Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

IC20115055 |

Pages: 229 |

Apr 2021 |

The global mobile value-added services market was valued at $479.0 billion in 2019, and is projected to reach $1,464.1 billion by 2027, at a CAGR of 15.3%.

Increase in the usage of mobile applications and mobile web is one of the major factors driving the growth of the mobile value-added services market. Increase in the usage of social networking applications and adoption of mobile payments is helping support the mobile value-added services market size.

Lack of guidelines and regulatory framework for the various market players of mobile value-added services (MVAS) that are accountable for consumer rights, data privacy and legal liabilities may limit the users and might restrict them from using mobile value-added services.

Asia-Pacific was the highest revenue contributor, accounting for $153.9 billion in 2019 and is estimated to grow with a CAGR of 14.90%.

Valued-added services are referred to as non-core services offered in a telecom industry. Mobile value-added service is a feature that can be added to a core product, offered by mobile operators through third-party mobile service providers as well as on their own apart from voice communication services. For instance, text messages, missed call alerts, call forwarding, call block are considered as mobile value-added services and are added to enhance the user experience.

The coronavirus pandemic has unleashed a series of unprecedented events affecting every industry. With the continuing spread of the novel coronavirus pandemic, organizations across the globe are gradually flattening their recessionary curve by leveraging technology. Many businesses will go through response, recovery and renew phases. Building business resilience and enabling agility will aid organizations to move forward in their journey out of the COVID-19 crisis towards the next normal. The mobile value-added services (VAS) market is predicted to witness a positive impact during the forecast period owing to the widespread growth of the COVID-19 pandemic. For instance, stay-at-home orders have introduced many people to apps that enable them to order takeout food or groceries online, and when they do go to the store, more people are choosing to pay with their phones instead of touching cash or credit cards. Moreover, the mobile value-added services like video calling services have also increased as a result of the contactless measures undertaken by the government bodies to minimize the spread of coronavirus.

Increase in the usage of mobile applications and mobile web is one of the major factors driving the growth of the mobile value-added services market. Increase in the social networking applications and mobile payments is helping support the mobile value-added services market size. Rising demand for entertainment services on mobile software’s is also a key-trend being witnessed in the mobile value-added services market, thereby resulting in the growth of online video content, live TV shows & events and localized vernacular content.

To know more about global mobile value-added services market drivers, get in touch with our analysts here.

Lack of guidelines and regulatory framework for various market players of mobile value-added services (MVAS) may limit the users and restrict them from using mobile value-added services. With the increase in technological advancements and new innovations, it is important to safeguard the data and information of value-added service users. Lack of privacy is the key challenge faced by mobile value-added service market. Furthermore, lack of government initiatives and limited ways of consumer authentications for the services that involve exchange of sensitive information such as payments may also limit the market’s growth.

Mobile value-added services are the additional features provided by the service operators at a premium to their customers along with other voice communication services. Increase in the usage of mobiles, smartphones and tablets along with the rollout of technologies like 4G and 5G network services in the market has created significant opportunities for the mobile value-added service providers. Moreover, the recent COVID-19 pandemic has accelerated digitization and remote activities and is further expected to provide plenty of opportunities for value-added services. In addition to this, rising demand for entertainment services on mobile handsets is also a key trend being witnessed in the market, thereby resulting into the development of key opportunities in on-demand music & video content, live TV shows & events and localized vernacular content.

Source: Research Dive Analysis

Short messaging services is expected to hold a significant market share in the forecast period. The short messaging service (SMS) sub-segment was the highest contributor to the market, with $94.1 billion in 2019, and is estimated to grow at a CAGR of 14.2% during the forecast period. The increased usage of short messaging services with the increased use of smartphones is rising the markets growth. Moreover, brands have increasingly found value in SMS marketing due to the fact that it earns higher open rates, engagement and click-through rates.

Source: Research Dive Analysis

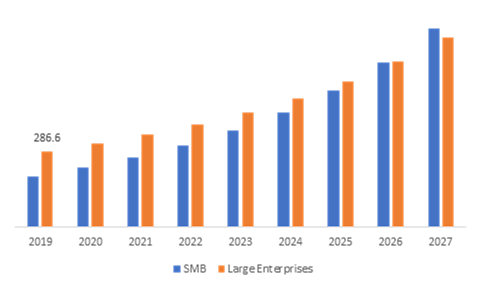

The large enterprises sub-segment was the highest contributor to the market, with $286.6 billion in 2019, and is estimated to grow at a CAGR of 12.4% during the forecast period. Due to the large-scale business economy, large companies are able to reduce the cost of business, while also maximizing their profit margins. This major advantage of large business economy is creating opportunities and paving the growth of the large enterprises.

Source: Research Dive Analysis

The government sub-segment was the highest contributor to the market, with $104.4 billion in 2019, and is estimated to grow at a CAGR of 14.0% during the forecast period. Increasing Internet services, advanced SMS services, and demand for high-end content from the consumers are predicated to boost the MVAS market growth in the near future. For instance, in India, the telecom players along with the government are investing in improving the infrastructure connectivity in rural regions to offer their services. In the urban region, MVAS players focus on providing additional VAS on mobile platforms due to the introduction of digital technologies.

Source: Research Dive Analysis

The Market for Mobile Value-Added Services in Asia-Pacific to be the Most Dominant

Asia-Pacific was the highest revenue contributor to the global market, accounting for $153.9 billion in 2019 and is estimated to reach $455.8 billion by 2027, with a CAGR of 14.9%. The increasing prevalence of smartphones in emerging economies such as China and India are driving the APAC MVAS market. Additionally, the reduced smartphone prices due to increased competition among manufacturers and service providers are further expected to expand the consumer base and thereby aid the mobile value-added services market. According to the India Brand Equity Foundation, India currently has the second-largest consumer base in the telecommunications market, with nearly 1.2 billion registered subscribers.

The Market for Mobile Value-Added Services in Europe to be the Fastest Growing

The market in Europe is the fastest growing, accounting for $124.9 billion in 2019 and estimated to reach $394.9 billion by 2027, at a significant CAGR of 15.8%. Europe is expected to be the fastest growing due to the increased internet penetration across the region. The European enterprise MVAS market is fairly evolved, combining technological innovation with demand forces that continue to facilitate the further expansion of services. The increasing penetration of long-term evolution (LTE) and smartphones, the adoption of MVAS platforms, IoT and connected devices and the emergence of FMC networks are the pivotal factors that will drive the growth of MVAS at enterprises over the coming years in Europe.

Source: Research Dive Analysis

Some of the significant mobile value-added service market players are Mozat, Apple Inc., Vodafone Group plc, Samsung Electronics Co. Ltd., Reliance Industries Ltd., Huawei Investment & Holding Co. Ltd., Onmobile Global Limited, Comviva Technologies, Alphabet Inc., and One97 Communication. Market players prefer inorganic growth strategies to expand into local markets. Mobile value-added service market players are emphasizing more on merger & acquisition and advanced product development. These are the frequent strategies followed by established organizations.

Porter’s Five Forces Analysis for Mobile Value-added Services Market:

| Aspect | Particulars |

| Historical Market Estimations | 2019-2020 |

| Base Year for Market Estimation | 2019 |

| Forecast timeline for Market Projection | 2020-2027 |

| Geographical Scope | North America, Europe, Asia-Pacific, LAMEA |

| Segmentation by Type |

|

| Segmentation by organization type |

|

| Segmentation by Vertical type |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.4.1.Assumptions

1.4.2.Forecast parameters

1.5.Data sources

1.5.1.Primary

1.5.2.Secondary

2.Executive Summary

2.1.360° summary

2.2.By Solution trends

2.3.By End-user trends

2.4.By vertical trends

3.Market overview

3.1.Market segmentation & definitions

3.2.Key takeaways

3.2.1.Top investment pockets

3.2.2.Top winning strategies

3.3.Porter’s five forces analysis

3.3.1.Bargaining power of consumers

3.3.2.Bargaining power of suppliers

3.3.3.Threat of new entrants

3.3.4.Threat of substitutes

3.3.5.Competitive rivalry in the market

3.4.Market dynamics

3.4.1.Drivers

3.4.2.Restraints

3.4.3.Opportunities

3.5.Technology landscape

3.6.Regulatory landscape

3.7.Patent landscape

3.8.Market value chain analysis

3.8.1.Stress point analysis

3.8.2.Raw material analysis

3.8.3.Manufacturing process

3.8.4.Distribution channel analysis

3.8.5.Operating vendors

3.8.5.1.Raw material suppliers

3.8.5.2.Product manufacturers

3.8.5.3.Product distributors

3.9.Strategic overview

4.Mobile Value-Added Services (MVAS) Market, by Solution

4.1.Short Messaging Services (SMS)

4.1.1.Market size and forecast, by region, 2019-2027

4.1.2.Comparative market share analysis, 2019 & 2027

4.2.Multimedia Messaging Services (MMS)

4.2.1.Market size and forecast, by region, 2019-2027

4.2.2.Comparative market share analysis, 2019 & 2027

4.3.Location Based Services

4.3.1.Market size and forecast, by region, 2019-2027

4.3.2.Comparative market share analysis, 2019 & 2027

4.4.Mobile Email & IM

4.4.1.Market size and forecast, by region, 2019-2027

4.4.2.Comparative market share analysis, 2019 & 2027

4.5.Mobile Money

4.5.1.Market size and forecast, by region, 2019-2027

4.5.2.Comparative market share analysis, 2019 & 2027

4.6.Mobile Advertising

4.6.1.Market size and forecast, by region, 2019-2027

4.6.2.Comparative market share analysis, 2019 & 2027

4.7.Mobile Infotainment

4.7.1.Market size and forecast, by region, 2019-2027

4.7.2.Comparative market share analysis, 2019 & 2027

4.8.Others

4.8.1.Market size and forecast, by region, 2019-2027

4.8.2.Comparative market share analysis, 2019 & 2027

5.Mobile Value-Added Services (MVAS) Market, by End-user

5.1.Small and Medium Enterprises

5.1.1.Market size and forecast, by region, 2019-2027

5.1.2.Comparative market share analysis, 2019 & 2027

5.2.Large Enterprises

5.2.1.Market size and forecast, by region, 2019-2027

5.2.2.Comparative market share analysis, 2019 & 2027

6.Mobile Value-Added Services (MVAS) Market, by Vertical

6.1.Media and Entertainment

6.1.1.Market size and forecast, by region, 2019-2027

6.1.2.Comparative market share analysis, 2019 & 2027

6.2.Healthcare

6.2.1.Market size and forecast, by region, 2019-2027

6.2.2.Comparative market share analysis, 2019 & 2027

6.3.Education

6.3.1.Market size and forecast, by region, 2019-2027

6.3.2.Comparative market share analysis, 2019 & 2027

6.4.Retail

6.4.1.Market size and forecast, by region, 2019-2027

6.4.2.Comparative market share analysis, 2019 & 2027

6.5.Government

6.5.1.Market size and forecast, by region, 2019-2027

6.5.2.Comparative market share analysis, 2019 & 2027

6.6.Telecom & IT

6.6.1.Market size and forecast, by region, 2019-2027

6.6.2.Comparative market share analysis, 2019 & 2027

6.7.Others

6.7.1.Market size and forecast, by region, 2019-2027

6.7.2.Comparative market share analysis, 2019 & 2027

6.8.North America

6.8.1.Market size and forecast, by Solution, 2019-2027

6.8.2.Market size and forecast, by End-user, 2019-2027

6.8.3.Market size and forecast, by Vertical, 2019-2027

6.8.4.Market size and forecast, by country, 2019-2027

6.8.5.Comparative market share analysis, 2019 & 2027

6.8.6.U.S.

6.8.6.1.Market size and forecast, by Solution, 2019-2027

6.8.6.2.Market size and forecast, by End-user, 2019-2027

6.8.6.3.Market size and forecast, by vertical, 2019-2027

6.8.6.4.Comparative market share analysis, 2019 & 2027

6.8.7.Canada

6.8.7.1.Market size and forecast, by Solution, 2019-2027

6.8.7.2.Market size and forecast, by End-user, 2019-2027

6.8.7.3.Market size and forecast, by vertical, 2019-2027

6.8.7.4.Comparative market share analysis, 2019 & 2027

6.8.8.Mexico

6.8.8.1.Market size and forecast, by Solution, 2019-2027

6.8.8.2.Market size and forecast, by End-user, 2019-2027

6.8.8.3.Market size and forecast, by vertical, 2019-2027

6.8.8.4.Comparative market share analysis, 2019 & 2027

6.9.Europe

6.9.1.Market size and forecast, by Solution, 2019-2027

6.9.2.Market size and forecast, by End-user, 2019-2027

6.9.3.Market size and forecast, by vertical, 2019-2027

6.9.4.Market size and forecast, by country, 2019-2027

6.9.5.Comparative market share analysis, 2019 & 2027

6.9.6.Germany

6.9.6.1.Market size and forecast, by Solution, 2019-2027

6.9.6.2.Market size and forecast, by End-user, 2019-2027

6.9.6.3.Market size and forecast, by vertical, 2019-2027

6.9.6.4.Comparative market share analysis, 2019 & 2027

6.9.7.UK

6.9.7.1.Market size and forecast, by Solution, 2019-2027

6.9.7.2.Market size and forecast, by End-user, 2019-2027

6.9.7.3.Market size and forecast, by vertical, 2019-2027

6.9.7.4.Comparative market share analysis, 2019 & 2027

6.9.8.France

6.9.8.1.Market size and forecast, by Solution, 2019-2027

6.9.8.2.Market size and forecast, by End-user, 2019-2027

6.9.8.3.Market size and forecast, by vertical, 2019-2027

6.9.8.4.Comparative market share analysis, 2019 & 2027

6.9.9.Spain

6.9.9.1.Market size and forecast, by Solution, 2019-2027

6.9.9.2.Market size and forecast, by End-user, 2019-2027

6.9.9.3.Market size and forecast, by vertical, 2019-2027

6.9.9.4.Comparative market share analysis, 2019 & 2027

6.9.10.Italy

6.9.10.1.Market size and forecast, by Solution, 2019-2027

6.9.10.2.Market size and forecast, by End-user, 2019-2027

6.9.10.3.Market size and forecast, by vertical, 2019-2027

6.9.10.4.Comparative market share analysis, 2019 & 2027

6.9.11.Rest of Europe

6.9.11.1.Market size and forecast, by Solution, 2019-2027

6.9.11.2.Market size and forecast, by End-user, 2019-2027

6.9.11.3.Market size and forecast, by vertical, 2019-2027

6.9.11.4.Comparative market share analysis, 2019 & 2027

6.10.Asia Pacific

6.10.1.Market size and forecast, by Solution, 2019-2027

6.10.2.Market size and forecast, by End-user, 2019-2027

6.10.3.Market size and forecast, by vertical, 2019-2027

6.10.4.Market size and forecast, by country, 2019-2027

6.10.5.Comparative market share analysis, 2019 & 2027

6.10.6.China

6.10.6.1.Market size and forecast, by Solution, 2019-2027

6.10.6.2.Market size and forecast, by End-user, 2019-2027

6.10.6.3.Market size and forecast, by vertical, 2019-2027

6.10.6.4.Comparative market share analysis, 2019 & 2027

6.10.7.India

6.10.7.1.Market size and forecast, by Solution, 2019-2027

6.10.7.2.Market size and forecast, by End-user, 2019-2027

6.10.7.3.Market size and forecast, by vertical, 2019-2027

6.10.7.4.Comparative market share analysis, 2019 & 2027

6.10.8.Japan

6.10.8.1.Market size and forecast, by Solution, 2019-2027

6.10.8.2.Market size and forecast, by End-user, 2019-2027

6.10.8.3.Market size and forecast, by vertical, 2019-2027

6.10.8.4.Comparative market share analysis, 2019 & 2027

6.10.9.Australia

6.10.9.1.Market size and forecast, by Solution, 2019-2027

6.10.9.2.Market size and forecast, by End-user, 2019-2027

6.10.9.3.Market size and forecast, by vertical, 2019-2027

6.10.9.4.Comparative market share analysis, 2019 & 2027

6.10.10.South Korea

6.10.10.1.Market size and forecast, by Solution, 2019-2027

6.10.10.2.Market size and forecast, by End-user, 2019-2027

6.10.10.3.Market size and forecast, by vertical, 2019-2027

6.10.10.4.Comparative market share analysis, 2019 & 2027

6.10.11.Rest of Asia Pacific

6.10.11.1.Market size and forecast, by Solution, 2019-2027

6.10.11.2.Market size and forecast, by End-user, 2019-2027

6.10.11.3.Market size and forecast, by vertical, 2019-2027

6.10.11.4.Comparative market share analysis, 2019 & 2027

6.11.LAMEA

6.11.1.Market size and forecast, by Solution, 2019-2027

6.11.2.Market size and forecast, by End-user, 2019-2027

6.11.3.Market size and forecast, by vertical, 2019-2027

6.11.4.Market size and forecast, by country, 2019-2027

6.11.5.Comparative market share analysis, 2019 & 2027

6.11.6.Latin America

6.11.6.1.Market size and forecast, by Solution, 2019-2027

6.11.6.2.Market size and forecast, by End-user, 2019-2027

6.11.6.3.Market size and forecast, by vertical, 2019-2027

6.11.6.4.Comparative market share analysis, 2019 & 2027

6.11.7.Middle East

6.11.7.1.Market size and forecast, by Solution, 2019-2027

6.11.7.2.Market size and forecast, by End-user, 2019-2027

6.11.7.3.Market size and forecast, by vertical, 2019-2027

6.11.7.4.Comparative market share analysis, 2019 & 2027

6.11.8.Africa

6.11.8.1.Market size and forecast, by Solution, 2019-2027

6.11.8.2.Market size and forecast, by End-user, 2019-2027

6.11.8.3.Market size and forecast, by vertical, 2019-2027

6.11.8.4.Comparative market share analysis, 2019 & 2027

7.Company profiles

7.1.Mozat

7.1.1.Business overview

7.1.2.Financial performance

7.1.3.Product portfolio

7.1.4.Recent strategic moves & developments

7.1.5.SWOT analysis

7.2.Apple Inc.

7.2.1.Business overview

7.2.2.Financial performance

7.2.3.Product portfolio

7.2.4.Recent strategic moves & developments

7.2.5.SWOT analysis

7.3.Vodafone Group plc

7.3.1.Business overview

7.3.2.Financial performance

7.3.3.Product portfolio

7.3.4.Recent strategic moves & developments

7.3.5.SWOT analysis

7.4.Samsung Electronics Co. Ltd.

7.4.1.Business overview

7.4.2.Financial performance

7.4.3.Product portfolio

7.4.4.Recent strategic moves & developments

7.4.5.SWOT analysis

7.5.Reliance Industries Ltd.

7.5.1.Business overview

7.5.2.Financial performance

7.5.3.Product portfolio

7.5.4.Recent strategic moves & developments

7.5.5.SWOT analysis

7.6.Huawei Investment & Holding Co. Ltd.

7.6.1.Business overview

7.6.2.Financial performance

7.6.3.Product portfolio

7.6.4.Recent strategic moves & developments

7.6.5.SWOT analysis

7.7.Onmobile Global Limited

7.7.1.Business overview

7.7.2.Financial performance

7.7.3.Product portfolio

7.7.4.Recent strategic moves & developments

7.7.5.SWOT analysis

7.8.Comviva Technologies

7.8.1.Business overview

7.8.2.Financial performance

7.8.3.Product portfolio

7.8.4.Recent strategic moves & developments

7.8.5.SWOT analysis

7.9.Alphabet Inc.

7.9.1.Business overview

7.9.2.Financial performance

7.9.3.Product portfolio

7.9.4.Recent strategic moves & developments

7.9.5.SWOT analysis

7.10.One97 Communication

7.10.1.Business overview

7.10.2.Financial performance

7.10.3.Product portfolio

7.10.4.Recent strategic moves & developments

7.10.5.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}