Toll Free : + 1-888-961-4454 | Int'l : + 91 (788) 802-9103 | support@researchdive.com

AU20112946 |

Pages: 250 |

Feb 2023 |

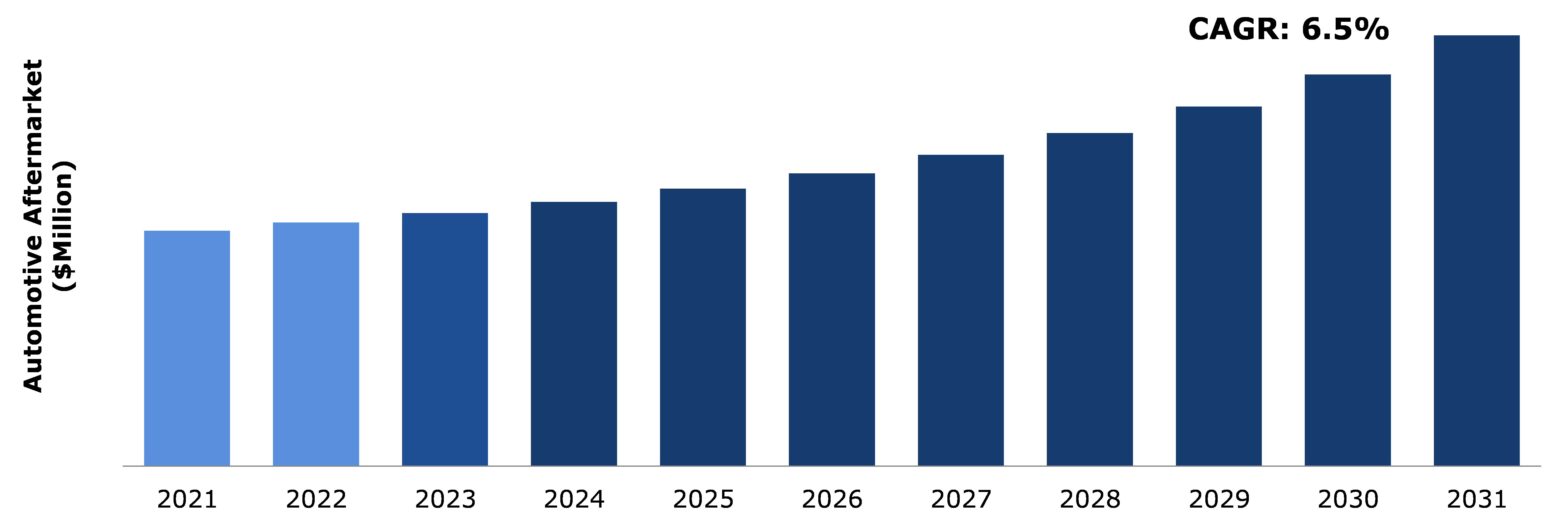

The demand for automotive parts is being driven primarily by rising in consumer awareness of maintenance and repair to improve vehicle age due to surge in consumer disposable income and demand for new vehicles with reduced fuel utilization owing to rise in government initiatives with stricter emission norms. Vehicles' average lifespan has grown due to developments in materials and manufacturing techniques. Vehicles' uncompromising quality has also increased. These factors are anticipated to boost the automotive aftermarket industry growth in the upcoming years. In addition, customers benefit from increased supplier diversity and pricing transparency as a result of the digitalization of automotive component delivery services. The surge in digitization of automotive component delivery services is expected to boost global automotive aftermarket growth.

Most consumers consider the cost of modifying a vehicle to be high. The consumers that choose to purchase the parts of the vehicles at a premium price are typically from high income group. However, the cost needs to decrease Making it more affordable for the average person. These factors hinder the automotive aftermarket growth.

Electric vehicle sales are rising globally as a result of surge in demand and stringent emission regulations for autos. The selection of electric vehicles being produced by many manufacturers is being expanded. Demand for fuel-efficient, high-performance, and low-emission automobiles has increased as a result of the increasing use of electric vehicles, and the automotive aftermarket has opportunities due to strict government emission regulations.

By region, the North America automotive aftermarket is expected to account for a dominant market share during the forecast period. Increased demand for passenger cars, the use of innovative technology in the manufacturing of auto components, and the digitization of component delivery services are all expected to drive market expansion in the region.

The automotive aftermarket is the industry that develops after the selling of original parts or components. It is sometimes known as non-OEM, generic, or competitive replacement components. While using aftermarket components might be less expensive than using OEM parts. Replacement parts and accessories are the two most frequent categories of aftermarket products. Replacement parts are real pieces of equipment that are not manufactured by the producer. Aftermarket parts are used to repair broken parts in autos and other equipment; however, they have the potential to affect the range of an insured item.

The COVID-19 pandemic has brought several uncertainties leading to severe economic losses as various businesses across the world were standstill. This has ultimately lowered the demand for automotive aftermarket had to disruptions in supply chain, closure of manufacturing plants, as well as economic slowdown across several countries. In addition, The COVID-19 pandemic was affecting several industries, however the automotive and transportation sector is among those most susceptible. The automobile aftermarket industry's supply chain and product demand are expected to be significantly impacted by COVID-19. Concern in the industry has switched from China's disruption of the supply chain to the general decline in aftermarket product demand. With the elimination of all non-essential services, it was expected that demand for commercial vehicle parts would significantly decrease. Additionally, modifications in consumer purchasing trends brought on by the pandemic's uncertainty may had a significant impact on the industry's expansion in the near future. People are now more likely to keep onto their vehicles despite economic challenges. The automotive aftermarket players are already feeling the effects of a liquidity and cash crunch that is expected to exacerbate in the next few years.

However, in February 2021, the Cooper Tire & Rubber Company took new initiative to manufacturer automotive aftermarket vehicle tyres. Cooper Tire & Rubber Company was acquired by Goodyear. In order to build a more potent U.S.-based leader in the global tire business, the combination merged two top tire firms with complementary product portfolios, services, and skills.

Original equipment manufacturers have progressively enhanced their degree of participation and emphasis inside the automotive parts aftermarket value chain. For example, they have created their own networks of repair shops that do not specialize in repairing a particular brand of automobile. In order to compete with independent aftermarket players and keep customers within their network for a longer period of time, major market players have introduced second service format and second brand such as VW direct express or remanufactured parts in an effort to keep up with the markets shift toward older vehicles. OEMs are also investing in customer experience optimization efforts and introducing differentiated aftermarket service offering.

The sensors installed in vehicles reduce the amount of wear and tear suffered by vehicles over time, particularly by the tyres and brakes that are exposed to tough driving conditions on a regular basis. This component decreases the need for replacement components, which may be damaging to the sector's growth. Furthermore, the constant R&D for new raw materials to stop the degradation of automobile components and accessories is another factor that is expected to hinder the growth of the automotive aftermarket.

The method that a consumer makes a purchase has changed due to digitization or digital influence. Customers that acquire aftermarket products read all they can, including reviews and videos. Customers are bombarded with online advertising on desktops and mobile devices every year. The industry's two fastest expanding areas are websites for wheels, tyres, and aftermarket touch-up paint. Through the use of smartphone e-commerce technologies, the aftermarket industry is thus catching up to the rest of the globe. They cost more and typically require specialists to install them properly, requiring fewer do-it-yourself mechanics (DIY). Thus, as auto parts get more complicated, there is a greater need for automotive aftermarket products.

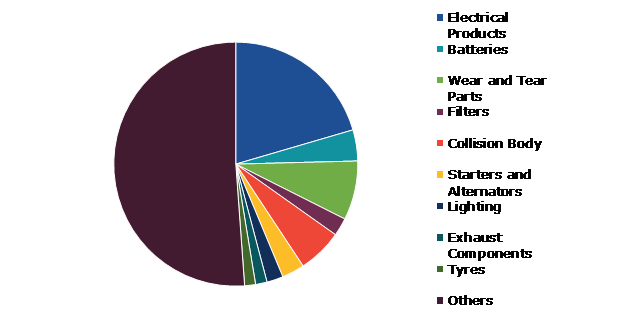

By product type, the market has been divided into electrical products, batteries, wear & tear parts, filters, collision body, starters & alternators, lighting, exhaust components, tyres, and others. Among these, the electrical products segment accounted for the highest market share in 2021 and is estimated to show the fastest growth during the forecast period.

Source: Research Dive Analysis

The electrical products segment accounted for the highest market share in 2021 and is estimated to show the fastest growth during the forecast period. The use of automotive electrical products is increasing as a result of improved vehicle safety. In order to prevent accidents, lane assist systems and adaptive cruise control are becoming prevalent and contribute for over three-tenths of all vehicle costs. The global market for automotive electrical products is also expected to rise as more consumers use infotainment systems for recreational activities. The market for automotive electrical products has been affected by makers' commercial activity due to a lack of semiconductors. The consumer electronics and personal computer industries have record-high demand, which have led to a chip scarcity in the automotive industry. Stakeholders are taking advantage of this opportunity to review their long-term supply chains.

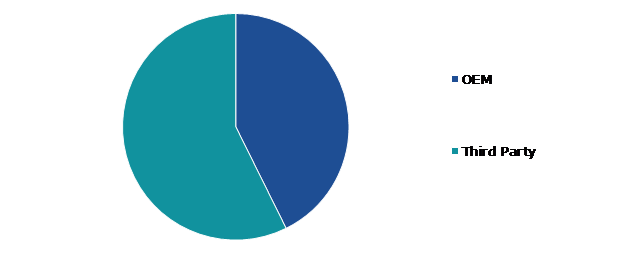

By distribution channel, the market has been bifurcated into OEM and third party. Between the two, the OEM segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The OEM segment is estimated to show the fastest growth during the forecast period. OEMs have included extra equipment in vehicles that may be upgraded in the aftermarket to suit consumers' desires for comfort and ease in transportation, which encourages the expansion of the automotive aftermarket. OEMs are enhancing and extending their aftermarket activity inside the automotive aftermarket parts value chain. The development of diverse aftermarket service options assists OEMs in improving their service repair decision-making and customer retention. OEMs' rapid development of aftermarket activity is expected to drive market expansion in the coming years.

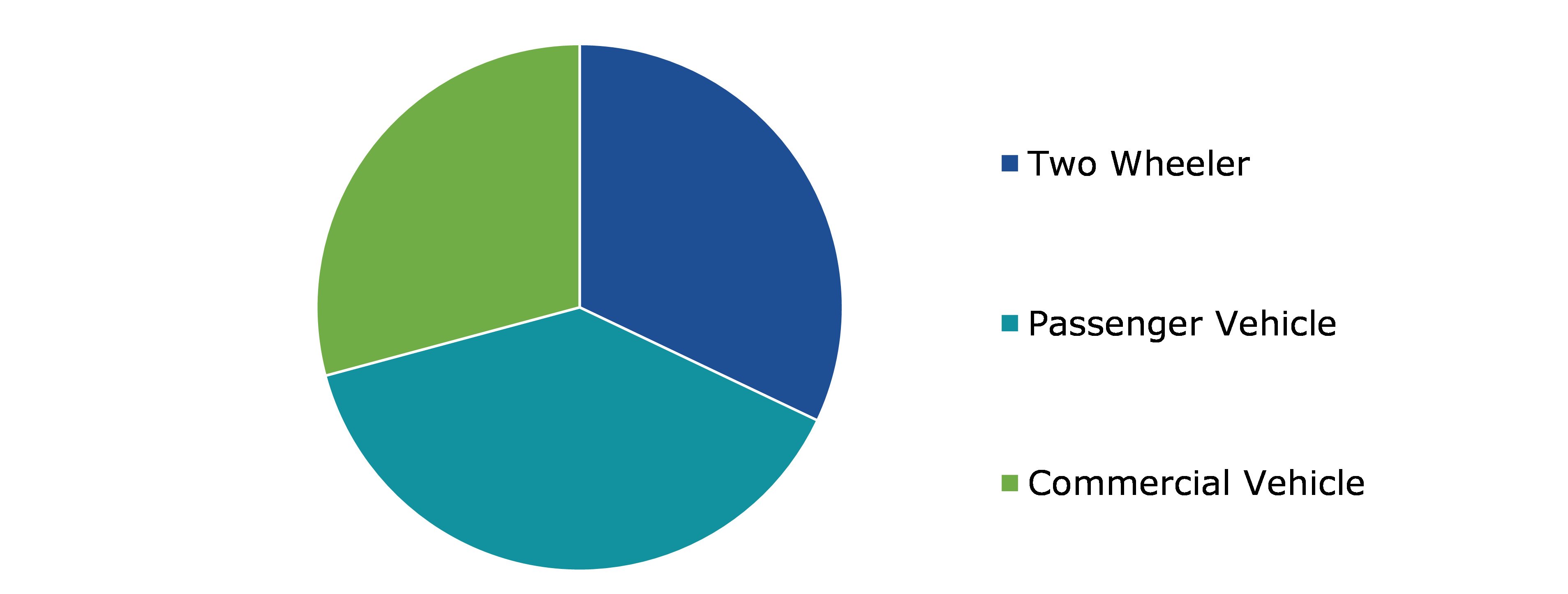

By vehicle type, the market has been divided into two-wheeler, passenger vehicle, and commercial vehicle. Among these, the passenger vehicle segment accounted for highest revenue share in 2021.

Source: Research Dive Analysis

The passenger vehicle segment accounted for the dominant market share in 2021. Customers should change various components of their vehicles at frequent intervals such as Passenger vehicles, for instance, require tire replacement every four years, depending on driving conditions. As a result, vehicle components have a sizable aftermarket. Furthermore, the aftermarket is gaining pace as a result of customer preference for installing innovative components in vehicles to improve product appearance and assure safety while driving. This increasing consumer interest leads to a rise in aftermarket servicing, which is likely to contribute to expansion in the automotive aftermarket in the near future.

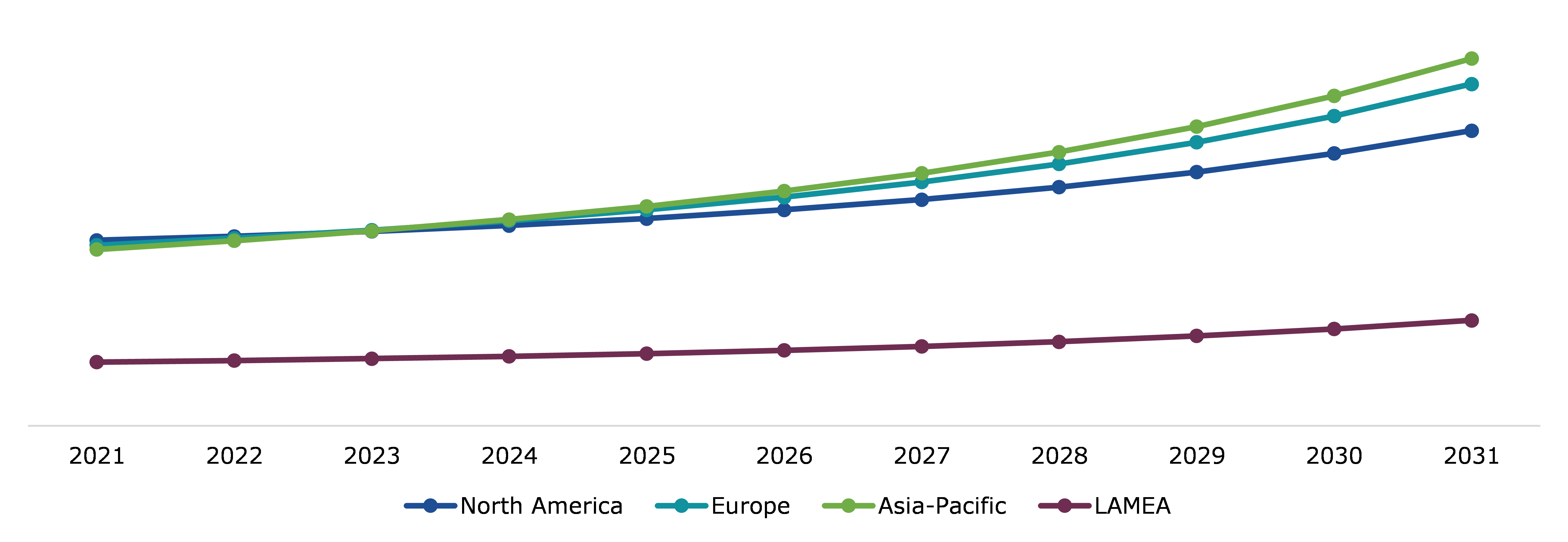

The automotive aftermarket was analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Source: Research Dive Analysis

The North America automotive aftermarket accounted a dominating market share in 2021. The increasing use of advanced technologies in the fabrication of auto parts, a rise in consumer and passenger vehicle manufacturing & sales, and increased digitization of automotive component delivery services are all factors driving the Automotive Aftermarket's growth in North America. The U.S. is anticipated to be one of the most attractive markets for aftermarket parts during the forecast period, owing to rising vehicle production and the presence of tier-1 manufacturers. Manufacturers in the U.S. concentrate on technological advances in order to produce new goods or enhance existing products for aftermarket parts, which is also one of the key factors driving market growth in North America.

Investment and agreement are common strategies followed by major market players. For instance, in October 2020, Bosch Rexroth announced a new e-commerce portal aimed to give consumers with the simplest access to select authorized Bosch Rexroth goods, including the opportunity to pay with a credit card and arrange rapid delivery.

Source: Research Dive Analysis

Some of the leading automotive aftermarket players are Alpine Electronics, Inc., Auto Zone, Inc., Bridgestone Corporation, Continental AG, Denso Corporation, Ford Motor Company, Harman International (SAMSUNG ELECTRONICS), Hella KGaA Hueck & Co., Hyundai Mobis, and Michelin.

| Aspect | Particulars |

| Historical Market Estimations | 2020-2021 |

| Base Year for Market Estimation | 2021 |

| Forecast Timeline for Market Projection | 2022-2031 |

| Regional Scope | North America, Europe, Asia-Pacific, and LAMEA |

| Segmentation by Product Type |

|

| Segmentation by Distribution Channel |

|

| Segmentation by Vehicle Type |

|

| Key Companies Profiled |

|

1.Research Methodology

1.1.Desk Research

1.2.Real time insights and validation

1.3.Forecast model

1.4.Assumptions and forecast parameters

1.5.Market size estimation

1.5.1.Top-down approach

1.5.2.Bottom-up approach

2.Report Scope

2.1.Market definition

2.2.Key objectives of the study

2.3.Report overview

2.4.Market segmentation

2.5.Overview of the impact of COVID-19 on Global automotive aftermarket

3.Executive Summary

4.Market Overview

4.1.Introduction

4.2.Growth impact forces

4.2.1.Drivers

4.2.2.Restraints

4.2.3.Opportunities

4.3.Market value chain analysis

4.3.1.List of raw material suppliers

4.3.2.List of manufacturers

4.3.3.List of distributors

4.4.Innovation & sustainability matrices

4.4.1.Technology matrix

4.4.2.Regulatory matrix

4.5.Porter’s five forces analysis

4.5.1.Bargaining power of suppliers

4.5.2.Bargaining power of consumers

4.5.3.Threat of substitutes

4.5.4.Threat of new entrants

4.5.5.Competitive rivalry intensity

4.6.PESTLE analysis

4.6.1.Political

4.6.2.Economical

4.6.3.Social

4.6.4.Technological

4.6.5.Environmental

4.7.Impact of COVID-19 on automotive aftermarket market

4.7.1.Pre-covid market scenario

4.7.2.Post-covid market scenario

5.Automotive Aftermarket Analysis, by Product Type

5.1.Overview

5.2.Electrical Products

5.2.1.Definition, key trends, growth factors, and opportunities

5.2.2.Market size analysis, by region

5.2.3.Market share analysis, by country

5.3.Batteries

5.3.1.Definition, key trends, growth factors, and opportunities

5.3.2.Market size analysis, by region

5.3.3.Market share analysis, by country

5.4.Wear and Tear Parts

5.4.1.Definition, key trends, growth factors, and opportunities

5.4.2.Market size analysis, by region

5.4.3.Market share analysis, by country

5.5.Filters

5.5.1.Definition, key trends, growth factors, and opportunities

5.5.2.Market size analysis, by region

5.5.3.Market share analysis, by country

5.6.Collision Body

5.6.1.Definition, key trends, growth factors, and opportunities

5.6.2.Market size analysis, by region

5.6.3.Market share analysis, by country

5.7.Starters and Alternators

5.7.1.Definition, key trends, growth factors, and opportunities

5.7.2.Market size analysis, by region

5.7.3.Market share analysis, by country

5.8.Lighting

5.8.1.Definition, key trends, growth factors, and opportunities

5.8.2.Market size analysis, by region

5.8.3.Market share analysis, by country

5.9.Exhaust Components

5.9.1.Definition, key trends, growth factors, and opportunities

5.9.2.Market size analysis, by region

5.9.3.Market share analysis, by country

5.10.Tires

5.10.1.Definition, key trends, growth factors, and opportunities

5.10.2.Market size analysis, by region

5.10.3.Market share analysis, by country

5.11.Others

5.11.1.Definition, key trends, growth factors, and opportunities

5.11.2.Market size analysis, by region

5.11.3.Market share analysis, by country

5.12.Research Dive Exclusive Insights

5.12.1.Market attractiveness

5.12.2.Competition heatmap

6.Automotive Aftermarket Analysis, by Distribution Channel

6.1.OEM

6.1.1.Definition, key trends, growth factors, and opportunities

6.1.2.Market size analysis, by region

6.1.3.Market share analysis, by country

6.2.Third Party

6.2.1.Definition, key trends, growth factors, and opportunities

6.2.2.Market size analysis, by region

6.2.3.Market share analysis, by country

6.3.Research Dive Exclusive Insights

6.3.1.Market attractiveness

6.3.2.Competition heatmap

7.Automotive Aftermarket Analysis, by Vehicle Type

7.1.Two-Wheeler

7.1.1.Definition, key trends, growth factors, and opportunities

7.1.2.Market size analysis, by region

7.1.3.Market share analysis, by country

7.2.Passenger Vehicle

7.2.1.Definition, key trends, growth factors, and opportunities

7.2.2.Market size analysis, by region

7.2.3.Market share analysis, by country

7.3.Commercial vehicle

7.3.1.Definition, key trends, growth factors, and opportunities

7.3.2.Market size analysis, by region

7.3.3.Market share analysis, by country

7.4.Research Dive Exclusive Insights

7.4.1.Market attractiveness

7.4.2.Competition heatmap

8.Automotive Aftermarket, by Region

8.1.North America

8.1.1.U.S.

8.1.1.1.Market size analysis, by Product Type

8.1.1.2.Market size analysis, by Distribution Channel

8.1.1.3.Market size analysis, by Vehicle Type

8.1.2.Canada

8.1.2.1.Market size analysis, by Product Type

8.1.2.2.Market size analysis, by Distribution Channel

8.1.2.3.Market size analysis, by Vehicle Type

8.1.3.Mexico

8.1.3.1.Market size analysis, by Product Type

8.1.3.2.Market size analysis, by Distribution Channel

8.1.3.3.Market size analysis, by Vehicle Type

8.1.4.Research Dive Exclusive Insights

8.1.4.1.Market attractiveness

8.1.4.2.Competition heatmap

8.2.Europe

8.2.1.Germany

8.2.1.1.Market size analysis, by Product Type

8.2.1.2.Market size analysis, by Distribution Channel

8.2.1.3.Market size analysis, by Vehicle Type

8.2.2.UK

8.2.2.1.Market size analysis, by Product Type

8.2.2.2.Market size analysis, by Distribution Channel

8.2.2.3.Market size analysis, by Vehicle Type

8.2.3.France

8.2.3.1.Market size analysis, by Product Type

8.2.3.2.Market size analysis, by Distribution Channel

8.2.3.3.Market size analysis, by Vehicle Type

8.2.4.Spain

8.2.4.1.Market size analysis, by Product Type

8.2.4.2.Market size analysis, by Distribution Channel

8.2.4.3.Market size analysis, by Vehicle Type

8.2.5.Italy

8.2.5.1.Market size analysis, by Product Type

8.2.5.2.Market size analysis, by Distribution Channel

8.2.5.3.Market size analysis, by Vehicle Type

8.2.6.Rest of Europe

8.2.6.1.Market size analysis, by Product Type

8.2.6.2.Market size analysis, by Distribution Channel

8.2.6.3.Market size analysis, by Vehicle Type

8.2.7.Research Dive Exclusive Insights

8.2.7.1.Market attractiveness

8.2.7.2.Competition heatmap

8.3.Asia-Pacific

8.3.1.China

8.3.1.1.Market size analysis, by Product Type

8.3.1.2.Market size analysis, by Distribution Channel

8.3.1.3.Market size analysis, by Vehicle Type

8.3.2.Japan

8.3.2.1.Market size analysis, by Product Type

8.3.2.2.Market size analysis, by Distribution Channel

8.3.2.3.Market size analysis, by Vehicle Type

8.3.3.India

8.3.3.1.Market size analysis, by Product Type

8.3.3.2.Market size analysis, by Distribution Channel

8.3.3.3.Market size analysis, by Vehicle Type

8.3.4.Australia

8.3.4.1.Market size analysis, by Product Type

8.3.4.2.Market size analysis, by Distribution Channel

8.3.4.3.Market size analysis, by Vehicle Type

8.3.5.South Korea

8.3.5.1.Market size analysis, by Product Type

8.3.5.2.Market size analysis, by Distribution Channel

8.3.5.3.Market size analysis, by Vehicle Type

8.3.6.Rest of Asia Pacific

8.3.6.1.Market size analysis, by Product Type

8.3.6.2.Market size analysis, by Distribution Channel

8.3.6.3.Market size analysis, by Vehicle Type

8.3.7.Research Dive Exclusive Insights

8.3.7.1.Market attractiveness

8.3.7.2.Competition heatmap

8.4.LAMEA

8.4.1.Brazil

8.4.1.1.Market size analysis, by Product Type

8.4.1.2.Market size analysis, by Distribution Channel

8.4.1.3.Market size analysis, by Vehicle Type

8.4.2.Saudi Arabia

8.4.2.1.Market size analysis, by Product Type

8.4.2.2.Market size analysis, by Distribution Channel

8.4.2.3.Market size analysis, by Vehicle Type

8.4.3.UAE

8.4.3.1.Market size analysis, by Product Type

8.4.3.2.Market size analysis, by Distribution Channel

8.4.3.3.Market size analysis, by Vehicle Type

8.4.4.South Africa

8.4.4.1.Market size analysis, by Product Type

8.4.4.2.Market size analysis, by Distribution Channel

8.4.4.3.Market size analysis, by Vehicle Type

8.4.5.Rest of LAMEA

8.4.5.1.Market size analysis, by Product Type

8.4.5.2.Market size analysis, by Distribution Channel

8.4.5.3.Market size analysis, by Vehicle Type

8.4.6.Research Dive Exclusive Insights

8.4.6.1.Market attractiveness

8.4.6.2.Competition heatmap

9.Competitive Landscape

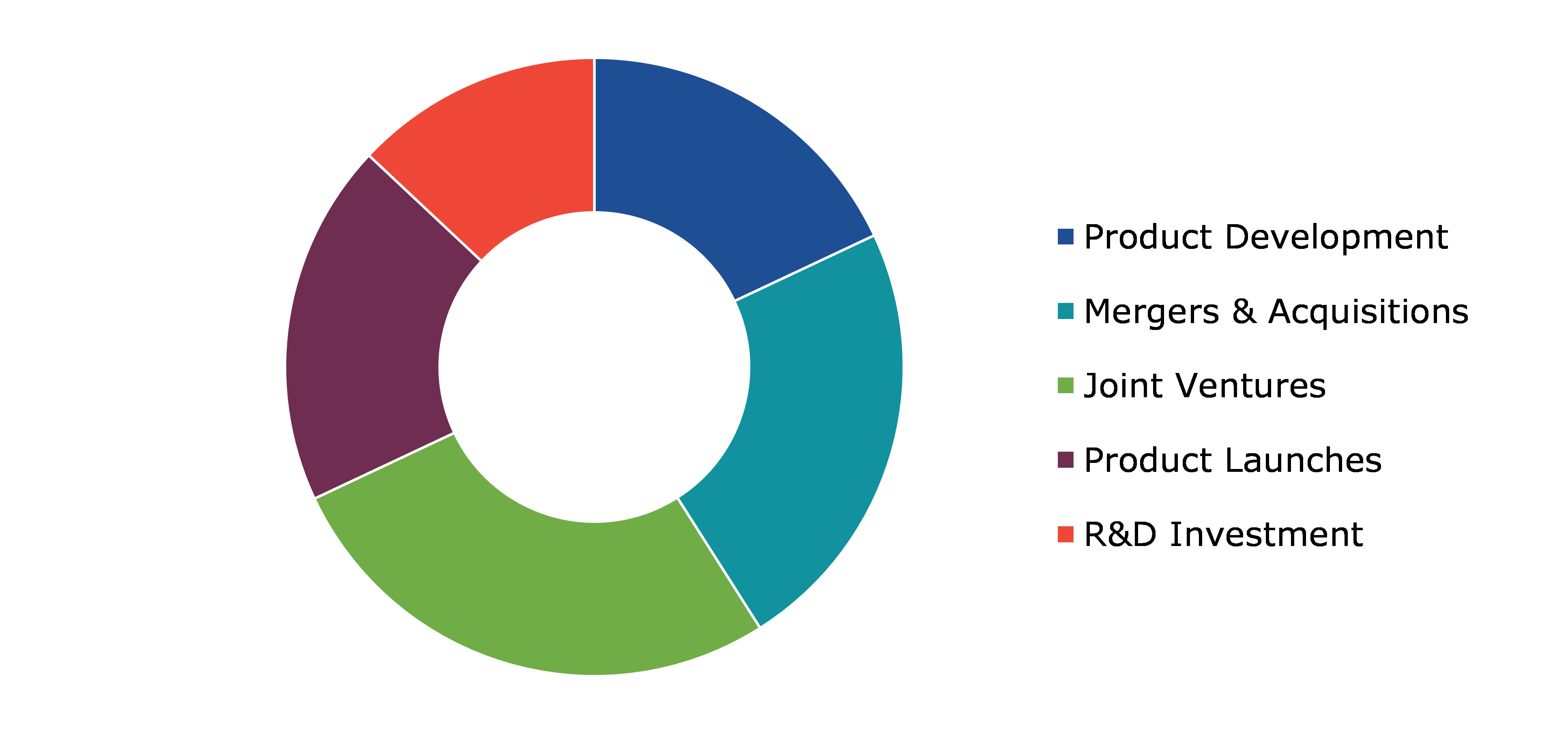

9.1.Top winning strategies, 2021

9.1.1.By strategy

9.1.2.By year

9.2.Strategic overview

9.3.Market share analysis, 2021

10.Company Profiles

10.1.Alpine Electronics, Inc.

10.1.1.Overview

10.1.2.Business segments

10.1.3.Product portfolio

10.1.4.Financial performance

10.1.5.Recent developments

10.1.6.SWOT analysis

10.2.Auto Zone, Inc.

10.2.1.Overview

10.2.2.Business segments

10.2.3.Product portfolio

10.2.4.Financial performance

10.2.5.Recent developments

10.2.6.SWOT analysis

10.3.Bridgestone Corporation

10.3.1.Overview

10.3.2.Business segments

10.3.3.Product portfolio

10.3.4.Financial performance

10.3.5.Recent developments

10.3.6.SWOT analysis

10.4.Continental AG

10.4.1.Overview

10.4.2.Business segments

10.4.3.Product portfolio

10.4.4.Financial performance

10.4.5.Recent developments

10.4.6.SWOT analysis

10.5.Denso Corporation

10.5.1.Overview

10.5.2.Business segments

10.5.3.Product portfolio

10.5.4.Financial performance

10.5.5.Recent developments

10.5.6.SWOT analysis

10.6.Ford Motor Company

10.6.1.Overview

10.6.2.Business segments

10.6.3.Product portfolio

10.6.4.Financial performance

10.6.5.Recent developments

10.6.6.SWOT analysis

10.7.Harman International (SAMSUNG ELECTRONICS)

10.7.1.Overview

10.7.2.Business segments

10.7.3.Product portfolio

10.7.4.Financial performance

10.7.5.Recent developments

10.7.6.SWOT analysis

10.8.Hella KGaA Hueck & Co.

10.8.1.Overview

10.8.2.Business segments

10.8.3.Product portfolio

10.8.4.Financial performance

10.8.5.Recent developments

10.8.6.SWOT analysis

10.9.Hyundai Mobis

10.9.1.Overview

10.9.2.Business segments

10.9.3.Product portfolio

10.9.4.Financial performance

10.9.5.Recent developments

10.9.6.SWOT analysis

10.10.Michelin

10.10.1.Overview

10.10.2.Business segments

10.10.3.Product portfolio

10.10.4.Financial performance

10.10.5.Recent developments

10.10.6.SWOT analysis

* Taxes/Fees, If applicable will be added during checkout. All prices in USD.

Have a question ?

Enquire To BuyNeed to add more ?

Request Customization

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}