), Technology (Non-contact Sensor and Contact Sensor), End-user (Automotive, Water & Wastewater, Oil & Gas, Chemical, Food & Beverage, Power & Utilities, and Others), and Regional Analysis (North America, Europe, Asia-Pacific, and LAMEA): Global Opportunity Analysis and Industry Forecast, 2022-2030

Global Fluid Sensors Market Analysis

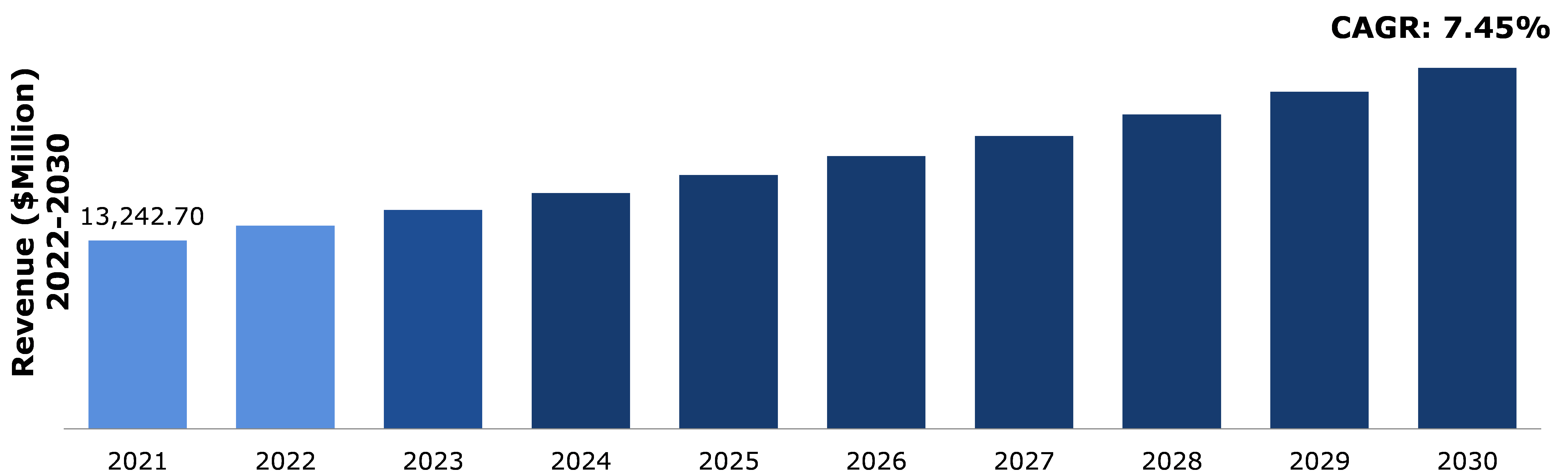

The global fluid sensors market is projected to garner $25,388.9 million in the 2022-2030 timeframe, growing from $13,242.7 million in 2021, at a healthy CAGR of 7.45%.

Market Synopsis

Increasing emphasis on industrial automation is expected to aid the growth of the fluid sensors market size. Fluid sensors are used in almost all manufacturing and processing industries. These sensors are used in the oil & gas industry for storage tank level monitoring, lubricating & hydraulic oil reservoirs, and wall-head automation. Chemical, power generation and water & waste water treatment sectors are some of the other major end-users of fluid sensors, and the growth of each of these industries is positively impacting the fluid sensors market.

However, the high initial investment required in the fluid sensors industry is predicted to restrict the market growth. Fluid sensors are very expensive as many costly parts are required for its manufacturing.

According to regional analysis, the Asia-Pacific fluid sensors market accounted for $4,495.9

million in 2021 and is predicted to grow with a CAGR of 8.42% in the projected timeframe.

Fluid Sensors Overview

A fluid sensor is an electronic device that measures or regulates the flow rate of liquids and gasses within pipes and tubes. Fluid sensors are generally connected to gauges to render measurements and can also be connected to computers and digital interfaces. They are used to measure fluid pressure, temperature, level control, volume of the fluid flowing, and others. Fluid sensors have applications in different industries such as oil and gas, water & wastewater, chemical, power generation, food and beverage, automotive, and others.

Covid-19 Impact on Fluid Sensors Market

The Covid-19 impact on fluid sensors market has been negative. During the pandemic period, industries and sectors where the fluid sensors are utilized in equipment such as automotive, oil & gas, chemical, food & beverage, power & utilities, and others witnessed a decline in their growth due to reduction in consumer demand. These factors are expected to negatively impact the fluid sensors market.

However, during the pandemic period, businesses across the world are experiencing the need for digital management of their operations. The need for implementation of technologies such as industrial internet of things (IIOT) will enable real-time monitoring of manufacturing process of fluid sensors products and virtual control of production. These factors are expected to have a positive impact on the market growth as well as desirable impact on the fluid sensors market size in the pandemic period.

Increasing Emphasis on Industrial Automation is Expected to Surge the Fluid Sensors Market Growth

The increasing emphasis on industrial automation is expected to aid the growth of the global fluid sensors market shares. The advancement in measurement technologies such as optical sensing, vibrating or tuning fork, ultrasonic sensors, capacitance sensing, and others has led to the reduction in manual measurement methods of different parameters of the fluid such as temperature, fluid pressure, and humidity and fluid acceleration in industries like automotive, manufacturing, chemical, medical, oil & gas, and power generation. In addition to this, the increased emphasis on research and development, for instance, in October 2020, Cambridge shire, United Kingdom based startup Flusso, a fabless semiconductor company, launched the world’s smallest flow sensors as part of a low-cost and complete digital flow sensing solution to be used in high-volume consumer and industrial markets. These factors are expected to aid the growth of the global fluid sensors market share in the forecast period.

The demand for high-performance automated solutions to ensure comfort and safety has increased in the automobile industry. Leading automobile manufacturers, such as Audi and BMW, are progressively incorporating sensors into their automobiles. To avoid potential problems, sensors are utilized to measure fluid in the braking system, as well as to detect water cooling and temperature. To detect many fluid points or low liquid levels, liquid sensors with integrated cable connections and magnetic floats can be employed.

To know more about global fluid sensors market drivers, get in touch with our analysts here.

The Capital-intensive Nature of Fluid Sensors Technology to Restrain the Market Growth

The high investment required for research & development and implementation of fluid sensors technology for the measurement of different parameters such as fluid pressure, temperature, level control, volume, and others can act as restraints in the growth of fluid sensors market. In addition to this, unreliable and insecure communication associated with wireless fluid sensor is one of the major challenges that is likely to hamper the growth of the fluid sensors industry. This is majorly observed in cases where the fluid sensor gives wrong or misleading signals related to any fluid flow due to some technical fault. Therefore, there is lack of synchronization in use of fluid sensors. These factors can hamper the growth of the fluid sensors market share in the forecast period.

The Increasing Prominence of Industrial Internet of Things (IIOT) is Expected to Create Massive Opportunities for The Market

Industrial internet of things (IIOT) refers to devices that are interconnected. Industrial equipment such as motors, wastewater transmission systems, sensors, and other machines work in a coordinated manner with the help of IOT software for industrial applications. The fluid sensors market trends such as the implementation of industrial internet of things is expected to bring benefits such as remote access of the device and technicians can control the fluid sensors from remote places. The system can predict the need of maintenance of the sensors when the chances of equipment failure are high. These features are expected to bring improvement in the domain of operational efficiency, mass customization, remote diagnostics, and others. These factors are anticipated to open new scope of opportunities for the fluid sensors market.

The adoption of fluid sensors in many industry verticals would be aided by technological advances in the fluid sensors market. Developments in wireless transmission technologies are allowing for improved communication across multiple devices, allowing for granular management of all system characteristics. Field effect sensors are unique as they can detect semi-solid objects and fluids without having to come into direct touch with them. The development of robust sensors that can resist hostile environments has been facilitated by continual improvements in the electronics and semiconductor industries. Fluid sensors market expansion would be aided by the introduction of smart sensors that can adapt to their surroundings and provide highly precise readings.

To know more about global fluid sensors market opportunities, get in touch with our analysts here.

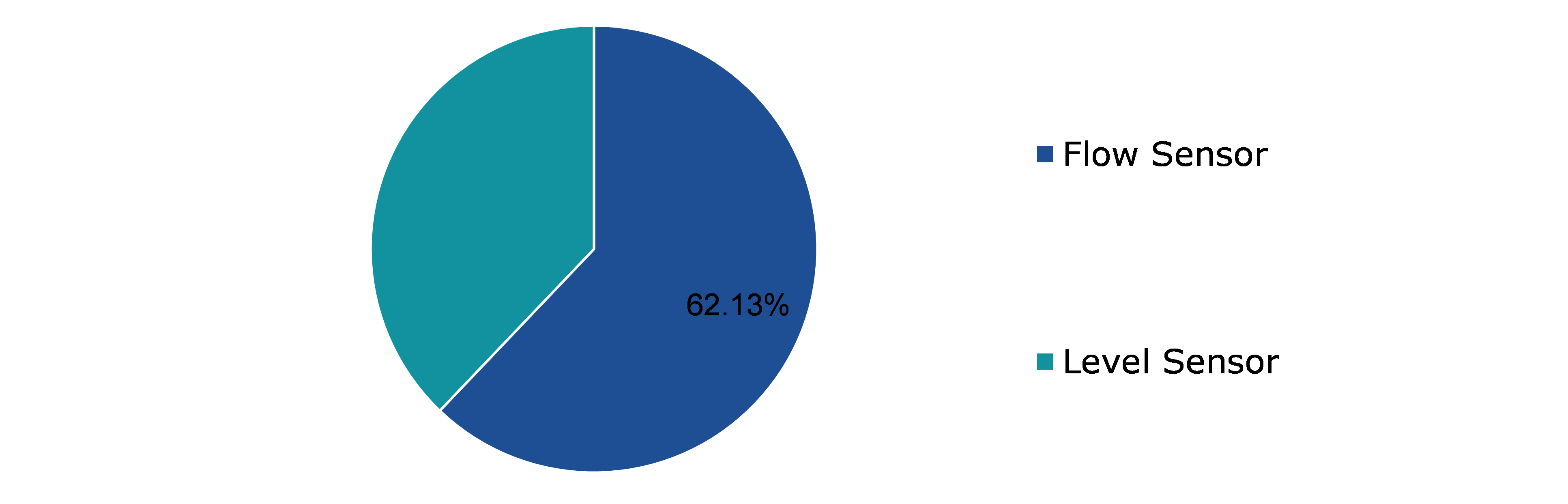

Global Fluid Sensors Market, by Type

Based on type, the market has been divided into flow sensor and level sensor. Among these, the flow sensor sub-segment is anticipated to generate the maximum revenue and the level sensor sub-segment is expected to show the fastest growth.

Global Fluid Sensor Market Share, By Type, 2021

Source: Research Dive Analysis

The flow sensor sub-segment is predicted to have a dominating share in the global market and register a revenue of $15,510.4 million in 2030, growing from $8,227.2 million in 2021 during the forecast period. Flow sensor is an electronic device that measures or regulates the flow rate of liquids and gasses within pipes and tubes. The increasing emphasis on industrial automation is expected to aid the growth of flow sensor sub-segment in the forecast period. The advancement in measurement technology has led to the reduction in manual measurement methods of different parameters of the fluid such as temperature, fluid pressure, humidity, and fluid acceleration in industries like oil & gas, manufacturing, automotive, chemical, medical and power generation. These factors are anticipated to propel the growth of the flow sensor sub-segment.

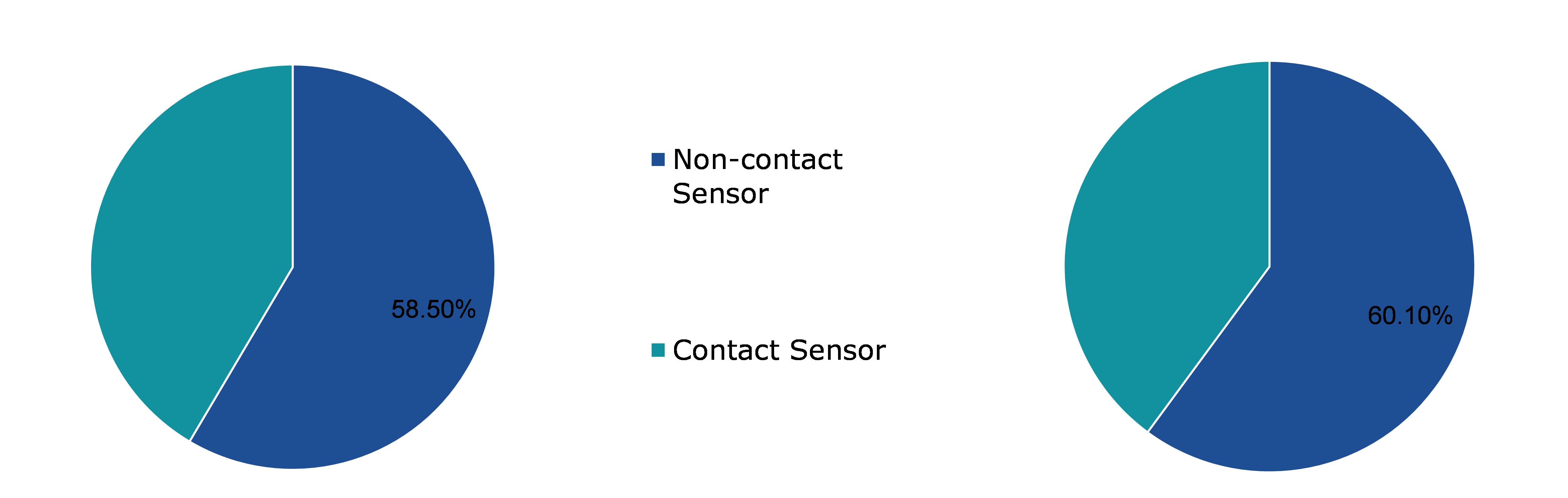

Global Fluid Sensors Market, by Technology

Based on technology, the market has been divided into non-contact sensor and contact sensor. Non-contact sensor sub-segment is anticipated to generate the maximum revenue as well as the fastest growth in the forecast period.

Global Fluid Sensor Market Share, By Technology, 2021 and 2030

Source: Research Dive Analysis

The non-contact sensor sub-segment is estimated to have a dominating market share as well as the fastest growth in the global market and register a revenue of $15,258.4 million in year 2030, with a healthy CAGR of 7.7% during the forecast period.

Non-contact sensors are the fluid sensors which measure the fluid parameters such as temperature, velocity, and the pressure of the fluid by using fluid pressure sensors without coming in contact with the fluid. The wide scale utilization of non-contact sensors for calculation of fluid velocity, temperature, and volume is expected to aid the growth of the sub-segment. The application of non-contact sensors in diverse fields such as measuring fluid flow rate in food production, blood infusions, catheterization, flow rate of liquids in rigid tubes of wafer cleaning equipment in the semiconductor industry, and others is expected to aid the growth of the non-contact sensor sub-segment.

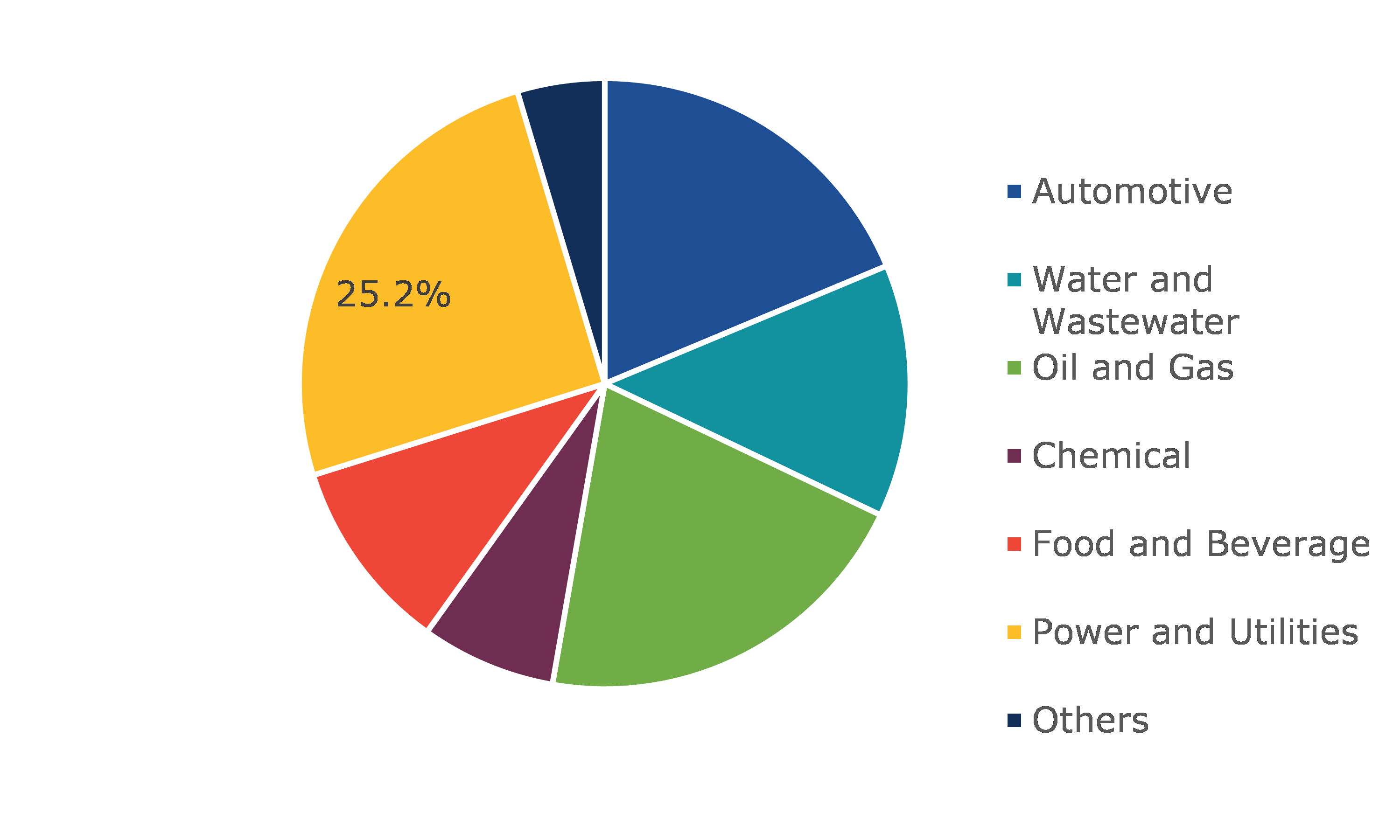

Global Fluid Sensors Market, by End-user

Based on end-user, the market has been sub-segmented into oil & gas, water & wastewater, chemical, power & utilities, food & beverage, automotive, and others. Among the mentioned sub-segments, the power & utilities sub-segment is estimated to show a dominant share, whereas the water & wastewater sub-segment is projected to garner the fastest growth.

Global Fluid Sensors Market Share, by End-user, 2021

Source: Research Dive Analysis

The power & utilities sub-segment is anticipated to have a dominating share in the global market and surpass $5,819.7 million by 2030, with an increase from $3,339.6 million in 2021.

The rising need for electricity globally due to increasing population around the globe coupled with large demand of electricity in industries has led to increase in the number of power generation plants and is aiding the growth of power & utility sub-segment. The application of fluid sensors in the power generation units such as thermal and hydro power plants has advantages such as the flow sensor ensures lowest level of emissions. For instance, advanced flow meters help monitor the rate of ammonia (NH3) gas from the chimneys, and flow measurement devices are flexible in terms of installation. These factors are expected to aid the growth of sub-segment in the forecast period.

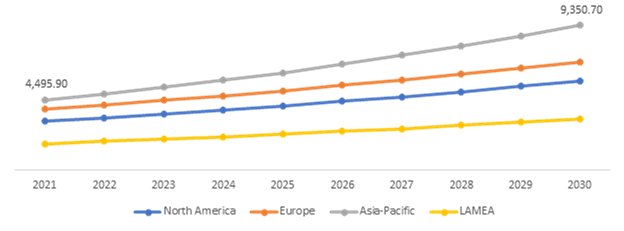

Global Fluid Sensors Market, Regional Insights:

The fluid sensors market was investigated across North America, Europe, Asia-Pacific, and LAMEA.

Global Fluid Sensors Market Size & Forecast, By Region, 2021-2030($Million)

Source: Research Dive Analysis

The Market for Fluid Sensors in Asia-Pacific to be the Most Dominating and Fastest Growing

The Asia-Pacific fluid sensors market generated $4,495.9 million in 2021 and is projected to register a revenue of $9,350.7 million by 2030. The increasing rate of industrial production in the emerging and developed countries of the region such as China, India, Japan, and South Korea that are the major centers of production of industrial fluid sensors is aiding the growth of the market in the region. In addition to this, rapid economic development in the Asia continent due to increase in per capita income and development of industrial infrastructure in the private & public domain has contributed to the high utilization of fluid sensors in the oil & gas, water & wastewater, chemical, food & beverage, automotive, and other sectors in the Asia-Pacific region, and propelling the growth of fluid sensors market.

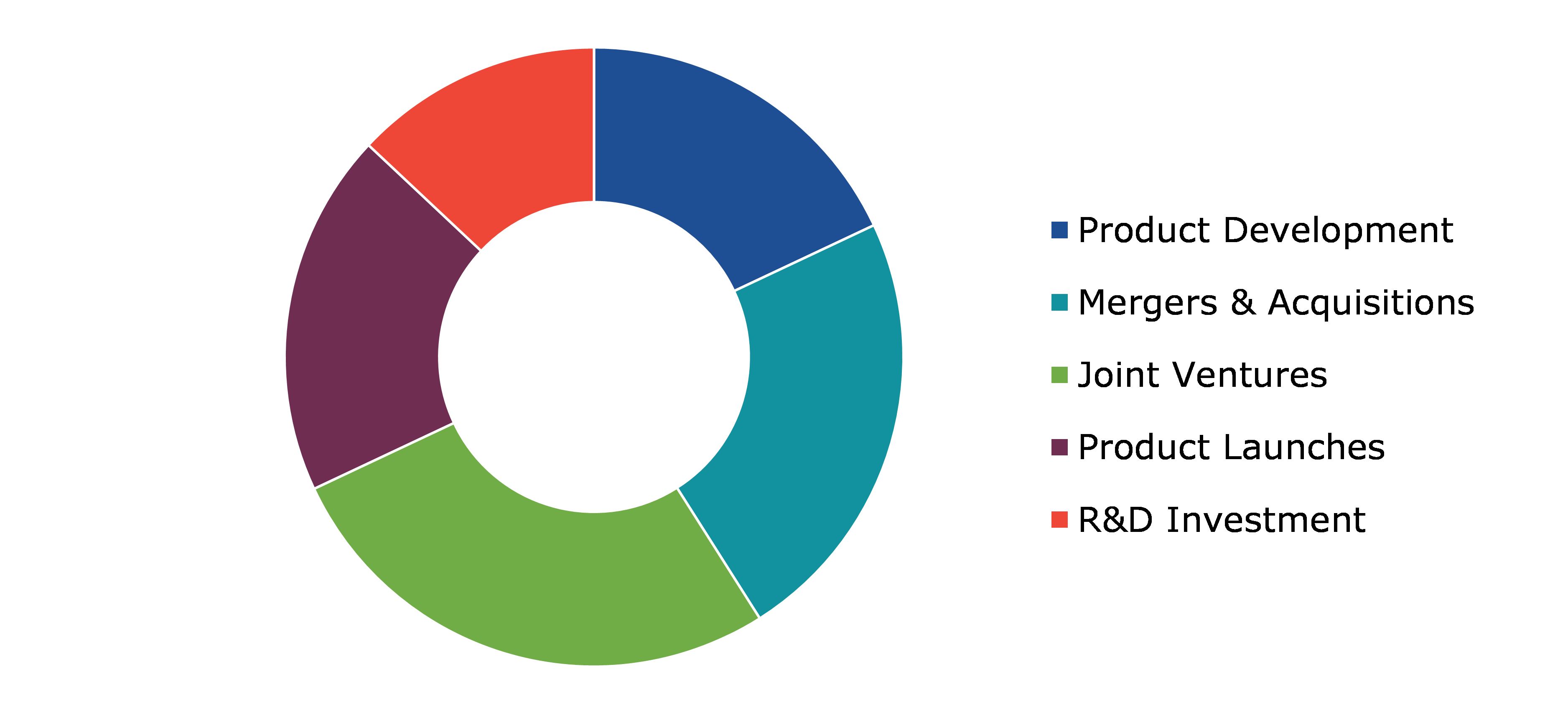

Competitive Scenario in the Global Fluid Sensors Market

Product launches and mergers & acquisitions are common strategies followed by major market players.

Source: Research Dive Analysis

Some of the leading fluid sensors market players are Schneider Electric, Siemens, ABB, Honeywell, Robert Bosch GmbH, Emersion Electric Company, SICK AG, NXP Semiconductors, Texas Instruments, and Rockwell Automation.

| Aspect | Particulars |

| Historical Market Estimations | 2020 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2030 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by Technology |

|

| Segmentation by End-user |

|

| Key Companies Profiled |

|

Q1. What is the size of the global fluid sensors market?

A. The global fluid sensors market is projected to garner $25,388.9 million in the 2022-2030 timeframe, growing from $13,242.7million in 2021, at a healthy CAGR of 7.45%.

Q2. Which are the major companies in the fluid sensors market?

A. Texas Instruments and Rockwell Automation are some of the key players in the global fluid sensors market.

Q3. Which region, among others, possesses greater investment opportunities in the near future?

A. The Asia-Pacific region possesses great investment opportunities for investors to witness the most promising growth in the future.

Q4. What will be the growth rate of the Asia-Pacific fluid sensors market?

A. Asia-Pacific fluid sensors market is anticipated to grow at an 8.42% CAGR during the forecast period.

Q5. What are the strategies opted by the leading players in this market?

A. Acquisition and agreement are the key strategies opted by the operating companies in this market.

Q6. Which companies are investing more on R&D practices?

A. Robert Bosch GmbH and Emersion Electric Company are investing more on R&D activities for developing new products and technologies.

Q7. What are the different types of level sensors?

A. The different types of level sensors are float, capacitance, radar, conductivity, and resistance.

Q8. How does a capacitive liquid level sensor work?

A. The capacitive liquid level sensor works by processing capacitance with reference to the dielectric constant of the material being measured and the voltage being used to complete the circuit.

Q9. What are flow and level sensors?

A. Flow sensor is an electronic device that measures or regulates the flow rate of liquids and gasses within pipes and tubes. A fluid level sensor is a device that is designed to measure the liquid levels that include slurries, granular materials, powders, and others.

Q10. Which sensor is used to detect water level?

A. The hydrostatic pressure level sensor is used to detect water level.

Q11. What does capacitive sensor detect?

A. The capacitive sensor detects proximity, pressure, position & displacement, force, humidity, fluid level, and acceleration.

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global fluid sensors market

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on fluid sensors market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Fluid Sensors Market, by Type

5.1.Overview

5.1.1.Market size and forecast, by Type

5.2.Flow Sensor

5.2.1.Key market trends, growth factors, and opportunities

5.2.2.Market size and forecast, by region, 2022-2030

5.2.3.Market share analysis, by country 2022 & 2030

5.3.Level Sensor

5.3.1.Key market trends, growth factors, and opportunities

5.3.2.Market size and forecast, by region, 2022-2030

5.3.3.Market share analysis, by country 2022 & 2030

5.4.Research Dive Exclusive Insights

5.4.1.Market attractiveness

5.4.2.Competition heatmap

6.Fluid Sensors Market, by Technology

6.1.Overview

6.1.1.Market size and forecast, by Technology

6.2.Non-contact Sensor

6.2.1.Key market trends, growth factors, and opportunities

6.2.2.Market size and forecast, by region, 2022-2030

6.2.3.Market share analysis, by country 2022 & 2030

6.3.Contact Sensor

6.3.1.Key market trends, growth factors, and opportunities

6.3.2.Market size and forecast, by region, 2022-2030

6.3.3.Market share analysis, by country 2022 & 2030

6.4.Research Dive Exclusive Insights

6.4.1.Market attractiveness

6.4.2.Competition heatmap

7.Fluid Sensors Market, by End-user

7.1.Overview

7.1.1.Market size and forecast, by end-user

7.2.Automotive

7.2.1.Key market trends, growth factors, and opportunities

7.2.2.Market size and forecast, by region, 2022-2030

7.2.3.Market share analysis, by country 2022 & 2030

7.3.Water & Wastewater

7.3.1.Key market trends, growth factors, and opportunities

7.3.2.Market size and forecast, by region, 2022-2030

7.3.3.Market share analysis, by country 2022 & 2030

7.4.Oil & Gas

7.4.1.Key market trends, growth factors, and opportunities

7.4.2.Market size and forecast, by region, 2022-2030

7.4.3.Market share analysis, by country 2022 & 2030

7.5.Chemical

7.5.1.Key market trends, growth factors, and opportunities

7.5.2.Market size and forecast, by region, 2022-2030

7.5.3.Market share analysis, by country 2022 & 2030

7.6.Food & Beverage

7.6.1.Key market trends, growth factors, and opportunities

7.6.2.Market size and forecast, by region, 2022-2030

7.6.3.Market share analysis, by country 2022 & 2030

7.7.Power & Utilities

7.7.1.Key market trends, growth factors, and opportunities

7.7.2.Market size and forecast, by region, 2022-2030

7.7.3.Market share analysis, by country 2022 & 2030

7.8.Others

7.8.1.Key market trends, growth factors, and opportunities

7.8.2.Market size and forecast, by region, 2022-2030

7.8.3.Market share analysis, by country 2022 & 2030

7.9.Research Dive Exclusive Insights

7.9.1.Market attractiveness

7.9.2.Competition heatmap

8.Fluid Sensors Market, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Type

8.1.1.2.Market size analysis, by Technology

8.1.1.3.Market size analysis, by end-user

8.1.2.Canada

8.1.2.1.Market size analysis, by Type

8.1.2.2.Market size analysis, by Technology

8.1.2.3.Market size analysis, by end-user

8.1.3.Mexico

8.1.3.1.Market size analysis, by Type

8.1.3.2.Market size analysis, by Technology

8.1.3.3.Market size analysis, by end-user

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Type

8.2.1.2.Market size analysis, by Technology

8.2.1.3.Market size analysis, by end-user

8.2.2.UK

8.2.2.1.Market size analysis, by Type

8.2.2.2.Market size analysis, by Technology

8.2.2.3.Market size analysis, by end-user

8.2.3.France

8.2.3.1.Market size analysis, by Type

8.2.3.2.Market size analysis, by Technology

8.2.3.3.Market size analysis, by end-user

8.2.4.Spain

8.2.4.1.Market size analysis, by Type

8.2.4.2.Market size analysis, by Technology

8.2.4.3.Market size analysis, by end-user

8.2.5.Italy

8.2.5.1.Market size analysis, by Type

8.2.5.2.Market size analysis, by Technology

8.2.5.3.Market size analysis, by end-user

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Type

8.2.6.2.Market size analysis, by Technology

8.2.6.3.Market size analysis, by end-user

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Type

8.3.1.2.Market size analysis, by Technology

8.3.1.3.Market size analysis, by end-user

8.3.2.Japan

8.3.2.1.Market size analysis, by Type

8.3.2.2.Market size analysis, by Technology

8.3.2.3.Market size analysis, by end-user

8.3.3.India

8.3.3.1.Market size analysis, by Type

8.3.3.2.Market size analysis, by Technology

8.3.3.3.Market size analysis, by end-user

8.3.4.Australia

8.3.4.1.Market size analysis, by Type

8.3.4.2.Market size analysis, by Technology

8.3.4.3.Market size analysis, by end-user

8.3.5.South Korea

8.3.5.1.Market size analysis, by Type

8.3.5.2.Market size analysis, by Technology

8.3.5.3.Market size analysis, by end-user

8.3.6.Rest of Asia Pacific

8.3.6.1.Market size analysis, by Type

8.3.6.2.Market size analysis, by Technology

8.3.6.3.Market size analysis, by end-user

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Type

8.4.1.2.Market size analysis, by Technology

8.4.1.3.Market size analysis, by end-user

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Type

8.4.2.2.Market size analysis, by Technology

8.4.2.3.Market size analysis, by end-user

8.4.3.UAE

8.4.3.1.Market size analysis, by Type

8.4.3.2.Market size analysis, by Technology

8.4.3.3.Market size analysis, by end-user

8.4.4.South Africa

8.4.4.1.Market size analysis, by Type

8.4.4.2.Market size analysis, by Technology

8.4.4.3.Market size analysis, by end-user

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Type

8.4.5.2.Market size analysis, by Technology

8.4.5.3.Market size analysis, by end-user

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Schneider Electric

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Siemens

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.ABB

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Honeywell

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Robert Bosch GmbH

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Emersion Electric Company

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.Rockwell Automation

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.SICK AG

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.NXP semiconductors

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.Texas Instruments

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

11.Appendix

11.1.Parent & peer market analysis

11.2.Premium insights from industry experts

11.3.Related reports

Fluid sensor is an equipment that analyzes and regulates the flow of liquids and gases present in pipes or tubes. Flow sensors are usually connected to gauges, but they can also be connected to computers and other digital appliances. Fluid sensors can not only detect clogs, leaks, pipe bursts but also fluctuations in liquid concentration which are caused due to the increase in pollution levels or contamination.

COVID-19 Impact on the Market

The outbreak of COVID-19 has had an adverse impact on the global fluid sensors market due to the prolonged lockdowns in various countries around the world during the pandemic. The lockdowns led to the closure of industries and factories, resulting in irregular flow and disruptions in the production & transport procedures. Stringent travel restrictions imposed by the government curbed the import and export of raw materials required to make the fluid sensors, leading to its decreased demand. Thus, the pandemic has had a negative impact on the growth of the market.

Recent Trends and Developments of the Fluid Sensors Market

The key companies operating in the industry are adopting various growth strategies & business tactics such as partnerships, collaborations, mergers & acquisitions, and launches to maintain a robust position in the overall market, which is subsequently helping the global fluid sensors market to grow exponentially.

For instance, in June 2019, Rochester Gauges, a dominant leader in design and manufacturing of liquid level gauges and sensors acquired FPI Sensors, a Minneapolis-based sensor manufacturing company that measures liquid levels, so as to expand Rochester’s market share in the liquid level sensor space.

In March 2020, TE Connectivity, an American Swiss-domiciled technology company acquired First Sensor, an innovative sensor technology company by holding its 71.87% shares, in order to maximize TE Connectivity’s presence in the fluid sensor market.

In April 2020, Sensiron, the world’s leading manufacturer of flow and environmental sensors, added a new product to its offering in the SLF3x series called, “SLF3S-0600F liquid flow sensor.” This sensor significantly helps in measuring low flow rates bidirectionally up to ±3000 µl/min, making it exemplary for applications in diagnostics and life sciences.

Forecast Analysis of the Global Fluid Sensors Market

The global fluid sensors market is expected to witness a noteworthy growth during the forecast period (2022-2030), owing to the increasing knowledge and emphasis on industrial automation among people. In addition, new features and enhancements in fluid sensors like optical sensing, ultrasonic sensors, capacitance sensing, etc. are expected to drive the growth of the market during the forecast period. But extortionate initial investments required for the fluid sensor technology is expected to restrain the growth of the market in the coming years. However, persistent technological advancements in the fluid sensor technology and increasing prevalence of industrial internet of things (IIOT) are expected to create enormous opportunities for the growth of the fluid sensors market in the analysis period.

According to the report published by Research Dive, the global fluid sensors market is expected to generate a revenue of $25,388.9 million by 2030, growing exponentially at a CAGR of 7.45% during the forecast period. The major players of the market include Schneider Electric, ABB, Siemens, Honeywell, Emersion Electric Company, Robert Bosch GmbH, SICK AG, Texas Instruments, NXP Semiconductors, and Rockwell Automation.

Most Profitable Region

The Asia-Pacific region is expected to have the highest market share, and hence is expected to dominate the market. The Asia-Pacific fluid sensors market is expected to garner a revenue of $9,350.7 million during the forecast period, owing to the rising rate of industrial production in the region. In addition, surging economic development and subsequent development in the industrial infrastructure in this region is further expected to bolster the growth of the Asia Pacific market during the forecast period.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com