Autotransfusion Devices Market Report

RA00049

Autotransfusion Devices Market by Product Type (On-Pump Transfusion Devices, Off-Pump Transfusion Devices), by End Users (Ambulatory Surgical Centers, Hospitals, Emergency Rooms, Nursing Homes, and Others), Global Opportunity Analysis and Industry Forecast, 2019–2027

Auto-transfusion Device Market Overview and Forecast 2027:

The global autotransfusion device market size was valued at $1,121.5 million in 2018 and is projected to reach $1,939.7 million by 2027, registering a CAGR of 6.5% from 2019 to 2027. North America accounted for the highest share in 2018 and is anticipated to maintain its lead in the global autotransfusion device market throughout the forecast period.

An autotransfusion device is a mechanical device that is used in the process of collecting and re-infusing blood lost from hemorrhage. Different forms of autotransfusion devices include intra-operative, emergency, or post-operative salvage devices and hemodilution devices used to re-infuse a patient's own blood. Autotransfusion devices market is growing because of growing prevalence of orthopedics and cardiac surgery. Furthermore, as autotransfusion devices is continually witnessing innovation is boosting the growth of autotransfusion device market globally.

Driving Factors in Autotransfusion Devices Market:

The factor that contribute toward growth of the global autotransfusion device market include high occurrence of cardiac devices contribute to the growth of autotransfusion device market globally. Furthermore, absence of any risk of transfusion or transmitted devices is a major factor that fuels the growth of the autotransfusion devices market. Moreover, absence of risk of alloimunization to blood cell boosts the growth of the autotransfusion devices market. However, inability to separate contaminations from blood cell is anticipated to hinder the growth of the autotransfusion Devices market. Conversely, growing adoption of full body transfusion devices is expected to offer lucrative opportunities during the forecast period.

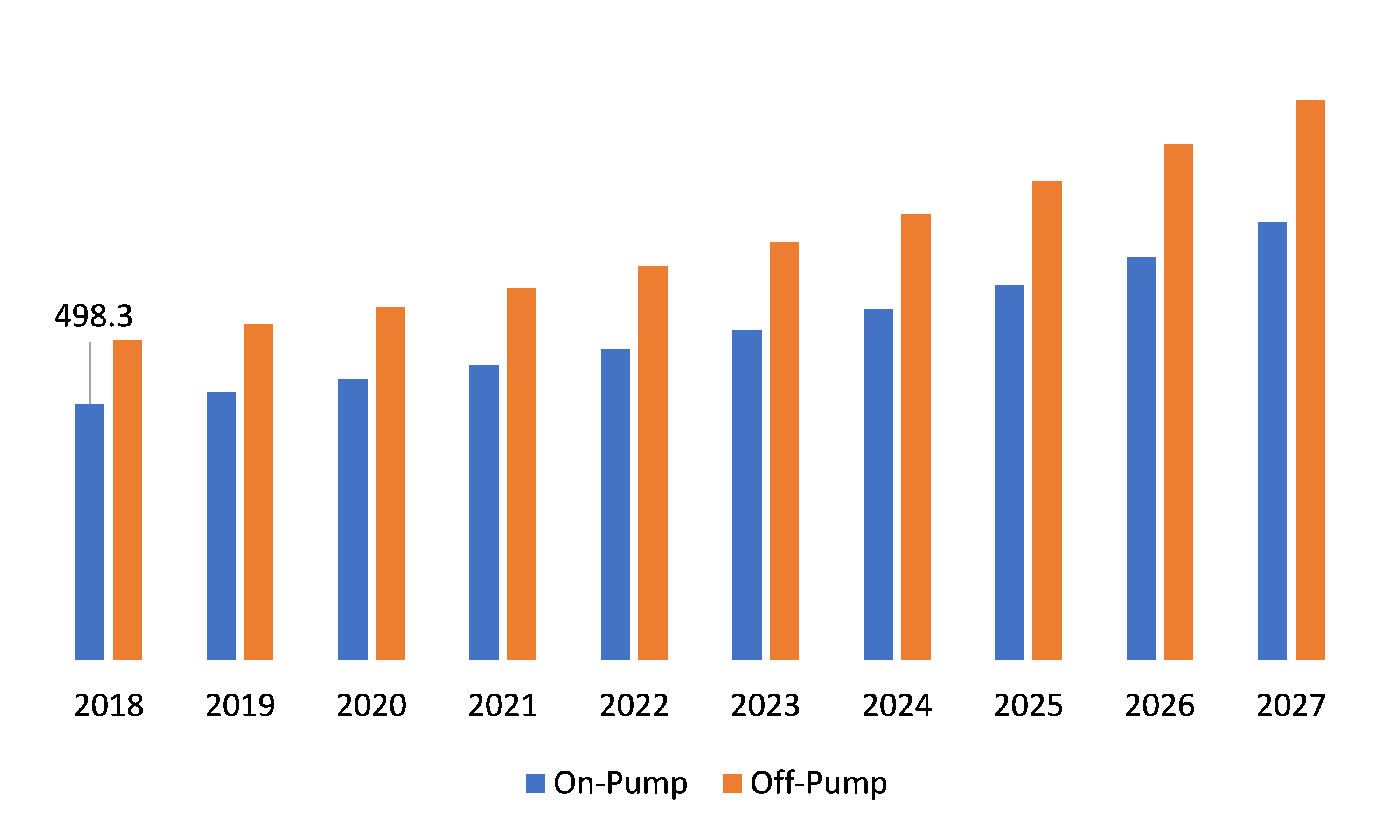

Global Autotransfusion Device Market, by Product Type

Source: Research Dive Analysis

Depending on product type the market is divided into on pump transfusion devices and off pump transfusion devices. Off pump transfusion devices has the highest market share and is expected to grow with the a CAGR of 6.6% during the forecast period owing to ease in use coupled with the fact that there’s no loss of blood during transfusion and it is considered safer than the conventional method.

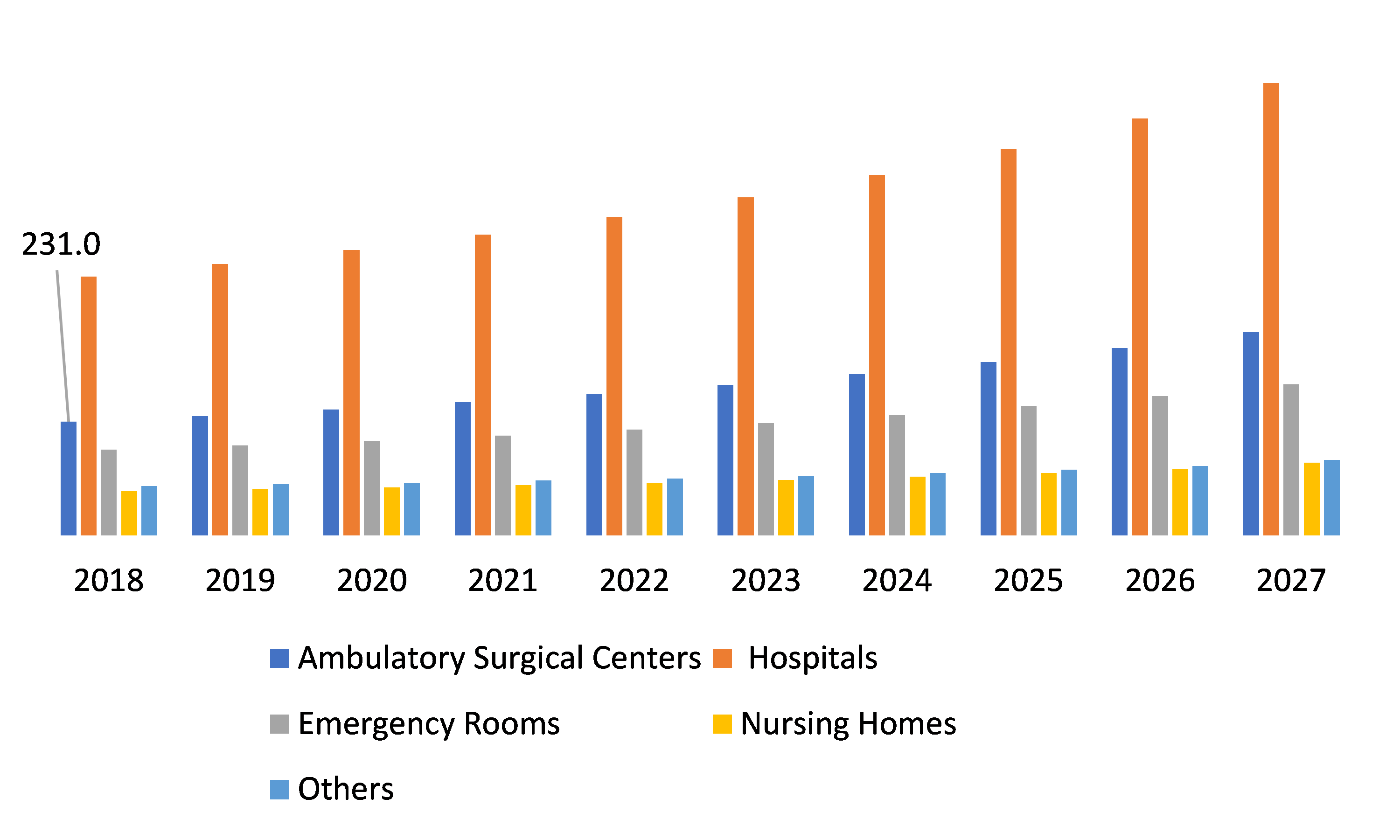

Global Autotransfusion Device Market, by End-User

Source: Research Dive Analysis

By End User, autotransfusion device market is categorized into Ambulatory Surgical Centers, Hospitals, Emergency Rooms, Nursing Homes, and others. Hospital segment contributes the most among the end user segment. This is driven by the fact that hospitals have various specialized departments wherein blood transfusion is required as such the autotransfusion devices are required in multiple numbers to cater to various transfusion requirements of specialized symptoms coupled with the Guidelines set by the American Association of Blood Banks, the blood should be re-infused within 4 hours for washing is driving the growth of autotransfusion devices globally.

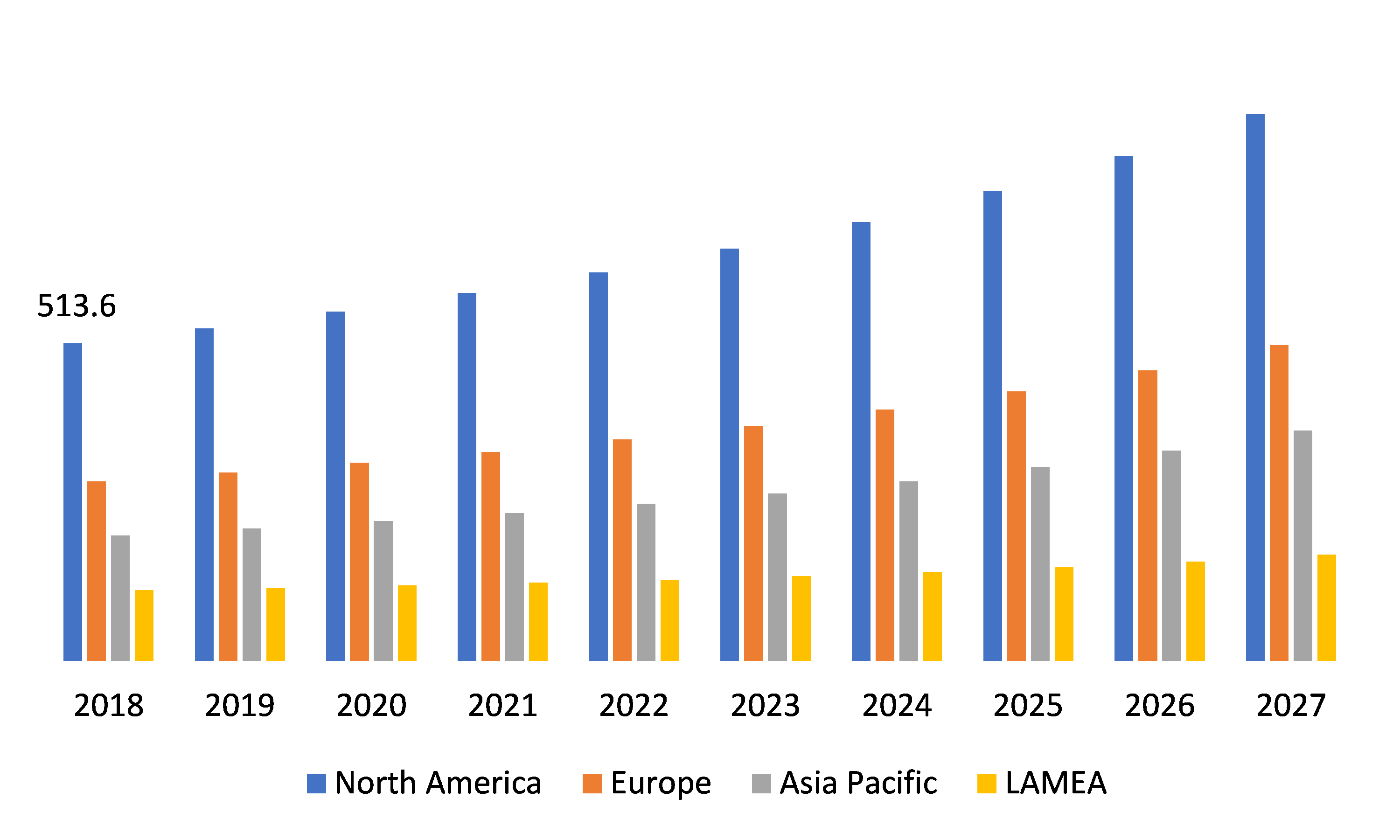

Regional Growth of Global Autotransfusion Device Market

Source: Research Dive Analysis

Geographically, the global market is segmented into North America, Europe, Asia-Pacific, and LAMEA.

North America Autotransfusion Device Market Overview:

North American market is projected to reach $884.4 million by 2026, increasing at a CAGR of 6.4%, followed by the Europe market.

Top Key Players in Global Autotransfusion Device Market:

Some of the autotransfusion device companies include Medtronic Plc, Becton Dickinson and Company, Zimmer Biomet Holding, Teleflex Incorporated, LivaNova, Plc, Fresenius Medical Care AG & Co. KGaA, Stryker Corporation, Haemonetics Corporation, Terumo Corporation and Getinge AB. To gain competitive advantage the companies are looking to increase their reach through acquisitions. For example –October 2019, Medtronics Acquired AV Medical Technologies that operates as a medical devices company. Similarly, Getinge acquired Applikon Biotechnology, A world leader in developing and supplying advanced bioreactor systems from laboratory scale to production scale in December 2019.

Global Autotransfusion Device Market Trends

High Occurrence of Cardiac Diseases Leads to the Huge Demand of Auto-Transfusion devices across the world

With the improvement of medical technology and the growing discrepancy between blood supply and demand, autologous blood transfusion (ABT) has attracted more attention in recent years; its safety and effectiveness has gradually become a subject of interest. ABT can avoid the serious harm caused by allogeneic blood transfusion, alleviate blood shortage and save blood resources, while lightening the burden of patients. Therefore, ABT has gained more attention, has become a common demand in clinical practice, and is becoming widely used clinically. Increased adoption of technologically advanced autotransfusion devices is stimulating the growth of autotransfusion devices market.

Absence of any risk of transfusion & transmitted infections

The risk of transmission of infectious diseases (hepatitis, malaria, AIDS etc.) is eliminated; there is no danger of isosensitization; autologous blood ensures a better oxygen transfer and higher activity of coagulation factors; pretransfusion examinations are eliminated; there is no need to postpone the operation for shortage of blood; the consumption of homologous blood is reduced; economy; religious objections against transfusion of homologous blood are eliminated. There are no disadvantages of autotransfusion. Blood for autotransfusion was collected from patients before a planned operation; multiple times two consecutive blood collections were made. No complication threatening the patient's health was encountered.

The exceptional increase in popularity of autotransfusion has certainly been due to the worldwide explosion of the AIDS pandemics, and to the diffusion within the general public of new critical appreciation of all medical procedures, and of blood transfusion in particular.

Inability to Separate Contaminants from Blood is Expected To Be A Major Restraint for Autotransfusion Devices Market

A major disadvantage is the inability of these machines to separate contaminants from blood without the removal and discard of blood elements other than the red blood cells. The beneficial blood elements which are removed include platelets and proteins, such as the clotting factors and albumin. The removal of these components from blood can be responsible for a dilutional coagulopathy when blood loss is high. Thus, this can act as a restraint to the growth of autotransfusion devices.

Expensive Autotransfusion System

Another significant disadvantage to such systems is the cost. The hardware required to process the blood is complicated and can cost $40,000 or more. The disposable software is also not inexpensive. Additionally, a trained, dedicated technician is required to run the equipment. Maintaining availability of autotransfusion with processing during second and third shift and weekends can be a serious scheduling problem. These drawbacks have caused a number of doctors to explore alternatives to cell processing. These clinicians point out that the need to centrifuge has not been proven and, when the blood is not contaminated, many consider processing to be a costly and often unnecessary step that removes beneficial elements

Growing Adoption of whole body autotransfusion devices

The benefits of whole blood intraoperative autotransfusion are numerous. The patient benefits because platelets and proteins, such as albumin and clotting factors are returned along with the oxygen carrying red blood cells. There is no delay in returning the blood to the patient due to a time consuming processing step. Moreover, a scheduling system for cell processors is not needed because whole blood systems are immediately available and time for setup is minimal. Such clear benefits to the patient and hospitals have created significant recent interest in whole blood autotransfusion. Thus, this is expected to be creating opportunity for the growth of Autotransfusion devices as autotransfusion are now used for whole body transfusion enabling reduction in time and cost.

Q1. What is Autotransfusion Devices?

A. Autotransfusion is a process where a person receives their own blood for transfusion process, instead of separate donor or banked allogenic. Thus devices used for this purpose are known as autotransfusion devices.

Q2. What does Autotransfusion Device do?

A. Autotransfusion device are used in autotransfusion process that includes centrifugation, aspiration, anticoagulation, reinfusion, and washing process in a cardiac patient. Moreover, it is used for concentrating the pump perfusate at the termination of cardiopulmonary bypass (CPB).

Q3. Which product type are expected to have highest growth rate in the Autotransfusion Device Market?

A. Autotransfusion device that is used for cardiac surgeries are anticipated to have highest growth in the market.

Q4. What are the key factors that drive the Autotransfusion Device Market?

A. Rising prevalence about cardiac diseases and increasing preference among people for auto-transfusion technique over allogeneic technique.

Q5. What will be the market value of Autotransfusion Device Market in the next Years?

A. The global autotransfusion device market is predicted to contribute a revenue of $1,660.9 million by 2025.

Q6. What are the emerging trends in Autotransfusion Device Market?

A. Recent development in autotransfusion devices such as Haemonetics Elite, LivaNova XTRA, and Fresenius CATSmart offers advantages such as continuous autotransfusion ability, contains single volume separation centre, auto-start function, hematocrit sensors, and available in different bowl sizes such as 55, 125, 175, and 225cc.

1. Research Methodology

1.1. Desk Research

1.2. Real time insights and validation

1.3. Forecast model

1.4. Assumptions and forecast parameters

1.4.1. Assumptions

1.4.2. Forecast parameters

1.5. Data sources

1.5.1. Primary

1.5.2. Secondary

2. Executive Summary

2.1. 360° summary

2.2. Product Type

2.3. End-User

3. Market overview

3.1. Market segmentation & definitions

3.2. Key takeaways

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.3. Porter’s five forces analysis

3.3.1. Bargaining power of consumers

3.3.2. Bargaining power of suppliers

3.3.3. Threat of new entrants

3.3.4. Threat of substitutes

3.3.5. Competitive rivalry in the market

3.4. Market dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Technology landscape

3.6. Regulatory landscape

3.7. Patent landscape

3.8. Market value chain analysis

3.8.1. Stress point analysis

3.9. Strategic overview

4. Autotransfusion Device Market, by Product Type

4.1. On-Pump

4.1.1. Market size and forecast, by region, 2016-2026

4.1.2. Comparative market share analysis, 2018 & 2027

4.2. Off-Pump

4.2.1. Market size and forecast, by region, 2016-2026

4.2.2. Comparative market share analysis, 2018 & 2027

5. Autotransfusion Device Market, by End-User

5.1. Ambulatory Surgical Centers

5.1.1. Market size and forecast, by region, 2016-2026

5.1.2. Comparative market share analysis, 2018 & 2027

5.2. Hospitals

5.2.1. Market size and forecast, by region, 2016-2026

5.2.2. Comparative market share analysis, 2018 & 2027

5.3. Emergency Rooms

5.3.1. Market size and forecast, by region, 2016-2026

5.3.2. Comparative market share analysis, 2018 & 2027

5.4. Nursing Homes

5.4.1. Market size and forecast, by region, 2016-2026

5.4.2. Comparative market share analysis, 2018 & 2027

5.5. Others

5.5.1. Market size and forecast, by region, 2016-2026

5.5.2. Comparative market share analysis, 2018 & 2027

6. Autotransfusion Device Market, by Region

6.1. North America

6.1.1. Market size and forecast, by product type, 2018-2027

6.1.2. Market size and forecast, by end-users, 2018-2027

6.1.3. Market size and forecast, by country, 2016-2026

6.1.4. Comparative market share analysis, 2018 & 2027

6.1.5. U.S.

6.1.5.1. Market size and forecast, by product type, 2018-2027

6.1.5.2. Market size and forecast, by end-users, 2018-2027

6.1.5.3. Comparative market share analysis, 2018 & 2027

6.1.6. Canada

6.1.6.1. Market size and forecast, by product type, 2018-2027

6.1.6.2. Market size and forecast, by end-users, 2018-2027

6.1.6.3. Comparative market share analysis, 2018 & 2027

6.1.7. Mexico

6.1.7.1. Market size and forecast, by product type, 2018-2027

6.1.7.2. Market size and forecast, by end-users, 2018-2027

6.1.7.3. Comparative market share analysis, 2018 & 2027

6.2. Europe

6.2.1. Market size and forecast, by product type, 2018-2027

6.2.2. Market size and forecast, by end-users, 2018-2027

6.2.3. Market size and forecast, by country, 2016-2026

6.2.4. Comparative market share analysis, 2018 & 2027

6.2.5. Germany

6.2.5.1. Market size and forecast, by product type, 2018-2027

6.2.5.2. Market size and forecast, by end-users, 2018-2027

6.2.5.3. Comparative market share analysis, 2018 & 2027

6.2.6. UK

6.2.6.1. Market size and forecast, by product type, 2018-2027

6.2.6.2. Market size and forecast, by end-users, 2018-2027

6.2.6.3. Comparative market share analysis, 2018 & 2027

6.2.7. France

6.2.7.1. Market size and forecast, by product type, 2018-2027

6.2.7.2. Market size and forecast, by end-users, 2018-2027

6.2.7.3. Comparative market share analysis, 2018 & 2027

6.2.8. Russia

6.2.8.1. Market size and forecast, by product type, 2018-2027

6.2.8.2. Market size and forecast, by end-users, 2018-2027

6.2.8.3. Comparative market share analysis, 2018 & 2027

6.2.9. Italy

6.2.9.1. Market size and forecast, by product type, 2018-2027

6.2.9.2. Market size and forecast, by end-users, 2018-2027

6.2.9.3. Comparative market share analysis, 2018 & 2027

6.2.10. Rest of the Europe

6.2.10.1. Market size and forecast, by product type, 2018-2027

6.2.10.2. Market size and forecast, by end-users, 2018-2027

6.2.10.3. Comparative market share analysis, 2018 & 2027

6.3. Asia-Pacific

6.3.1. Market size and forecast, by product type, 2018-2027

6.3.2. Market size and forecast, by end-users, 2018-2027

6.3.3. Market size and forecast, by country, 2016-2026

6.3.4. Comparative market share analysis, 2018 & 2027

6.3.5. China

6.3.5.1. Market size and forecast, by product type, 2018-2027

6.3.5.2. Market size and forecast, by end-users, 2018-2027

6.3.5.3. Comparative market share analysis, 2018 & 2027

6.3.6. India

6.3.6.1. Market size and forecast, by product type, 2018-2027

6.3.6.2. Market size and forecast, by end-users, 2018-2027

6.3.6.3. Comparative market share analysis, 2018 & 2027

6.3.7. Japan

6.3.7.1. Market size and forecast, by product type, 2018-2027

6.3.7.2. Market size and forecast, by end-users, 2018-2027

6.3.7.3. Comparative market share analysis, 2018 & 2027

6.3.8. South Korea

6.3.8.1. Market size and forecast, by product type, 2018-2027

6.3.8.2. Market size and forecast, by end-users, 2018-2027

6.3.8.3. Comparative market share analysis, 2018 & 2027

6.3.9. Rest of the Asia Pacific

6.3.9.1. Market size and forecast, by product type, 2018-2027

6.3.9.2. Market size and forecast, by end-users, 2018-2027

6.3.9.3. Comparative market share analysis, 2018 & 2027

6.4. LAMEA

6.4.1. Market size and forecast, by product type, 2018-2027

6.4.2. Market size and forecast, by end-users, 2018-2027

6.4.3. Market size and forecast, by country, 2016-2026

6.4.4. Comparative market share analysis, 2018 & 2027

6.4.5. Latin America

6.4.5.1. Market size and forecast, by product type, 2018-2027

6.4.5.2. Market size and forecast, by end-users, 2018-2027

6.4.5.3. Comparative market share analysis, 2018 & 2027

6.4.6. Middle East

6.4.6.1. Market size and forecast, by product type, 2018-2027

6.4.6.2. Market size and forecast, by end-users, 2018-2027

6.4.6.3. Comparative market share analysis, 2018 & 2027

6.4.7. Africa

6.4.7.1. Market size and forecast, by product type, 2018-2027

6.4.7.2. Market size and forecast, by end-users, 2018-2027

6.4.7.3. Comparative market share analysis, 2018 & 2027

7. Company profiles

7.1. Medtronic Plc

7.1.1. Business overview

7.1.2. Financial performance

7.1.3. Product portfolio

7.1.4. Recent strategic moves & developments

7.1.5. SWOT analysis

7.2. Becton Dickinson and Company

7.2.1. Business overview

7.2.2. Financial performance

7.2.3. Product portfolio

7.2.4. Recent strategic moves & developments

7.2.5. SWOT analysis

7.3. Zimmer Biomet Holding

7.3.1. Business overview

7.3.2. Financial performance

7.3.3. Product portfolio

7.3.4. Recent strategic moves & developments

7.3.5. SWOT analysis

7.4. Teleflex Incorporated

7.4.1. Business overview

7.4.2. Financial performance

7.4.3. Product portfolio

7.4.4. Recent strategic moves & developments

7.4.5. SWOT analysis

7.5. LivaNova, Plc

7.5.1. Business overview

7.5.2. Financial performance

7.5.3. Product portfolio

7.5.4. Recent strategic moves & developments

7.5.5. SWOT analysis

7.6. Fresenius Medical Care AG & Co. KGaA

7.6.1. Business overview

7.6.2. Financial performance

7.6.3. Product portfolio

7.6.4. Recent strategic moves & developments

7.6.5. SWOT analysis

7.7. Stryker Corporation

7.7.1. Business overview

7.7.2. Financial performance

7.7.3. Product portfolio

7.7.4. Recent strategic moves & developments

7.7.5. SWOT analysis

7.8. Haemonetics Corporation

7.8.1. Business overview

7.8.2. Financial performance

7.8.3. Product portfolio

7.8.4. Recent strategic moves & developments

7.8.5. SWOT analysis

7.9. Terumo Corporation

7.9.1. Business overview

7.9.2. Financial performance

7.9.3. Product portfolio

7.9.4. Recent strategic moves & developments

7.9.5. SWOT analysis

7.10. Getinge AB

7.10.1. Business overview

7.10.2. Financial performance

7.10.3. Product portfolio

7.10.4. Recent strategic moves & developments

7.10.5. SWOT analysis

There are several reasons a person might need to undergo blood transfusion treatment. It may be a severe liver infection that affects the person’s capacity of producing blood or an infection that causes anemia, such as kidney disorder or cancer. Moreover, in cases of accident, a person might experience serious internal bleeding which requires substituting the lost blood with fresh donor blood, but this is not always possible. In urban locations or the areas that have an absence of healthcare services, donor blood may not be available always.

Replacement for blood transfusion

To tackle all these issues, scientists and doctors have invented an innovative technique called autotransfusion—which can be used as a substitute for the traditional blood transfusion method. Autotransfusion of blood is a process in which a person gives his/her blood for transfusion, rather than taking it from banked allogenic blood. Using this technique, the blood in the body cavity of a patient, postoperatively drained blood, or blood lost during a surgical procedure can be recovered by means of a blood recovery instrument called as autotransfusion device. The guidelines by the American Association of Blood Banks indicate that intraoperative or postoperative autotransfusion should be done in surgical treatments which involves excessive bleeding (more than 20% total volume). In intraoperative autotransfusion, the lost blood is recovered in an extracorporeal circuit during surgery. Whereas, in postoperative autotransfusion, the lost blood is recovered in the extracorporeal circuit at the end of surgery or from aspirated drainage.

Benefits and uses of autotransfusion devices

Generally, an autotransfusion device is used in cases wherein the body loses one or more units of blood and can be most beneficial in cases that involve risk of transmission of infectious disease, rare blood groups, limited homologous blood supply or other medical conditions for which the usage of homologous blood is contraindicated. A major drawback of this device is its cost. The hardware that is used for processing the blood is complex and can charge around $40,000 or more. The disposable software is also expensive and a qualified, dedicated operator is required to run this device. Sustaining the availability of autotransfusion services especially during second and third shifts and weekends is a major problem associated with this technique.

Nowadays, the rising inconsistency between blood supply and demand has led to the growing popularity and adoption of autologous blood transfusion (ABT). Also, the increased safety and efficiency offered by this technique is resulting in its increased usage all across the world. This process avoids the risks caused by allogeneic blood transfusion, lessens blood shortage, saves blood resources, and eases the burden of patients. Hence, the demand for ABT in clinical practice is increasing day by day, and gaining more importance all over the world.

Additionally, the use of autotransfusion devices eliminates the risk of transmission of infectious diseases such as hepatitis, malaria, AIDS etc. Also, with this technique, there is no danger of isosensitization. Furthermore, autologous blood guarantees a better oxygen transfer, enhanced activities of coagulation factors, elimination of pretransfusion inspections, eradicates blood shortage problems and reduces the use of homologous blood.

Apart from this, autotransfusion devices are used in various application areas including Ambulatory surgical centers, Hospitals, Emergency Centers, Nursing Homes, and other healthcare service centers. Hence, the growing usage of such advanced autotransfusion techniques is expected to fuel the growth of the autotransfusion devices industry in the near future.

Growing adoption of auto-transfusion devices

Currently, many surgeons are using autotransfusion with a cell processing step. Cell processing systems use a vacuum to aspirate blood from the surgical site to a cardiotomy reservoir. The blood is mixed with citrate or heparin while it is being collected in order to avoid coagulation. The anticoagulated blood is then mixed with saline solution and centrifuged at about 4800 rpm. This procedure eliminates almost 90% of the supernatant hemoglobin, citrate, heparin, activated complement, and proteins such as albumin and clotting factors. The final washed red blood cell product has a hematocrit of 55-60%.

There are numerous advantages of whole blood intraoperative autotransfusion. This process recovers platelets and proteins, such as albumin and clotting factors with the oxygen-carrying red blood cells. Furthermore, the process does not require a scheduling system for cell processors as the entire blood system is instantly available and time required for arranging the entire system is minimal. Due to these factors, the demand for autotransfusion devices from patients and hospitals in increasing significantly. Therefore, it is expected that the autotransfusion device market will show a substantial growth in the upcoming years. Also, a report by Research Dive has stated that the global market for autotransfusion devices will generate a revenue of $1,939.7 million by 2027, growing at a CAGR of 6.5% from 2019 to 2027.

Growing investments for the development of autotransfusion devices

Several major companies in Autotransfusion Device are greatly investing in R&D for attaining competitive advantage over their competitors. For instance—in 2019, BD (Becton, Dickinson and Company), a worldwide leader in medical technology, declared its recent development in Combating Antimicrobial Resistance (AMR) with new analytics combined into the company’s connected medication management platform that recognizes when a potentially ineffective and inappropriate antibiotic gets prescribed, depending on the detailed diagnosis of patient’s infection.

Apart from this company, there are several other companies in the autotransfusion market which are making efforts to grow their business through strategic collaborations, partnerships, new product developments, and acquisitions. Some of these companies include Becton Dickinson and Company, Medtronic Plc, Zimmer Biomet Holding, LivaNova, Plc, Fresenius Medical Care AG & Co. KGaA, Terumo Corporation, Stryker Corporation, Haemonetics Corporation, Teleflex Incorporated, and Getinge AB. In October 2019, Medtronics PLC, headquartered in Dublin acquired AV Medical Technologies which is an Israeli medical technology company. Hence, looking at the activities of several market players in this market it is clear that the autotransfusion devices market will observe substantial growth in the near future.

Personalize this research

- Triangulate with your own data

- Request your format and definition

- Get a deeper dive on a specific application, geography, customer or competitor

- + 1-888-961-4454 Toll - Free

- support@researchdive.com